Steel Bar Market

Steel Bar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702070 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Steel Bar Market Size

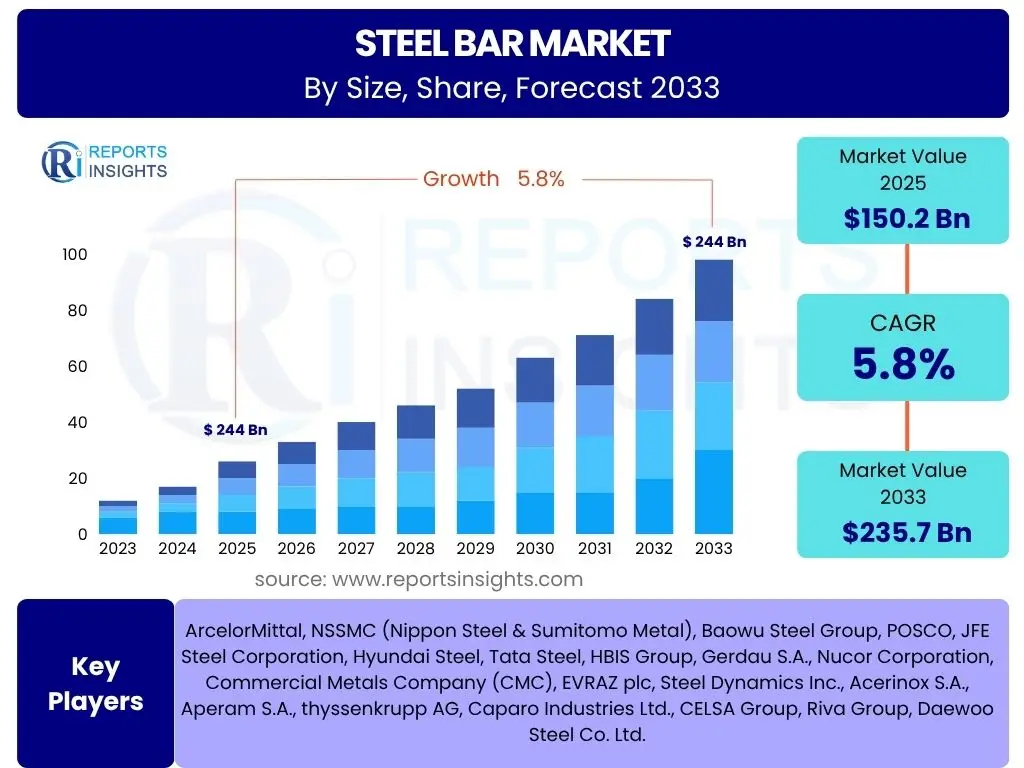

According to Reports Insights Consulting Pvt Ltd, The Steel Bar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 150.2 Billion in 2025 and is projected to reach USD 235.7 Billion by the end of the forecast period in 2033.

Key Steel Bar Market Trends & Insights

Common user inquiries about the steel bar market frequently revolve around its evolutionary trajectory, particularly concerning technological integration and sustainability efforts. There is significant interest in how advancements in manufacturing processes and material science are shaping product capabilities and applications. Furthermore, market participants and observers are keen to understand the impact of global macroeconomic shifts and regional development initiatives on demand dynamics.

A prominent trend is the increasing demand for high-strength and corrosion-resistant steel bars, driven by the need for more durable and resilient infrastructure projects. The adoption of advanced manufacturing techniques, such as automation and digital twins, is improving production efficiency and product quality. Additionally, there is a growing emphasis on sustainable practices within the steel industry, including the use of recycled materials and the reduction of carbon emissions, influencing both production methods and supply chain choices.

The market is also witnessing a surge in modular and prefabricated construction methods, which necessitate precise and standardized steel bar components. This trend is fostering innovation in fabrication and logistics. Furthermore, the expansion of renewable energy infrastructure, such as wind and solar farms, is creating new niches for specialized steel bar applications that require specific structural properties.

- Growing demand for high-strength and corrosion-resistant steel bars for enhanced durability.

- Increased adoption of advanced manufacturing technologies, including automation and digitalization.

- Shift towards sustainable production practices and increased use of recycled content.

- Rising popularity of modular and prefabricated construction methods influencing demand for standardized steel bars.

- Expansion of renewable energy infrastructure driving demand for specialized steel bar applications.

AI Impact Analysis on Steel Bar

User queries regarding the impact of Artificial Intelligence (AI) on the steel bar sector often focus on potential improvements in operational efficiency, quality control, and supply chain management. Stakeholders are keen to understand how AI algorithms can optimize complex processes, from raw material handling to final product delivery. There is also curiosity about AI's role in predictive maintenance and its implications for reducing downtime and operational costs in steel manufacturing plants.

AI is increasingly being deployed in steel bar manufacturing to optimize energy consumption and enhance process control. By analyzing vast datasets from sensors and machinery, AI can predict equipment failures, allowing for proactive maintenance and minimizing production interruptions. This leads to higher throughput and reduced operational expenditures. Furthermore, AI-powered vision systems are improving quality inspection, detecting defects with greater accuracy and speed than traditional methods.

In the supply chain, AI algorithms are enabling more efficient inventory management and logistics, optimizing routes and reducing transportation costs for steel bars. Predictive analytics, driven by AI, can forecast market demand more accurately, helping manufacturers align production levels with market needs and mitigate inventory risks. This comprehensive integration of AI across various stages of the steel bar value chain is set to revolutionize efficiency, sustainability, and profitability.

- Optimization of energy consumption and process control in steel bar manufacturing through AI.

- Enhanced predictive maintenance capabilities reducing equipment downtime and operational costs.

- Improved quality control and defect detection using AI-powered vision systems.

- Streamlined supply chain management and logistics through AI algorithms.

- More accurate demand forecasting for production alignment and inventory optimization.

Key Takeaways Steel Bar Market Size & Forecast

Common user questions about the steel bar market's future often center on the primary drivers of its expansion, potential challenges to growth, and the overall long-term viability of the sector. Users frequently seek to understand the resilience of the market against economic fluctuations and the influence of emerging technologies on its trajectory. There is also significant interest in identifying key regions and applications that will drive the most substantial growth over the forecast period.

The steel bar market is poised for robust growth through 2033, primarily fueled by extensive global infrastructure development and rapid urbanization, particularly in emerging economies. While raw material price volatility and stringent environmental regulations pose ongoing challenges, the industry's commitment to sustainable practices and technological innovation is creating significant opportunities. The long-term outlook remains positive, supported by continuous demand from the construction, automotive, and manufacturing sectors.

A crucial takeaway is the increasing segmentation within the market, driven by specific application requirements for high-performance and specialized steel bars. Regional growth disparities will persist, with Asia Pacific maintaining its dominance due to large-scale development projects, while North America and Europe focus on modernizing existing infrastructure and adopting advanced construction techniques. Investment in green steel production and circular economy principles will be critical for future competitiveness and market expansion.

- Sustained market growth driven by global infrastructure development and urbanization.

- Resilience despite challenges from raw material price volatility and environmental regulations.

- Increasing demand for high-performance and specialized steel bar variants.

- Asia Pacific to remain a key growth engine, while developed regions focus on modernization.

- Emphasis on green steel production and circular economy principles as future growth enablers.

Steel Bar Market Drivers Analysis

The global steel bar market is primarily propelled by significant investments in infrastructure development across both developed and developing nations. Governments worldwide are allocating substantial budgets towards building and upgrading roads, bridges, public transportation networks, and utilities. This sustained investment creates a consistent and high volume demand for various types of steel bars, which are fundamental components in these large-scale construction projects.

Rapid urbanization, particularly in emerging economies, is another critical driver. As populations migrate to urban centers, there is an escalating need for residential, commercial, and industrial buildings. Steel bars are indispensable in the reinforced concrete structures that form the backbone of these urban developments, ensuring structural integrity and safety. This demographic shift directly translates into increased consumption of steel bars for foundational and structural elements.

The expansion of the automotive sector, driven by increasing vehicle production and the shift towards electric vehicles, also significantly contributes to market growth. Steel bars are used extensively in automotive components, including chassis, axles, and engine parts, providing strength and durability. Furthermore, the growth in manufacturing industries, encompassing machinery, equipment, and consumer goods, requires steel bars for various fabrication and structural applications, underpinning consistent demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure Development | +1.5% | Global, particularly Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Rapid Urbanization & Construction Boom | +1.2% | Asia Pacific, Africa, Latin America | Mid to Long-term (2025-2033) |

| Growth in Automotive & Manufacturing Sectors | +0.8% | Global, particularly China, India, Germany, USA | Mid-term (2025-2030) |

| Renewable Energy Projects | +0.5% | Europe, North America, China, India | Long-term (2025-2033) |

Steel Bar Market Restraints Analysis

One of the primary restraints on the steel bar market is the significant volatility in raw material prices, particularly for iron ore and coking coal. These fluctuations directly impact production costs, making it challenging for manufacturers to maintain stable pricing and profit margins. Unpredictable input costs can deter investment in new capacity and lead to uncertainties in project budgeting for end-users, thus dampening overall market growth.

Stringent environmental regulations aimed at reducing carbon emissions and managing industrial waste also pose a considerable restraint. Steel production is an energy-intensive process with a substantial environmental footprint. Compliance with stricter emission standards and waste disposal protocols necessitates significant investments in cleaner technologies and operational adjustments, increasing production costs and potentially limiting output for some manufacturers, especially smaller players.

Economic slowdowns and geopolitical instabilities can significantly curb construction and manufacturing activities, directly impacting steel bar demand. Recessions, trade wars, or political conflicts disrupt supply chains, reduce consumer and investor confidence, and lead to delayed or canceled projects. Such macro-economic uncertainties create a challenging environment for market expansion, as demand correlates strongly with global economic health.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.9% | Global | Ongoing (2025-2033) |

| Stringent Environmental Regulations | -0.7% | Europe, North America, China | Long-term (2025-2033) |

| Economic Slowdowns & Geopolitical Instability | -0.6% | Global, varying by region | Short to Mid-term (2025-2028) |

| Competition from Alternative Materials | -0.4% | North America, Europe | Mid to Long-term (2025-2033) |

Steel Bar Market Opportunities Analysis

The increasing focus on "green steel" production presents a significant opportunity for the steel bar market. As environmental concerns grow, there is a rising demand for steel produced with reduced carbon emissions, often through the use of hydrogen, electric arc furnaces powered by renewable energy, or carbon capture technologies. Companies investing in these sustainable methods can gain a competitive edge and cater to environmentally conscious consumers and projects, unlocking new market segments.

The adoption of modular and prefabricated construction techniques offers a substantial growth opportunity. These methods emphasize off-site manufacturing of building components, including steel bar cages and assemblies, which are then transported to the construction site for rapid erection. This approach reduces construction time, labor costs, and waste, making it highly attractive for various building projects and driving demand for precision-fabricated steel bar products.

Emerging applications in the renewable energy sector, particularly for wind turbines, solar panel foundations, and geothermal energy systems, represent a burgeoning opportunity. These applications require specialized steel bars capable of withstanding extreme environmental conditions and providing robust structural support. The global push for clean energy initiatives will continue to drive demand for these high-performance steel bar solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Green Steel Production Initiatives | +0.8% | Europe, North America, Japan, South Korea | Long-term (2025-2033) |

| Modular & Prefabricated Construction Adoption | +0.7% | North America, Europe, Asia Pacific (developed markets) | Mid to Long-term (2025-2033) |

| Emerging Applications in Renewable Energy | +0.6% | Global, particularly Europe, China, USA | Long-term (2025-2033) |

| Digitalization & Industry 4.0 Integration | +0.5% | Global, especially developed industrial nations | Mid-term (2025-2030) |

Steel Bar Market Challenges Impact Analysis

The steel bar market faces significant challenges from intense global competition and overcapacity in some regions. Numerous producers, particularly in Asia, lead to fierce price competition, which can erode profit margins for manufacturers. This competitive pressure often forces companies to innovate their processes or products to maintain market share, but it also creates a downward pressure on pricing, impacting overall revenue growth across the industry.

Supply chain disruptions, stemming from events like pandemics, natural disasters, or geopolitical conflicts, present a substantial challenge. These disruptions can lead to delays in raw material procurement, increased logistics costs, and interruptions in product delivery. The globalized nature of the steel industry makes it particularly vulnerable to such events, which can cause significant market volatility and operational inefficiencies for steel bar manufacturers and their customers.

The high energy consumption inherent in steel production is another enduring challenge, exacerbated by fluctuating energy prices. Manufacturing steel bars requires substantial electricity and fuel, making operational costs highly susceptible to energy market volatility. This not only impacts profitability but also poses challenges for manufacturers aiming to reduce their carbon footprint and align with global sustainability goals, requiring significant investment in energy-efficient technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Global Competition & Overcapacity | -0.8% | Global, particularly Asia | Ongoing (2025-2033) |

| Supply Chain Disruptions & Logistics Issues | -0.7% | Global | Short to Mid-term (2025-2028) |

| High Energy Consumption & Cost Volatility | -0.6% | Global | Long-term (2025-2033) |

| Skilled Labor Shortage | -0.5% | Developed regions, select emerging markets | Mid to Long-term (2025-2033) |

Steel Bar Market - Updated Report Scope

This comprehensive report provides a detailed analysis of the global steel bar market, covering historical data, current market dynamics, and future projections. It segments the market by various types, materials, applications, and end-uses, offering a granular view of market performance and growth opportunities across key regions. The scope encompasses an in-depth assessment of market drivers, restraints, opportunities, and challenges, along with a competitive landscape analysis featuring key industry players and their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 150.2 Billion |

| Market Forecast in 2033 | USD 235.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, NSSMC (Nippon Steel & Sumitomo Metal), Baowu Steel Group, POSCO, JFE Steel Corporation, Hyundai Steel, Tata Steel, HBIS Group, Gerdau S.A., Nucor Corporation, Commercial Metals Company (CMC), EVRAZ plc, Steel Dynamics Inc., Acerinox S.A., Aperam S.A., thyssenkrupp AG, Caparo Industries Ltd., CELSA Group, Riva Group, Daewoo Steel Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The steel bar market is highly segmented based on various attributes including type, material, application, and end-use, reflecting the diverse requirements across industries. This segmentation highlights the specialized needs of different sectors and allows for a more granular understanding of market dynamics. Each segment exhibits unique growth drivers and market characteristics, ranging from general construction to highly specialized industrial applications.

By type, the market is broadly categorized into rebar, wire rod, merchant bar, and structural bar, with rebar dominating due to its extensive use in reinforced concrete. Material segmentation includes carbon steel, stainless steel, and alloy steel, each chosen for specific properties such as strength, corrosion resistance, or ductility. Application-wise, construction remains the largest consumer, but automotive, manufacturing, and energy sectors also represent significant demand pools for tailored steel bar products.

The end-use segmentation further refines the analysis, distinguishing between residential buildings, commercial structures, industrial facilities, and infrastructure projects like roads and bridges. This multi-faceted segmentation provides a comprehensive framework for market participants to identify lucrative niches, develop targeted strategies, and understand the intricate interplay of demand and supply across various market dimensions. The growth in specific end-use sectors, such as renewable energy installations, will increasingly influence the demand for specialized steel bar types.

- By Type: Rebar (Deformed Bar, Plain Bar), Wire Rod, Merchant Bar, Structural Bar, Flat Bar, Round Bar, Square Bar

- By Material: Carbon Steel Bar, Stainless Steel Bar, Alloy Steel Bar, Specialty Steel Bar

- By Application: Construction (Residential, Commercial, Industrial, Infrastructure), Automotive, Manufacturing & Fabrication, Oil & Gas, Energy, Mining, Aerospace, Agriculture

- By End-Use: Residential Buildings, Commercial Structures, Industrial Facilities, Roads & Bridges, Power Plants, Vehicle Manufacturing, Heavy Machinery, Pipelines

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for steel bars, driven by robust infrastructure development in China and India, rapid urbanization, and significant investments in residential and commercial construction. Countries like Indonesia, Vietnam, and Australia also contribute substantially to regional demand.

- North America: Characterized by mature markets with steady demand, primarily from infrastructure modernization projects, commercial building construction, and a strong automotive sector. Focus on high-quality and specialized steel bars, with increasing adoption of sustainable practices.

- Europe: A significant market with stringent environmental regulations, driving demand for green steel and advanced manufacturing techniques. Growth is supported by rebuilding and upgrading existing infrastructure, renewable energy projects, and a strong emphasis on circular economy principles in the construction industry.

- Latin America: Expected to witness moderate growth, fueled by urbanization trends, government investments in public infrastructure, and expanding industrial sectors in countries like Brazil and Mexico. Economic stability and foreign direct investment are key determinants of market expansion.

- Middle East and Africa (MEA): Emerging as a high-growth region due to ambitious infrastructure megaprojects, diversification initiatives away from oil, and rapid population growth in key countries such as Saudi Arabia, UAE, and South Africa. Demand is strong for both general construction and specialized industrial applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steel Bar Market.- ArcelorMittal

- NSSMC (Nippon Steel & Sumitomo Metal)

- Baowu Steel Group

- POSCO

- JFE Steel Corporation

- Hyundai Steel

- Tata Steel

- HBIS Group

- Gerdau S.A.

- Nucor Corporation

- Commercial Metals Company (CMC)

- EVRAZ plc

- Steel Dynamics Inc.

- Acerinox S.A.

- Aperam S.A.

- thyssenkrupp AG

- Caparo Industries Ltd.

- CELSA Group

- Riva Group

- Daewoo Steel Co. Ltd.

Frequently Asked Questions

What is a steel bar primarily used for?

Steel bars are primarily used as reinforcement in concrete structures within the construction industry. They provide tensile strength to concrete, preventing cracking and enhancing durability in buildings, bridges, roads, and other infrastructure projects. They are also vital in the automotive and manufacturing sectors for various components.

What are the key factors driving the growth of the steel bar market?

The steel bar market's growth is predominantly driven by global infrastructure development projects, rapid urbanization, and expansion in the residential and commercial construction sectors. Additionally, the increasing demand from the automotive and general manufacturing industries significantly contributes to market expansion.

What are the main types of steel bars available in the market?

The main types of steel bars include rebar (deformed and plain), wire rod, merchant bar, and structural bar. Each type is characterized by its shape, size, and intended application, ranging from concrete reinforcement to general fabrication and structural support.

How do environmental regulations impact the steel bar industry?

Environmental regulations impose significant challenges on the steel bar industry by necessitating investments in cleaner production technologies to reduce carbon emissions and manage waste. While increasing operational costs, these regulations also drive innovation towards more sustainable and green steel production methods.

What is the future outlook for the steel bar market?

The future outlook for the steel bar market is positive, with projected steady growth through 2033. This growth is supported by ongoing infrastructure development, urbanization, and advancements in manufacturing, despite challenges from raw material price volatility and intense competition. The shift towards sustainable practices and smart construction methods will also play a crucial role in its evolution.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted