Large Diameter Steel Pipe Market

Large Diameter Steel Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704018 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

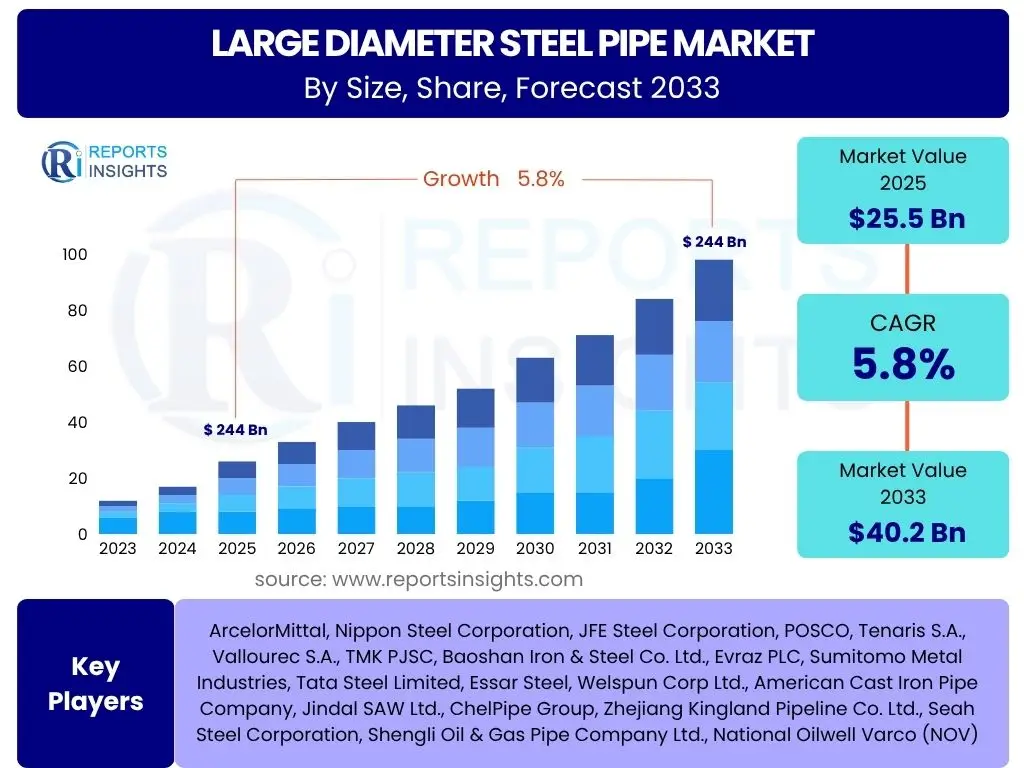

Large Diameter Steel Pipe Market Size

According to Reports Insights Consulting Pvt Ltd, The Large Diameter Steel Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 40.2 Billion by the end of the forecast period in 2033.

The large diameter steel pipe market exhibits a robust growth trajectory, primarily fueled by extensive global infrastructure development and increasing energy demands. These pipes are critical components in various sectors, including oil and gas transmission, water and wastewater management, and structural applications in construction. The market's expansion is intrinsically linked to substantial investments in cross-country pipelines, urban water supply networks, and industrial facilities, particularly in rapidly urbanizing economies and regions with growing industrial bases.

The consistent demand for reliable and durable large diameter steel pipes underscores their essential role in supporting vital economic activities worldwide. Their ability to transport large volumes of liquids and gases efficiently and safely makes them indispensable for both traditional and emerging applications. The forecast growth reflects sustained infrastructure initiatives, coupled with the need for upgrading and replacing aging pipeline systems globally, ensuring long-term stability and expansion in this specialized industrial segment.

Key Large Diameter Steel Pipe Market Trends & Insights

The Large Diameter Steel Pipe market is undergoing significant transformation driven by evolving industrial needs and technological advancements. A primary trend is the substantial investment in new energy infrastructure, including pipelines for natural gas, hydrogen, and carbon capture and storage (CCS) projects, reflecting a global shift towards diversified energy portfolios. Additionally, the increasing global population and urbanization are intensifying the demand for efficient water and wastewater management systems, necessitating extensive networks of large diameter pipes for distribution and collection. The focus on pipeline integrity and safety, driven by stringent regulatory frameworks and environmental concerns, is also a prominent trend, leading to the adoption of higher-grade materials and advanced monitoring technologies.

Another crucial insight points to the growing emphasis on sustainable manufacturing practices within the steel industry. This involves not only optimizing production processes to reduce carbon footprints but also exploring recyclable materials and enhancing the lifespan of pipes to minimize environmental impact. Furthermore, the market is witnessing a rise in customization and specialized pipe solutions tailored for extreme operating conditions, such as high-pressure, high-temperature, or corrosive environments. This trend is supported by advancements in metallurgy and welding techniques, allowing for the production of pipes with enhanced strength, durability, and corrosion resistance. The integration of digital technologies, including sensors and data analytics for real-time monitoring and predictive maintenance, is also emerging as a key development, optimizing operational efficiency and reducing downtime across various applications.

The market dynamics are also influenced by geopolitical considerations and trade policies, which can impact raw material supply chains and the overall cost structure of steel production. Companies are increasingly focusing on strategic partnerships and localized manufacturing to mitigate these risks and ensure supply chain resilience. The competitive landscape is characterized by a drive for innovation, with manufacturers investing in research and development to offer products that meet stringent international standards and performance requirements. This ongoing innovation ensures that large diameter steel pipes remain the preferred choice for critical infrastructure projects, adapting to new challenges and opportunities in a dynamic global environment.

- Expanding Oil and Gas Infrastructure: Significant investments in new pipeline projects for crude oil, natural gas, and refined products globally.

- Growing Water and Wastewater Management Needs: Increased demand for pipes in municipal water supply, irrigation, and sewage systems due to population growth and urbanization.

- Emergence of Hydrogen and CCS Pipelines: Development of infrastructure for transporting hydrogen and capturing carbon dioxide as part of decarbonization efforts.

- Focus on Pipeline Integrity and Safety: Adoption of advanced materials, coatings, and monitoring technologies to ensure long-term performance and prevent failures.

- Technological Advancements in Manufacturing: Improvements in steel grades, welding techniques, and non-destructive testing for enhanced pipe quality and durability.

- Urbanization and Industrialization: Sustained demand from large-scale construction projects and industrial facilities in developing economies.

- Emphasis on Sustainable Production: Drive towards eco-friendly manufacturing processes and recyclable materials to reduce environmental impact.

AI Impact Analysis on Large Diameter Steel Pipe

The integration of Artificial Intelligence (AI) is set to significantly transform various facets of the Large Diameter Steel Pipe market, addressing common user questions related to efficiency, quality, and operational intelligence. Users are keenly interested in how AI can optimize the complex manufacturing processes involved in pipe production, from raw material selection to final product inspection. AI algorithms can analyze vast datasets from historical production runs, identify optimal parameters for rolling, welding, and heat treatment, thereby minimizing defects, reducing material waste, and enhancing overall production efficiency. Predictive modeling capabilities of AI can anticipate equipment failures, enabling proactive maintenance and significantly reducing costly downtime, a critical concern for large-scale industrial operations.

Furthermore, AI plays a pivotal role in enhancing quality control and assurance for large diameter steel pipes. Computer vision systems powered by AI can perform highly accurate and consistent inspections for surface defects, dimensional deviations, and weld integrity at unprecedented speeds, surpassing human capabilities. This leads to superior product quality, reduced rework, and increased compliance with stringent industry standards. Beyond manufacturing, AI's impact extends to logistics and supply chain management, where intelligent algorithms can optimize inventory levels, forecast demand fluctuations, and streamline transportation routes, ensuring timely delivery and cost-effectiveness. This addresses user concerns about supply chain resilience and efficiency, particularly in a globalized market.

In the operational phase of pipelines, AI is poised to revolutionize monitoring and maintenance strategies. AI-driven sensor networks can provide real-time data on pipe conditions, detecting anomalies such as leaks, corrosion, or structural stress with high precision. Predictive maintenance schedules generated by AI can anticipate potential failures before they occur, allowing operators to intervene proactively and prevent catastrophic incidents. This not only enhances safety and reliability but also extends the operational lifespan of pipelines, offering substantial long-term cost savings. The adoption of AI in large diameter steel pipe applications is moving beyond theoretical concepts, with pilot projects demonstrating tangible benefits in terms of operational efficiency, quality improvement, and enhanced safety protocols, setting a new benchmark for industry standards.

- Optimized Manufacturing Processes: AI algorithms enhance rolling, welding, and heat treatment, reducing defects and improving efficiency.

- Predictive Maintenance: AI analyzes sensor data to forecast equipment failures, minimizing downtime in production facilities.

- Enhanced Quality Control: AI-powered computer vision systems automate and improve inspection for surface defects and weld integrity.

- Supply Chain Optimization: AI streamlines logistics, inventory management, and demand forecasting for raw materials and finished products.

- Real-time Pipeline Monitoring: AI-driven sensors detect anomalies, leaks, and corrosion in operational pipelines, ensuring safety and integrity.

- Smart Design and Simulation: AI assists in the design phase, optimizing pipe specifications for specific applications and stress conditions.

Key Takeaways Large Diameter Steel Pipe Market Size & Forecast

The Large Diameter Steel Pipe market is poised for significant expansion, driven by foundational global infrastructure needs and evolving energy landscapes. A key takeaway is the sustained demand originating from the traditional oil and gas sector, which continues to invest in new pipeline networks and the maintenance of existing ones. Simultaneously, the burgeoning renewable energy sector, particularly in hydrogen transportation and carbon capture, is opening up new avenues for growth, positioning large diameter steel pipes as essential conduits for future energy ecosystems. The forecast indicates robust growth, reflecting a market that is both resilient to conventional energy shifts and adaptable to emerging sustainable technologies, ensuring its foundational role in critical infrastructure projects worldwide.

Another crucial insight is the increasing emphasis on technological advancements and material innovation within the industry. Manufacturers are focusing on developing pipes with enhanced durability, corrosion resistance, and operational efficiency to meet stringent safety and environmental regulations. This includes the adoption of advanced steel grades, specialized coatings, and state-of-the-art welding techniques. Such innovations are vital for meeting the demanding requirements of deep-sea applications, extreme temperature environments, and high-pressure transmission lines, further solidifying the market's trajectory towards higher performance and reliability standards. The commitment to research and development underscores a strategic shift towards value-added products that can withstand challenging operational conditions over extended periods.

The market's future growth is also intricately linked to global urbanization and industrialization, particularly in developing regions. These areas are experiencing rapid expansion in municipal water infrastructure, industrial facilities, and transportation networks, all of which require substantial volumes of large diameter steel pipes. While geopolitical factors and raw material price volatility present challenges, the long-term fundamentals of infrastructure development and energy transition provide a strong underpinning for continuous market expansion. Companies that strategically invest in sustainable practices, advanced manufacturing capabilities, and efficient supply chain management are best positioned to capitalize on these enduring market drivers and navigate potential headwinds, ensuring sustained profitability and market share.

- Market Growth Driven by Infrastructure and Energy: Expected robust growth fueled by oil and gas, water, and emerging energy (hydrogen, CCS) projects.

- Technological Advancements are Critical: Innovations in materials, coatings, and manufacturing processes enhance pipe durability and performance.

- Sustainability and Regulations Influence Demand: Growing demand for environmentally friendly production and adherence to stringent safety standards.

- Geographic Expansion in Emerging Economies: Significant opportunities in Asia Pacific, Latin America, and Africa due to rapid urbanization.

- Supply Chain Resilience is Key: Navigating raw material price volatility and geopolitical risks is essential for market stability.

Large Diameter Steel Pipe Market Drivers Analysis

The Large Diameter Steel Pipe market is propelled by a confluence of macroeconomic trends and industry-specific demands that necessitate robust and extensive piping infrastructure. A primary driver is the ongoing global investment in oil and gas exploration, production, and transportation. Despite a push towards renewable energy, natural gas and crude oil remain foundational to the global energy mix, requiring vast networks of pipelines to deliver resources from production sites to consumption centers. This includes both new pipeline construction in untapped regions and the expansion or replacement of aging infrastructure in mature markets, ensuring a consistent demand for large diameter steel pipes capable of high-volume transmission over long distances.

Furthermore, rapid urbanization and industrial development, particularly across emerging economies, are significant catalysts for market growth. As populations concentrate in urban centers and industrial activities expand, there is an escalating need for sophisticated municipal infrastructure, including extensive water supply, wastewater treatment, and drainage systems. Large diameter steel pipes are indispensable for these applications, providing durable and reliable solutions for transporting vast quantities of water and effluents. The increasing demand for industrial process piping in sectors such as petrochemicals, mining, and power generation further reinforces the market's upward trajectory, driven by industrial output and economic growth.

The global energy transition, while a long-term shift, also presents unique drivers for the large diameter steel pipe market. The growing interest and investment in hydrogen transportation and carbon capture, utilization, and storage (CCUS) technologies require specialized pipeline infrastructure. These emerging applications necessitate pipes designed to handle specific pressures, temperatures, and corrosive properties of new energy carriers, driving innovation in material science and pipe manufacturing. The long-term commitment of various nations to achieving net-zero emissions, alongside significant investments in renewable energy projects, promises to unlock new segments for large diameter steel pipes as critical components for a sustainable future energy landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Investment in Oil & Gas Pipelines | +1.5% | Global, particularly Middle East, North America, Russia | 2025-2033 |

| Expanding Water Infrastructure Projects | +1.2% | Asia Pacific (China, India), MEA, Latin America | 2025-2033 |

| Growth in Renewable Energy (Hydrogen, CCS) | +0.8% | Europe, North America, Australia | 2027-2033 |

| Urbanization and Industrial Development | +0.7% | Asia Pacific (Southeast Asia), Latin America, Africa | 2025-2030 |

| Replacement of Aging Infrastructure | +0.6% | North America, Europe | 2025-2033 |

Large Diameter Steel Pipe Market Restraints Analysis

The Large Diameter Steel Pipe market faces several significant restraints that could potentially impede its growth trajectory. One of the most prominent challenges is the inherent volatility of raw material prices, particularly for steel and its alloying elements. Steel production is highly dependent on iron ore, coking coal, and scrap, whose prices are subject to global supply-demand dynamics, geopolitical events, and economic fluctuations. Unpredictable and sharp increases in these costs directly impact the manufacturing expenses of large diameter pipes, often leading to higher end-product prices, which can deter investment in new projects or squeeze profit margins for manufacturers and project developers alike. This price instability makes long-term project planning and budgeting particularly challenging for stakeholders across the value chain.

Another considerable restraint comes from increasingly stringent environmental regulations and public opposition to new pipeline projects. Governments worldwide are implementing stricter environmental impact assessments, permitting processes, and emission standards for industrial activities, including steel production and pipeline construction. Public awareness and activism against fossil fuel infrastructure or projects perceived as environmentally damaging can lead to delays, increased compliance costs, or even outright cancellation of major pipeline initiatives. While these regulations are crucial for sustainability, they add complexity and cost to project development, potentially shifting investments towards alternative energy sources that do not rely as heavily on extensive pipeline networks.

Furthermore, the emergence and increasing adoption of alternative materials, such as high-density polyethylene (HDPE) and composite pipes, particularly for certain applications like water and less demanding gas distribution, pose a competitive threat. While steel remains superior for high-pressure, large-volume, and structural applications, advancements in polymer and composite technologies offer viable alternatives for specific segments, often with advantages in terms of corrosion resistance, lighter weight, and easier installation. Although these alternatives currently occupy a niche, their expanding application scope could gradually erode market share for steel pipes in less critical or specific project types. These competitive pressures compel steel pipe manufacturers to continuously innovate and emphasize the superior characteristics of steel for heavy-duty applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Steel) | -0.7% | Global | 2025-2029 |

| Stringent Environmental Regulations and Public Opposition | -0.5% | Europe, North America, Australia | 2025-2033 |

| Competition from Alternative Materials (Plastics, Composites) | -0.4% | North America, Europe, parts of Asia | 2028-2033 |

| Geopolitical Instability and Trade Barriers | -0.3% | Global, particularly affecting trade routes | 2025-2028 |

| High Capital Expenditure for Manufacturing | -0.2% | Global | 2025-2033 |

Large Diameter Steel Pipe Market Opportunities Analysis

The Large Diameter Steel Pipe market is presented with several promising opportunities that can significantly drive future growth and innovation. One major opportunity lies in the burgeoning investment in new energy infrastructure, particularly projects related to hydrogen transportation and carbon capture, utilization, and storage (CCUS). As nations commit to decarbonization goals, the development of robust pipeline networks for these novel energy carriers becomes imperative. Large diameter steel pipes are ideally suited for these applications due to their inherent strength, durability, and ability to withstand high pressures, positioning them at the forefront of the global energy transition. This opens up a specialized, high-value market segment that requires tailored pipe solutions and advanced material specifications.

Furthermore, substantial opportunities exist in emerging markets, especially across Asia Pacific, Africa, and Latin America, where rapid industrialization and urbanization are fueling demand for comprehensive infrastructure development. These regions require significant investments in new municipal water supply systems, sewage networks, and industrial pipelines to support economic expansion and improve living standards. As these economies grow, the need for large-scale, durable piping solutions for water, energy, and industrial processes will continue to escalate, offering manufacturers extensive untapped markets. Companies that establish strong local presence and adapt their offerings to regional specificities stand to gain substantial market share in these high-growth areas.

Technological advancements and the embrace of digital transformation also represent key opportunities. The adoption of advanced manufacturing techniques, such as additive manufacturing for specialized components, and the integration of smart technologies like sensors, IoT, and AI into pipeline systems, can enhance operational efficiency, safety, and predictive maintenance capabilities. Developing pipes with integrated sensing capabilities or offering comprehensive digital monitoring solutions as part of a product-service package can create new revenue streams and competitive advantages. Moreover, the increasing focus on sustainable practices, including the use of recycled steel and development of greener production methods, can differentiate manufacturers and appeal to environmentally conscious clients, aligning with global corporate social responsibility goals and long-term market trends.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Advanced Manufacturing Technologies | +1.0% | Global, particularly developed economies | 2027-2033 |

| Emerging Markets for Infrastructure Development | +0.9% | Asia Pacific, Africa, Latin America | 2025-2033 |

| Hydrogen Transportation and Carbon Capture Pipelines | +0.7% | Europe, North America, Australia, Japan | 2028-2033 |

| Smart Pipeline Systems and IoT Integration | +0.6% | Global | 2026-2033 |

| Expansion in Desalination and Water Reuse Projects | +0.5% | Middle East, North Africa, arid regions globally | 2025-2033 |

Large Diameter Steel Pipe Market Challenges Impact Analysis

The Large Diameter Steel Pipe market faces several persistent challenges that require strategic responses from manufacturers and stakeholders. One significant challenge pertains to the aging global infrastructure, particularly in mature economies. While this presents opportunities for replacement, the sheer scale and cost associated with upgrading or replacing vast networks of deteriorating pipelines for oil, gas, and water are immense. Financing these mega-projects often involves complex public-private partnerships, navigating bureaucratic hurdles, and dealing with lengthy approval processes. The deferred maintenance in many regions means that urgent replacement needs often clash with budgetary constraints, slowing down potential market activity for new pipe installations despite the clear necessity.

Another critical challenge is the persistent issue of skilled labor shortages across the value chain, from steel production and pipe manufacturing to pipeline installation and maintenance. The highly specialized nature of large diameter steel pipe production and deployment demands a workforce with specific welding, engineering, and project management expertise. A dwindling pool of experienced professionals, coupled with a lack of new entrants into these technical trades, poses a bottleneck for project execution and can lead to increased labor costs and project delays. Addressing this requires significant investment in vocational training, educational partnerships, and attractive career pathways to cultivate the next generation of skilled workers necessary for the industry's sustained growth.

Furthermore, global supply chain disruptions, exemplified by recent events such as the COVID-19 pandemic and geopolitical conflicts, pose significant challenges to the Large Diameter Steel Pipe market. These disruptions can lead to unpredictable delays in the delivery of raw materials, components, and even finished pipes, impacting production schedules and project timelines. Trade protectionism and tariffs also contribute to supply chain complexities and can increase the landed cost of pipes, making international trade less predictable and more expensive. Manufacturers must therefore focus on building more resilient and diversified supply chains, potentially through regionalized sourcing or greater vertical integration, to mitigate these external risks and maintain operational continuity in a turbulent global economic landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Infrastructure and Replacement Costs | -0.6% | North America, Europe, Russia | 2025-2030 |

| Skilled Labor Shortages | -0.4% | Global, particularly developed economies | 2025-2033 |

| Supply Chain Disruptions and Trade Barriers | -0.3% | Global | 2025-2027 |

| Ensuring Long-Term Corrosion Resistance and Durability | -0.2% | Global, especially coastal and harsh environments | 2025-2033 |

| Intense Competition and Price Pressure | -0.1% | Global | 2025-2033 |

Large Diameter Steel Pipe Market - Updated Report Scope

This comprehensive market research report on the Large Diameter Steel Pipe market provides an in-depth analysis of industry trends, market dynamics, and future projections. The scope of the report encompasses a detailed examination of market size and growth, segmented by various critical parameters such as type, material, application, and end-use industry. It offers a robust framework for understanding the market's current state and its potential trajectory over the forecast period, leveraging extensive primary and secondary research to ensure data accuracy and reliability. The analysis includes a thorough assessment of market drivers, restraints, opportunities, and challenges, providing a holistic view of the forces shaping the industry landscape and enabling strategic decision-making for stakeholders.

The report also delves into the competitive environment, profiling key players and evaluating their strategies, product offerings, and market presence. Regional analyses are a significant component, highlighting market performance and growth prospects across major geographical segments, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Special attention is paid to emerging trends such as the impact of artificial intelligence on manufacturing and operational processes, and the implications of the global energy transition, including hydrogen and carbon capture infrastructure. This detailed segmentation and regional focus allow for a nuanced understanding of market dynamics specific to different industrial and geographical contexts, supporting targeted market entry and expansion strategies.

Ultimately, the report serves as an invaluable resource for manufacturers, suppliers, investors, and policymakers seeking to gain actionable insights into the Large Diameter Steel Pipe market. It provides a forward-looking perspective, forecasting market values and growth rates, and identifies critical success factors for navigating the evolving industry landscape. The inclusion of an updated report scope with specific data points, key trends, and a comprehensive list of market segments and companies ensures that readers receive a precise and well-structured overview, enabling them to make informed strategic choices and capitalize on emerging opportunities within this vital industrial sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 40.2 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, JFE Steel Corporation, POSCO, Tenaris S.A., Vallourec S.A., TMK PJSC, Baoshan Iron & Steel Co. Ltd., Evraz PLC, Sumitomo Metal Industries, Tata Steel Limited, Essar Steel, Welspun Corp Ltd., American Cast Iron Pipe Company, Jindal SAW Ltd., ChelPipe Group, Zhejiang Kingland Pipeline Co. Ltd., Seah Steel Corporation, Shengli Oil & Gas Pipe Company Ltd., National Oilwell Varco (NOV) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Large Diameter Steel Pipe market is extensively segmented to provide a granular understanding of its diverse applications and product categories, reflecting the complexity and varied demands across industries. This segmentation facilitates a detailed analysis of market dynamics, allowing stakeholders to identify specific growth areas, competitive landscapes, and technological preferences within each sub-segment. The market is primarily categorized by pipe type, material composition, end-use application, and the specific end-use industry, each offering unique insights into demand drivers and technological requirements. Understanding these distinctions is crucial for manufacturers to tailor their production, for suppliers to optimize their distribution channels, and for investors to pinpoint lucrative investment opportunities.

The segmentation by pipe type distinguishes between seamless and welded pipes, with welded pipes further broken down into Electric Resistance Welded (ERW), Longitudinal Submerged Arc Welded (LSAW), and Spiral Submerged Arc Welded (SSAW). Each type possesses distinct manufacturing processes, cost implications, and performance characteristics, making them suitable for different pressure ratings, diameters, and lengths. Material segmentation, encompassing carbon steel, alloy steel, and stainless steel, highlights the importance of material properties such as strength, corrosion resistance, and temperature tolerance, which dictate their suitability for various demanding environments and applications. These classifications directly influence the market's overall value proposition and technological evolution.

Furthermore, the segmentation by application—including oil & gas transmission (both onshore and offshore), water & wastewater management, chemical & petrochemical processing, mining, and infrastructure & construction (for piling and structural uses)—reveals the diverse sectors reliant on large diameter steel pipes. Each application has specific requirements concerning pipe diameter, pressure rating, coating, and regulatory compliance. The end-use industry segmentation provides a broader categorization, such as energy, industrial, and municipal, helping to understand overarching demand patterns. This multi-layered segmentation ensures a comprehensive market overview, enabling precise market positioning and strategic development for companies operating within or looking to enter this essential industrial component market.

- By Type:

- Seamless

- Welded

- Electric Resistance Welded (ERW)

- Longitudinal Submerged Arc Welded (LSAW)

- Spiral Submerged Arc Welded (SSAW)

- By Material:

- Carbon Steel

- Alloy Steel

- Stainless Steel

- By Application:

- Oil & Gas Transmission

- Onshore

- Offshore

- Water & Wastewater

- Chemical & Petrochemical

- Mining

- Infrastructure & Construction

- Piling

- Structural

- Others

- Oil & Gas Transmission

- By End-Use Industry:

- Energy (Oil & Gas, Power Generation)

- Industrial (Manufacturing, Chemicals)

- Municipal

- Others

Regional Highlights

The global Large Diameter Steel Pipe market exhibits significant regional variations in demand, driven by differing infrastructure development priorities, energy policies, and economic growth rates. Asia Pacific stands out as a dominant and rapidly expanding market, primarily fueled by extensive urbanization, industrialization, and massive infrastructure projects in countries such as China, India, and Southeast Asian nations. The region's robust economic growth translates into substantial investments in water supply networks, wastewater treatment facilities, and energy pipelines, positioning it as a key driver for market expansion over the forecast period. The growing demand for raw materials and energy in this region further stimulates the need for large diameter pipes for transportation and processing.

North America and Europe represent mature markets characterized by significant existing infrastructure and a strong emphasis on maintenance, replacement, and modernization. In North America, the ongoing development of shale oil and gas resources, coupled with the need to upgrade aging pipeline networks, contributes substantially to market demand. Europe, while increasingly focused on renewable energy and decarbonization, still requires large diameter steel pipes for traditional energy infrastructure, as well as for emerging applications such as hydrogen and carbon capture pipelines. Both regions benefit from stringent safety standards and a push towards advanced materials and technologies, fostering demand for high-quality and specialized pipe solutions.

The Middle East and Africa (MEA) region is critically important due to its vast oil and gas reserves and ongoing mega-projects in infrastructure development. Countries in the Middle East, particularly Saudi Arabia and UAE, are investing heavily in expanding their oil and gas export capabilities, as well as diversifying their economies through new industrial and urban development projects, creating a high demand for large diameter steel pipes. Africa, on the other hand, presents significant long-term growth potential as countries develop their natural resources and invest in fundamental infrastructure like water supply and power generation. Latin America also contributes to market growth, driven by investments in mining, oil and gas, and public utility projects, particularly in countries like Brazil and Mexico. Each region's unique economic and geopolitical landscape shapes its specific demand patterns for large diameter steel pipes, underscoring the market's global and diverse nature.

- Asia Pacific (APAC): Dominant and fastest-growing region due to rapid urbanization, industrialization, and massive infrastructure investments in China, India, and Southeast Asia. Significant demand from energy and water sectors.

- North America: Mature market with strong demand from shale oil and gas development, extensive pipeline network upgrades, and water infrastructure rehabilitation projects. Focus on high-grade materials and advanced technologies.

- Europe: Stable demand driven by the replacement of aging infrastructure, gas pipeline networks, and emerging investments in hydrogen and carbon capture transportation. Stringent environmental and safety regulations influence product specifications.

- Middle East and Africa (MEA): Key region driven by substantial oil and gas pipeline projects, especially in the Middle East, and growing infrastructure development in major African economies. Desalination plants also contribute to water pipeline demand.

- Latin America: Growing market supported by investments in mining, oil and gas exploration, and public utility projects in countries like Brazil, Mexico, and Argentina. Infrastructure development for industrial and municipal needs fuels demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Large Diameter Steel Pipe Market.- ArcelorMittal

- Nippon Steel Corporation

- JFE Steel Corporation

- POSCO

- Tenaris S.A.

- Vallourec S.A.

- TMK PJSC

- Baoshan Iron & Steel Co. Ltd.

- Evraz PLC

- Sumitomo Metal Industries

- Tata Steel Limited

- Essar Steel

- Welspun Corp Ltd.

- American Cast Iron Pipe Company

- Jindal SAW Ltd.

- ChelPipe Group

- Zhejiang Kingland Pipeline Co. Ltd.

- Seah Steel Corporation

- Shengli Oil & Gas Pipe Company Ltd.

- National Oilwell Varco (NOV)

Frequently Asked Questions

What factors are driving the Large Diameter Steel Pipe Market growth?

The market growth is primarily driven by increasing global investments in oil and gas transmission pipelines, rapid expansion of water and wastewater infrastructure due to urbanization, and emerging demand from renewable energy projects, particularly for hydrogen and carbon capture transport. Additionally, the need for replacing aging infrastructure globally contributes significantly to sustained demand.

How will environmental regulations impact the Large Diameter Steel Pipe market?

Environmental regulations impose stricter standards on pipeline construction, operation, and steel manufacturing, leading to increased compliance costs and potential project delays. While challenging, these regulations also drive innovation in sustainable production methods and the development of more durable, corrosion-resistant pipes, ensuring higher environmental safety and efficiency.

What role does technology play in the Large Diameter Steel Pipe market?

Technology is crucial for enhancing manufacturing efficiency through advanced welding and material processes, improving product quality via AI-powered inspection systems, and optimizing pipeline operations with IoT-enabled monitoring for predictive maintenance. These technological advancements lead to safer, more reliable, and cost-effective pipe solutions.

Which regions are key contributors to Large Diameter Steel Pipe market expansion?

Asia Pacific is a leading contributor due to rapid industrialization and urbanization. North America and Europe are significant for infrastructure maintenance and energy projects. The Middle East and Africa contribute substantially through extensive oil and gas developments and foundational infrastructure expansion, driving global market growth.

What are the primary applications for large diameter steel pipes?

Large diameter steel pipes are predominantly used in oil and gas transmission for crude oil, natural gas, and refined products. Other critical applications include municipal water supply and wastewater management, chemical and petrochemical processing, mining operations, and structural components in large-scale infrastructure and construction projects such as piling.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted