Smart Connected Residential Water Heater Market

Smart Connected Residential Water Heater Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704079 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Smart Connected Residential Water Heater Market Size

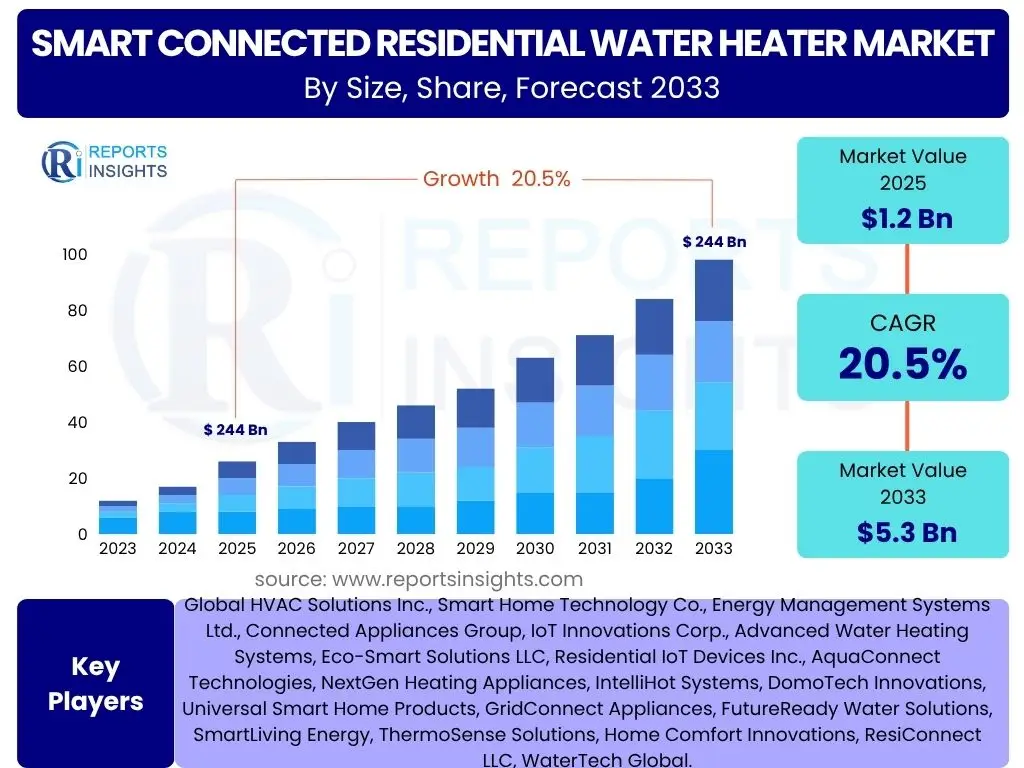

According to Reports Insights Consulting Pvt Ltd, The Smart Connected Residential Water Heater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 5.3 Billion by the end of the forecast period in 2033.

Key Smart Connected Residential Water Heater Market Trends & Insights

User inquiries frequently highlight the increasing consumer demand for energy efficiency and the seamless integration of household appliances within broader smart home ecosystems. This trend is driven by rising utility costs and a growing environmental consciousness among homeowners, who seek intelligent solutions to manage their energy consumption effectively. The ability to monitor and control water heating remotely, optimize schedules based on usage patterns, and receive real-time performance data are paramount features that resonate with modern consumers.

Another significant area of user interest revolves around the adoption of Internet of Things (IoT) technologies and advanced connectivity options like Wi-Fi and Bluetooth. Homeowners are keen to understand how these technologies enable greater convenience, such as voice control integration with virtual assistants and automated adjustments based on geo-fencing. The focus extends beyond basic remote control to predictive maintenance capabilities, where the water heater can alert users to potential issues before they escalate, thereby enhancing reliability and extending product lifespan. This proactive approach to appliance management is becoming a key differentiator in the market.

Furthermore, there is a growing trend towards personalized hot water delivery and demand response programs. Consumers are increasingly seeking solutions that adapt to their specific hot water needs throughout the day, ensuring availability while minimizing energy waste. Utility companies are also promoting smart water heaters as a means to manage grid load during peak hours, offering incentives for users to participate in demand response initiatives. This convergence of consumer convenience and utility benefits is shaping the innovation landscape, driving manufacturers to develop more sophisticated algorithms and connectivity features that support smart grid integration.

- Increasing integration with broader smart home ecosystems for centralized control.

- Rising demand for energy-efficient solutions to reduce utility costs and environmental impact.

- Proliferation of IoT connectivity (Wi-Fi, Bluetooth) for remote monitoring and control.

- Emphasis on predictive maintenance features to enhance reliability and prolong lifespan.

- Growth in voice control compatibility with popular virtual assistant platforms.

- Development of demand response capabilities for utility grid optimization.

- Focus on personalized hot water scheduling and usage pattern learning.

- Adoption of advanced sensors for real-time performance monitoring and diagnostics.

AI Impact Analysis on Smart Connected Residential Water Heater

Common user questions regarding AI's impact on smart connected residential water heaters often center on how artificial intelligence can move beyond basic automation to offer truly intelligent and adaptive solutions. Users are curious about AI's role in optimizing energy consumption through predictive analytics, where the system learns household hot water usage patterns and anticipates demand. This predictive capability promises significant energy savings by heating water only when necessary, rather than maintaining a constant temperature regardless of actual need, addressing a key consumer desire for efficiency without compromise.

Furthermore, concerns and expectations frequently arise about AI's ability to enhance the user experience through personalization and proactive problem-solving. Homeowners are interested in features such as self-diagnosis of malfunctions, the ability of the water heater to communicate potential issues directly to a service provider, or even to automatically order replacement parts. AI-driven fault detection and anomaly recognition contribute significantly to reduced downtime and maintenance costs, fostering a sense of reliability. Additionally, the integration of AI for natural language processing enables more intuitive interactions, such as voice commands for setting temperature or scheduling, simplifying the overall user interface.

Another area of focus for users is the potential for AI to integrate smart water heaters more deeply into a holistic smart energy management system for the entire home. This includes AI algorithms that coordinate water heater operation with solar power generation, variable electricity rates, or other smart appliances to maximize energy independence and minimize utility bills. Data privacy and security, however, remain a pervasive concern as AI systems collect and process sensitive usage data. Users seek assurances that their data is protected and utilized solely for enhancing product performance and user benefits, ensuring trust in these increasingly intelligent appliances.

- Predictive analytics for optimized energy consumption based on learned usage patterns.

- Enhanced fault detection and self-diagnosis capabilities for proactive maintenance.

- Personalized hot water delivery profiles adapting to individual household needs.

- Integration with voice assistants for intuitive control and natural language interaction.

- Automated anomaly detection to prevent system failures and minimize downtime.

- Data-driven insights for improved product performance and energy efficiency recommendations.

- Coordination with smart grid initiatives for demand response and peak load management.

Key Takeaways Smart Connected Residential Water Heater Market Size & Forecast

User queries about the key takeaways from the Smart Connected Residential Water Heater market size and forecast consistently point towards the significant growth potential driven by evolving consumer priorities. The market is poised for robust expansion, primarily due to the increasing adoption of smart home technologies and a heightened awareness regarding energy conservation. Consumers are actively seeking appliances that offer not only convenience through remote control but also tangible savings on utility bills, positioning smart water heaters as a compelling investment for modern households. This confluence of technological advancement and consumer demand forms the bedrock of the market's anticipated upward trajectory.

A crucial insight derived from market projections is the escalating importance of interoperability and seamless integration within existing smart home ecosystems. Homeowners desire a cohesive connected environment where devices communicate effortlessly, rather than disparate systems requiring individual management. This emphasis drives manufacturers to prioritize open standards and compatibility with leading smart home platforms, ensuring broader market acceptance and reducing consumer friction. The ability of smart water heaters to contribute to a comprehensive home energy management strategy is becoming a primary purchasing criterion, further influencing market growth and product development directions.

Furthermore, the forecast underscores the pivotal role of regional regulatory landscapes and utility incentives in accelerating market penetration. Governments and energy providers worldwide are increasingly promoting energy-efficient solutions through rebates, tax credits, and demand response programs, which directly incentivize the adoption of smart connected water heaters. These external drivers, combined with a growing consumer appreciation for features like predictive maintenance and real-time energy monitoring, suggest that the market is transitioning from a niche offering to a mainstream residential utility. The consistent upward trend in market valuation reflects a fundamental shift in consumer expectations towards smarter, more sustainable home living.

- Significant market growth projected, driven by smart home adoption and energy efficiency demands.

- Increasing consumer focus on remote control, real-time monitoring, and energy savings.

- Growing importance of interoperability with existing smart home platforms.

- Predictive maintenance and enhanced reliability are becoming critical value propositions.

- Regional government policies and utility incentives are key accelerators for market expansion.

- Data privacy and cybersecurity remain important considerations for continued consumer trust.

- Innovation in AI and IoT integration will continue to shape product development.

Smart Connected Residential Water Heater Market Drivers Analysis

The primary drivers propelling the Smart Connected Residential Water Heater market include the escalating global focus on energy efficiency and sustainability. With rising energy costs and increasing environmental awareness, consumers are actively seeking solutions that minimize energy consumption and reduce their carbon footprint. Smart water heaters, equipped with features like optimized scheduling, remote control, and usage monitoring, directly address these concerns by significantly reducing energy waste associated with traditional models. This aligns with broader societal shifts towards greener living and resource conservation, making smart solutions highly appealing.

Concurrently, the widespread adoption of smart home technology ecosystems is creating a fertile ground for the integration of smart water heaters. As more households invest in smart thermostats, lighting, and security systems, the desire for a fully integrated and centrally controlled home environment grows. Smart water heaters seamlessly fit into this ecosystem, offering convenient control through a single app or voice command, enhancing the overall smart home experience. This convenience factor, combined with the perceived value of a fully connected home, significantly drives consumer interest and purchasing decisions for smart appliances.

Moreover, supportive government policies and utility incentives play a crucial role in accelerating market penetration. Many regions offer rebates, tax credits, or specific programs for homeowners who upgrade to energy-efficient appliances, including smart water heaters. Utility companies also promote demand response programs, where smart water heaters can adjust their operation during peak energy demand periods, contributing to grid stability while potentially offering consumers cost savings. These financial incentives lower the initial investment barrier, making smart water heaters more accessible and attractive to a wider consumer base, thereby boosting market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for energy efficiency and sustainability | +5.0% | Global, particularly North America, Europe, APAC | 2025-2033 |

| Increasing adoption of smart home ecosystems and IoT devices | +4.5% | North America, Europe, China | 2025-2033 |

| Supportive government regulations and utility incentives | +4.0% | USA, Germany, UK, Australia | 2025-2033 |

| Enhanced convenience and remote accessibility for control | +3.5% | Global | 2025-2033 |

Smart Connected Residential Water Heater Market Restraints Analysis

One significant restraint impacting the Smart Connected Residential Water Heater market is the relatively high initial investment cost compared to traditional water heaters. While smart models offer long-term energy savings and advanced features, their upfront price point can deter price-sensitive consumers, particularly in developing regions or for households with limited budgets. This higher cost of acquisition creates a barrier to entry, often necessitating a longer payback period for the energy savings to offset the initial expenditure, thus slowing down mass market adoption.

Another key challenge involves the complexities associated with installation and connectivity setup. Integrating a smart water heater into an existing home network, ensuring seamless Wi-Fi connectivity, and pairing it with smart home hubs can be daunting for the average homeowner who may lack technical expertise. The need for professional installation or specialized technical support adds to the overall cost and complexity, potentially leading to user frustration and limiting DIY adoption. This complexity can also lead to perceived reliability issues if connectivity problems persist, undermining user confidence in smart home technology.

Furthermore, concerns regarding data privacy and cybersecurity represent a notable restraint. Smart water heaters collect usage data, which, if compromised, could potentially expose sensitive information about a household's daily routines. Users are increasingly wary of how their personal data is collected, stored, and utilized by connected devices and manufacturers. The risk of cyber threats, such as hacking or unauthorized access to smart home networks through vulnerable appliances, also poses a significant concern. Addressing these security and privacy anxieties is critical for building consumer trust and encouraging broader market acceptance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial upfront cost compared to conventional models | -3.0% | Global, especially emerging economies | 2025-2030 |

| Complexity of installation and connectivity setup | -2.5% | Global | 2025-2030 |

| Concerns regarding data privacy and cybersecurity vulnerabilities | -2.0% | North America, Europe | 2025-2033 |

| Limited consumer awareness and perceived necessity in some markets | -1.5% | Developing regions | 2025-2030 |

Smart Connected Residential Water Heater Market Opportunities Analysis

Significant opportunities exist in the Smart Connected Residential Water Heater market through the continued integration with broader home energy management systems and renewable energy sources. As homeowners increasingly adopt solar panels or other forms of distributed energy generation, the ability of a smart water heater to intelligently store and utilize excess energy becomes highly valuable. This integration allows for optimization of energy consumption based on production or grid pricing, leading to greater energy independence and cost savings. Developing solutions that seamlessly communicate with and respond to these energy sources can unlock new market segments and drive substantial growth.

Furthermore, the expansion into emerging geographical markets presents a considerable opportunity. While established markets in North America and Europe have seen early adoption, regions in Asia Pacific, Latin America, and the Middle East and Africa are rapidly urbanizing and witnessing a surge in disposable incomes and technological literacy. These markets represent untapped potential for smart home devices, where manufacturers can tailor solutions to local energy infrastructure, climate conditions, and consumer preferences. Establishing strong distribution networks and localized marketing strategies in these areas can yield significant market share gains.

Another promising avenue lies in the development of subscription-based services and advanced data analytics offerings. Beyond the initial hardware sale, manufacturers can create recurring revenue streams by providing value-added services such as extended warranties, predictive maintenance plans, or premium features like detailed energy usage reports and personalized optimization tips. Leveraging the data collected from smart water heaters can also provide invaluable insights into consumer behavior and product performance, informing future product development and fostering stronger customer relationships, thereby enhancing the overall value proposition and market competitiveness.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with renewable energy sources and home energy management systems | +4.0% | Global, particularly developed economies | 2026-2033 |

| Expansion into emerging markets with growing smart home adoption | +3.5% | Asia Pacific, Latin America, Middle East & Africa | 2027-2033 |

| Development of value-added services and subscription models | +3.0% | Global | 2025-2033 |

| Partnerships with utility companies for demand response programs | +2.5% | North America, Europe, Australia | 2025-2033 |

Smart Connected Residential Water Heater Market Challenges Impact Analysis

A significant challenge in the Smart Connected Residential Water Heater market is ensuring seamless interoperability across diverse smart home ecosystems and communication protocols. The fragmented nature of the smart home industry, with multiple proprietary platforms and standards (e.g., Apple HomeKit, Google Home, Amazon Alexa, Zigbee, Z-Wave), creates complexities for both manufacturers and consumers. Products from different brands may not communicate effectively, leading to a disjointed user experience and hindering the adoption of a truly integrated smart home. Addressing this fragmentation requires industry-wide collaboration on open standards, which remains an ongoing and complex endeavor.

Another critical challenge involves the reluctance of consumers to replace perfectly functional traditional water heaters with newer, more expensive smart models. The long lifespan of conventional water heaters means that homeowners often do not consider upgrading until their existing unit fails, which can be many years. This inertia in replacement cycles slows down the market penetration of smart alternatives, despite their long-term benefits in energy savings and convenience. Overcoming this challenge requires compelling marketing that emphasizes the immediate and long-term value proposition, beyond just end-of-life replacement.

Moreover, ensuring robust data security and privacy protection remains a paramount challenge for manufacturers in the connected appliance space. As smart water heaters collect and transmit sensitive data about household usage patterns, the risk of cyber vulnerabilities and data breaches is a constant concern. A single security incident could severely damage consumer trust and hinder market growth. Manufacturers must continuously invest in advanced encryption, secure communication protocols, and regular software updates to mitigate these risks. Building and maintaining consumer confidence in the security of their connected devices is essential for sustainable market expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability issues with diverse smart home ecosystems | -2.5% | Global | 2025-2030 |

| Consumer reluctance to replace functional traditional units | -2.0% | Global | 2025-2030 |

| Maintaining robust cybersecurity and data privacy | -1.8% | Global | 2025-2033 |

| Lack of standardized communication protocols across devices | -1.5% | Global | 2025-2029 |

Smart Connected Residential Water Heater Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the Smart Connected Residential Water Heater market, offering a detailed analysis of its current landscape and future growth trajectory. It encompasses a thorough examination of market size estimations, historical trends, and future projections, providing a robust framework for strategic decision-making. The scope also extends to an in-depth exploration of key market drivers, restraints, opportunities, and challenges that shape the industry, alongside an assessment of the transformative impact of Artificial Intelligence and IoT technologies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 5.3 Billion |

| Growth Rate | 20.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global HVAC Solutions Inc., Smart Home Technology Co., Energy Management Systems Ltd., Connected Appliances Group, IoT Innovations Corp., Advanced Water Heating Systems, Eco-Smart Solutions LLC, Residential IoT Devices Inc., AquaConnect Technologies, NextGen Heating Appliances, IntelliHot Systems, DomoTech Innovations, Universal Smart Home Products, GridConnect Appliances, FutureReady Water Solutions, SmartLiving Energy, ThermoSense Solutions, Home Comfort Innovations, ResiConnect LLC, WaterTech Global. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Connected Residential Water Heater market is comprehensively segmented to provide granular insights into its diverse components, enabling a deeper understanding of market dynamics and consumer preferences. This segmentation allows for the analysis of varying product types, connectivity methods, and application scenarios within the residential sector. Understanding these segments is crucial for manufacturers to tailor their offerings and for stakeholders to identify lucrative niche markets and develop targeted strategies that resonate with specific consumer needs and technological infrastructures.

- By Product Type: This segment includes different water heater designs equipped with smart capabilities.

- Tank: Traditional storage-tank water heaters with added smart features.

- Tankless: On-demand water heaters that provide hot water instantly as needed, integrated with smart connectivity.

- Hybrid: Water heaters combining traditional electric elements with heat pump technology for enhanced efficiency, featuring smart controls.

- By Connectivity: This segmentation focuses on the communication technologies employed for smart features.

- Wi-Fi: Enables connection to home networks for internet-based control and monitoring.

- Bluetooth: Used for short-range direct connection to mobile devices.

- Zigbee: A low-power, mesh networking standard commonly used in smart home devices.

- Z-Wave: Another low-power, wireless mesh networking technology designed for home automation.

- Others (e.g., Cellular): Including proprietary wireless protocols or cellular connectivity for broader remote access.

- By Application: This segment categorizes the market based on the type of residential dwelling.

- Single-Family Homes: Independent residential units typically requiring larger capacity water heating solutions.

- Multi-Family Homes/Apartments: Residential units within larger complexes, often requiring more compact or centralized smart solutions.

- By Distribution Channel: This segment analyzes the various avenues through which products reach consumers.

- Online Retail: Sales through e-commerce platforms and brand websites.

- Offline Retail: Purchases made through physical stores such as hardware stores, appliance showrooms, and big-box retailers.

- Professional Installers/HVAC Contractors: Sales facilitated directly by plumbing and heating professionals who also handle installation.

Regional Highlights

- North America: This region is a leading market, characterized by early adoption of smart home technologies, high disposable incomes, and a strong consumer emphasis on energy efficiency. The presence of major technology players and proactive utility incentive programs significantly drives market growth. The United States and Canada are key contributors, with a robust infrastructure for smart device integration.

- Europe: Driven by stringent energy efficiency regulations, high electricity costs, and a mature smart home market, Europe represents a substantial market for smart connected residential water heaters. Countries like Germany, the United Kingdom, and the Nordics are at the forefront of adoption, propelled by sustainability initiatives and consumer demand for eco-friendly solutions.

- Asia Pacific (APAC): Expected to witness the highest growth rate, primarily due to rapid urbanization, increasing disposable incomes, and a growing middle class that is tech-savvy and open to adopting smart home solutions. China, India, Japan, and South Korea are key markets, with government initiatives supporting smart city development and energy conservation fueling demand.

- Latin America: This region is an emerging market with increasing internet penetration and a rising interest in smart home devices. Brazil and Mexico are showing promising growth, influenced by economic development and a growing awareness of energy management. Opportunities exist for affordable and accessible smart water heating solutions.

- Middle East and Africa (MEA): Characterized by significant infrastructure development and investment in smart technologies, particularly in the Gulf Cooperation Council (GCC) countries. The region's hot climate often necessitates efficient water heating and cooling solutions, providing a unique market dynamic for smart systems that can adapt to high ambient temperatures and energy demands.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Connected Residential Water Heater Market.- Global HVAC Solutions Inc.

- Smart Home Technology Co.

- Energy Management Systems Ltd.

- Connected Appliances Group

- IoT Innovations Corp.

- Advanced Water Heating Systems

- Eco-Smart Solutions LLC

- Residential IoT Devices Inc.

- AquaConnect Technologies

- NextGen Heating Appliances

- IntelliHot Systems

- DomoTech Innovations

- Universal Smart Home Products

- GridConnect Appliances

- FutureReady Water Solutions

- SmartLiving Energy

- ThermoSense Solutions

- Home Comfort Innovations

- ResiConnect LLC

- WaterTech Global

Frequently Asked Questions

What is a smart connected residential water heater?

A smart connected residential water heater is an appliance that heats water for household use and includes integrated connectivity (e.g., Wi-Fi, Bluetooth) and intelligent controls. These features allow for remote monitoring and management via a smartphone app, integration with smart home ecosystems, optimized scheduling for energy efficiency, and often provide real-time performance data and predictive maintenance alerts. They are designed to offer enhanced convenience, greater energy savings, and improved reliability compared to traditional models.

What are the primary benefits of using a smart water heater?

The primary benefits of using a smart water heater include significant energy savings through optimized scheduling and usage pattern learning, leading to lower utility bills. They offer unparalleled convenience with remote control capabilities, allowing users to adjust settings from anywhere via a smartphone. Furthermore, smart water heaters provide enhanced reliability through predictive maintenance alerts and self-diagnosis features, reducing the likelihood of unexpected breakdowns and extending the appliance's lifespan. Their integration into smart home systems also contributes to a more cohesive and automated living environment.

How does AI enhance the functionality of smart water heaters?

Artificial Intelligence (AI) enhances smart water heaters by enabling advanced predictive analytics and personalized optimization. AI algorithms learn household hot water consumption patterns, anticipating demand to heat water only when needed, thereby maximizing energy efficiency. They also facilitate sophisticated fault detection and anomaly recognition, allowing the system to self-diagnose potential issues and alert users or service providers proactively. Moreover, AI powers intuitive voice control interfaces and can integrate the water heater into broader home energy management systems, adapting its operation based on real-time factors like electricity rates or renewable energy availability.

What are the main challenges in adopting smart connected residential water heaters?

The main challenges in adopting smart connected residential water heaters include their higher initial upfront cost compared to conventional models, which can deter price-sensitive consumers. The complexity of installation and ensuring seamless connectivity with existing smart home networks can also be a barrier for homeowners without technical expertise. Furthermore, consumer concerns regarding data privacy and cybersecurity vulnerabilities, as these devices collect sensitive usage data, represent a significant hurdle that manufacturers must continuously address to build and maintain trust in the connected home ecosystem.

What is the market growth forecast for smart connected residential water heaters?

The Smart Connected Residential Water Heater Market is projected for substantial growth, with a Compound Annual Growth Rate (CAGR) of approximately 20.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is forecasted to reach USD 5.3 Billion by the end of 2033. This robust growth is primarily driven by increasing consumer demand for energy-efficient solutions, the expanding adoption of smart home technologies, supportive government policies promoting green initiatives, and the ongoing development of advanced features like AI-driven optimization and predictive maintenance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted