Semiconductor NAND Memory Chip Market

Semiconductor NAND Memory Chip Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700818 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor NAND Memory Chip Market Size

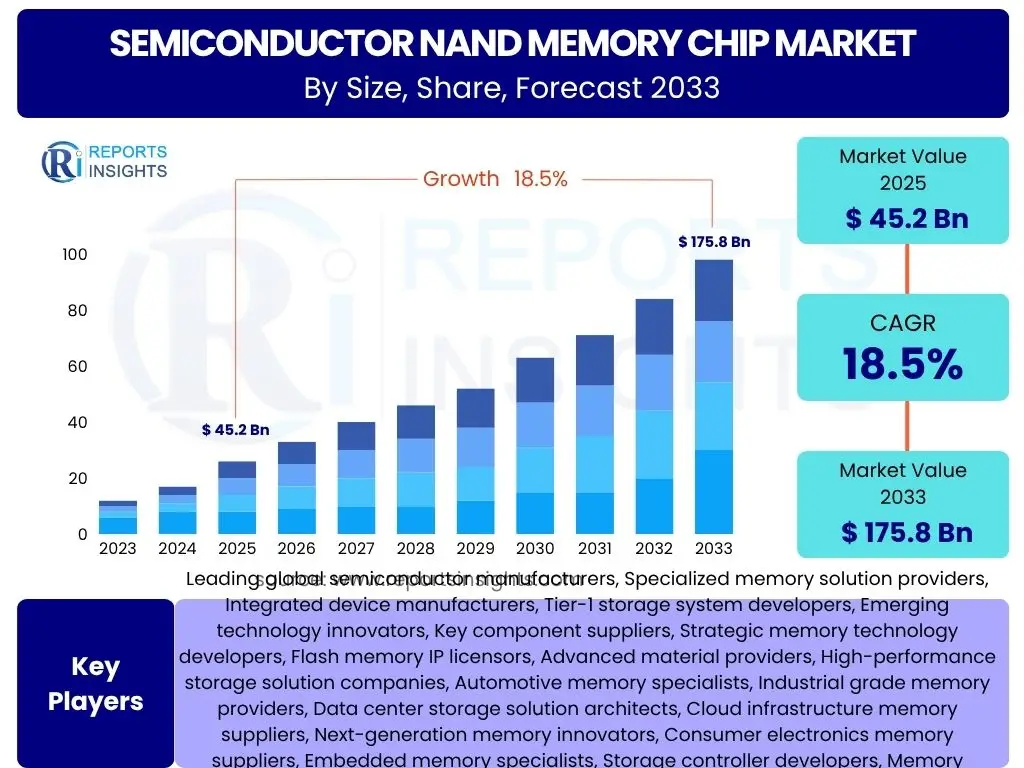

According to Reports Insights Consulting Pvt Ltd, The Semiconductor NAND Memory Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 45.2 billion in 2025 and is projected to reach USD 175.8 billion by the end of the forecast period in 2033.

Key Semiconductor NAND Memory Chip Market Trends & Insights

The Semiconductor NAND Memory Chip market is undergoing significant transformations driven by evolving technological landscapes and increasing data generation. Key trends indicate a persistent shift towards higher density solutions, particularly 3D NAND technology with increasing layer counts, which enables greater storage capacity within smaller footprints and at a lower cost per bit. This technological advancement is crucial for meeting the escalating demands from enterprise data centers, cloud infrastructure, and consumer electronics, all of which require vast amounts of fast, reliable storage.

Another prominent trend is the growing adoption of Quad-Level Cell (QLC) NAND, which stores four bits per cell, offering even higher densities and more cost-effective storage solutions compared to Triple-Level Cell (TLC) or Multi-Level Cell (MLC) technologies. While QLC may present challenges in terms of endurance and performance for certain applications, its cost benefits make it highly attractive for read-intensive workloads such as data archiving, content delivery networks, and consumer-grade SSDs. The continuous optimization of QLC technology, alongside advancements in controllers and error correction, is expanding its applicability across various market segments.

Furthermore, the market is witnessing an accelerating integration of NAND flash into a wider array of applications beyond traditional computing, including automotive systems, industrial IoT devices, and specialized AI hardware. This diversification of end-use cases is fueling innovation in package types, form factors, and interface technologies to cater to specific performance, power consumption, and environmental requirements. The strategic partnerships and vertical integration initiatives among memory manufacturers and system developers are also shaping the competitive landscape, aiming to optimize performance and supply chain efficiencies for next-generation storage solutions.

- Persistent shift towards higher density 3D NAND with increased layer counts.

- Rising adoption of Quad-Level Cell (QLC) NAND for cost-effective, high-capacity storage.

- Diversification of NAND applications into automotive, industrial IoT, and AI hardware.

- Advancements in controller technology and error correction mechanisms to enhance NAND performance and reliability.

- Strategic vertical integration and partnerships among industry players to optimize supply chains and product development.

AI Impact Analysis on Semiconductor NAND Memory Chip

The proliferation of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally reshaping the demand landscape for Semiconductor NAND Memory Chips. AI workloads, particularly deep learning training and inference, are inherently data-intensive, requiring immense volumes of high-speed storage for datasets, model parameters, and intermediate computations. This necessitates NAND solutions that offer not only high capacity but also exceptional read/write performance and endurance, driving innovation in advanced NAND architectures and interfaces like PCIe Gen5 and NVMe over Fabrics (NVMe-oF) to mitigate data bottlenecks.

Moreover, the trend towards edge AI, where AI processing occurs closer to the data source rather than exclusively in centralized cloud environments, is creating new opportunities for embedded and industrial-grade NAND solutions. Devices such as smart cameras, autonomous vehicles, industrial robots, and IoT sensors require robust, low-power, and high-capacity storage to manage on-device AI models and continuously generated data streams. This demand is pushing for more durable and energy-efficient NAND variants optimized for diverse operating conditions and longer product lifecycles.

Consequently, manufacturers are increasingly focusing their research and development efforts on optimizing NAND chips for AI-specific applications. This includes developing specialized NAND architectures that can more efficiently handle random access patterns typical of AI workloads, improving the garbage collection and wear-leveling algorithms, and integrating AI-friendly features into memory controllers. The symbiotic relationship between AI advancements and NAND technology evolution is expected to accelerate, with AI acting as a significant catalyst for continued growth and innovation within the semiconductor memory market.

- Increased demand for high-capacity, high-performance NAND for AI training and inference datasets.

- Accelerated adoption of advanced interfaces (e.g., PCIe Gen5, NVMe-oF) to support AI data throughput.

- Growth in embedded and industrial-grade NAND for edge AI applications in autonomous systems and IoT.

- Emphasis on developing AI-optimized NAND architectures, controllers, and firmware for efficient data handling.

- AI-driven innovation in NAND endurance, power efficiency, and form factors for diverse deployment scenarios.

Key Takeaways Semiconductor NAND Memory Chip Market Size & Forecast

The Semiconductor NAND Memory Chip market is poised for substantial growth over the forecast period, driven by an insatiable global demand for data storage across various sectors. The projected Compound Annual Growth Rate (CAGR) of 18.5% highlights a robust expansion, reflecting the critical role of NAND flash in enabling digital transformation and advanced technological ecosystems. This growth is fundamentally underpinned by the continuous generation of digital content, the expansion of cloud computing infrastructure, and the widespread adoption of smart devices and emerging technologies like AI and the Internet of Things (IoT).

A key takeaway from the market forecast is the significant increase in market valuation, from an estimated USD 45.2 billion in 2025 to USD 175.8 billion by 2033. This remarkable rise underscores the increasing reliance on non-volatile memory for diverse applications, ranging from consumer electronics like smartphones and personal computers to high-end enterprise Solid State Drives (SSDs) and sophisticated automotive systems. The demand for higher density and more cost-effective storage solutions will continue to be a primary driver, fostering ongoing innovation in NAND technology, particularly in 3D NAND and QLC advancements.

Furthermore, the market's trajectory indicates a strong resilience despite potential market fluctuations, with underlying demand fueled by long-term structural shifts in data consumption and processing. The ongoing technological evolution, coupled with the expansion into new application areas such as specialized AI hardware and industrial automation, ensures sustained market buoyancy. For stakeholders, this implies a need for continuous investment in research and development, capacity expansion, and strategic partnerships to capitalize on the burgeoning opportunities within the dynamic semiconductor memory landscape.

- Projected robust market growth at an 18.5% CAGR, reaching USD 175.8 billion by 2033.

- Growth primarily driven by escalating global data generation, cloud infrastructure expansion, and IoT adoption.

- Strong demand for higher density and cost-effective NAND solutions driving 3D NAND and QLC advancements.

- Increasing integration of NAND into diversified applications like AI, automotive, and industrial IoT.

- Continued investment in R&D and capacity expansion is crucial for market participants.

Semiconductor NAND Memory Chip Market Drivers Analysis

The Semiconductor NAND Memory Chip market is propelled by a confluence of powerful drivers that collectively contribute to its significant growth trajectory. The proliferation of smartphones, tablets, and other consumer electronics remains a foundational driver, as these devices increasingly require higher storage capacities to accommodate rich media, advanced applications, and user data. This consistent demand from the consumer segment pushes manufacturers to innovate in terms of density and cost efficiency.

Beyond consumer electronics, the exponential growth of cloud computing and data centers is a major catalyst. Cloud service providers require massive, scalable, and high-performance storage solutions to handle vast amounts of data generated globally, supporting everything from enterprise applications to streaming services. NAND-based Solid State Drives (SSDs) offer superior speed and lower power consumption compared to traditional Hard Disk Drives (HDDs), making them indispensable for modern data center infrastructure and driving a significant portion of the market's expansion.

Furthermore, the automotive industry's rapid adoption of advanced driver-assistance systems (ADAS), in-car infotainment, and autonomous driving technologies is creating a burgeoning demand for robust and reliable NAND memory. These applications require high-speed, high-endurance storage to process sensor data, run complex AI algorithms, and store navigation maps and software updates. Similarly, the expansion of the Internet of Things (IoT) across various industries, from smart homes to industrial automation, necessitates compact, low-power, and durable storage solutions, fueling the demand for embedded NAND chips.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Smartphones & Consumer Electronics | +4.0% | Asia Pacific, North America, Europe | 2025-2033 (Long-term) |

| Expansion of Cloud Computing & Data Centers | +5.5% | North America, Asia Pacific (China, India), Europe | 2025-2033 (Long-term) |

| Rising Adoption of AI, ML, & IoT Technologies | +4.5% | Global (Strong in North America, Asia Pacific) | 2025-2033 (Long-term) |

| Growth in Automotive (ADAS, Infotainment) | +3.0% | Europe, North America, Asia Pacific (Japan, South Korea, China) | 2025-2033 (Mid to Long-term) |

| Increasing Demand for Enterprise SSDs | +3.5% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

Semiconductor NAND Memory Chip Market Restraints Analysis

Despite robust growth, the Semiconductor NAND Memory Chip market faces several significant restraints that could impede its full potential. Price volatility and market oversupply are perennial challenges. The cyclical nature of the semiconductor industry often leads to periods of overproduction, resulting in sharp declines in average selling prices (ASPs). This price erosion can severely impact manufacturers' profitability and investment in future technologies, particularly when demand forecasts do not align precisely with production outputs. Such instability makes long-term planning difficult for market participants.

Another key restraint is the substantial capital expenditure and high research and development (R&D) costs associated with advancing NAND technology. Developing new generations of 3D NAND with higher layer counts and more complex architectures requires enormous investments in fabrication facilities, specialized equipment, and skilled engineering talent. The rapid pace of technological obsolescence further exacerbates this, as companies must constantly innovate to remain competitive, leading to significant financial burdens and risks for manufacturers.

Furthermore, the market is highly susceptible to global macroeconomic uncertainties and geopolitical tensions. Economic downturns can reduce consumer spending on electronics and enterprise investments in data infrastructure, directly impacting NAND demand. Geopolitical factors, such as trade disputes, technology export controls, or regional conflicts, can disrupt global supply chains, affecting raw material availability, manufacturing capabilities, and market access, thereby posing considerable risks to market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Volatility & Market Oversupply | -3.0% | Global | 2025-2033 (Cyclical) |

| High Capital Expenditure & R&D Costs | -2.5% | Global (Impacts major manufacturers) | 2025-2033 (Long-term) |

| Global Macroeconomic Uncertainties & Geopolitical Tensions | -2.0% | Global (Especially US-China, EU-Asia) | 2025-2028 (Short to Mid-term) |

| Technical Challenges in Scaling (Endurance, Performance) | -1.5% | Global | 2025-2030 (Mid-term) |

Semiconductor NAND Memory Chip Market Opportunities Analysis

Despite existing challenges, the Semiconductor NAND Memory Chip market is replete with significant opportunities that can drive substantial future growth. One major opportunity lies in the continuous advancements in 3D NAND technology, specifically the development of higher layer counts (e.g., beyond 200 or 300 layers) and innovative architectures like string stacking. These advancements enable even greater storage densities and lower cost per bit, opening new avenues for ultra-high-capacity SSDs and embedded solutions that can address the ever-increasing data storage demands across various industries.

The burgeoning fields of Artificial Intelligence (AI) and Machine Learning (ML), along with the expansion of edge computing, present enormous growth prospects. AI workloads require specialized high-performance storage solutions for training massive datasets and rapid inference. The shift towards processing data closer to its source at the edge creates demand for robust, energy-efficient NAND memory in devices ranging from smart sensors to autonomous vehicles. This creates a niche for customized NAND products optimized for specific AI and edge use cases, driving innovation in both hardware and software aspects of memory management.

Furthermore, the automotive industry's ongoing evolution towards autonomous vehicles and electric vehicles (EVs) offers a substantial long-term opportunity. These vehicles integrate numerous sensors, advanced computing platforms, and extensive software, all of which require vast amounts of secure, high-reliability NAND storage for data logging, infotainment systems, firmware updates, and critical operational data. The stringent quality and longevity requirements of automotive applications will foster demand for premium, ruggedized NAND solutions, commanding higher value and encouraging specialized product development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Next-Generation 3D NAND & QLC Technology | +3.5% | Global (Key R&D in Asia Pacific, North America) | 2025-2033 (Long-term) |

| Emergence of AI/ML and Edge Computing Applications | +4.0% | Global (Strong in North America, Asia Pacific, Europe) | 2025-2033 (Long-term) |

| Expanding Automotive Electronics & Autonomous Driving | +2.5% | Europe, North America, Asia Pacific | 2025-2033 (Mid to Long-term) |

| Increased Adoption of Enterprise & Data Center SSDs | +3.0% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

Semiconductor NAND Memory Chip Market Challenges Impact Analysis

The Semiconductor NAND Memory Chip market faces inherent technical and operational challenges that can impact its sustained growth and profitability. One primary technical challenge is the increasing difficulty in scaling NAND technology to achieve higher densities while maintaining acceptable levels of performance, endurance, and reliability. As 3D NAND layers increase, manufacturing complexities rise, leading to lower yields and higher production costs. Moreover, pushing beyond Quad-Level Cell (QLC) to Penta-Level Cell (PLC) or Hexa-Level Cell (HLC) introduces significant challenges in distinguishing voltage states, demanding more sophisticated error correction codes and advanced controllers, which can impact overall device endurance and speed.

Another significant challenge is the intense competition and the associated pressure to reduce the cost-per-bit. The market is dominated by a few major players who constantly strive to gain market share through aggressive pricing and technological innovation. This competitive environment can lead to periods of significant price erosion, squeezing profit margins for manufacturers, particularly smaller or less diversified ones. The need to continuously invest in cutting-edge R&D and manufacturing capabilities to stay competitive adds to the financial burden and risk for market participants.

Furthermore, global supply chain complexities and geopolitical risks pose substantial operational challenges. The highly interconnected nature of the semiconductor supply chain means that disruptions in one region, whether due to natural disasters, political instability, or trade disputes, can have ripple effects worldwide. Ensuring a stable and resilient supply of raw materials, manufacturing equipment, and skilled labor across different geographies remains a critical concern, impacting production schedules, delivery times, and overall market stability. Navigating these complexities requires robust risk management strategies and diversified supply networks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Scaling Limitations (Density, Endurance, Reliability) | -2.8% | Global (R&D concentrated in key regions) | 2025-2033 (Long-term) |

| Intense Competition & Pressure on Cost-per-bit | -3.2% | Global | 2025-2033 (Continuous) |

| Global Supply Chain Vulnerabilities & Geopolitical Risks | -2.5% | Global (Especially Asia Pacific, North America) | 2025-2028 (Short to Mid-term) |

| Ensuring Data Integrity and Security in High-Density Storage | -1.5% | Global | 2025-2033 (Ongoing) |

Semiconductor NAND Memory Chip Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Semiconductor NAND Memory Chip market, covering historical data, current market dynamics, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges influencing the industry. The report segments the market by product type, technology, application, and end-user industry, providing granular insights into each category. Furthermore, it includes a thorough regional analysis, highlighting key market trends and competitive landscapes across major geographic regions. A dedicated section profiles leading market players, offering insights into their strategies, product portfolios, and recent developments, ensuring a holistic understanding of the market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.2 Billion |

| Market Forecast in 2033 | USD 175.8 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading global semiconductor manufacturers, Specialized memory solution providers, Integrated device manufacturers, Tier-1 storage system developers, Emerging technology innovators, Key component suppliers, Strategic memory technology developers, Flash memory IP licensors, Advanced material providers, High-performance storage solution companies, Automotive memory specialists, Industrial grade memory providers, Data center storage solution architects, Cloud infrastructure memory suppliers, Next-generation memory innovators, Consumer electronics memory suppliers, Embedded memory specialists, Storage controller developers, Memory module assemblers, Turnkey memory solution providers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor NAND Memory Chip market is extensively segmented to provide a granular understanding of its diverse components and their respective market dynamics. These segmentations are critical for identifying specific growth drivers, competitive landscapes, and opportunities within various product categories, technological advancements, applications, and end-user industries. Analyzing these segments helps stakeholders pinpoint high-growth areas and tailor their strategies to specific market needs and demands, ensuring targeted development and market penetration efforts.

Product type segmentation differentiates between various forms of NAND memory widely used in commercial and consumer applications. SSDs represent the high-performance segment critical for enterprise and PC markets, offering superior speed and reliability. Embedded solutions like eMMC and UFS are vital for mobile devices, providing integrated storage with optimized performance for smartphones and tablets. Memory cards and USB flash drives cater to portable storage needs, illustrating the broad applicability of NAND across different form factors and use cases, each with distinct market drivers and technological requirements.

Technology-based segmentation highlights the evolution from planar (2D) NAND to advanced 3D NAND architectures. While 2D NAND (comprising SLC, MLC, TLC) still holds relevance in specific niche applications, the market's trajectory is overwhelmingly towards 3D NAND, which achieves higher densities by stacking memory cells vertically. Within 3D NAND, the transition from TLC to QLC is particularly impactful, enabling significantly lower cost-per-bit and catering to bulk storage needs, albeit with different performance and endurance characteristics. The application and end-user segments further define where these technologies are deployed, from demanding enterprise data centers and the growing automotive sector to pervasive consumer electronics, underscoring the ubiquitous nature of NAND flash memory in the digital economy.

- By Product Type:

- SSD (Solid State Drive)

- eMMC (Embedded MultiMediaCard)

- UFS (Universal Flash Storage)

- Memory Cards (SD, MicroSD)

- USB Flash Drives

- By Technology:

- 2D NAND (SLC, MLC, TLC)

- 3D NAND (TLC, QLC)

- By Application:

- Consumer Electronics (Smartphones, Tablets, PCs, Digital Cameras)

- Enterprise & Data Center (Servers, Storage Arrays, Cloud Infrastructure)

- Automotive (Infotainment, ADAS, Autonomous Driving Systems)

- Industrial (Industrial Automation, Robotics, Surveillance Systems)

- Telecommunications (Networking Equipment, Base Stations)

- Healthcare (Medical Imaging, Portable Devices)

- By End-User Industry:

- Mobile Devices

- Laptops/PCs

- Servers & Storage Systems

- Automotive Electronics

- Industrial Automation

- Networking & Communication

- Medical Devices

- Military & Aerospace

Regional Highlights

- Asia Pacific (APAC): APAC stands as the dominant region in the Semiconductor NAND Memory Chip market, primarily due to the presence of major memory manufacturers in South Korea, Japan, and Taiwan, which serve as global production hubs. The region also accounts for the largest share of global electronics manufacturing and consumption, particularly in smartphones, laptops, and other consumer devices. Rapid growth in cloud infrastructure development, IoT adoption, and automotive electronics in China and India further fuel the demand, making APAC a critical market for both supply and demand.

- North America: North America is a significant market driven by its robust cloud computing industry, substantial investments in data centers, and the high adoption rate of enterprise Solid State Drives (SSDs). The region is a hub for technological innovation, with strong demand from industries like AI, machine learning, and high-performance computing. Additionally, the presence of major technology companies and a mature consumer electronics market contribute substantially to the region's market share and advanced technology adoption.

- Europe: Europe represents a strong market for Semiconductor NAND Memory Chips, particularly driven by its established automotive industry and growing industrial automation sector. The region's focus on Industry 4.0 initiatives and smart factory developments increases the demand for embedded and industrial-grade NAND solutions. The expansion of cloud services and the increasing digitalization across various sectors, including healthcare and telecommunications, also contribute to market growth, albeit at a different pace than APAC or North America.

- Latin America: The Latin American market for Semiconductor NAND Memory Chips is characterized by emerging growth, primarily driven by increasing smartphone penetration, expanding internet connectivity, and growing investments in digital infrastructure. While smaller than other major regions, the rising adoption of cloud services and the gradual modernization of IT infrastructure in countries like Brazil and Mexico present opportunities for market expansion.

- Middle East and Africa (MEA): The MEA region is an nascent but growing market for NAND memory, propelled by governmental initiatives for digital transformation, increasing adoption of smartphones, and the development of data centers in key economies. Investments in smart city projects and diversification away from traditional industries are creating new avenues for technology adoption, including advanced storage solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor NAND Memory Chip Market.- Leading Global Semiconductor Manufacturer A

- Major Memory Technology Innovator B

- Advanced Storage Solutions Provider C

- Integrated Device Manufacturer D

- High-Performance Flash Memory Company E

- Specialized Embedded Memory Producer F

- Global Storage Product Developer G

- Enterprise SSD Solution Specialist H

- Next-Generation Memory Architect I

- Key Component Supplier J

- Strategic Memory Partner K

- Industrial & Automotive Memory Provider L

- Cloud & Data Center Memory Innovator M

- Consumer Electronics Memory Supplier N

- Emerging Technology Memory Company O

- Flash Memory Control Solution Provider P

- Memory Module Integrator Q

- Advanced Packaging Memory Company R

- High-Density Storage Leader S

- Reliable Non-Volatile Memory Firm T

Frequently Asked Questions

Analyze common user questions about the Semiconductor NAND Memory Chip market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Semiconductor NAND Memory Chip and its primary function?

A Semiconductor NAND Memory Chip is a type of non-volatile flash memory that retains data even when power is off. Its primary function is to store digital information for various electronic devices, offering high storage density, faster read/write speeds, and lower power consumption compared to traditional hard drives, making it ideal for solid-state drives, smartphones, and other digital devices.

What are the key factors driving the growth of the NAND memory market?

The NAND memory market's growth is primarily driven by the escalating demand for data storage from cloud computing and data centers, the continuous proliferation of smartphones and consumer electronics, the expansion of the Internet of Things (IoT), and the rapid advancements in automotive electronics, including ADAS and autonomous driving systems, all requiring higher capacity and faster memory solutions.

How does 3D NAND technology differ from 2D NAND and why is it important?

3D NAND technology stacks memory cells vertically in multiple layers, unlike 2D (planar) NAND which arranges cells horizontally on a single plane. This vertical stacking allows for significantly higher storage densities within a smaller footprint and at a lower cost per bit, making it crucial for meeting the increasing storage demands of modern applications and devices while improving performance and power efficiency.

What is the impact of Artificial Intelligence (AI) on the demand for Semiconductor NAND Memory Chips?

AI significantly boosts demand for NAND memory chips by requiring vast amounts of high-speed storage for training large datasets and facilitating rapid inference. AI workloads drive the need for high-capacity, high-performance NAND solutions in data centers, as well as robust, low-power embedded NAND in edge AI devices like autonomous vehicles and smart sensors, accelerating innovation in NAND technology.

What are the main challenges faced by the Semiconductor NAND Memory Chip market?

The main challenges include intense price volatility and potential market oversupply, which can impact profitability. Additionally, the high capital expenditure and escalating research and development costs associated with advancing NAND technology, along with technical scaling limitations and global supply chain vulnerabilities, pose significant hurdles for market participants.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted