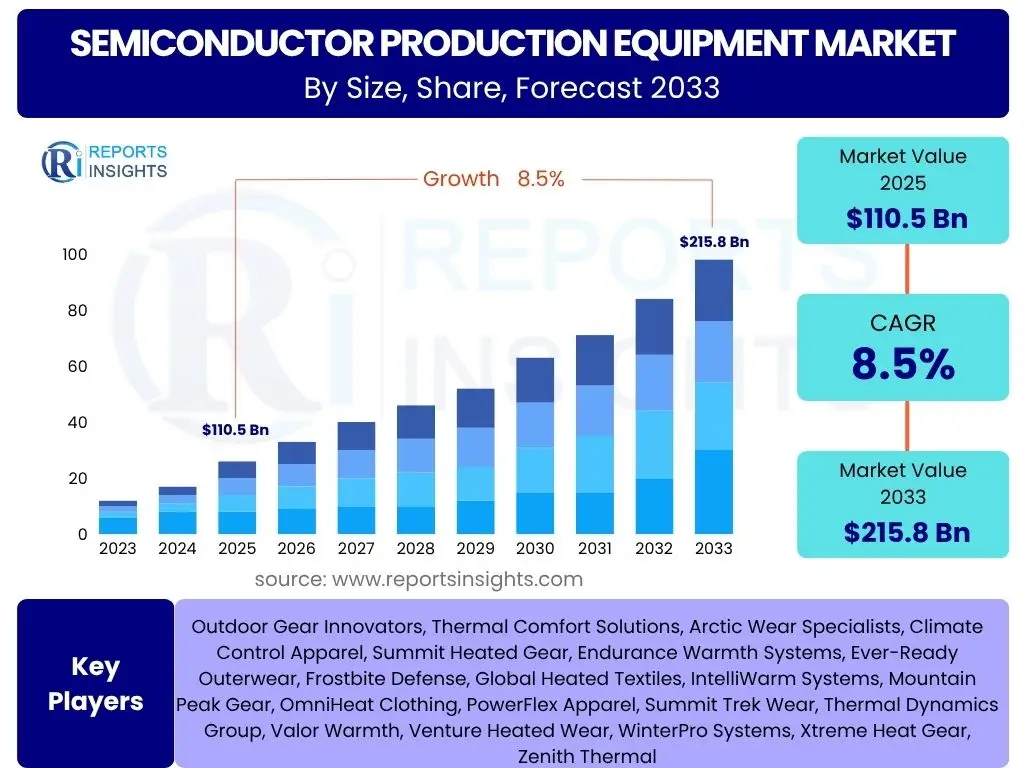

Semiconductor Production Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, valued at USD 110.5 billion in 2025 and is projected to grow to USD 215.8 billion by 2033 the end of the forecast period.

Key Semiconductor Production Equipment Market Trends & Insights

The semiconductor production equipment market is experiencing a period of significant innovation and expansion, driven by the escalating demand for advanced semiconductors across diverse applications. Key trends include the relentless pursuit of miniaturization, demanding more sophisticated lithography and etching solutions, and the increasing complexity of chip designs which necessitates advanced metrology and inspection equipment. Furthermore, the industry is seeing a pronounced shift towards automation and artificial intelligence integration within manufacturing processes, optimizing efficiency and reducing human error. The focus on sustainable manufacturing practices is also gaining traction, with equipment manufacturers developing more energy-efficient and environmentally responsible solutions. Lastly, the distributed nature of global supply chains continues to influence equipment design, with an emphasis on modularity and adaptability to various fab environments.

- Continued advancements in Extreme Ultraviolet (EUV) lithography and next-generation patterning technologies.

- Escalating demand for advanced packaging equipment due to heterogeneous integration trends.

- Increased adoption of Artificial Intelligence (AI) and Machine Learning (ML) for process optimization and predictive maintenance.

- Growing investment in specialized equipment for novel materials and quantum computing applications.

- Emphasis on sustainable manufacturing processes and energy-efficient equipment designs.

- Regionalization of supply chains fostering localized equipment manufacturing and support.

AI Impact Analysis on Semiconductor Production Equipment

Artificial intelligence is profoundly transforming the semiconductor production equipment landscape, enhancing operational efficiency, yield rates, and predictive capabilities across the manufacturing lifecycle. AI-powered algorithms are being integrated into various stages, from optimizing design for manufacturability (DFM) to controlling complex fabrication processes, leading to tighter process control and reduced variability. Predictive maintenance models, enabled by AI, analyze equipment sensor data to forecast potential failures, minimizing downtime and extending asset lifespan. This intelligence also extends to quality control, where AI-driven inspection systems can detect microscopic defects with unparalleled speed and accuracy, surpassing human capabilities.

- AI-driven predictive maintenance reducing equipment downtime and extending operational lifecycles.

- Enhanced process control and optimization through AI and machine learning algorithms for improved yield.

- Automated defect inspection and classification utilizing computer vision and deep learning.

- Intelligent scheduling and resource allocation for wafer fabrication plants.

- Acceleration of R&D cycles through AI-assisted material discovery and process simulation.

- Development of self-optimizing equipment capable of autonomous adjustments.

Key Takeaways Semiconductor Production Equipment Market Size & Forecast

- The global Semiconductor Production Equipment Market is poised for robust growth, driven by sustained demand for advanced electronics.

- Market valuation is projected to nearly double from 2025 to 2033, reflecting significant industry expansion and technological advancements.

- The Compound Annual Growth Rate (CAGR) of 8.5% signifies a healthy and consistent upward trajectory over the forecast period.

- Investments in new fabrication facilities (fabs) and upgrades to existing ones will be a primary growth catalyst.

- Asia Pacific is expected to remain the dominant region due to its established manufacturing ecosystem and ongoing capacity expansions.

- Technological evolution, particularly in lithography and advanced packaging, will continue to dictate market trends and investment priorities.

Semiconductor Production Equipment Market Drivers Analysis

The Semiconductor Production Equipment Market is propelled by a confluence of powerful drivers, primarily the relentless advancement of semiconductor technology itself. The continuous demand for smaller, faster, and more energy-efficient electronic devices necessitates increasingly sophisticated manufacturing tools. This miniaturization trend, coupled with the proliferation of emerging technologies like Artificial Intelligence, 5G, the Internet of Things, and advanced automotive electronics, fuels significant investments in next-generation fabrication capabilities. Furthermore, government initiatives and incentives in various regions aimed at bolstering domestic semiconductor manufacturing capacity contribute substantially to market expansion by encouraging the establishment of new fabs and the modernization of existing ones, thereby increasing the demand for advanced equipment.

| Drivers |

(~) Impact on CAGR % Forecast |

Regional/Country Relevance |

Impact Time Period |

|

Increasing Demand for Advanced Semiconductors

|

+2.1%

|

Global, particularly Asia Pacific (Taiwan, South Korea, China) and North America

|

Long-term (2025-2033)

|

|

Proliferation of Emerging Technologies (AI, 5G, IoT, Automotive)

|

+1.8%

|

North America, Europe, Asia Pacific (China, Japan)

|

Medium- to Long-term (2025-2033)

|

|

Government Investments and Subsidies for Domestic Manufacturing

|

+1.5%

|

North America (USA), Europe (Germany, France), Asia Pacific (Japan, India)

|

Medium-term (2025-2030)

|

|

Growing Foundry and IDM Capital Expenditure

|

+1.2%

|

Asia Pacific (Taiwan, South Korea, China), North America

|

Short- to Medium-term (2025-2028)

|

|

Transition to Smaller Process Nodes (e.g., 3nm, 2nm)

|

+1.0%

|

Global, led by advanced technology hubs

|

Long-term (2025-2033)

|

Semiconductor Production Equipment Market Restraints Analysis

Despite its robust growth prospects, the Semiconductor Production Equipment Market faces several significant restraints that could temper its expansion. The extraordinarily high research and development costs associated with developing next-generation equipment, particularly for advanced lithography and deposition techniques, present a substantial barrier to entry and ongoing innovation. The cyclical nature of the semiconductor industry, characterized by periods of rapid growth followed by slowdowns due to oversupply or economic downturns, introduces market volatility and can lead to fluctuating demand for equipment. Furthermore, geopolitical tensions and trade disputes can disrupt global supply chains for critical components and materials, impacting equipment manufacturing and delivery timelines. Lastly, increasingly stringent environmental regulations and the rising cost of energy in some regions can add to operational expenses for both equipment manufacturers and semiconductor fabs, potentially slowing investment.

| Restraints |

(~) Impact on CAGR % Forecast |

Regional/Country Relevance |

Impact Time Period |

|

High Capital Expenditure and R&D Costs

|

-0.9%

|

Global, impacts smaller players disproportionately

|

Long-term (2025-2033)

|

|

Cyclical Nature of the Semiconductor Industry

|

-0.8%

|

Global, affects market sentiment and investment cycles

|

Short- to Medium-term (intermittent)

|

|

Geopolitical Tensions and Supply Chain Disruptions

|

-0.7%

|

Asia Pacific, North America, Europe (cross-border impacts)

|

Medium-term (2025-2030)

|

|

Shortage of Skilled Workforce and Talent Drain

|

-0.6%

|

Global, particularly in advanced manufacturing hubs

|

Long-term (2025-2033)

|

Semiconductor Production Equipment Market Opportunities Analysis

The Semiconductor Production Equipment Market is brimming with compelling opportunities that are expected to fuel substantial growth over the forecast period. The surging adoption of advanced packaging technologies, such as 3D integration and chiplets, is creating demand for specialized equipment that can handle complex multi-die assembly and interconnections. The nascent but rapidly evolving fields of quantum computing and specialized memory solutions (e.g., HBM, MRAM) present niche but high-value opportunities for equipment manufacturers to develop tailored tools. Furthermore, the expansion of semiconductor manufacturing into new geographic regions, driven by supply chain diversification strategies and government incentives, opens up new markets for equipment sales and service. The increasing focus on factory automation and smart manufacturing (Industry 4.0) within fabs also creates opportunities for equipment offering enhanced connectivity, real-time data analytics, and AI-driven process optimization.

| Opportunities |

(~) Impact on CAGR % Forecast |

Regional/Country Relevance |

Impact Time Period |

|

Growing Adoption of Advanced Packaging Technologies

|

+1.3%

|

Global, particularly Asia Pacific (OSATs)

|

Medium- to Long-term (2025-2033)

|

|

Emergence of Quantum Computing and Novel Computing Architectures

|

+0.9%

|

North America, Europe, Asia Pacific (Research Hubs)

|

Long-term (2028-2033)

|

|

Expansion into New Geographic Regions and Emerging Markets

|

+0.8%

|

India, Southeast Asia, parts of Europe, Middle East

|

Medium-term (2025-2030)

|

|

Integration of Industry 4.0 and Smart Manufacturing Solutions

|

+0.7%

|

Global, particularly advanced manufacturing regions

|

Medium- to Long-term (2025-2033)

|

Semiconductor Production Equipment Market Challenges Impact Analysis

The Semiconductor Production Equipment Market faces several intricate challenges that demand strategic responses from industry players. The escalating costs of advanced manufacturing equipment, particularly for next-generation process nodes, pose a significant financial hurdle for semiconductor manufacturers and could limit the pace of technology adoption for some. Rapid technological obsolescence is another critical challenge; given the fast pace of innovation in chip design, equipment must evolve constantly, leading to shorter product lifecycles and high R&D pressure. Furthermore, the industry is grappling with a persistent shortage of highly skilled talent in areas such as precision engineering, materials science, and AI, which can impede both equipment development and the operational efficiency of fabs. Lastly, the stringent technical requirements and complex integration processes for new equipment in existing fab environments create significant hurdles for seamless upgrades and expansions, demanding extensive collaboration and validation.

| Challenges |

(~) Impact on CAGR % Forecast |

Regional/Country Relevance |

Impact Time Period |

|

Escalating Equipment Costs for Advanced Nodes

|

-0.8%

|

Global, particularly affecting new fab investments

|

Long-term (2025-2033)

|

|

Rapid Technological Obsolescence and Short Product Lifecycles

|

-0.7%

|

Global, high R&D pressure for equipment vendors

|

Long-term (2025-2033)

|

|

Talent Shortages in Highly Specialized Fields

|

-0.6%

|

North America, Europe, Asia Pacific (Taiwan, South Korea)

|

Long-term (2025-2033)

|

|

Complex Integration and Validation Processes for New Tools

|

-0.5%

|

Global, impacts fab operational efficiency

|

Medium-term (2025-2030)

|

Semiconductor Production Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Semiconductor Production Equipment Market, offering strategic insights into market dynamics, segmentation, regional landscapes, and competitive developments. It meticulously forecasts market size and growth trajectories, taking into account current trends, key drivers, restraints, opportunities, and challenges. The scope covers the full spectrum of equipment used in semiconductor manufacturing, from front-end processing to back-end assembly and testing, empowering stakeholders with actionable intelligence for informed decision-making within this rapidly evolving industry.

| Report Attributes |

Report Details |

| Base Year |

2024 |

| Historical Year |

2019 to 2023 |

| Forecast Year |

2025 - 2033 |

| Market Size in 2025 |

USD 110.5 billion |

| Market Forecast in 2033 |

USD 215.8 billion |

| Growth Rate |

8.5% CAGR from 2025 to 2033 |

| Number of Pages |

257 |

| Key Trends |

- EUV lithography advancements

- Advanced packaging surge

- AI/ML integration in manufacturing

- Sustainable equipment designs

- Regional supply chain diversification

|

| Segments Covered |

- Equipment Type (Front-End Equipment, Back-End Equipment)

- Front-End Equipment Sub-segments (Lithography Equipment, Etch Equipment, Deposition Equipment, Ion Implantation Equipment, Cleaning Equipment, Metrology and Inspection Equipment, Other Front-End Equipment)

- Back-End Equipment Sub-segments (Packaging Equipment, Test Equipment)

- Application (Foundry, Integrated Device Manufacturers (IDMs), Outsourced Semiconductor Assembly and Test (OSAT) Companies)

- End-User Industry (Consumer Electronics, Automotive, Healthcare, Industrial, IT & Telecommunications, Others)

- Regional (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa)

|

| Key Companies Covered |

Precision Wafer Systems, Global Etch Solutions, Advanced Deposition Technologies, Integrated Lithography Tools, Quantum Test Systems, NextGen Packaging Automation, SmartFab Metrology, Universal Process Control, Future Wafer Solutions, Dynamic Ion Implantation, Apex Cleanroom Equipment, OptiView Inspection, Silicon Edge Innovations, Core Microfab Systems, Proximity Process Solutions, Vector Chip Assembly, Nexus Test & Measurement, GigaFab Equipment, Stellar Semiconductor Tools, Zenith Automation Systems |

| Regions Covered |

North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst |

Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:

The Semiconductor Production Equipment Market is comprehensively segmented to provide granular insights into its diverse components. These segments include classifications by the type of equipment, its specific application within the semiconductor manufacturing process, the primary end-user industries adopting these technologies, and the geographical regions driving market demand. This multi-dimensional segmentation allows for a detailed understanding of market dynamics across various categories, enabling stakeholders to identify high-growth areas and tailor strategies accordingly.

- By Equipment Type: This segment distinguishes between equipment used in the initial stages of chip manufacturing and those employed in the final stages.

- Front-End Equipment: Tools used for wafer fabrication, creating the integrated circuits on silicon wafers.

- Lithography Equipment: Machines for patterning circuit designs onto wafers.

- Etch Equipment: Systems for removing material from the wafer surface according to patterns.

- Deposition Equipment: Tools for applying thin films of materials onto wafers.

- Ion Implantation Equipment: Devices for doping wafers with impurities to alter electrical properties.

- Cleaning Equipment: Systems for removing contaminants from wafers during various process steps.

- Metrology and Inspection Equipment: Instruments for measuring, monitoring, and inspecting wafers for quality control.

- Other Front-End Equipment: Includes furnaces, thermal processors, and chemical mechanical planarization (CMP) tools.

- Back-End Equipment: Tools for assembly, packaging, and testing of finished semiconductor devices.

- Packaging Equipment: Machines for die bonding, wire bonding, encapsulation, and other assembly processes.

- Test Equipment: Systems for electrical testing, functional testing, and quality assurance of packaged chips.

- By Application: Categorization based on the type of semiconductor manufacturing entity utilizing the equipment.

- Foundry: Companies that manufacture chips for other fabless design companies.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own chips.

- Outsourced Semiconductor Assembly and Test (OSAT) Companies: Firms specializing in post-fabrication services like assembly, packaging, and testing.

- By End-User Industry: Segmentation by the final industry where the semiconductors are deployed.

- Consumer Electronics: Devices like smartphones, laptops, and wearables.

- Automotive: Semiconductors for infotainment, ADAS, and electric vehicles.

- Healthcare: Chips for medical devices, diagnostics, and imaging.

- Industrial: Components for automation, robotics, and industrial control systems.

- IT & Telecommunications: Semiconductors for data centers, networking, and communication infrastructure.

- Others: Includes aerospace, defense, and research applications.

- By Regional: Geographical distribution of market revenue and growth opportunities.

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East, and Africa (MEA)

Regional Highlights

- Asia Pacific: This region is unequivocally the powerhouse of the global semiconductor industry and consequently the largest market for semiconductor production equipment. Countries like Taiwan, South Korea, China, and Japan host the world's leading foundries, IDMs, and OSAT companies, driving massive investments in new fab construction and capacity expansion. Government support, established supply chains, and a robust talent pool further solidify its dominance. The relentless demand for consumer electronics, automotive components, and advanced computing solutions from this region continues to fuel equipment procurement.

- North America: Driven by significant government incentives aimed at reshoring semiconductor manufacturing and fostering technological independence, North America is witnessing a resurgence in fab construction and equipment investment. The presence of leading research institutions, pioneering chip design companies, and a strong emphasis on R&D for next-generation technologies (like AI chips and quantum computing) makes it a critical region for advanced equipment demand. The United States, in particular, is a key focus area for significant capital expenditure.

- Europe: Europe is steadily increasing its footprint in semiconductor manufacturing, backed by initiatives focused on boosting domestic chip production and strengthening its position in niche markets like automotive, industrial, and specialized sensor technologies. Countries like Germany, France, and Ireland are attracting investments for new fabs and R&D centers, stimulating demand for highly specialized and energy-efficient production equipment. The region's focus on sustainable manufacturing also influences equipment design and procurement decisions.

- Middle East and Africa (MEA): While still a nascent market compared to other regions, MEA is emerging as a potential growth area for semiconductor production equipment. Driven by ambitions for economic diversification and technological self-reliance, several countries in the region are exploring investments in semiconductor manufacturing infrastructure. This nascent development presents long-term opportunities for equipment suppliers as foundational fabs and research facilities are established.

Top Key Players:

The market research report covers the analysis of key stake holders of the Semiconductor Production Equipment Market. Some of the leading players profiled in the report include -

- Precision Wafer Systems

- Global Etch Solutions

- Advanced Deposition Technologies

- Integrated Lithography Tools

- Quantum Test Systems

- NextGen Packaging Automation

- SmartFab Metrology

- Universal Process Control

- Future Wafer Solutions

- Dynamic Ion Implantation

- Apex Cleanroom Equipment

- OptiView Inspection

- Silicon Edge Innovations

- Core Microfab Systems

- Proximity Process Solutions

- Vector Chip Assembly

- Nexus Test & Measurement

- GigaFab Equipment

- Stellar Semiconductor Tools

- Zenith Automation Systems

Frequently Asked Questions:

What is the projected growth rate for the Semiconductor Production Equipment Market?

The Semiconductor Production Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, indicating robust expansion driven by increasing global demand for semiconductors.What was the market size of the Semiconductor Production Equipment Market in 2025?

The Semiconductor Production Equipment Market was valued at an estimated USD 110.5 billion in 2025. This figure reflects the significant capital investments made by semiconductor manufacturers in new and advanced production capabilities.Which key factors are driving the growth of the Semiconductor Production Equipment Market?

Key growth drivers include the escalating global demand for advanced semiconductors in consumer electronics, automotive, and AI applications, along with significant government investments and subsidies aimed at boosting domestic semiconductor manufacturing capacities worldwide.What are the primary segments covered in the Semiconductor Production Equipment Market report?

The report segments the market by Equipment Type (Front-End and Back-End, with sub-segments like Lithography, Etch, Deposition, Packaging, and Test Equipment), Application (Foundry, IDM, OSAT), End-User Industry (Consumer Electronics, Automotive, Healthcare, Industrial, IT & Telecom), and major Geographic Regions.What role does Artificial Intelligence play in the Semiconductor Production Equipment Market?

Artificial Intelligence significantly impacts the market by enabling advanced predictive maintenance for equipment, optimizing complex fabrication processes for improved yield, enhancing defect inspection capabilities through computer vision, and accelerating R&D cycles for new materials and processes.