Marine Seismic Equipment and Acquisition Market

Marine Seismic Equipment and Acquisition Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705309 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

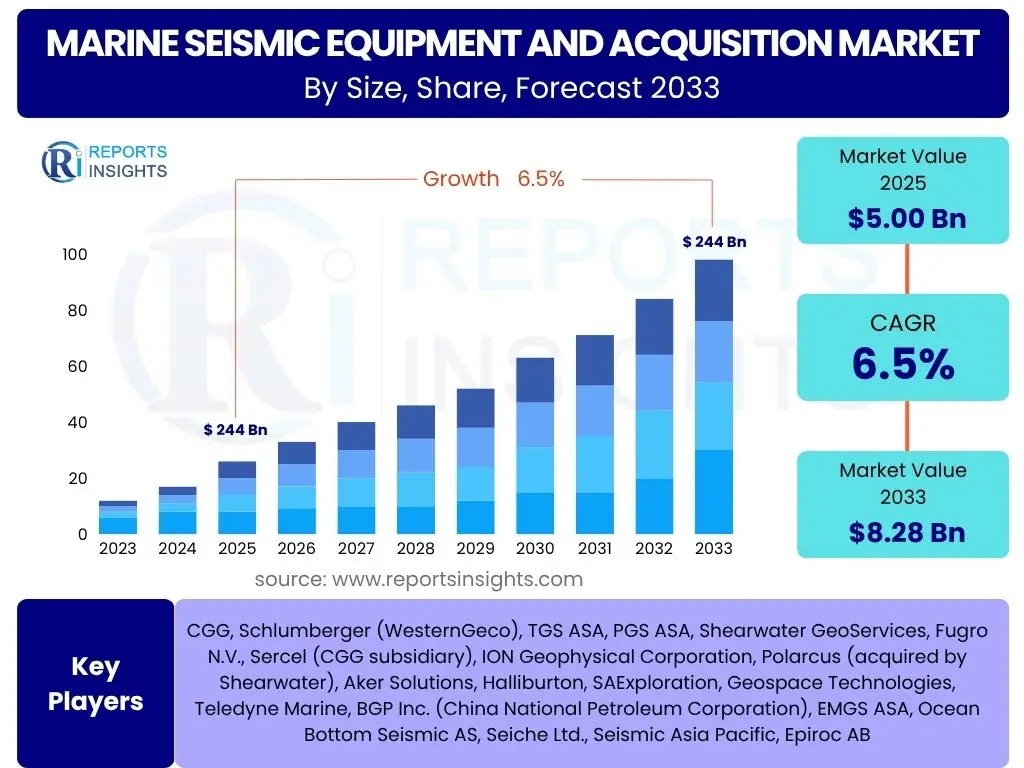

Marine Seismic Equipment and Acquisition Market Size

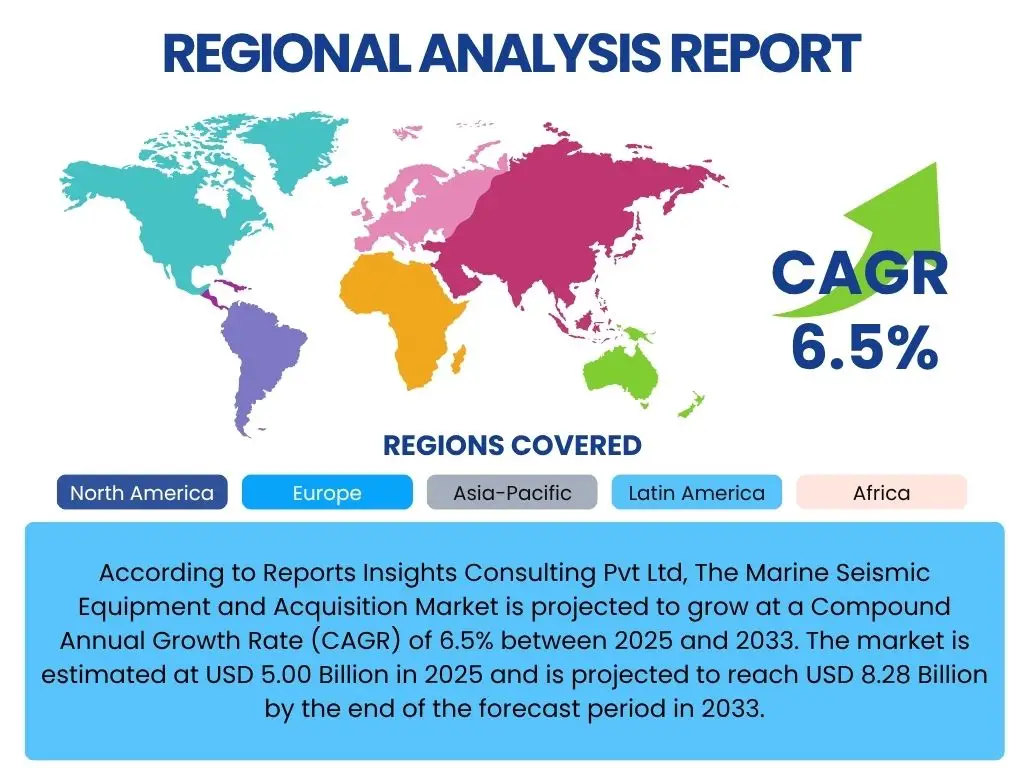

According to Reports Insights Consulting Pvt Ltd, The Marine Seismic Equipment and Acquisition Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 5.00 Billion in 2025 and is projected to reach USD 8.28 Billion by the end of the forecast period in 2033.

Key Marine Seismic Equipment and Acquisition Market Trends & Insights

User inquiries frequently focus on the evolving technological landscape, the shift in application areas, and the increasing emphasis on environmental sustainability within the marine seismic equipment and acquisition sector. There is significant interest in how advanced data processing techniques, such as those leveraging artificial intelligence and machine learning, are transforming the efficiency and accuracy of seismic surveys. Furthermore, users are keen to understand the market's diversification beyond traditional oil and gas exploration, particularly into renewable energy projects like offshore wind and emerging applications such as carbon capture and storage (CCS) site characterization. The demand for higher resolution data and faster turnaround times is a recurring theme, highlighting the industry's drive towards greater operational efficacy.

Another prevalent area of user concern revolves around the methods and technologies employed to minimize the environmental footprint of marine seismic operations. Questions often arise regarding the impact on marine life, the adoption of quieter seismic sources, and the adherence to stricter regulatory frameworks. This reflects a growing industry awareness and stakeholder pressure to balance energy resource development with ecological preservation. The integration of autonomous or semi-autonomous marine vessels and remotely operated vehicles (ROVs) for data acquisition is also a topic of high interest, indicating a broader trend towards automation and reducing human exposure to hazardous environments, while simultaneously enhancing survey capabilities.

Finally, there is a clear interest in the economics of marine seismic, including the cost-effectiveness of new technologies and the long-term investment outlook for equipment and acquisition services. The demand for multi-client seismic data libraries is gaining traction as companies seek to optimize exploration budgets and access pre-existing, high-quality data. This trend reflects a broader shift towards collaborative data sharing and a more strategic approach to exploration and development, driven by the need for efficiency and reduced risk in capital-intensive offshore projects. These multifaceted trends underscore a dynamic market that is rapidly adapting to new energy paradigms, technological advancements, and stringent environmental mandates.

- Shift Towards Ocean Bottom Seismic (OBS) and Node-Based Systems: Increasing adoption for superior data quality in complex geological settings.

- Growth of Multi-Client Seismic Libraries: Cost-effective data solutions reducing individual company exploration risks.

- Integration of Advanced Data Analytics and Artificial Intelligence (AI): Enhancing data processing, interpretation, and predictive capabilities.

- Diversification into Renewable Energy and Carbon Capture and Storage (CCS): Growing demand for site characterization for offshore wind farms and CO2 storage.

- Focus on Environmental Stewardship and Low-Impact Technologies: Development of quieter sources and techniques to minimize marine life disruption.

- Increasing Adoption of Autonomous and Remote Operations: Improving safety, efficiency, and data acquisition capabilities.

AI Impact Analysis on Marine Seismic Equipment and Acquisition

User queries regarding the impact of AI on marine seismic equipment and acquisition frequently center on its potential to revolutionize data processing and interpretation. Users are keen to understand how AI algorithms can accelerate the analysis of vast datasets, identify subtle geological features, and reduce human error, thereby leading to more accurate and efficient subsurface imaging. There is also significant interest in AI's role in optimizing survey design and execution, including real-time quality control and predictive maintenance for seismic equipment, which could translate into substantial cost savings and operational efficiencies. The expectation is that AI will move beyond mere automation to provide deeper insights, enabling better decision-making in exploration and production workflows.

Another area of focus for users is the application of AI in enhancing the safety and autonomy of marine seismic operations. Questions arise about AI-powered navigation systems for seismic vessels, autonomous underwater vehicles (AUVs) for data acquisition, and intelligent monitoring systems that can detect potential hazards or equipment malfunctions proactively. The potential for AI to reduce human presence in high-risk offshore environments and improve overall operational safety is a significant draw. However, alongside these positive expectations, users also express concerns about the reliability of AI systems in critical applications, the need for robust cybersecurity measures, and the potential impact on workforce skills and employment.

Furthermore, the discussion often extends to the long-term implications of AI for the marine seismic industry's competitive landscape. Users are interested in how early adoption of AI technologies might create a competitive advantage, how data ownership and intellectual property will be managed in an AI-driven environment, and the challenges associated with integrating legacy systems with new AI platforms. The demand for high-quality, labeled datasets to train AI models is a recognized prerequisite, prompting questions about data standardization and sharing practices across the industry. Overall, AI is viewed as a transformative force, promising unprecedented levels of efficiency and insight, while simultaneously presenting new challenges related to implementation, ethical considerations, and workforce adaptation.

- Enhanced Data Processing and Interpretation: AI algorithms accelerate analysis, identify subtle features, and improve seismic image resolution.

- Optimized Survey Planning and Execution: AI enables real-time adjustments, predictive maintenance, and efficient resource allocation for seismic operations.

- Improved Anomaly Detection and Risk Assessment: Machine learning identifies potential geohazards and subsurface risks more accurately.

- Development of Autonomous Operations: AI facilitates autonomous seismic vessels and AUVs, reducing human exposure and increasing efficiency.

- Predictive Maintenance for Equipment: AI models forecast equipment failures, minimizing downtime and operational costs.

- New Business Models: AI supports multi-client data libraries and advanced analytics services, creating new revenue streams.

Key Takeaways Marine Seismic Equipment and Acquisition Market Size & Forecast

User inquiries concerning the key takeaways from the marine seismic equipment and acquisition market size and forecast consistently highlight the market's resilience and adaptive capacity in a fluctuating energy landscape. A primary insight is the market's continued growth, driven by an ongoing global demand for energy, which necessitates both conventional hydrocarbon exploration and significant investment in renewable energy infrastructure. The forecast indicates a steady expansion, primarily propelled by technological advancements that enhance the efficiency, accuracy, and environmental sustainability of seismic operations. This underlines a market that is not just reacting to external pressures but proactively innovating to meet evolving industry standards and energy transition goals.

Another crucial takeaway frequently sought by users pertains to the evolving application spectrum of marine seismic technology. While oil and gas exploration remains a foundational driver, the increasing significance of offshore wind farm development and carbon capture and storage (CCS) projects is profoundly reshaping market dynamics. These new applications are creating substantial demand for specialized seismic surveys focused on site characterization, geohazard assessment, and reservoir monitoring. This diversification is critical for market stability and long-term growth, as it mitigates dependency on a single energy sector and opens up new avenues for equipment manufacturers and service providers alike.

Finally, a key insight is the profound influence of geopolitical factors, environmental regulations, and capital expenditure trends on regional market performance. Users are keen to understand which geographies offer the most promising growth prospects, often linked to new exploration rounds, renewable energy targets, or strategic national energy security initiatives. The competitive landscape is also a significant point of interest, with consolidation and strategic partnerships emerging as prevalent strategies to navigate market complexities. These factors collectively indicate a market that, while poised for growth, requires continuous innovation, strategic adaptability, and a keen awareness of both global energy policy shifts and localized demand drivers to succeed.

- Sustained Growth Trajectory: The market is projected for consistent growth, driven by global energy demand and technological innovation.

- Diversifying Applications: Significant expansion into offshore wind, carbon capture and storage (CCS), and geohazard assessment.

- Technological Advancements as Core Drivers: Continuous innovation in data acquisition (e.g., OBN), processing (AI/ML), and interpretation.

- Increased Focus on Environmental Sustainability: Regulatory pressures and corporate responsibility drive demand for low-impact seismic solutions.

- Regional Market Shifts: Growth influenced by specific energy policies, exploration activities, and renewable energy investments in different geographies.

- Capital-Intensive Industry: High investment in R&D and equipment remains a key characteristic, impacting market entry and consolidation.

Marine Seismic Equipment and Acquisition Market Drivers Analysis

The Marine Seismic Equipment and Acquisition Market is primarily driven by the persistent global demand for energy, necessitating continued exploration and development of offshore hydrocarbon reserves. Despite a global push towards renewable energy, oil and natural gas continue to form a significant portion of the world's energy mix, particularly in developing economies. This sustained demand fuels investment in offshore exploration, especially in deepwater and ultra-deepwater areas where significant untapped resources are believed to exist. The need for advanced seismic data to accurately identify and characterize these complex reservoirs is a fundamental driver for both equipment sales and acquisition services.

Beyond traditional oil and gas, the burgeoning offshore renewable energy sector, particularly offshore wind, represents a substantial new driver for the marine seismic market. The planning, construction, and operation of offshore wind farms require extensive seismic surveys for site characterization, foundation design, and geohazard assessment to ensure structural integrity and operational safety. Similarly, the growing global focus on carbon capture and storage (CCS) initiatives necessitates detailed seismic imaging to identify suitable geological formations for CO2 sequestration and to monitor stored CO2 plumes over time, ensuring long-term containment. These diversified applications expand the addressable market for seismic technologies, providing new revenue streams and fostering innovation.

Technological advancements also play a critical role in propelling market growth. Innovations in seismic acquisition techniques, such as the increasing adoption of Ocean Bottom Nodes (OBN) for superior data quality in challenging environments, and the development of 4D seismic for reservoir monitoring, enhance the value proposition of seismic services. Furthermore, improvements in data processing capabilities, including the integration of artificial intelligence and machine learning algorithms, enable faster and more accurate interpretation of complex seismic data. These technological strides not only improve efficiency and reduce operational costs but also open up new possibilities for subsurface imaging, thereby sustaining the demand for cutting-edge equipment and services.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Energy Demand & Offshore Exploration | +1.5% | North America (Gulf of Mexico), Latin America (Brazil), West Africa, Asia Pacific (Southeast Asia) | Long-term (5+ years) |

| Growth in Offshore Wind Energy Projects | +1.2% | Europe (North Sea), North America (East Coast), Asia Pacific (Japan, South Korea) | Mid-term (3-7 years) |

| Increased Investment in Carbon Capture & Storage (CCS) | +0.8% | North America, Europe, Australia | Mid-to-Long-term (4-8 years) |

| Technological Advancements in Seismic Imaging | +1.0% | Global | Ongoing (Short-to-Long-term) |

| Demand for High-Resolution 4D Seismic Data | +0.7% | Mature Basins (North Sea, Gulf of Mexico), Deepwater Fields | Mid-term (3-6 years) |

Marine Seismic Equipment and Acquisition Market Restraints Analysis

The Marine Seismic Equipment and Acquisition Market faces significant restraints primarily due to the inherent volatility and fluctuations in global crude oil and natural gas prices. When commodity prices are low, oil and gas companies tend to reduce their exploration and production (E&P) expenditures, leading to a decrease in demand for seismic surveys and equipment. This direct correlation makes the market susceptible to geopolitical events, supply-demand imbalances, and broader economic downturns that impact energy prices. The long-term nature of seismic investments clashes with the short-term unpredictability of oil prices, often resulting in deferred projects and reduced activity, thereby dampening market growth.

Stringent environmental regulations and growing public opposition to seismic activities, particularly concerning their potential impact on marine life, represent another major restraint. Regulatory bodies worldwide are imposing stricter guidelines on noise levels, operational timing, and mitigation measures, increasing the complexity and cost of seismic surveys. Environmental impact assessments (EIAs) are becoming more rigorous, sometimes leading to project delays or cancellations. This heightened scrutiny and the associated legal and compliance burdens compel companies to invest in more expensive, quieter technologies or restrict operations to specific windows, directly affecting profitability and operational scope within the market.

Furthermore, the high capital expenditure required for marine seismic equipment and vessels acts as a substantial barrier to entry for new players and limits the ability of existing companies to rapidly scale or modernize their fleets. The acquisition of advanced seismic vessels, specialized equipment like Ocean Bottom Nodes, and sophisticated data processing software involves considerable upfront investment. This capital-intensive nature means that companies must secure long-term contracts and maintain high utilization rates to ensure return on investment. In an environment characterized by fluctuating demand and intense competition, the financial burden of maintaining and upgrading a state-of-the-art seismic fleet can be a significant impediment to sustained market growth and innovation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Crude Oil and Natural Gas Prices | -1.5% | Global | Short-to-Mid-term (1-5 years) |

| Stringent Environmental Regulations and Public Opposition | -1.0% | Europe, North America, Arctic Regions | Long-term (5+ years) |

| High Capital Expenditure and Operating Costs | -0.8% | Global | Ongoing |

| Geopolitical Instability and Sanctions | -0.7% | Specific conflict zones, Russia, Middle East | Short-to-Mid-term (1-4 years) |

| Risk of Project Delays or Cancellations | -0.5% | Global | Short-to-Mid-term (1-3 years) |

Marine Seismic Equipment and Acquisition Market Opportunities Analysis

Significant opportunities in the Marine Seismic Equipment and Acquisition Market stem from the rapidly expanding global investment in offshore renewable energy, particularly offshore wind. As nations worldwide commit to decarbonization targets, the development of offshore wind farms requires extensive preliminary seismic surveys for site assessment, foundation design, and geohazard identification. This represents a burgeoning new application area, providing a stable and growing demand base for high-resolution 2D and 3D seismic data, distinct from the more volatile oil and gas sector. Companies that can adapt their equipment and expertise to meet the specific requirements of the offshore wind industry stand to gain a considerable competitive advantage and secure long-term contracts, diversifying their revenue streams.

The increasing focus on Carbon Capture and Storage (CCS) projects also presents a substantial opportunity for market growth. CCS technology is crucial for achieving net-zero emissions, and its implementation relies heavily on detailed geological characterization to identify suitable subsurface reservoirs for CO2 injection and long-term storage. Marine seismic technology is indispensable for both the initial site selection and the subsequent monitoring of injected CO2 plumes to ensure containment and detect any leakage. As more industrial emitters explore CCS solutions, the demand for specialized seismic surveys and monitoring services will expand significantly, creating a specialized niche for seismic providers with expertise in reservoir monitoring and environmental compliance.

Furthermore, technological innovation, particularly in data processing and analytics, opens up new market opportunities. The integration of artificial intelligence (AI) and machine learning (ML) allows for more efficient, accurate, and rapid interpretation of complex seismic data, enhancing the value proposition of seismic services. The development of advanced seismic sources that minimize environmental impact, along with autonomous or semi-autonomous data acquisition systems, can lead to reduced operational costs and improved survey capabilities. Companies that invest in these cutting-edge technologies and offer integrated solutions, from data acquisition to advanced interpretation, will be well-positioned to capture a larger share of the evolving market, catering to clients seeking not just data, but actionable insights and sustainable practices.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Offshore Wind Farm Development | +1.8% | Europe (North Sea, Baltic Sea), North America (US East Coast), Asia Pacific (Taiwan, Japan, South Korea) | Long-term (5+ years) |

| Carbon Capture and Storage (CCS) Projects | +1.4% | North America, Europe, Australia, Norway | Mid-to-Long-term (4-8 years) |

| Technological Advancement (AI/ML, Autonomous Systems) | +1.0% | Global | Ongoing (Short-to-Long-term) |

| Expansion of Multi-Client Seismic Programs | +0.9% | Emerging Basins, Frontier Areas (e.g., Brazil, West Africa) | Mid-term (3-6 years) |

| Deepwater and Frontier Exploration | +0.7% | Latin America, West Africa, Arctic (selectively) | Mid-term (3-7 years) |

Marine Seismic Equipment and Acquisition Market Challenges Impact Analysis

The Marine Seismic Equipment and Acquisition Market faces significant challenges stemming from the inherently high operational risks associated with offshore activities. These risks include unpredictable weather conditions, equipment malfunctions in harsh marine environments, and the logistical complexities of deploying and maintaining large-scale seismic spreads. Ensuring the safety of personnel and equipment while adhering to strict environmental and operational protocols adds layers of complexity and cost. Furthermore, managing the cybersecurity risks associated with increasingly digitalized operations and sensitive data is a growing concern, demanding robust infrastructure and continuous vigilance to protect proprietary information and prevent operational disruptions.

Another major challenge is the intense price competition and oversupply of seismic vessels and equipment that periodically characterize the market. Periods of reduced demand for seismic services, often linked to oil price downturns, can lead to a surplus of available assets, driving down day rates and profit margins for seismic companies. This creates significant financial pressure, making it difficult for companies to justify new investments in equipment upgrades or fleet expansion. The cyclical nature of the industry and the high fixed costs associated with maintaining a seismic fleet exacerbate these challenges, leading to consolidation and rationalization within the sector as companies struggle to maintain profitability.

Finally, attracting and retaining skilled labor presents a persistent challenge for the marine seismic industry. The highly specialized nature of seismic operations requires personnel with expertise in geophysics, marine engineering, data science, and advanced analytics. However, the cyclical nature of the industry, combined with the often remote and demanding work environment, makes it difficult to consistently attract young talent and retain experienced professionals. The shift towards automation and AI also necessitates continuous upskilling of the existing workforce, adding to training costs and creating a potential skills gap. Addressing this talent deficit is critical for ensuring the long-term operational capabilities and innovative capacity of the marine seismic equipment and acquisition market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition and Market Oversupply | -1.3% | Global | Ongoing (Short-to-Mid-term) |

| High Operational Risks and Cybersecurity Threats | -0.9% | Global | Ongoing |

| Skilled Labor Shortages and Talent Retention | -0.8% | Global | Long-term (5+ years) |

| Navigating Evolving Regulatory Landscape | -0.7% | Regional (Europe, Arctic) | Ongoing |

| Integration of New Technologies with Legacy Systems | -0.6% | Global | Mid-term (3-7 years) |

Marine Seismic Equipment and Acquisition Market - Updated Report Scope

This comprehensive report delves into the Marine Seismic Equipment and Acquisition Market, offering an in-depth analysis of its current size, historical performance, and future growth projections through 2033. It meticulously examines key market trends, drivers, restraints, opportunities, and challenges shaping the industry landscape. The report provides detailed segmentation analysis by equipment type, acquisition type, deployment method, and application, alongside a thorough regional assessment to highlight growth hotspots. Furthermore, it includes an impact analysis of artificial intelligence on market dynamics and profiles leading companies, offering a holistic view for stakeholders seeking strategic insights and investment opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.00 Billion |

| Market Forecast in 2033 | USD 8.28 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CGG, Schlumberger (WesternGeco), TGS ASA, PGS ASA, Shearwater GeoServices, Fugro N.V., Sercel (CGG subsidiary), ION Geophysical Corporation, Polarcus (acquired by Shearwater), Aker Solutions, Halliburton, SAExploration, Geospace Technologies, Teledyne Marine, BGP Inc. (China National Petroleum Corporation), EMGS ASA, Ocean Bottom Seismic AS, Seiche Ltd., Seismic Asia Pacific, Epiroc AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Marine Seismic Equipment and Acquisition Market is comprehensively segmented to provide a granular view of its diverse components and applications. This segmentation highlights the various types of equipment utilized, the methodologies employed for data acquisition, the deployment strategies, and the specific end-use applications driving demand across different sectors. Understanding these segments is crucial for identifying niche markets, assessing technological shifts, and formulating targeted business strategies. The detailed breakdown reflects the evolving landscape of marine seismic activities, from traditional hydrocarbon exploration to the growing significance of renewable energy and environmental monitoring projects. Each segment offers distinct opportunities and challenges, influencing market dynamics and competitive positioning.

- By Equipment Type: This segment includes a wide array of specialized equipment such as streamers (for towed seismic surveys), various seismic sources (like air guns and marine vibrators), geophones and hydrophones (for detecting seismic waves), data recorders, specialized seismic vessels, navigation systems, and advanced data processing workstations. The demand for specific equipment types is often driven by the nature of the survey, water depth, and target resolution requirements.

- By Acquisition Type: This categorization covers the different dimensional approaches to seismic data collection, including 2D seismic (single line surveys), 3D seismic (volumetric surveys for detailed subsurface imaging), and 4D seismic (repeated 3D surveys over time to monitor changes in reservoirs). Ocean Bottom Seismic (OBS), encompassing both Ocean Bottom Nodes (OBN) and Ocean Bottom Cables (OBC), is also a crucial acquisition type, preferred for complex geological settings and superior data quality.

- By Deployment: This segment focuses on how equipment is deployed in the marine environment. Towed streamer deployment involves vessels towing long cables with hydrophones. Ocean Bottom Node (OBN) and Ocean Bottom Cable (OBC) deployments involve placing sensors directly on the seabed, offering advantages in congested areas or for multi-component data acquisition.

- By Application: This vital segment illustrates the end-use industries driving market demand. Key applications include traditional oil and gas exploration and production, geohazard assessment (for pipeline routes or platform installations), renewable energy projects (primarily offshore wind site characterization), carbon capture and storage (CCS) for reservoir identification and monitoring, and scientific research. Each application has unique requirements for seismic data resolution and coverage.

Regional Highlights

- North America: This region is a significant market driven by ongoing oil and gas exploration in the Gulf of Mexico and increasing investments in offshore wind projects along the East Coast. Technological innovation and strategic partnerships are prevalent.

- Europe: A mature market with strong emphasis on environmental regulations. It is a leader in offshore wind energy development in the North Sea and Baltic Sea, driving demand for site characterization seismic. Also active in CCS pilot projects.

- Asia Pacific (APAC): Expected to be one of the fastest-growing regions due to rising energy demand, new exploration activities in deepwater basins (e.g., Southeast Asia, Australia), and burgeoning offshore wind energy markets (e.g., Taiwan, Japan, South Korea).

- Latin America: Driven by substantial oil and gas reserves, particularly in Brazil's pre-salt region, and ongoing exploration efforts in countries like Guyana and Suriname. Investment decisions here heavily influence market activity.

- Middle East and Africa (MEA): Remains a crucial region for conventional oil and gas exploration and production, with significant ongoing and planned projects. West Africa, in particular, continues to attract seismic investments for frontier and deepwater exploration.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Marine Seismic Equipment and Acquisition Market.- CGG

- Schlumberger (WesternGeco)

- TGS ASA

- PGS ASA

- Shearwater GeoServices

- Fugro N.V.

- Sercel (CGG subsidiary)

- ION Geophysical Corporation

- Aker Solutions

- Halliburton

- SAExploration

- Geospace Technologies

- Teledyne Marine

- BGP Inc. (China National Petroleum Corporation)

- EMGS ASA

- Ocean Bottom Seismic AS

- Seiche Ltd.

- Seismic Asia Pacific

- Epiroc AB

- Kongsberg Gruppen

Frequently Asked Questions

What is marine seismic equipment and acquisition?

Marine seismic equipment and acquisition refer to specialized tools and methods used to image the subsurface geology beneath the ocean floor. This typically involves deploying seismic sources (like air guns) to generate acoustic waves that travel through the water and rock layers, and then using receivers (like hydrophones or geophones on streamers or ocean bottom nodes) to detect the reflected waves. The acquired data is then processed and interpreted to create detailed maps of underground geological structures, which are critical for various applications.

Why is marine seismic important for the energy industry?

Marine seismic technology is crucial for the energy industry as it provides essential data for identifying and evaluating potential hydrocarbon reservoirs beneath the seabed. Accurate seismic imaging helps oil and gas companies make informed decisions about exploration drilling, reservoir development, and production optimization. Beyond traditional hydrocarbons, it is increasingly vital for site characterization for offshore wind farms and for identifying suitable geological formations for carbon capture and storage (CCS) projects, supporting the global energy transition.

How is marine seismic data used in offshore wind farm development?

In offshore wind farm development, marine seismic data is used for detailed site characterization. This involves mapping the seafloor and shallow subsurface geology to identify suitable locations for turbine foundations, assess ground conditions, and detect potential geohazards such as shallow gas pockets, faults, or unstable sediments. This information is critical for engineering design, risk mitigation, and ensuring the long-term stability and safety of the wind farm infrastructure.

What are the key environmental concerns associated with marine seismic surveys?

The primary environmental concerns associated with marine seismic surveys relate to the potential impact of acoustic energy (sound) on marine life. High-intensity sounds from seismic sources, particularly air guns, can potentially disturb, injure, or displace marine mammals and fish. Industry efforts and regulatory frameworks focus on mitigation measures such as "soft-starts" (gradually increasing sound levels), operational exclusion zones, and the development of quieter seismic technologies like marine vibrators or alternative sources to minimize these impacts and ensure responsible operations.

What are the latest technological advancements in marine seismic equipment?

Recent technological advancements in marine seismic equipment include the widespread adoption of Ocean Bottom Node (OBN) technology, which offers superior data quality in complex geological settings and challenging environments compared to traditional towed streamers. There is also a significant trend towards integrating artificial intelligence (AI) and machine learning (ML) for faster and more accurate data processing and interpretation. Furthermore, advancements in autonomous underwater vehicles (AUVs) and remote operation capabilities are enhancing survey efficiency, safety, and reducing the environmental footprint of operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted