Supplementary Cementitiou Material Market

Supplementary Cementitiou Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700885 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

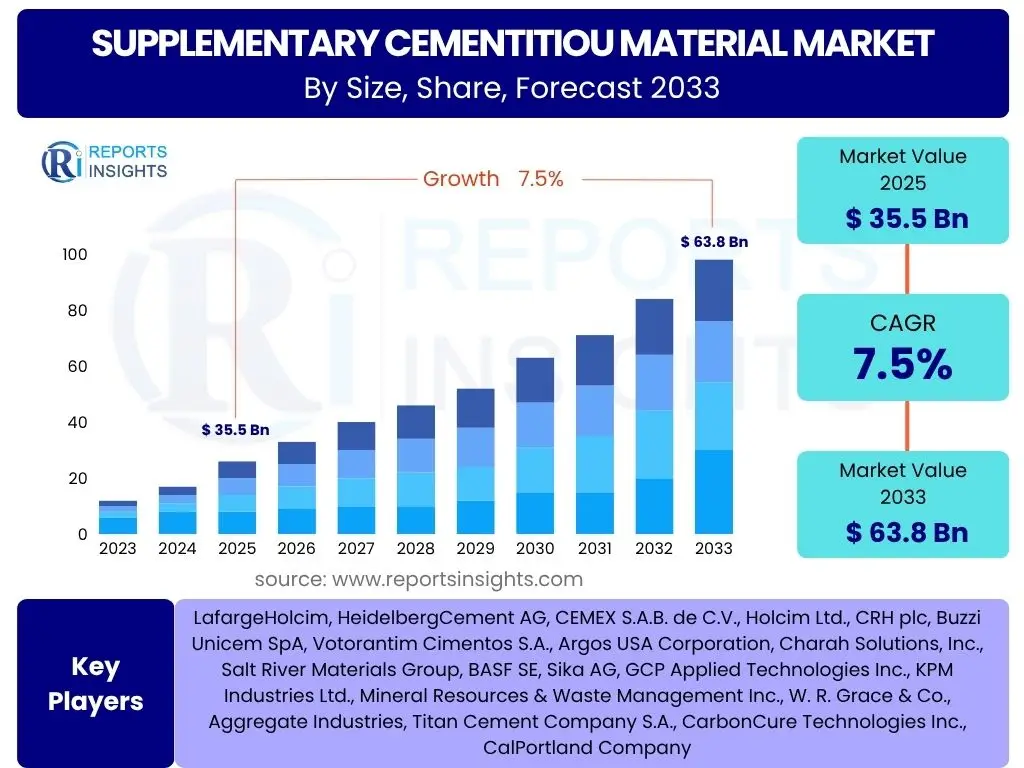

Supplementary Cementitiou Material Market Size

According to Reports Insights Consulting Pvt Ltd, The Supplementary Cementitiou Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 35.5 Billion in 2025 and is projected to reach USD 63.8 Billion by the end of the forecast period in 2033.

Key Supplementary Cementitiou Material Market Trends & Insights

The Supplementary Cementitious Material (SCM) market is experiencing transformative shifts driven by global sustainability imperatives and the evolving dynamics of the construction sector. Key inquiries from stakeholders often center on how environmental regulations, technological innovations, and resource availability are reshaping SCM adoption. The increasing demand for low-carbon building solutions and the depletion of traditional SCM sources like quality fly ash are compelling the industry to explore novel materials and advanced processing techniques. This shift is not only about compliance but also about achieving superior concrete performance and economic viability in the long term.

Furthermore, there is a growing interest in understanding the interplay between traditional SCMs and emerging alternatives, alongside the impact of digital technologies on their production and deployment. The market is witnessing a move towards performance-based specifications rather than prescriptive ones, allowing for greater flexibility in SCM utilization. Regional variations in industrial by-product availability and local environmental policies also significantly influence the prevalent SCM trends, leading to diverse market developments across different geographies. The focus remains on enhancing concrete durability, reducing carbon footprint, and optimizing material efficiency.

- Increasing adoption of green building practices and sustainable construction methods.

- Growing scarcity and inconsistent quality of traditional SCMs such as high-grade fly ash.

- Development and commercialization of novel SCMs, including calcined clays and ground-glass pozzolans.

- Rising focus on circular economy principles, promoting the use of industrial waste products as SCMs.

- Advancements in material characterization and performance-based concrete mix design.

- Stringent environmental regulations mandating reductions in carbon emissions from cement production.

- Digitalization and automation in SCM production and quality control processes.

- Expansion of infrastructure projects globally, particularly in emerging economies, driving demand.

- Emphasis on enhancing concrete durability, strength, and resistance to environmental degradation.

AI Impact Analysis on Supplementary Cementitiou Material

Common user questions regarding AI's impact on Supplementary Cementitious Materials frequently revolve around its potential to optimize material properties, streamline supply chains, and enhance quality control. Stakeholders are keen to understand how artificial intelligence can accelerate the discovery of new SCMs, predict their performance characteristics, and facilitate more efficient concrete mix designs. The underlying expectation is that AI will introduce unprecedented levels of precision and efficiency into an industry traditionally reliant on empirical methods and extensive laboratory testing. This technological integration is anticipated to reduce material waste, lower production costs, and significantly shorten development cycles for innovative cementitious solutions.

The broader concerns often include the initial investment required for AI implementation, the need for specialized data and skilled personnel, and the challenges associated with integrating AI with existing legacy systems. Despite these challenges, there is a clear recognition that AI offers transformative capabilities, particularly in predictive analytics for material sourcing and demand forecasting, enabling more robust and resilient supply chains for SCMs. AI's ability to process vast datasets quickly can also lead to breakthroughs in understanding complex chemical interactions, paving the way for superior and more sustainable concrete formulations. It is seen as a key enabler for the next generation of high-performance and eco-friendly construction materials.

- AI-driven optimization of SCM composition for enhanced concrete performance and durability.

- Predictive modeling for SCM sourcing and supply chain management, improving logistics and reducing costs.

- Automated quality control and anomaly detection in SCM production through machine learning algorithms.

- Accelerated discovery and characterization of novel SCMs using AI-powered material informatics.

- Optimization of concrete mix designs with various SCM blends for specific applications and environmental conditions.

- Real-time monitoring of SCM properties during manufacturing to ensure consistency and compliance.

- Improved demand forecasting for SCMs based on construction project pipelines and economic indicators.

- Enhanced understanding of SCMs' long-term behavior in concrete through data-driven simulations.

Key Takeaways Supplementary Cementitiou Material Market Size & Forecast

Key inquiries from industry stakeholders regarding the Supplementary Cementitious Material (SCM) market size and forecast often focus on identifying primary growth drivers, understanding regional market dominance, and pinpointing emerging opportunities. The analysis indicates a robust growth trajectory, primarily fueled by the global push for sustainable construction practices and increasingly stringent environmental regulations targeting carbon emissions from traditional cement production. Emerging economies, particularly in Asia Pacific, are poised to be significant growth engines due to rapid urbanization and large-scale infrastructure development projects. These regions are actively seeking cost-effective and environmentally friendly alternatives to conventional Portland cement, boosting SCM demand.

Furthermore, market participants are keenly observing the shift towards high-performance concrete and the diversification of SCM sources beyond traditional by-products. The market is not just expanding in volume but also evolving in terms of material diversity and application scope. Innovation in SCM formulation and processing technology is crucial for unlocking new market segments and overcoming challenges related to raw material availability and consistency. The long-term forecast underscores a sustained transition towards more sustainable building materials, making SCMs indispensable components of future construction endeavors.

- Significant market expansion is driven by global sustainability initiatives and climate change mitigation efforts.

- Asia Pacific is expected to maintain its leadership position due to extensive infrastructure development and urbanization.

- The market is witnessing a notable shift from traditional fly ash and slag to novel and engineered SCMs.

- Increasing emphasis on concrete durability and performance is fueling demand for high-quality SCMs.

- Regulatory frameworks promoting lower carbon concrete are acting as strong market accelerators.

- Investment in research and development for new SCMs and processing technologies is crucial for competitive advantage.

- Opportunities abound in specialized applications such as high-performance concrete and geotechnical works.

Supplementary Cementitiou Material Market Drivers Analysis

The Supplementary Cementitious Material (SCM) market is significantly propelled by a confluence of environmental, economic, and technological factors. A primary driver is the escalating global imperative to reduce carbon emissions from the construction sector, with cement production being a major contributor. SCMs offer a proven solution by replacing a portion of high-carbon Portland cement, thereby lowering the overall carbon footprint of concrete. This environmental advantage is further amplified by the economic benefits, as SCMs are often industrial by-products that can be more cost-effective than virgin cement, providing an economic incentive for their adoption.

Furthermore, the rapid pace of infrastructure development worldwide, particularly in developing economies, creates a sustained demand for concrete. The utilization of SCMs enhances the durability and long-term performance of concrete structures, offering superior resistance to chemical attack and improved strength development, which is critical for resilient infrastructure. This performance aspect, coupled with increasing governmental support for sustainable building practices through regulations and incentives, creates a strong enabling environment for market growth. The industry's continuous innovation in processing various waste streams into viable SCMs also contributes significantly to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for sustainable and low-carbon construction practices | +2.1% | Global, particularly Europe, North America, and APAC | Short to Long-term |

| Rising cost and environmental impact of traditional Portland cement | +1.8% | Global, with pronounced effect in cost-sensitive markets | Mid-term |

| Growing infrastructure development and urbanization in emerging economies | +1.6% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Advancements in concrete technology enhancing SCM performance benefits | +1.2% | Developed regions leading innovation, followed by adoption globally | Mid to Long-term |

Supplementary Cementitiou Material Market Restraints Analysis

Despite the strong growth drivers, the Supplementary Cementitious Material (SCM) market faces several restraints that can impede its full potential. A significant challenge is the inconsistent availability and variable quality of certain traditional SCMs, such as fly ash and slag, which are by-products of other industrial processes. Fluctuations in the output of coal-fired power plants or steel production directly impact the supply of these materials, leading to price volatility and supply chain disruptions. This variability can make it difficult for concrete producers to ensure consistent product performance and reliable sourcing, hindering broader adoption, especially in regions with limited industrial activity.

Furthermore, the lack of standardized specifications and testing protocols across different regions poses a hurdle. While efforts are underway to harmonize standards, variations in material classification and performance requirements can create technical and regulatory barriers for SCM manufacturers and users. Logistical challenges associated with transporting bulky SCMs over long distances, coupled with the need for specialized storage facilities, also add to operational costs and limit their economic viability in certain remote areas. Overcoming these restraints requires concerted efforts in material processing, standardization, and infrastructure development to ensure a stable and high-quality supply of SCMs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inconsistent availability and variable quality of raw SCMs | -1.5% | Global, particularly regions dependent on industrial by-products | Short to Mid-term |

| Lack of standardized specifications and testing procedures for diverse SCMs | -1.0% | Global, impacting market uniformity and acceptance | Mid-term |

| High transportation and logistics costs for bulky SCMs | -0.8% | Remote areas and regions with underdeveloped infrastructure | Short to Mid-term |

| Limited awareness and technical expertise among some end-users regarding SCM benefits and application | -0.7% | Developing countries and smaller construction firms | Long-term |

Supplementary Cementitiou Material Market Opportunities Analysis

The Supplementary Cementitious Material (SCM) market is ripe with opportunities driven by innovation, regulatory support, and expanding application areas. A significant opportunity lies in the development and commercialization of novel SCMs derived from alternative waste streams or engineered materials, such as calcined clays, ground-glass pozzolans, and agricultural wastes. As traditional SCMs like fly ash become scarcer or more inconsistent in quality, the industry's focus shifts towards these new sources, offering sustainable and potentially more consistent material options. This diversification not only addresses supply challenges but also broadens the scope of materials available for concrete production, catering to specific performance requirements.

Furthermore, the increasing global emphasis on circular economy principles presents a substantial opportunity for SCMs, as they facilitate the re-utilization of industrial by-products that would otherwise be discarded. Government initiatives and green building certifications that incentivize the use of recycled content and low-carbon materials are creating new market niches and driving demand. The expansion of SCM applications beyond conventional concrete, into areas like specialized grouts, mortars, and prefabrication, also opens up new revenue streams. Continuous research and development in SCM processing technologies and mix designs will be key to unlocking these opportunities, ensuring their technical viability and economic competitiveness across diverse construction segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of novel and engineered SCMs from diverse waste streams | +1.9% | Global, particularly in regions with limited traditional SCMs | Mid to Long-term |

| Expanding applications of SCMs in specialized concrete, precast, and repair works | +1.5% | Developed markets with advanced construction practices | Mid-term |

| Government incentives and regulations promoting circular economy and green building | +1.3% | Europe, North America, and increasingly Asia Pacific | Short to Mid-term |

| Technological advancements in SCM processing and activation for enhanced reactivity | +1.1% | Global, driven by R&D investment | Long-term |

Supplementary Cementitiou Material Market Challenges Impact Analysis

The Supplementary Cementitious Material (SCM) market, despite its growth potential, is confronted by several significant challenges that necessitate strategic responses from industry players. One major challenge is ensuring the consistent quality and chemical stability of SCMs, particularly those derived from industrial waste. Variations in source material composition and processing can lead to unpredictable performance in concrete, which can deter widespread adoption, especially in critical structural applications where reliability is paramount. This necessitates rigorous quality control measures and advanced characterization techniques to build confidence among end-users and regulatory bodies.

Another key challenge involves the significant capital investment required for establishing new SCM production facilities, especially for novel materials that require specialized processing technologies. The high upfront costs and long payback periods can be a barrier for new entrants and limit the scalability of innovative SCM solutions. Furthermore, market fragmentation, characterized by numerous small-scale producers and regional supply chains, can lead to inefficiencies and hinder the development of a cohesive global market. Overcoming these challenges will require collaborative efforts between producers, researchers, and policymakers to establish robust supply chains, standardized practices, and supportive investment frameworks for the SCM industry's sustainable growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring consistent quality and performance across diverse SCM sources | -1.2% | Global, impacting trust and widespread adoption | Short to Mid-term |

| High capital investment required for new SCM production facilities and R&D | -0.9% | Global, particularly for scaling novel SCM technologies | Long-term |

| Competition from established traditional cement and alternative binders | -0.6% | Global, especially in price-sensitive markets | Short-term |

| Market fragmentation and complexities in regional supply chains for SCMs | -0.5% | Developing regions and countries with disparate industrial activity | Mid-term |

Supplementary Cementitiou Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Supplementary Cementitious Material (SCM) market, encompassing historical data, current trends, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It offers strategic insights into the competitive landscape, profiling leading players and highlighting their market strategies. The report aims to equip stakeholders with actionable intelligence to make informed business decisions within the dynamic SCM industry, focusing on sustainable and performance-driven solutions for the global construction sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.5 Billion |

| Market Forecast in 2033 | USD 63.8 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LafargeHolcim, HeidelbergCement AG, CEMEX S.A.B. de C.V., Holcim Ltd., CRH plc, Buzzi Unicem SpA, Votorantim Cimentos S.A., Argos USA Corporation, Charah Solutions, Inc., Salt River Materials Group, BASF SE, Sika AG, GCP Applied Technologies Inc., KPM Industries Ltd., Mineral Resources & Waste Management Inc., W. R. Grace & Co., Aggregate Industries, Titan Cement Company S.A., CarbonCure Technologies Inc., CalPortland Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Supplementary Cementitious Material (SCM) market is extensively segmented by type and application to provide a granular view of its diverse dynamics and growth opportunities. Understanding these segmentations is crucial for market participants to identify lucrative niches, tailor product offerings, and develop targeted strategies. The "By Type" segmentation categorizes SCMs based on their chemical composition and source, reflecting their unique performance characteristics and availability. This allows for a deeper analysis of the market share and growth prospects of traditional SCMs like fly ash and GGBS, as well as emerging materials such as calcined clay and silica fume, which are gaining prominence due to specific performance benefits or sustainability profiles.

The "By Application" segmentation dissects the market based on the end-use sectors where SCMs are primarily utilized, including residential, commercial, infrastructure, and industrial construction. Each application area has distinct requirements for concrete performance, durability, and cost-efficiency, influencing the choice and volume of SCMs. For instance, large-scale infrastructure projects prioritize long-term durability and strength, often leading to higher SCM usage, while residential construction might focus more on cost-effectiveness and ease of use. This detailed segmentation enables an assessment of demand drivers across different construction segments and helps in forecasting future consumption patterns based on sectoral growth projections and evolving building standards.

- By Type

- Fly Ash (Class C, Class F)

- Ground Granulated Blast-Furnace Slag (GGBS)

- Silica Fume

- Metakaolin

- Calcined Clay

- Others (e.g., Rice Husk Ash, Glass Pozzolan)

- By Application

- Residential Construction

- Commercial Construction

- Infrastructure (Roads, Bridges, Dams)

- Industrial Construction

- Repair and Maintenance

- Specialty Applications (e.g., Grouting, Mortars)

Regional Highlights

- Asia Pacific (APAC): Dominates the Supplementary Cementitious Material market due to extensive infrastructure development, rapid urbanization, and a high volume of construction activities in countries like China, India, and Southeast Asian nations. The region benefits from abundant availability of traditional SCMs from industrial output and a growing emphasis on sustainable building practices.

- Europe: Exhibits significant growth driven by stringent environmental regulations, a strong focus on decarbonization in the construction industry, and the adoption of advanced concrete technologies. Countries like Germany, France, and the UK are leading in the development and utilization of novel SCMs and circular economy initiatives.

- North America: Characterized by increasing investment in resilient infrastructure and a rising awareness of sustainable construction. The market here is driven by the need to upgrade aging infrastructure and a growing demand for high-performance concrete, with a focus on innovation in SCM applications.

- Latin America: Shows promising growth owing to increasing public and private investments in infrastructure and housing projects. Countries such as Brazil and Mexico are witnessing expanding construction sectors, which contribute to the demand for cost-effective and sustainable SCM solutions.

- Middle East & Africa (MEA): Emerging as a growth region with ambitious construction megaprojects and diversification efforts away from oil economies. The demand for SCMs is driven by large-scale urban development and infrastructure initiatives, with a growing emphasis on sustainable building materials to address environmental concerns in arid climates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Supplementary Cementitiou Material Market.- LafargeHolcim

- HeidelbergCement AG

- CEMEX S.A.B. de C.V.

- Holcim Ltd.

- CRH plc

- Buzzi Unicem SpA

- Votorantim Cimentos S.A.

- Argos USA Corporation

- Charah Solutions, Inc.

- Salt River Materials Group

- BASF SE

- Sika AG

- GCP Applied Technologies Inc.

- KPM Industries Ltd.

- Mineral Resources & Waste Management Inc.

- W. R. Grace & Co.

- Aggregate Industries

- Titan Cement Company S.A.

- CarbonCure Technologies Inc.

- CalPortland Company

Frequently Asked Questions

Analyze common user questions about the Supplementary Cementitiou Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Supplementary Cementitious Materials (SCMs)?

Supplementary Cementitious Materials (SCMs) are finely ground materials that, when used in conjunction with Portland cement, contribute to the properties of hardened concrete through hydraulic or pozzolanic activity. They enhance concrete durability, strength, and workability, while also reducing its environmental footprint by partially replacing cement.

Why are SCMs important for sustainable construction?

SCMs are crucial for sustainable construction because they reduce the demand for energy-intensive Portland cement production, thereby lowering carbon dioxide emissions. Many SCMs are industrial by-products (like fly ash or slag), promoting waste valorization and circular economy principles in the building industry.

What are the primary types of SCMs used today?

The primary types of SCMs include fly ash (a by-product of coal combustion), ground granulated blast-furnace slag (a by-product of steel production), silica fume (from silicon metal or ferrosilicon alloys), and metakaolin (a calcined clay). Newer SCMs like calcined clays and ground-glass pozzolans are also gaining prominence.

How do SCMs improve concrete performance?

SCMs improve concrete performance by refining pore structure, reducing permeability, increasing long-term strength, and enhancing resistance to chemical attack and alkali-silica reaction. They can also improve workability and reduce heat of hydration, beneficial for mass concrete pours.

What is the future outlook for the SCM market?

The SCM market is projected for robust growth, driven by increasing global infrastructure development, stringent environmental regulations pushing for decarbonization, and continuous innovation in material science. The trend towards sustainable and durable construction practices will further solidify SCMs' indispensable role in the future of the building industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted