Temporary Adhesive Tape for Semiconductor Manufacturing Market

Temporary Adhesive Tape for Semiconductor Manufacturing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702149 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Temporary Adhesive Tape for Semiconductor Manufacturing Market Size

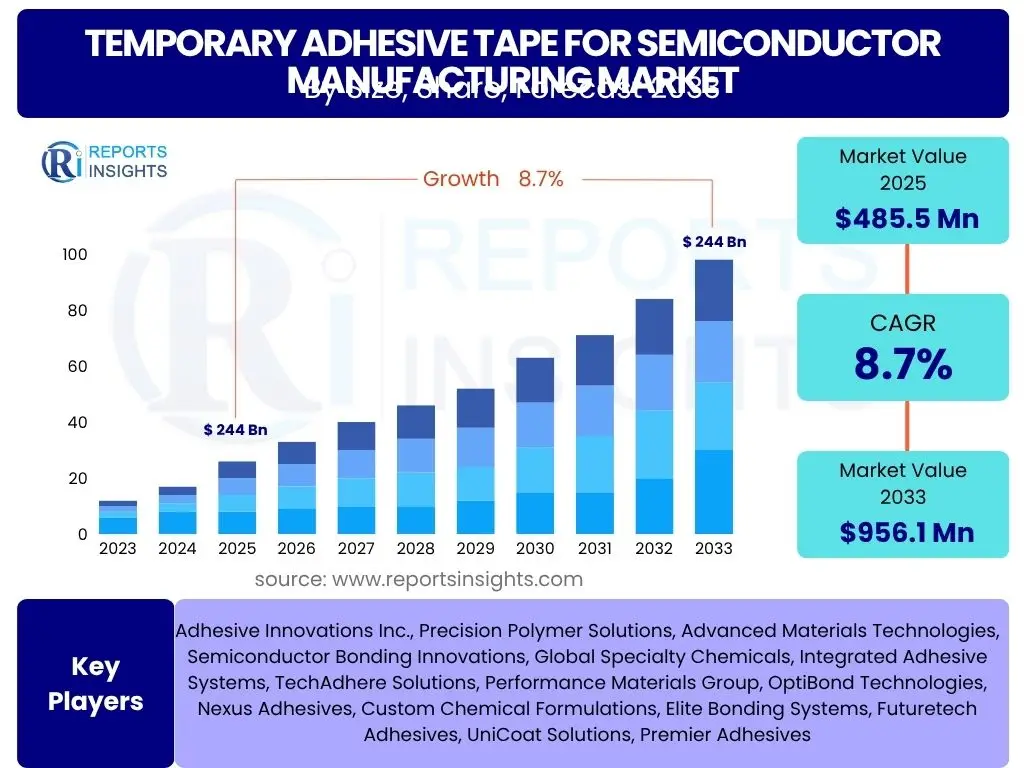

According to Reports Insights Consulting Pvt Ltd, The Temporary Adhesive Tape for Semiconductor Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 485.5 million in 2025 and is projected to reach USD 956.1 million by the end of the forecast period in 2033.

Key Temporary Adhesive Tape for Semiconductor Manufacturing Market Trends & Insights

The Temporary Adhesive Tape for Semiconductor Manufacturing market is undergoing significant transformation, driven by persistent demand for smaller, more powerful, and energy-efficient electronic devices. A primary trend involves the increasing adoption of advanced packaging technologies like 3D ICs, fan-out wafer-level packaging (FOWLP), and chip-on-wafer (CoW), all of which necessitate highly precise and reliable temporary bonding solutions. These technologies require adhesives that can withstand extreme processing conditions, including high temperatures and chemical exposure, while ensuring clean, residue-free debonding.

Another crucial insight points towards the growing emphasis on sustainable manufacturing practices within the semiconductor industry. This translates into a rising demand for eco-friendly temporary adhesive tapes, particularly those with low VOC (Volatile Organic Compound) content or UV-curable formulations that offer energy-efficient processing and easier waste management. Furthermore, the market is witnessing a trend towards customizable adhesive solutions, as different semiconductor processes and materials require unique bonding and debonding characteristics, driving innovation in material science and adhesive formulation.

Finally, the proliferation of artificial intelligence (AI), Internet of Things (IoT), and 5G technologies is spurring an unprecedented demand for high-performance semiconductor components. This surge in demand directly impacts the temporary adhesive tape market by increasing the volume of wafer processing and advanced packaging operations, thereby creating a sustained need for efficient and reliable temporary bonding solutions across the entire semiconductor supply chain. Manufacturers are continuously investing in research and development to enhance adhesive performance, improve process efficiency, and reduce overall manufacturing costs.

- Miniaturization and advanced packaging technologies (3D IC, FOWLP) are driving demand for high-performance adhesives.

- Increased focus on eco-friendly and sustainable adhesive formulations, including low VOC and UV-curable options.

- Growing need for customized temporary adhesive solutions to meet diverse process requirements.

- Accelerated demand for semiconductor components due to AI, IoT, and 5G proliferation.

- Continuous investment in R&D for enhanced adhesive performance, process efficiency, and cost reduction.

AI Impact Analysis on Temporary Adhesive Tape for Semiconductor Manufacturing

The integration of Artificial Intelligence (AI) is set to significantly revolutionize various facets of the temporary adhesive tape market within semiconductor manufacturing. Common user questions often revolve around how AI can enhance efficiency, improve quality control, and contribute to predictive analytics in adhesive application. AI-driven systems can analyze vast datasets from manufacturing processes, including adhesive application parameters, curing profiles, and debonding performance. This capability enables real-time optimization of processes, leading to reduced material waste, improved yield rates, and more consistent product quality. For instance, machine learning algorithms can predict optimal adhesive thickness or curing times based on specific wafer characteristics, thereby minimizing errors and maximizing throughput.

Furthermore, AI plays a crucial role in predictive maintenance for manufacturing equipment used in adhesive application and debonding. By monitoring equipment performance and identifying anomalies, AI can anticipate potential failures or deviations in adhesive dispensing systems, UV curing units, or thermal debonding machines. This proactive approach minimizes downtime, extends equipment lifespan, and ensures uninterrupted production, which is critical in high-volume semiconductor fabrication plants. Users are keen to understand how AI can make their operations more resilient and cost-effective.

Beyond process optimization, AI is also impacting material discovery and development for next-generation temporary adhesives. AI algorithms can rapidly screen potential chemical compositions and predict their properties, significantly accelerating the research and development cycle for novel adhesive materials with superior bonding strength, temperature resistance, and clean debonding characteristics. This expedites the creation of adhesives tailored for emerging semiconductor technologies and complex packaging architectures, directly addressing user demands for higher performance and custom solutions.

- AI enables real-time optimization of adhesive application processes, reducing waste and improving yield.

- Predictive maintenance for adhesive dispensing and debonding equipment is enhanced by AI, minimizing downtime.

- AI accelerates material discovery and development for new, high-performance temporary adhesives.

- Enhanced quality control through AI-driven anomaly detection in adhesive layers.

- Automated defect detection using computer vision and AI ensures precise adhesive placement.

Key Takeaways Temporary Adhesive Tape for Semiconductor Manufacturing Market Size & Forecast

The Temporary Adhesive Tape for Semiconductor Manufacturing market is poised for robust growth, driven by the relentless advancement in semiconductor technology and increasing global demand for electronic components. A significant takeaway is the strong Compound Annual Growth Rate projected through 2033, underscoring the indispensable role of these specialized tapes in modern wafer processing and advanced packaging techniques. The market's expansion is intrinsically linked to the continuous innovations in device miniaturization and the complexities associated with multi-chip integration, which necessitate highly precise and reliable temporary bonding solutions throughout various manufacturing stages.

Another crucial insight is the dynamic interplay between technological development and market demand. As semiconductor manufacturing processes become more intricate, there is a heightened requirement for temporary adhesives that can withstand extreme conditions, offer superior adhesion during processing, and ensure clean, residue-free debonding. This drives significant investment in research and development by manufacturers to meet evolving industry standards and performance benchmarks. The growth trajectory also reflects the expanding application scope of semiconductors across diverse end-use industries, including automotive, healthcare, and consumer electronics, each contributing to the sustained demand for advanced temporary adhesive solutions.

Finally, the market forecast highlights the increasing shift towards high-value adhesive products, such as UV-curable and thermal release tapes, which offer distinct advantages in terms of efficiency, environmental impact, and process compatibility. This shift signifies a maturation of the market, where performance and sustainability are becoming as critical as cost. The dominance of the Asia Pacific region in semiconductor manufacturing ensures that it will remain the primary growth engine, though other regions are also expected to see notable expansion as global semiconductor capacities diversify.

- Market demonstrates robust growth with a significant CAGR through 2033, driven by semiconductor innovation.

- The essential role of temporary adhesives in advanced wafer processing and complex packaging drives sustained demand.

- Technological advancements in semiconductors necessitate high-performance, resilient adhesive solutions.

- Growth is supported by expanding semiconductor applications across diverse end-use industries.

- Shift towards high-value, efficient, and eco-friendly adhesive types such as UV-curable and thermal release.

Temporary Adhesive Tape for Semiconductor Manufacturing Market Drivers Analysis

The Temporary Adhesive Tape for Semiconductor Manufacturing market is primarily propelled by the exponential growth and increasing complexity of the global semiconductor industry. The relentless pursuit of miniaturization and higher performance in electronic devices demands sophisticated wafer processing and advanced packaging techniques, such as 3D IC stacking and fan-out wafer-level packaging (FOWLP). These processes inherently rely on temporary adhesive tapes to secure ultra-thin wafers during critical stages like grinding, dicing, and bonding, ensuring structural integrity and precise alignment without damaging the delicate silicon. The expansion of these advanced manufacturing methods directly translates into a surging demand for specialized temporary adhesives that can meet stringent technical requirements for adhesion, thermal stability, and clean debonding.

Furthermore, the pervasive integration of semiconductor components into an ever-widening array of end-use applications is a significant market driver. Industries such as consumer electronics, automotive (especially for electric vehicles and autonomous driving), industrial automation, and healthcare are witnessing unprecedented growth in their demand for high-performance chips. Each new application, from advanced driver-assistance systems (ADAS) to AI accelerators and IoT sensors, requires robust and reliable semiconductor manufacturing processes, where temporary adhesive tapes play a critical enabling role. This broad-based demand ensures a consistent and expanding market for temporary bonding solutions.

Lastly, ongoing technological advancements within the adhesive industry itself contribute to market growth. Continuous research and development efforts are leading to the creation of next-generation temporary adhesive tapes that offer improved performance characteristics, such as enhanced heat resistance, superior chemical inertness, and more efficient debonding mechanisms (e.g., laser debondable or water-soluble options). These innovations address evolving manufacturing challenges and enable semiconductor manufacturers to achieve higher yields, reduce processing times, and lower overall production costs, thereby fostering greater adoption of advanced temporary bonding solutions across the industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Advanced Packaging Technologies (e.g., 3D IC, FOWLP) | +2.1% | Global, particularly Asia Pacific (South Korea, Taiwan, Japan, China) | Short-term to Mid-term (2025-2029) |

| Rising Adoption of Semiconductor Devices Across End-use Industries (5G, AI, IoT, Automotive) | +1.8% | Global, especially North America, Europe, and Asia Pacific | Mid-term to Long-term (2027-2033) |

| Technological Advancements in Temporary Adhesive Formulations (e.g., UV-curable, thermal release) | +1.5% | Global, primarily R&D hubs in North America, Europe, Japan | Continuous, Long-term |

| Growth in Wafer Thinning and Dicing Processes for Miniaturization | +1.3% | Global, strong in established semiconductor manufacturing regions | Short-term to Mid-term (2025-2030) |

| Investment in New Semiconductor Manufacturing Fabs and Expansion of Existing Facilities | +1.0% | Asia Pacific (China, Taiwan), North America, Europe | Mid-term (2026-2031) |

Temporary Adhesive Tape for Semiconductor Manufacturing Market Restraints Analysis

Despite robust growth prospects, the Temporary Adhesive Tape for Semiconductor Manufacturing market faces several notable restraints. One significant challenge is the high cost associated with advanced temporary adhesive materials and the specialized equipment required for their application and debonding. Developing adhesives that can withstand extreme thermal cycling, chemical exposure, and mechanical stress while ensuring residue-free removal demands sophisticated formulations and stringent quality control, which drives up production costs. This elevated cost can be a barrier for some manufacturers, particularly smaller players or those operating with tighter margins, potentially leading them to seek less optimal but more economical bonding solutions or alternative technologies.

Another key restraint is the stringent performance requirements and the technical complexity involved in achieving consistent and reliable debonding without damaging delicate semiconductor wafers. Any residual adhesive or mechanical stress during debonding can lead to costly defects, reduced yields, and compromised device performance. The industry constantly demands finer tolerances and lower defect rates, pushing adhesive manufacturers to innovate under immense pressure. This technical hurdle necessitates extensive research and development, prolonged validation processes, and highly precise manufacturing techniques, which can slow down market adoption for new adhesive products and limit the scalability of some solutions.

Furthermore, the increasing focus on environmental regulations and sustainability poses a restraint, particularly concerning the disposal and recyclability of temporary adhesive tapes and their associated residues. Many traditional adhesives contain volatile organic compounds (VOCs) or require chemical solvents for cleaning, raising environmental concerns and increasing compliance costs. While the industry is moving towards more eco-friendly alternatives like UV-curable and thermal-release tapes, the transition requires significant investment in new equipment and processes, which can act as a short-term impediment to wider adoption. The complexity of managing end-of-life adhesive materials and reducing the overall environmental footprint presents an ongoing challenge for market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Temporary Adhesive Materials and Equipment | -1.5% | Global, affecting cost-sensitive regions like emerging economies | Short-term to Mid-term (2025-2029) |

| Stringent Performance Requirements and Technical Complexity of Debonding | -1.3% | Global, particularly advanced manufacturing hubs | Continuous, Long-term |

| Environmental Regulations and Challenges in Waste Management/Recycling | -1.0% | Europe, North America, Japan (regions with strict environmental policies) | Mid-term to Long-term (2027-2033) |

| Emergence of Alternative Wafer Handling Technologies (e.g., carrier-free bonding) | -0.8% | Global, especially R&D intensive areas | Long-term (2030-2033) |

| Supply Chain Vulnerabilities and Geopolitical Tensions Affecting Raw Material Availability | -0.7% | Global, particularly regions dependent on specific raw material imports | Short-term (2025-2026) |

Temporary Adhesive Tape for Semiconductor Manufacturing Market Opportunities Analysis

The Temporary Adhesive Tape for Semiconductor Manufacturing market presents significant opportunities driven by evolving technological landscapes and expanding application domains. One primary opportunity lies in the continuous innovation of semiconductor packaging, particularly the widespread adoption of 3D integration and heterogeneous integration technologies. These advanced methods, which involve stacking multiple chips and components, demand highly sophisticated temporary bonding solutions that can facilitate precise alignment, withstand complex processing steps, and ensure robust yet reversible adhesion. Developing adhesives specifically tailored for these next-generation packaging architectures, offering improved thermal management and stress reduction capabilities, creates new avenues for market growth and differentiation.

Moreover, the burgeoning demand for semiconductors in emerging fields such as the Internet of Things (IoT), artificial intelligence (AI) at the edge, and high-performance computing (HPC) offers a substantial opportunity. Each of these applications requires specialized chips with unique performance characteristics, often involving novel materials and manufacturing processes that necessitate custom temporary adhesive solutions. For instance, the automotive sector's pivot towards electric vehicles and autonomous driving is driving an unprecedented need for robust and reliable automotive-grade semiconductors, opening up a lucrative niche for adhesive manufacturers who can provide solutions meeting stringent automotive industry standards for reliability and longevity.

Finally, the growing global emphasis on sustainable manufacturing practices presents a notable opportunity for adhesive manufacturers. There is increasing demand for temporary adhesive tapes that are environmentally friendly, featuring low-VOC formulations, solvent-free debonding processes, or even fully biodegradable options. Companies that invest in green chemistry and develop temporary adhesives with reduced environmental impact can gain a competitive edge and capture market share from environmentally conscious semiconductor manufacturers. Furthermore, the development of intelligent adhesives that can be precisely controlled and monitored during the manufacturing process, possibly through integrated sensors or smart debonding mechanisms, represents a future growth area, aligning with the broader trend of smart manufacturing and Industry 4.0 within the semiconductor sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Semiconductor Applications (e.g., Automotive, Healthcare, Wearables) | +1.9% | Global, with strong potential in developed economies and emerging markets | Mid-term to Long-term (2027-2033) |

| Development of Advanced Debonding Technologies (e.g., Laser Debonding, UV-Assisted Thermal Debonding) | +1.6% | Global, particularly in R&D-intensive regions (North America, Japan, Europe) | Continuous, Long-term |

| Increasing Focus on Eco-friendly and Sustainable Adhesive Solutions | +1.4% | Europe, North America, Japan, and environmentally conscious manufacturers globally | Mid-term (2026-2031) |

| Expansion of Semiconductor Manufacturing Capacities in New Geographic Regions | +1.1% | Southeast Asia, India, North America, Europe (diversification of supply chains) | Mid-term to Long-term (2028-2033) |

| Demand for Customizable and Application-Specific Adhesive Solutions | +0.9% | Global, especially among specialized semiconductor foundries | Continuous |

Temporary Adhesive Tape for Semiconductor Manufacturing Market Challenges Impact Analysis

The Temporary Adhesive Tape for Semiconductor Manufacturing market faces several significant challenges that can impede its growth and innovation. A key challenge lies in the increasingly stringent performance requirements for temporary adhesives, driven by the continuous advancements in semiconductor technology. As wafers become thinner and device structures more intricate, adhesives must provide exceptionally uniform bonding, withstand higher processing temperatures, and ensure absolutely residue-free debonding. Achieving this delicate balance across diverse wafer materials and process conditions is technically demanding and requires substantial research and development investment, often leading to prolonged development cycles and higher product costs, which can be difficult for market players to absorb and pass on to customers.

Another substantial challenge is the intense competitive landscape and the pressure to reduce costs while maintaining high quality. The semiconductor industry is highly capital-intensive, and manufacturers are constantly seeking ways to optimize their production processes and lower expenses. This puts immense pressure on temporary adhesive suppliers to offer cost-effective solutions without compromising performance or reliability. The need to balance innovation with affordability, especially for specialized high-performance products, often leads to compressed profit margins for adhesive manufacturers and fierce competition, which can discourage smaller companies from entering the market or investing in groundbreaking research.

Furthermore, supply chain volatility and geopolitical uncertainties pose a significant challenge. The raw materials used in temporary adhesive tapes often come from a limited number of suppliers or specific regions, making the supply chain vulnerable to disruptions from natural disasters, trade disputes, or political instability. Any interruption in the supply of critical raw materials can lead to increased costs, production delays, and a potential inability to meet customer demand, directly impacting market stability and growth. Managing these risks requires robust supply chain strategies, including diversification of suppliers and increased inventory, which can add to operational complexities and costs for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Performance Requirements and Technical Complexity of Next-Gen Adhesives | -1.6% | Global, particularly for leading-edge semiconductor manufacturing | Continuous, Long-term |

| Cost Pressure and Competitive Pricing in a High-Volume Industry | -1.4% | Global, especially in mature manufacturing regions | Short-term to Mid-term (2025-2029) |

| Supply Chain Volatility and Geopolitical Instability Affecting Raw Materials | -1.2% | Global, impacting regions reliant on specific material imports | Short-term (2025-2027) |

| Long Qualification Cycles and High R&D Investment for New Products | -0.9% | Global, affecting innovation speed and market entry | Continuous |

| Management of Adhesive Residues and Environmental Compliance Post-Debonding | -0.8% | Europe, North America, Japan (regions with strict environmental regulations) | Mid-term (2026-2031) |

Temporary Adhesive Tape for Semiconductor Manufacturing Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Temporary Adhesive Tape for Semiconductor Manufacturing market, encompassing market size estimations, growth projections, and detailed insights into key trends, drivers, restraints, opportunities, and challenges. It segments the market by material type, application, and end-use industry, offering a granular view of market dynamics across various regions. The report also includes a competitive landscape analysis, profiling leading players and assessing their strategic initiatives to provide a holistic understanding of the market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 485.5 million |

| Market Forecast in 2033 | USD 956.1 million |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Adhesive Innovations Inc., Precision Polymer Solutions, Advanced Materials Technologies, Semiconductor Bonding Innovations, Global Specialty Chemicals, Integrated Adhesive Systems, TechAdhere Solutions, Performance Materials Group, OptiBond Technologies, Nexus Adhesives, Custom Chemical Formulations, Elite Bonding Systems, Futuretech Adhesives, UniCoat Solutions, Premier Adhesives |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Temporary Adhesive Tape for Semiconductor Manufacturing market is intricately segmented to provide a comprehensive understanding of its diverse components and their respective dynamics. This segmentation facilitates detailed analysis of market performance across different material types, application areas, and end-use industries, allowing stakeholders to identify key growth areas and strategic opportunities. Each segment represents a distinct facet of the market, driven by specific technological requirements and industry demands.

For instance, the segmentation by material type highlights the evolution of adhesive technologies, from traditional solvent-based options to advanced UV-curable and thermal release adhesives, which offer superior performance and environmental benefits. Understanding the adoption trends within these material categories is crucial for anticipating future market shifts and investment priorities. Similarly, segmenting by application clarifies the critical roles temporary adhesives play across the entire semiconductor manufacturing process, from initial wafer preparation to complex advanced packaging, revealing areas of high demand and specialized requirements.

Finally, the end-use industry segmentation provides insight into the primary drivers of semiconductor demand and, consequently, the demand for temporary adhesives. Whether it is the robust growth in consumer electronics, the stringent requirements of the automotive sector, or the specialized needs of the industrial and healthcare industries, each vertical contributes uniquely to the market's overall trajectory. This detailed segmentation framework is essential for conducting targeted market analysis, developing tailored solutions, and formulating effective business strategies within the dynamic semiconductor ecosystem.

- By Material Type:

- UV Curable Adhesives

- Thermal Release Adhesives

- Solvent-based Adhesives

- Water-based Adhesives

- Other Adhesives (e.g., Laser Debondable, Radiation Curable)

- By Application:

- Wafer Thinning and Grinding

- Wafer Dicing

- Advanced Packaging (e.g., 3D IC, FOWLP, Bumping)

- Temporary Carrier Bonding

- Other Wafer Processing Steps

- By End-use Industry:

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Telecommunications

- Other Industries

Regional Highlights

- Asia Pacific (APAC): Dominates the Temporary Adhesive Tape for Semiconductor Manufacturing market due to the concentration of major semiconductor foundries, packaging houses, and electronic manufacturing facilities in countries like Taiwan, South Korea, China, and Japan. The region's robust investment in new fabs and advanced packaging technologies, coupled with high demand for consumer electronics, makes it the largest and fastest-growing market. APAC countries are at the forefront of wafer production and advanced chip manufacturing, necessitating extensive use of temporary adhesives.

- North America: Represents a significant market driven by strong research and development activities, innovation in advanced semiconductor technologies, and the presence of leading fabless design companies and specialized foundries. The region's focus on high-performance computing, AI, and defense applications demands cutting-edge temporary adhesive solutions. Investments in reshoring semiconductor manufacturing also contribute to sustained growth.

- Europe: Exhibits steady growth, primarily fueled by the region's strong automotive and industrial electronics sectors, which increasingly rely on advanced semiconductors. Countries like Germany and France are key players in automotive electronics and smart manufacturing, driving demand for reliable temporary bonding solutions. Europe also focuses on sustainable and environmentally friendly adhesive solutions, aligning with its strict regulatory environment.

- Latin America: A nascent but emerging market for semiconductor manufacturing, with growing interest in establishing local production capabilities. While currently a smaller share, increasing investments in electronics assembly and the expansion of consumer electronics consumption are expected to drive gradual growth in the demand for temporary adhesive tapes.

- Middle East and Africa (MEA): Currently holds a relatively smaller share of the market, primarily due to limited semiconductor manufacturing infrastructure. However, ongoing diversification efforts and investments in technology hubs, particularly in countries like UAE and Saudi Arabia, could lead to future opportunities for growth in electronics assembly and, consequently, demand for temporary adhesives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Temporary Adhesive Tape for Semiconductor Manufacturing Market.- Adhesive Innovations Inc.

- Precision Polymer Solutions

- Advanced Materials Technologies

- Semiconductor Bonding Innovations

- Global Specialty Chemicals

- Integrated Adhesive Systems

- TechAdhere Solutions

- Performance Materials Group

- OptiBond Technologies

- Nexus Adhesives

- Custom Chemical Formulations

- Elite Bonding Systems

- Futuretech Adhesives

- UniCoat Solutions

- Premier Adhesives

- Specialty Adhesive Products

- Bonding Solutions Inc.

- Industrial Polymer Solutions

- High-Tech Adhesives Corp.

- Innovate Adhesion Ltd.

Frequently Asked Questions

What is temporary adhesive tape used for in semiconductor manufacturing?

Temporary adhesive tape is crucial for securely holding delicate semiconductor wafers during various processing steps, such as wafer thinning, grinding, dicing, and advanced packaging. It provides stable support and protection, enabling precise handling and preventing damage, then allows for clean, residue-free debonding once the process is complete.

What are the key types of temporary adhesive tapes in this market?

The primary types include UV-curable adhesives, which debond when exposed to UV light, and thermal release adhesives, which lose adhesion when heated. Other types include solvent-based and water-based adhesives, along with emerging laser debondable solutions, each offering specific advantages for different manufacturing processes.

Which region dominates the Temporary Adhesive Tape for Semiconductor Manufacturing market?

The Asia Pacific (APAC) region currently dominates the market due to the high concentration of major semiconductor manufacturing facilities, including leading foundries and advanced packaging companies, in countries like Taiwan, South Korea, China, and Japan.

What are the main drivers for market growth?

Key drivers include the increasing demand for advanced semiconductor packaging technologies (e.g., 3D IC, FOWLP), the continuous miniaturization of electronic devices, and the expanding adoption of semiconductors in high-growth industries like 5G, AI, IoT, and automotive electronics.

What are the biggest challenges facing this market?

Significant challenges include the high cost of advanced temporary adhesive materials, the technical complexity of achieving consistently residue-free debonding for ultra-thin wafers, stringent performance requirements, and managing supply chain vulnerabilities and environmental regulations related to adhesive waste.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted