Semiconductor Strain Gauge Sensor Market

Semiconductor Strain Gauge Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701607 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Strain Gauge Sensor Market Size

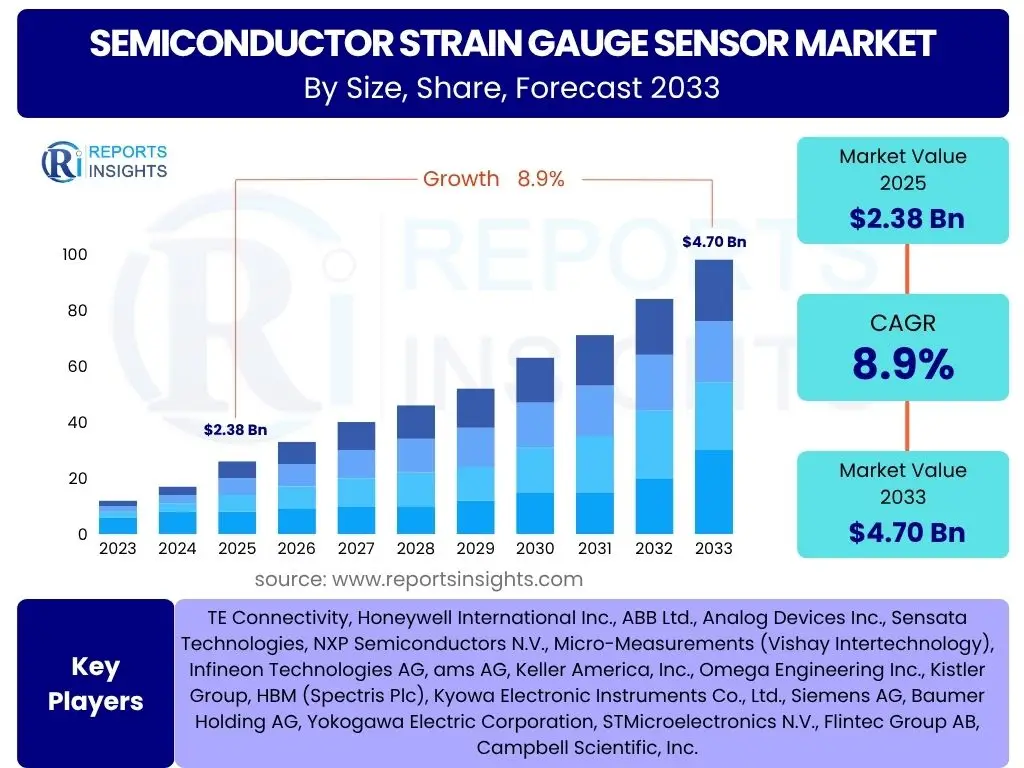

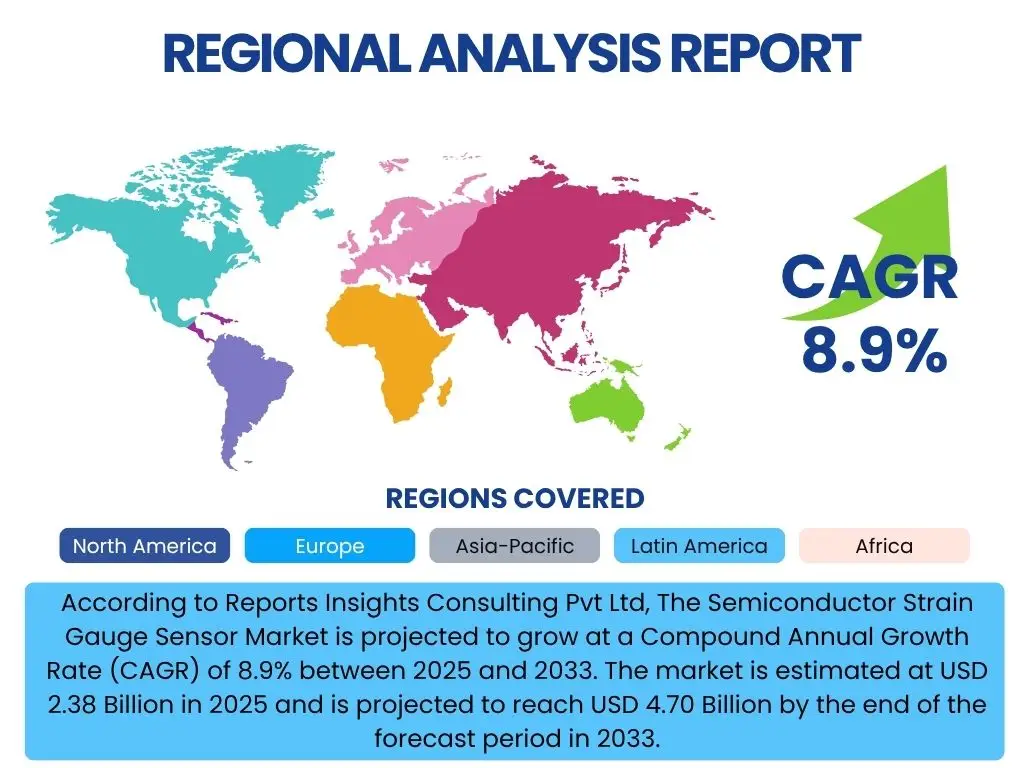

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Strain Gauge Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 2.38 Billion in 2025 and is projected to reach USD 4.70 Billion by the end of the forecast period in 2033.

Key Semiconductor Strain Gauge Sensor Market Trends & Insights

The Semiconductor Strain Gauge Sensor market is undergoing significant transformation driven by technological advancements and evolving application requirements. Current market dynamics indicate a strong shift towards miniaturization and integration, allowing these sensors to be embedded into smaller, more complex systems. This trend is particularly evident in portable electronics and advanced medical devices, where space and weight are critical considerations. Furthermore, there is an increasing demand for enhanced accuracy and stability across various operating conditions, pushing manufacturers to innovate in material science and fabrication processes to reduce hysteresis and improve long-term reliability. The focus is also on developing sensors with broader temperature ranges and resistance to harsh environments, extending their utility in industrial and automotive applications.

Another prominent trend involves the growing adoption of wireless connectivity and smart sensor technologies. Integrating these capabilities allows for real-time data acquisition and remote monitoring, which is crucial for predictive maintenance in industrial machinery and structural health monitoring. The proliferation of the Internet of Things (IoT) is a major catalyst, as strain gauge sensors become foundational components for collecting critical physical data points in interconnected systems. This integration facilitates more efficient data analysis and provides actionable insights, driving operational efficiencies and preventing equipment failures. The emphasis on smart features also includes self-calibration and diagnostic capabilities, reducing the need for manual intervention and improving system uptime.

- Miniaturization and compact design for integration into smaller devices.

- Enhanced accuracy, stability, and reliability for demanding applications.

- Development of sensors resistant to harsh environmental conditions (temperature, pressure, chemical exposure).

- Increased integration with wireless communication technologies (Bluetooth, Wi-Fi) for remote monitoring.

- Growing adoption in IoT ecosystems for real-time data collection and analysis.

- Focus on smart features such as self-calibration and predictive diagnostics.

AI Impact Analysis on Semiconductor Strain Gauge Sensor

Artificial Intelligence (AI) is set to profoundly reshape the landscape of semiconductor strain gauge sensors, primarily by optimizing data processing and enabling more sophisticated applications. Users frequently inquire about how AI can enhance the performance and utility of these sensors. AI algorithms can process vast amounts of sensor data in real-time, identifying subtle patterns and anomalies that human analysis might miss. This capability is critical for applications requiring high precision and rapid response, such as structural health monitoring, where AI can detect early signs of material fatigue or damage by analyzing minute changes in strain data. Furthermore, AI-driven predictive maintenance systems leverage strain gauge data to forecast equipment failures, allowing for timely interventions and significantly reducing downtime and operational costs.

Beyond data analysis, AI influences the design and calibration of semiconductor strain gauge sensors. Machine learning models can be employed to optimize sensor geometries and material compositions for specific applications, improving sensitivity and linearity. AI also facilitates dynamic calibration processes, adapting sensor performance to changing environmental conditions or load profiles, thereby enhancing accuracy and reliability over time. The integration of AI with sensor networks enables the creation of "smart" sensing systems capable of autonomous decision-making and adaptive responses. This paradigm shift moves beyond mere data collection to intelligent interpretation and action, leading to more efficient and resilient industrial, automotive, and healthcare systems. Concerns often revolve around data privacy, computational overhead, and the robustness of AI models in safety-critical applications, necessitating robust validation and secure data handling protocols.

- Enables real-time, sophisticated analysis of complex strain data for anomaly detection.

- Facilitates predictive maintenance and extends equipment lifespan through data-driven insights.

- Optimizes sensor design and material selection using machine learning for improved performance.

- Supports dynamic and adaptive calibration, enhancing accuracy across varying conditions.

- Drives autonomous decision-making and adaptive responses in smart sensing systems.

- Mitigates risks associated with data privacy and computational demands through advanced algorithms.

Key Takeaways Semiconductor Strain Gauge Sensor Market Size & Forecast

The Semiconductor Strain Gauge Sensor market is poised for robust expansion over the forecast period, driven by escalating demand across diverse industrial sectors and a continuous push for technological innovation. A key takeaway from the market forecast is the consistent growth trajectory, underpinned by the increasing integration of these sensors into critical infrastructure, advanced manufacturing processes, and next-generation automotive systems. The market's resilience is further highlighted by its ability to adapt to emerging application needs, particularly in areas requiring precise force, pressure, and weight measurement. This sustained growth underscores the fundamental role of strain gauge technology in enabling smart systems and enhancing operational efficiency and safety across various industries.

Another significant insight derived from the market size analysis is the substantial investment in research and development aimed at improving sensor performance and reducing manufacturing costs. This investment is crucial for expanding market accessibility and fostering new applications. The market is also witnessing a trend towards consolidation and strategic partnerships, as companies seek to leverage complementary expertise and broaden their product portfolios to capture a larger market share. The forecast indicates that while industrial automation and automotive sectors will remain dominant, emerging applications in healthcare, consumer electronics, and aerospace will significantly contribute to market expansion. Stakeholders must focus on innovation, strategic alliances, and market diversification to capitalize on these growth opportunities and maintain a competitive edge.

- The market exhibits strong growth potential, driven by broad industrial adoption and technological advancements.

- Continuous integration into critical infrastructure, manufacturing, and automotive systems is a primary growth driver.

- Significant R&D investments are enhancing sensor performance and reducing production costs.

- Strategic collaborations and market consolidation are shaping competitive dynamics.

- Diversification into healthcare, consumer electronics, and aerospace applications is expanding market reach.

- Operational efficiency and safety improvements across industries are key outcomes of sensor deployment.

Semiconductor Strain Gauge Sensor Market Drivers Analysis

The escalating adoption of industrial automation and robotics across manufacturing sectors globally represents a primary driver for the Semiconductor Strain Gauge Sensor market. As industries strive for higher precision, efficiency, and safety in their operations, these sensors are becoming indispensable for real-time monitoring of force, weight, and pressure in robotic arms, automated assembly lines, and material handling systems. The increasing complexity of automated processes necessitates highly accurate and reliable feedback mechanisms, which semiconductor strain gauges provide effectively, contributing directly to enhanced productivity and reduced operational errors.

Advancements in the automotive industry, particularly the transition towards electric vehicles (EVs) and autonomous driving systems, significantly boost the demand for these sensors. Semiconductor strain gauges are vital components in various automotive applications, including occupant detection systems, brake-by-wire systems, torque sensing in electric powertrains, and suspension monitoring for improved vehicle stability and safety. The stringent requirements for reliability and performance in automotive components, coupled with the rapid innovation in vehicle technology, fuel the continuous integration of advanced strain sensing solutions.

Furthermore, the expanding applications in the healthcare sector, including medical devices and diagnostic equipment, are driving market growth. Semiconductor strain gauges are employed in patient monitoring systems, infusion pumps, surgical instruments, and prosthetic limbs, where precise measurement of force and pressure is critical for patient safety and diagnostic accuracy. The aging global population and increasing healthcare expenditure contribute to the demand for sophisticated medical devices, subsequently propelling the market for high-performance semiconductor strain gauge sensors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation & Robotics | +2.1% | North America, Europe, Asia Pacific (China, Germany, Japan) | Short to Mid-term (2025-2029) |

| Growth in Automotive Sector (EVs & Autonomous Vehicles) | +1.8% | Asia Pacific (China, Japan, South Korea), Europe, North America | Mid to Long-term (2027-2033) |

| Rising Demand in Healthcare & Medical Devices | +1.5% | North America, Europe, Asia Pacific (India, China) | Mid-term (2026-2030) |

| Expansion of Internet of Things (IoT) & Smart Devices | +1.3% | Global, particularly developed economies | Short to Mid-term (2025-2030) |

| Infrastructure Monitoring & Smart Cities Initiatives | +1.0% | Asia Pacific (China, India), Europe, North America | Mid to Long-term (2028-2033) |

Semiconductor Strain Gauge Sensor Market Restraints Analysis

One significant restraint impacting the Semiconductor Strain Gauge Sensor market is the high cost associated with the research, development, and manufacturing of these precision devices. The fabrication process for semiconductor sensors requires specialized materials, advanced cleanroom facilities, and sophisticated micro-electromechanical systems (MEMS) technologies, which contribute to elevated production expenses. This high initial investment can be a barrier for smaller enterprises or for widespread adoption in cost-sensitive applications, potentially limiting market penetration in certain segments, particularly emerging ones where budget constraints are more pronounced.

Another notable challenge is the susceptibility of semiconductor strain gauges to environmental factors and the complexities involved in their calibration and temperature compensation. These sensors can be highly sensitive to changes in temperature, humidity, and electromagnetic interference, which can lead to measurement inaccuracies. Ensuring stable and reliable performance across varying environmental conditions often requires intricate calibration procedures and the integration of sophisticated compensation circuits, adding to the overall system complexity and cost. Maintaining accuracy over extended periods in harsh industrial or outdoor environments remains a persistent technical hurdle, requiring frequent recalibration or advanced design solutions.

Furthermore, the inherent fragility and limited lifespan of certain semiconductor strain gauge designs, especially when subjected to extreme mechanical stress or fatigue over repeated cycles, pose a restraint. While advancements are being made in material science and packaging to enhance durability, prolonged exposure to high-stress environments or aggressive chemical agents can degrade sensor performance or lead to premature failure. This limitation necessitates careful design considerations for applications with demanding operational cycles or harsh chemical exposures, potentially increasing maintenance costs or limiting their suitability for specific long-term monitoring tasks without protective measures.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing & Development Costs | -0.9% | Global, particularly developing regions | Short to Mid-term (2025-2030) |

| Complexity of Calibration & Temperature Compensation | -0.7% | Global, across all high-precision applications | Mid-term (2026-2031) |

| Susceptibility to Harsh Environmental Factors | -0.6% | Industrial, Automotive, Aerospace sectors | Long-term (2028-2033) |

| Limited Lifespan in Extreme Stress Applications | -0.5% | Heavy machinery, high-cycle industrial applications | Mid to Long-term (2027-2033) |

Semiconductor Strain Gauge Sensor Market Opportunities Analysis

The growing demand for customized and application-specific strain gauge solutions presents a significant opportunity for market players. Industries are increasingly seeking sensors tailored to their unique operational parameters, environmental conditions, and integration requirements, moving beyond generic off-the-shelf products. This trend encourages manufacturers to invest in flexible design and production capabilities, offering bespoke solutions that can command higher margins and foster stronger client relationships. Niche applications in specialized robotics, advanced prosthetics, and precision agriculture, which require highly specific sensor characteristics, are particularly ripe for such customized developments, allowing for market differentiation and value creation.

Emerging economies, particularly in Asia Pacific and Latin America, offer substantial untapped market potential due to rapid industrialization, urbanization, and increasing investments in infrastructure development. These regions are experiencing a surge in demand for industrial automation, smart building technologies, and advanced transportation systems, all of which require precise strain measurement capabilities. As these economies continue to grow and adopt modern manufacturing and infrastructure practices, the demand for semiconductor strain gauge sensors is expected to rise considerably, providing fertile ground for market expansion and new sales channels for global and regional players alike.

The continuous advancements in material science and micro-fabrication technologies present ongoing opportunities for innovation in semiconductor strain gauge sensors. Research into novel materials, such as graphene or new semiconductor alloys, promises to yield sensors with enhanced sensitivity, broader operating temperature ranges, and improved durability. Simultaneously, breakthroughs in MEMS and NEMS (Nano-electromechanical systems) fabrication techniques allow for further miniaturization, higher integration densities, and more complex sensor geometries. These technological leaps enable the development of next-generation sensors that can address previously unmet needs or unlock entirely new applications, pushing the boundaries of what is currently achievable in strain measurement.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Customization & Application-Specific Solutions | +1.2% | Global, high-value industrial sectors | Mid to Long-term (2027-2033) |

| Expansion into Emerging Economies | +1.0% | Asia Pacific (China, India), Latin America, MEA | Short to Mid-term (2025-2030) |

| Advancements in Materials & Fabrication Technologies | +0.9% | Global, R&D intensive regions (North America, Europe, Japan) | Long-term (2028-2033) |

| Integration with AI & Advanced Analytics for Smart Systems | +0.8% | Global, particularly in developed markets | Mid-term (2026-2031) |

| Growth in Wearable Technology & Consumer Electronics | +0.7% | North America, Europe, Asia Pacific (South Korea, China) | Short-term (2025-2029) |

Semiconductor Strain Gauge Sensor Market Challenges Impact Analysis

One of the primary challenges confronting the Semiconductor Strain Gauge Sensor market is the complexity of integrating these sensors into existing or new systems, particularly in highly regulated or safety-critical environments. Proper integration requires not only mechanical fitting but also electrical interfacing, signal conditioning, and software development, which can be time-consuming and expensive. Ensuring seamless compatibility with diverse control systems and data acquisition platforms presents a technical hurdle, often requiring specialized engineering expertise. This complexity can deter potential adopters who lack the in-house capabilities or face budgetary constraints for such comprehensive system overhauls.

The intense competitive landscape, characterized by the presence of numerous established players and emerging startups, poses a significant challenge for market participants. This competition drives down profit margins and necessitates continuous innovation to maintain market share. Companies must invest heavily in research and development to differentiate their products through superior performance, cost-effectiveness, or unique features. Furthermore, the global supply chain for semiconductor components is prone to disruptions, as evidenced by recent events, which can lead to material shortages, production delays, and increased raw material costs, directly impacting the manufacturing capabilities and pricing strategies of sensor producers.

Another critical challenge is ensuring data integrity and security, especially as semiconductor strain gauge sensors become more interconnected within IoT and industrial IoT (IIoT) ecosystems. The data collected by these sensors often includes sensitive operational information, making it a target for cyber threats. Protecting this data from unauthorized access, manipulation, or exfiltration is paramount to maintaining trust and preventing system vulnerabilities. Developing robust cybersecurity measures for sensor networks, from hardware-level encryption to secure communication protocols, adds complexity and cost to sensor deployment, requiring ongoing vigilance and investment in a rapidly evolving threat landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Integration & System Compatibility | -0.8% | Global, across diverse industrial applications | Short to Mid-term (2025-2030) |

| Intense Competition & Price Pressure | -0.7% | Global, particularly in mature markets | Short to Mid-term (2025-2030) |

| Supply Chain Disruptions & Raw Material Volatility | -0.6% | Global, particularly impacting manufacturing hubs | Short-term (2025-2027) |

| Data Security & Privacy Concerns in IoT/IIoT Integration | -0.5% | Global, across all interconnected applications | Mid to Long-term (2027-2033) |

| Lack of Skilled Workforce for Advanced Sensor Technologies | -0.4% | Developed economies (North America, Europe) | Long-term (2028-2033) |

Semiconductor Strain Gauge Sensor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Semiconductor Strain Gauge Sensor Market, offering detailed insights into market dynamics, segmentation, regional landscapes, and the competitive environment. It covers historical data, current trends, and future projections, enabling stakeholders to make informed strategic decisions. The scope includes a thorough examination of market drivers, restraints, opportunities, and challenges, along with an impact analysis of key macroeconomic factors and technological advancements like AI on market growth. The report aims to deliver actionable intelligence for businesses operating within or looking to enter this dynamic market segment, providing a holistic view of its potential and trajectories.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.38 Billion |

| Market Forecast in 2033 | USD 4.70 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, Honeywell International Inc., ABB Ltd., Analog Devices Inc., Sensata Technologies, NXP Semiconductors N.V., Micro-Measurements (Vishay Intertechnology), Infineon Technologies AG, ams AG, Keller America, Inc., Omega Engineering Inc., Kistler Group, HBM (Spectris Plc), Kyowa Electronic Instruments Co., Ltd., Siemens AG, Baumer Holding AG, Yokogawa Electric Corporation, STMicroelectronics N.V., Flintec Group AB, Campbell Scientific, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Strain Gauge Sensor market is extensively segmented to provide a granular understanding of its diverse landscape. This segmentation is crucial for identifying specific market niches, understanding consumer preferences, and developing targeted strategies. The primary segmentation categories include the sensor type, the various applications where these sensors are deployed, and the distinct end-user industries that leverage this technology. Each segment represents a unique demand pattern and technological requirement, influencing market dynamics and competitive positioning across the global value chain. Understanding these segments is key to analyzing market opportunities and challenges comprehensively.

- By Type

- Piezoresistive Strain Gauge: Characterized by their high sensitivity and suitability for integration into silicon-based micro-electromechanical systems (MEMS). They are widely used in pressure sensors and accelerometers due to their robust performance and direct compatibility with semiconductor fabrication processes.

- Thin-Film Strain Gauge: Manufactured by depositing thin layers of resistive material onto a substrate, offering excellent stability, repeatability, and resistance to harsh environments. They are favored in applications requiring high endurance and precision over extended periods, such as industrial process control and aerospace.

- Others: Includes specialized types like Silicon-on-Insulator (SOI) strain gauges which offer superior performance at high temperatures, and Silicon Carbide (SiC) based sensors designed for extreme temperature and radiation environments. These cater to niche, high-performance applications.

- By Application

- Automotive: Utilized in engine management, brake systems (ABS, ESP), occupant detection, suspension control, and tire pressure monitoring systems, enhancing safety and performance.

- Industrial Automation: Essential for force measurement in robotics, load cells, process control, and machinery monitoring, improving efficiency and operational reliability.

- Healthcare & Medical Devices: Found in patient monitoring, infusion pumps, surgical instruments, and prosthetic limbs for precise force, weight, and pressure measurement, critical for patient care.

- Aerospace & Defense: Applied in aircraft structural health monitoring, flight control surfaces, and missile systems for stress, vibration, and fatigue analysis, ensuring structural integrity and safety.

- Consumer Electronics: Integrated into wearables, smartphones (force touch), and gaming devices for advanced haptic feedback and interaction, enabling new user experiences.

- Infrastructure & Building Monitoring: Employed in bridges, dams, and buildings for structural integrity assessment, detecting strain, stress, and cracks to prevent catastrophic failures.

- Test & Measurement: Used in laboratories and quality control environments for precise material testing, component validation, and calibration of other sensors and systems.

- Others: Includes applications in agriculture (soil compaction, harvest monitoring), sports equipment (performance analysis), and smart textiles.

- By End-User Industry

- Automotive: Manufacturers and suppliers of passenger vehicles, commercial vehicles, and automotive components.

- Manufacturing: Industrial machinery, heavy equipment, and general manufacturing companies.

- Healthcare: Hospitals, medical device manufacturers, and pharmaceutical companies.

- Aerospace & Defense: Aircraft manufacturers, defense contractors, and space agencies.

- Construction: Engineering firms, construction companies, and infrastructure development agencies.

- Consumer Goods: Manufacturers of electronic gadgets, home appliances, and sports equipment.

- Energy: Power generation, oil and gas, and renewable energy sectors for equipment monitoring.

- Research & Development: Academic institutions, government laboratories, and private R&D centers.

Regional Highlights

- North America: This region maintains a significant market share, driven by robust industrial automation adoption, strong automotive sector innovation, and extensive R&D investments in advanced sensing technologies. The presence of key market players and a high rate of technological absorption, particularly in the United States, contributes to its dominance.

- Europe: Europe is a mature market characterized by stringent regulations in automotive and industrial sectors, fostering demand for high-precision and reliable semiconductor strain gauge sensors. Germany, with its strong manufacturing base and focus on Industry 4.0, along with the UK and France, are key contributors to market growth.

- Asia Pacific (APAC): APAC is projected to exhibit the highest growth rate, primarily due to rapid industrialization, burgeoning automotive manufacturing (especially EVs), and increasing infrastructure development in countries like China, India, Japan, and South Korea. Government initiatives promoting smart cities and advanced manufacturing further accelerate market expansion.

- Latin America: This region is an emerging market for semiconductor strain gauge sensors, with growing industrialization and investments in infrastructure and automotive sectors. Brazil and Mexico are leading the adoption, though market growth here is slower compared to APAC or North America due to nascent technological infrastructure.

- Middle East and Africa (MEA): The MEA region is witnessing gradual adoption, driven by diversification efforts from oil-dependent economies into manufacturing, infrastructure, and smart city projects. Investments in critical infrastructure, particularly in countries like UAE and Saudi Arabia, are expected to fuel demand for monitoring solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Strain Gauge Sensor Market.- TE Connectivity

- Honeywell International Inc.

- ABB Ltd.

- Analog Devices Inc.

- Sensata Technologies

- NXP Semiconductors N.V.

- Micro-Measurements (Vishay Intertechnology)

- Infineon Technologies AG

- ams AG

- Keller America, Inc.

- Omega Engineering Inc.

- Kistler Group

- HBM (Spectris Plc)

- Kyowa Electronic Instruments Co., Ltd.

- Siemens AG

- Baumer Holding AG

- Yokogawa Electric Corporation

- STMicroelectronics N.V.

- Flintec Group AB

- Campbell Scientific, Inc.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Strain Gauge Sensor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Semiconductor Strain Gauge Sensor Market?

The Semiconductor Strain Gauge Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033, reaching an estimated USD 4.70 Billion by 2033 from USD 2.38 Billion in 2025.

What are the primary applications of semiconductor strain gauge sensors?

These sensors are extensively used across diverse applications including automotive (e.g., brake systems, occupant detection), industrial automation (robotics, load cells), healthcare (medical devices, patient monitoring), aerospace, consumer electronics, and infrastructure monitoring.

How does AI impact the Semiconductor Strain Gauge Sensor market?

AI significantly impacts the market by enabling real-time, sophisticated data analysis for anomaly detection, facilitating predictive maintenance, optimizing sensor design and calibration, and driving autonomous decision-making in smart sensing systems.

Which region is expected to lead in market growth for semiconductor strain gauge sensors?

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate, driven by rapid industrialization, robust automotive manufacturing, and increasing infrastructure development in countries such as China, India, and South Korea.

What are the main challenges faced by the Semiconductor Strain Gauge Sensor market?

Key challenges include the complexity of sensor integration into existing systems, intense market competition leading to price pressures, potential disruptions in the global supply chain, and growing concerns regarding data security and privacy in interconnected IoT/IIoT environments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted