Spinal Implant and Device Market

Spinal Implant and Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704083 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

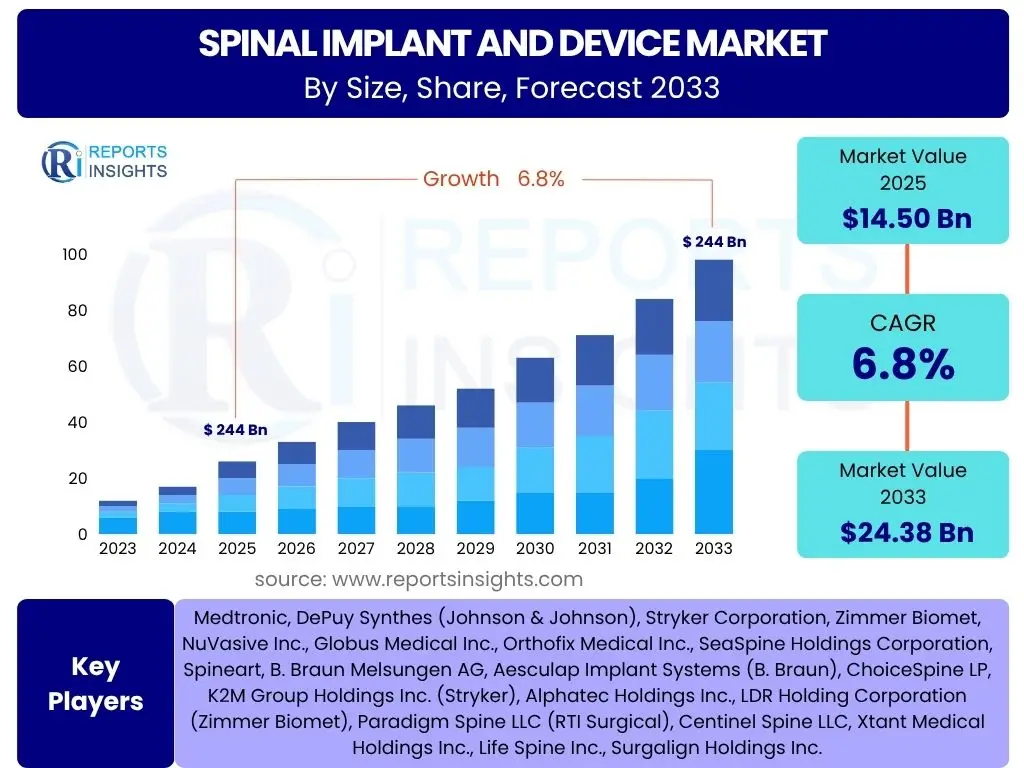

Spinal Implant and Device Market Size

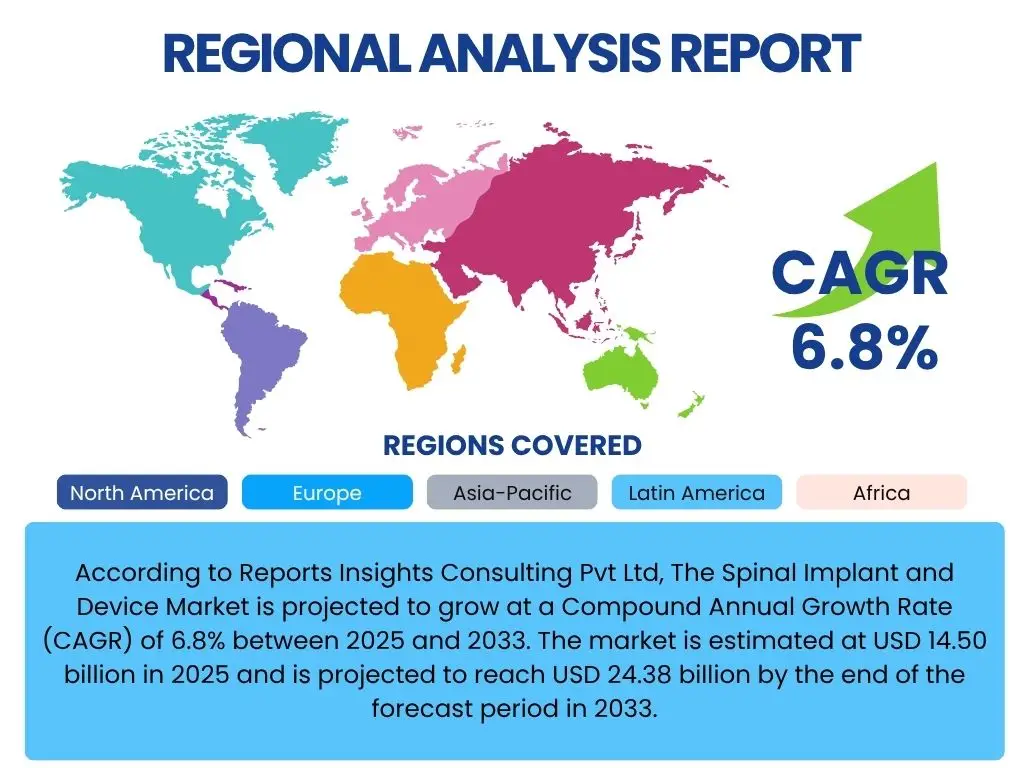

According to Reports Insights Consulting Pvt Ltd, The Spinal Implant and Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 14.50 billion in 2025 and is projected to reach USD 24.38 billion by the end of the forecast period in 2033.

This substantial growth is primarily driven by an increasing global geriatric population, which is more susceptible to degenerative spinal conditions, alongside a rising prevalence of spinal disorders such as scoliosis, kyphosis, and spinal stenosis. Advancements in surgical techniques and biomaterials are also playing a crucial role in expanding the market's reach and effectiveness.

The market's expansion is further supported by a growing demand for minimally invasive spinal procedures, which offer benefits such as reduced recovery times, less post-operative pain, and lower risks of complications compared to traditional open surgeries. These factors collectively contribute to the robust forecast for the spinal implant and device sector, indicating continued innovation and adoption in healthcare systems worldwide.

Key Spinal Implant and Device Market Trends & Insights

The spinal implant and device market is undergoing significant transformation, driven by a confluence of technological advancements, evolving patient demographics, and changing healthcare paradigms. A predominant trend is the shift towards minimally invasive surgical (MIS) techniques, which are gaining widespread acceptance due to their patient-centric benefits, including shorter hospital stays, reduced blood loss, and faster recovery. This is fostering innovation in implant design and delivery systems tailored for MIS procedures.

Another critical insight is the increasing demand for personalized and patient-specific implants, facilitated by advancements in 3D printing and additive manufacturing. These technologies allow for the creation of custom implants that precisely fit individual patient anatomies, potentially leading to improved surgical outcomes and reduced revision rates. Furthermore, the integration of smart technologies, such as sensors and robotics, into spinal surgery is enhancing precision and safety, paving the way for more sophisticated and effective treatments.

The market is also witnessing a growing focus on biologics and regenerative medicine, particularly in spinal fusion procedures, aiming to enhance bone growth and fusion rates. This includes the use of bone morphogenetic proteins (BMPs), bone marrow aspirate (BMA), and stem cell therapies. The convergence of these trends underscores a dynamic market striving for less invasive, more personalized, and highly effective solutions for a broad spectrum of spinal conditions.

- Minimally Invasive Spinal (MIS) Surgery Adoption: Increasing preference for less invasive procedures due to reduced patient trauma and quicker recovery.

- Personalized and 3D-Printed Implants: Growth in custom-made implants tailored to individual patient anatomy, improving fit and outcomes.

- Integration of Robotics and Navigation Systems: Enhanced precision, safety, and reproducibility in spinal surgical procedures.

- Advancements in Biologics and Regenerative Therapies: Focus on improving fusion rates and promoting natural healing processes.

- Expansion of Telemedicine and Remote Monitoring: Facilitating pre-operative planning and post-operative follow-up, especially in remote areas.

- Rise of Non-Fusion Technologies: Increasing interest in motion-preserving and dynamic stabilization devices as alternatives to traditional fusion.

- Data Analytics and AI for Surgical Planning: Leveraging large datasets for predictive modeling and optimizing surgical strategies.

AI Impact Analysis on Spinal Implant and Device

Artificial intelligence (AI) is poised to revolutionize the spinal implant and device market by enhancing precision, efficiency, and personalization across the entire patient journey. Users commonly inquire about AI's role in improving surgical outcomes, streamlining diagnostics, and developing next-generation implants. AI algorithms can analyze vast amounts of patient data, including imaging, genetics, and clinical history, to provide highly accurate diagnoses and predict treatment responses, thereby guiding surgeons in selecting the most appropriate implants and surgical approaches.

In the operating room, AI-powered robotics and navigation systems are transforming spinal surgery by offering unparalleled precision and reducing human error. These systems can assist with pre-operative planning, intra-operative guidance, and real-time monitoring, leading to more consistent and safer procedures. The application of machine learning in implant design is also accelerating the development of innovative devices, optimizing their biomechanical properties and improving long-term efficacy.

Beyond surgery, AI contributes significantly to post-operative care and patient management through remote monitoring and predictive analytics. This allows for early detection of complications, personalized rehabilitation plans, and improved patient adherence to treatment protocols. While concerns about data privacy, regulatory hurdles, and the learning curve for adoption exist, the overarching sentiment is that AI will be a transformative force, driving significant advancements and ultimately improving patient quality of life in spinal care.

- Enhanced Diagnostic Accuracy: AI algorithms improve interpretation of medical images (X-rays, MRI, CT) for precise spinal condition diagnosis.

- Personalized Treatment Planning: AI analyzes patient data to recommend optimal surgical strategies and implant selections.

- Robotics and Navigation Systems: AI-powered robots assist in precise implant placement and complex spinal surgeries, reducing human error.

- Predictive Analytics for Outcomes: AI models forecast surgical success rates and potential complications based on patient profiles.

- Optimized Implant Design: Machine learning algorithms accelerate the development of biomechanically superior and patient-specific implants.

- Post-operative Monitoring and Rehabilitation: AI-driven wearables and platforms track recovery, detect issues, and customize therapy plans.

- Streamlined Workflow and Efficiency: AI automates administrative tasks and optimizes resource allocation in spinal care facilities.

Key Takeaways Spinal Implant and Device Market Size & Forecast

The spinal implant and device market is on a robust growth trajectory, fundamentally driven by an aging global population and a surge in spinal degenerative disorders. A primary takeaway is the significant shift towards less invasive surgical interventions, which are enhancing patient recovery and expanding the pool of eligible patients for surgical treatment. This trend is fostering continuous innovation in implant technology and surgical tools, making procedures safer and more effective.

Another crucial insight is the increasing influence of advanced technologies such as 3D printing, artificial intelligence, and robotics. These innovations are not only enabling the creation of highly customized implants but also elevating the precision and safety of spinal surgeries. The market is becoming increasingly competitive, with a strong emphasis on research and development to introduce next-generation solutions that address unmet clinical needs and improve long-term patient outcomes.

Furthermore, the market's future growth will be significantly shaped by factors such as healthcare expenditure trends, regulatory landscape evolution, and the expansion into emerging economies. While North America and Europe currently dominate, the Asia Pacific region is expected to exhibit the fastest growth due to improving healthcare infrastructure, rising medical tourism, and increasing awareness about advanced spinal treatments. These combined factors underscore a dynamic and evolving market with substantial opportunities for innovation and expansion.

- Significant Market Expansion: Projected robust growth driven by demographics and increasing prevalence of spinal conditions.

- Dominance of Minimally Invasive Procedures: Continual shift towards less invasive techniques as a key driver for market innovation and adoption.

- Technological Advancements as Core Growth Enablers: AI, robotics, and 3D printing are transforming diagnostics, surgical precision, and implant design.

- Focus on Patient-Centric Solutions: Emphasis on personalized implants and therapies for improved patient outcomes and satisfaction.

- High Investment in R&D: Continuous innovation is essential for competitive advantage and addressing evolving clinical demands.

- Emerging Markets as Growth Hotspots: Asia Pacific and Latin America offer substantial untapped potential due to improving healthcare access.

- Regulatory Compliance and Reimbursement Challenges: Ongoing factors influencing market entry and product commercialization.

Spinal Implant and Device Market Drivers Analysis

The spinal implant and device market is significantly propelled by several key factors. The escalating global geriatric population is a primary driver, as age-related degenerative spinal conditions become more prevalent, necessitating surgical interventions. Concurrently, the rising incidence of spinal disorders such as scoliosis, herniated discs, and spinal trauma due to changing lifestyles and increasing awareness further fuels the demand for advanced treatment options. Technological advancements, particularly in minimally invasive surgical techniques and the development of innovative biomaterials, also play a pivotal role in expanding the market by offering safer and more effective solutions.

Increased healthcare expenditure and improving healthcare infrastructure globally, especially in emerging economies, are contributing to greater access to spinal care and advanced surgical procedures. Furthermore, growing patient awareness regarding available treatment options and the benefits of modern spinal surgeries is driving higher adoption rates. The shift towards value-based healthcare models also encourages the development of cost-effective yet high-quality implants, promoting market growth and innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Population & Spinal Disorders | +2.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements (MIS, Biomaterials) | +2.0% | Global, High-income countries leading adoption | Mid to Long-term (2025-2033) |

| Increased Healthcare Expenditure | +1.5% | Emerging Economies (APAC, Latin America), Developed Nations | Mid to Long-term (2025-2033) |

| Growing Awareness & Patient Acceptance | +0.8% | Global, particularly urban areas | Mid-term (2025-2029) |

Spinal Implant and Device Market Restraints Analysis

Despite robust growth, the spinal implant and device market faces several significant restraints that could impede its expansion. The high cost associated with spinal implants and surgical procedures remains a major barrier, particularly in developing regions where healthcare budgets are limited and affordability is a key concern. This often leads to limited accessibility for a significant portion of the population.

Stringent regulatory approval processes for new devices and technologies, especially in markets like the United States and Europe, pose substantial challenges. These extensive and time-consuming approval pathways can delay market entry for innovative products and increase development costs, affecting manufacturers' ability to rapidly introduce new solutions. Furthermore, complications and failures associated with spinal surgeries, such as infection, implant loosening, or pseudarthrosis, can deter both patients and healthcare providers, potentially slowing down adoption rates. Reimbursement policies, which vary significantly by region and insurance provider, also play a critical role, as unfavorable policies can limit the financial viability of certain procedures for hospitals and patients.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implants & Procedures | -1.8% | Global, particularly developing nations | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -1.5% | North America, Europe | Long-term (2025-2033) |

| Post-operative Complications & Failures | -1.0% | Global | Mid-term (2025-2029) |

| Limited Reimbursement Policies | -0.7% | Regional variations, specific countries | Mid to Long-term (2025-2033) |

Spinal Implant and Device Market Opportunities Analysis

Significant opportunities exist within the spinal implant and device market, particularly in the expansion into emerging economies. Countries in Asia Pacific, Latin America, and the Middle East and Africa are characterized by rapidly developing healthcare infrastructure, increasing disposable incomes, and a growing medical tourism sector. These regions represent largely untapped markets with considerable potential for increased adoption of advanced spinal technologies and procedures.

The advent of personalized medicine and additive manufacturing, specifically 3D printing, offers a transformative opportunity for highly customized implants. This allows for the creation of patient-specific devices that can significantly improve surgical outcomes and reduce complications, catering to unique anatomical needs. Furthermore, the burgeoning field of regenerative medicine, including cell therapies and biologics for spinal repair, presents a long-term growth opportunity by offering novel approaches to treat degenerative conditions and enhance spinal fusion, moving beyond traditional mechanical fixation.

Additionally, the increasing integration of digital health solutions, such as remote monitoring platforms and telemedicine for pre- and post-operative care, creates new avenues for market players. These solutions can enhance patient access, optimize care delivery, and improve patient adherence, thereby expanding the reach and efficiency of spinal care. The development of non-fusion and motion-preserving technologies also presents a strong opportunity as they address the limitations of traditional fusion surgeries and cater to a growing patient preference for maintaining spinal mobility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets | +2.0% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Personalized & 3D-Printed Implants | +1.8% | Global, especially developed nations | Mid to Long-term (2025-2033) |

| Regenerative Medicine & Biologics | +1.5% | Global, R&D intensive regions | Long-term (2025-2033) |

| Non-Fusion & Motion Preservation Technologies | +1.2% | Global, increasing patient preference | Mid to Long-term (2025-2033) |

| Integration of Digital Health Solutions | +0.9% | Global, enhanced connectivity | Short to Mid-term (2025-2029) |

Spinal Implant and Device Market Challenges Impact Analysis

The spinal implant and device market faces several challenges that can impact its growth trajectory. The complex and often lengthy clinical trial and regulatory approval processes for new devices represent a significant hurdle. Meeting stringent safety and efficacy requirements, especially for innovative technologies, can be time-consuming and expensive, delaying market entry and increasing development costs for manufacturers.

Another challenge stems from the competitive landscape, which is characterized by the presence of numerous established players and emerging innovators. Intense competition often leads to pricing pressures, impacting profit margins and necessitating continuous differentiation through product innovation and superior clinical outcomes. Furthermore, the requirement for highly skilled surgeons and specialized training programs for advanced spinal procedures can limit the widespread adoption of certain cutting-edge technologies, particularly in regions with a shortage of trained medical professionals.

Supply chain disruptions, as experienced recently, can also pose a considerable challenge, affecting the availability of critical raw materials, components, and finished products. Ensuring robust and resilient supply chains is crucial for maintaining market stability and meeting demand. Additionally, ethical considerations surrounding the use of advanced technologies like AI and the implications of long-term implant performance present ongoing challenges that require careful navigation and robust post-market surveillance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory & Clinical Pathways | -1.3% | Global, particularly developed markets | Long-term (2025-2033) |

| Intense Market Competition & Pricing Pressure | -1.0% | Global | Long-term (2025-2033) |

| Shortage of Skilled Surgeons & Training Needs | -0.8% | Global, varies by region | Long-term (2025-2033) |

| Supply Chain Disruptions | -0.5% | Global | Short to Mid-term (2025-2027) |

| Ethical & Long-term Performance Considerations | -0.3% | Global | Long-term (2025-2033) |

Spinal Implant and Device Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Spinal Implant and Device Market, covering historical performance from 2019 to 2023 and offering detailed forecasts from 2025 to 2033. The scope encompasses a thorough examination of market size estimations, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory. It further dissects the market by various segments, including product type, procedure, material, and end-use, providing granular insights into each category's contribution to overall market dynamics. The report also highlights regional market performances and competitive landscapes, featuring profiles of key market players to offer a holistic understanding of the industry's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.50 Billion |

| Market Forecast in 2033 | USD 24.38 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet, NuVasive Inc., Globus Medical Inc., Orthofix Medical Inc., SeaSpine Holdings Corporation, Spineart, B. Braun Melsungen AG, Aesculap Implant Systems (B. Braun), ChoiceSpine LP, K2M Group Holdings Inc. (Stryker), Alphatec Holdings Inc., LDR Holding Corporation (Zimmer Biomet), Paradigm Spine LLC (RTI Surgical), Centinel Spine LLC, Xtant Medical Holdings Inc., Life Spine Inc., Surgalign Holdings Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Spinal Implant and Device Market is broadly segmented based on product type, procedure, material, and end-use, each playing a crucial role in shaping market dynamics. The product type segment is dominated by spinal fusion devices, which continue to be the gold standard for treating various spinal instabilities and deformities, further categorized into thoracolumbar, cervical fixation, interbody fusion devices, and biologics. Non-fusion devices, including dynamic stabilization, artificial discs, and VCF devices, are gaining traction as alternatives, offering motion preservation and addressing specific patient needs.

Procedurally, the market is undergoing a significant transition from traditional open surgeries to minimally invasive spinal (MIS) procedures. MIS techniques are favored due to their numerous benefits, such as reduced incision size, less muscle dissection, lower blood loss, shorter hospital stays, and quicker patient recovery, driving their increasing adoption globally. Material-wise, titanium and its alloys remain widely used due to their biocompatibility and strength, while PEEK (Polyetheretherketone) is gaining prominence for its radiolucency and elastic modulus similar to bone, offering advantages in post-operative imaging.

In terms of end-use, hospitals represent the largest segment due to their comprehensive infrastructure and capacity for complex surgical procedures. However, ambulatory surgical centers (ASCs) are emerging as significant growth centers, particularly for less complex spinal surgeries, owing to their cost-effectiveness and efficiency. Specialty clinics also contribute to market demand by offering specialized diagnostic and therapeutic services. This multi-faceted segmentation provides a granular view of market trends and consumer preferences across different applications and settings.

- By Product Type:

- Spinal Fusion Devices: Thoracolumbar Devices, Cervical Fixation Devices, Interbody Fusion Devices, Biologics

- Non-Fusion Devices: Dynamic Stabilization Devices, Artificial Discs (Cervical, Lumbar), Vertebral Compression Fracture (VCF) Devices, Bone Graft Substitutes, Spinal Bone Stimulators

- By Procedure:

- Open Surgery

- Minimally Invasive Surgery (MIS)

- By Material:

- Titanium

- Stainless Steel

- PEEK

- Others (e.g., Cobalt-Chrome, Polyethylene)

- By End-Use:

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

Regional Highlights

- North America: Dominates the global market share, attributed to the presence of technologically advanced healthcare infrastructure, high prevalence of spinal disorders, robust reimbursement policies, and significant investments in research and development by key market players. The U.S. leads in adoption of innovative spinal technologies.

- Europe: A mature market characterized by an aging population, increasing incidence of chronic spinal conditions, and well-established healthcare systems. Countries like Germany, the UK, and France are key contributors, with a strong focus on clinical research and the adoption of minimally invasive techniques.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period. This growth is driven by improving healthcare expenditure, rising medical tourism, increasing awareness about advanced spinal treatments, and a large patient pool in populous countries like China and India. Expanding healthcare access and improving economic conditions are significant growth enablers.

- Latin America: Showing gradual growth fueled by increasing awareness of spinal disorders, improvements in healthcare infrastructure, and rising disposable incomes. Brazil and Mexico are emerging as key markets, with a growing demand for advanced surgical solutions.

- Middle East and Africa (MEA): A developing market with increasing healthcare investments, particularly in countries like UAE and Saudi Arabia. The region faces challenges related to healthcare access and infrastructure but presents opportunities for growth as economic conditions and medical tourism expand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Spinal Implant and Device Market.- Medtronic

- DePuy Synthes (Johnson & Johnson)

- Stryker Corporation

- Zimmer Biomet

- NuVasive Inc.

- Globus Medical Inc.

- Orthofix Medical Inc.

- SeaSpine Holdings Corporation

- Spineart

- B. Braun Melsungen AG

- Aesculap Implant Systems (B. Braun)

- ChoiceSpine LP

- K2M Group Holdings Inc. (Stryker)

- Alphatec Holdings Inc.

- LDR Holding Corporation (Zimmer Biomet)

- Paradigm Spine LLC (RTI Surgical)

- Centinel Spine LLC

- Xtant Medical Holdings Inc.

- Life Spine Inc.

- Surgalign Holdings Inc.

Frequently Asked Questions

What is the current market size of the Spinal Implant and Device Market?

The Spinal Implant and Device Market is estimated at USD 14.50 billion in 2025, demonstrating significant growth driven by advancements in medical technology and an increasing patient base.

What are the key growth drivers for the Spinal Implant and Device Market?

Key drivers include the rising global geriatric population, increasing prevalence of spinal disorders, growing adoption of minimally invasive surgical (MIS) techniques, and continuous technological advancements in implant design and surgical tools.

How is artificial intelligence (AI) impacting the Spinal Implant and Device Market?

AI is transforming the market by enhancing diagnostic accuracy, enabling personalized treatment planning, improving surgical precision through robotics and navigation systems, and optimizing implant design, leading to improved patient outcomes.

Which regions are leading in the adoption and growth of spinal implants and devices?

North America currently holds the largest market share due to advanced healthcare infrastructure, while the Asia Pacific region is projected to exhibit the fastest growth owing to improving healthcare access and rising awareness.

What are the major types of spinal implants and devices available in the market?

The market primarily includes spinal fusion devices (such as thoracolumbar, cervical fixation, and interbody fusion devices) and non-fusion devices (like artificial discs, dynamic stabilization systems, and VCF devices), alongside various bone graft substitutes and spinal bone stimulators.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted