Semiconductor Capital Equipment Market

Semiconductor Capital Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704120 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Capital Equipment Market Size

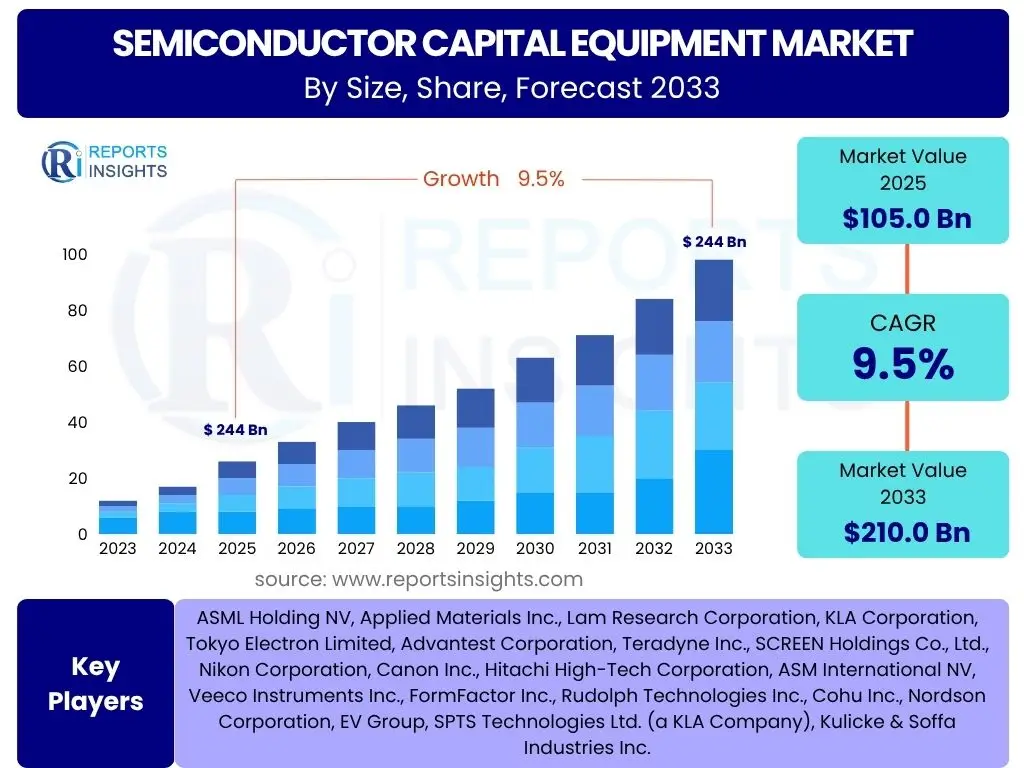

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Capital Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 105.0 billion in 2025 and is projected to reach USD 210.0 billion by the end of the forecast period in 2033.

Key Semiconductor Capital Equipment Market Trends & Insights

Current discussions and queries regarding the Semiconductor Capital Equipment market frequently center on how technological advancements, geopolitical influences, and evolving consumer electronics demand are shaping the industry. A recurring theme is the push towards advanced manufacturing processes, driven by the increasing complexity and miniaturization of semiconductor devices. The imperative for higher performance, lower power consumption, and greater integration across various applications fuels innovation in equipment design and functionality. Furthermore, sustainability and supply chain resilience are emerging as critical considerations, influencing investment decisions and operational strategies within the sector.

The market is experiencing a significant shift towards advanced packaging solutions, such as 3D stacking and chiplets, which necessitate new types of equipment for bonding, inspection, and testing. This trend is complemented by the continuous evolution of lithography, etching, and deposition technologies, aiming for ever-smaller feature sizes and improved yield. Regionalization of supply chains, spurred by geopolitical considerations and the desire for self-sufficiency in semiconductor manufacturing, is leading to substantial investments in new fabrication facilities worldwide. This global expansion directly translates into increased demand for a broad spectrum of capital equipment, from front-end processing to back-end assembly and test.

- Advanced Lithography Progression: Continued investment in EUV and next-generation lithography solutions for smaller nodes.

- Advanced Packaging Technologies: Growth in demand for equipment supporting 3D integration, chiplets, and wafer-level packaging.

- Increased Automation and AI Integration: Adoption of AI and machine learning for predictive maintenance, process optimization, and enhanced fab efficiency.

- Regionalization of Manufacturing: Expansion of semiconductor fabrication facilities in diverse geographies, driven by geopolitical and supply chain resilience goals.

- Sustainability and Energy Efficiency: Focus on developing and deploying equipment with reduced environmental footprint and lower energy consumption.

- Data Center and AI Accelerator Demand: Surging demand for high-performance computing (HPC) and AI chips fuels investment in specialized equipment.

AI Impact Analysis on Semiconductor Capital Equipment

Common inquiries related to the impact of Artificial Intelligence (AI) on Semiconductor Capital Equipment largely revolve around two primary aspects: how AI drives the demand for more sophisticated chips, thereby necessitating advanced equipment, and how AI itself is being integrated into the manufacturing process to enhance efficiency and yield. Users are keen to understand the specific types of equipment benefiting most from the AI surge and whether AI-driven manufacturing will lead to fundamentally new operational paradigms within semiconductor fabs. The overarching expectation is that AI will be a profound accelerator for both the demand side and the operational side of the capital equipment market.

The proliferation of AI and High-Performance Computing (HPC) applications, from data centers and edge devices to autonomous vehicles and IoT, is a major catalyst for the semiconductor industry. These applications demand chips with unparalleled processing power, memory capacity, and energy efficiency, pushing the boundaries of current manufacturing capabilities. This necessitates continuous innovation in front-end equipment for lithography, etching, and deposition to achieve smaller transistors and more complex circuit designs. Similarly, back-end equipment for advanced packaging and high-speed testing sees increased demand to ensure the integrity and performance of these sophisticated AI-optimized components.

Beyond driving chip demand, AI and Machine Learning (ML) are increasingly being integrated into the semiconductor manufacturing process itself. AI algorithms are employed for real-time process control, predictive maintenance of equipment, yield optimization, and defect detection, leading to significant improvements in operational efficiency and cost reduction. For instance, AI-powered systems can analyze vast amounts of sensor data from equipment to predict failures before they occur, minimizing downtime. Furthermore, AI is crucial in designing and simulating new chip architectures, leading to more efficient R&D cycles for equipment manufacturers. This dual impact positions AI as both a primary demand driver and a transformative operational tool for the semiconductor capital equipment market.

- Increased Demand for High-Performance Chips: AI and HPC drive the need for advanced logic, memory, and specialized accelerator chips, requiring cutting-edge manufacturing equipment.

- Technological Acceleration: Fuels R&D in advanced lithography, etching, and deposition to achieve smaller nodes and higher transistor density.

- Optimization of Manufacturing Processes: AI/ML algorithms enhance equipment performance, predictive maintenance, yield management, and quality control in fabs.

- Growth in Advanced Packaging Equipment: AI chips often utilize advanced packaging solutions (e.g., HBM, 2.5D/3D), boosting demand for related assembly and test equipment.

- New Design Methodologies: AI aids in optimizing chip design and layout, indirectly influencing demand for design automation tools and validation equipment.

- Data-Driven Decision Making: Real-time data analysis from equipment using AI improves operational efficiency and capacity planning for manufacturers.

Key Takeaways Semiconductor Capital Equipment Market Size & Forecast

Analysis of common user questions regarding key takeaways from the Semiconductor Capital Equipment market size and forecast reveals a strong emphasis on understanding the resilience and growth drivers of the industry amidst global economic fluctuations. Users are particularly interested in identifying the primary forces behind the market's projected expansion, the impact of technological transitions, and the strategic implications for businesses operating within or dependent on the semiconductor ecosystem. There's also a significant focus on how geopolitical shifts and supply chain dynamics are influencing long-term investment and market stability.

The market is poised for robust expansion, primarily fueled by the pervasive digitalization across industries and the accelerating adoption of advanced technologies such as Artificial Intelligence, 5G, and the Internet of Things. These macro trends create an insatiable demand for more powerful and efficient semiconductor devices, directly translating into increased orders for sophisticated capital equipment. Furthermore, the global push for domestic semiconductor manufacturing capabilities, driven by national security and economic resilience objectives, is stimulating massive investments in new fabrication facilities worldwide. This expansion of manufacturing capacity is a direct and significant contributor to the market's growth trajectory, ensuring sustained demand for a wide array of equipment over the forecast period.

A critical takeaway is the increasing importance of technological leadership and innovation. As chip designs become more complex and feature sizes shrink, equipment manufacturers must continuously innovate to provide the advanced lithography, etching, deposition, and metrology solutions required by leading-edge fabs. The market's future growth is heavily dependent on overcoming technical challenges associated with next-generation nodes and advanced packaging. Additionally, the industry's interconnected nature means that global economic health, trade policies, and supply chain stability will continue to play a pivotal role in shaping market dynamics, requiring strategic agility from all stakeholders.

- Sustained Growth Momentum: The market is projected for significant growth, driven by fundamental long-term trends in digitalization and technological adoption.

- Technology-Driven Expansion: Advanced technologies like AI, 5G, IoT, and high-performance computing are primary catalysts for equipment demand.

- Global Fab Expansion: Widespread investments in new semiconductor manufacturing facilities globally are a key demand driver for capital equipment.

- Innovation Imperative: Continuous R&D in advanced process technologies (e.g., EUV, advanced packaging) is crucial for market leadership and growth.

- Geopolitical Influence: Government initiatives and regionalization strategies are significantly impacting investment patterns and supply chain development.

- Resilience Amidst Challenges: Despite economic uncertainties, the foundational role of semiconductors ensures sustained investment and a positive long-term outlook.

Semiconductor Capital Equipment Market Drivers Analysis

The Semiconductor Capital Equipment market is propelled by a confluence of powerful forces stemming from both technological advancements and pervasive digitalization. The insatiable global demand for advanced electronic devices, ranging from smartphones and high-performance computing systems to automotive electronics and IoT devices, forms the bedrock of this market's growth. Each new generation of these devices demands more powerful, compact, and energy-efficient chips, directly stimulating the need for sophisticated manufacturing equipment capable of achieving smaller feature sizes and higher yields.

Furthermore, the escalating adoption of transformative technologies such as Artificial Intelligence (AI), 5G connectivity, and the Internet of Things (IoT) is creating unprecedented demand for specialized semiconductor components. AI, in particular, requires high-performance processors and memory, driving significant investment in advanced logic and memory fabrication facilities. Similarly, the rollout of 5G networks and the proliferation of IoT devices necessitate a vast array of new chips, which in turn fuels the market for equipment used in their production. Government initiatives and strategic investments in domestic semiconductor manufacturing capabilities, prompted by supply chain security concerns, also serve as substantial drivers, accelerating the establishment of new fabs and the modernization of existing ones.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand for Advanced Electronics & Computing | +2.5% | Global, particularly Asia Pacific (China, Korea, Taiwan), North America | Long-term (2025-2033) |

| Rapid Adoption of AI, 5G, & IoT Technologies | +2.0% | Global, especially North America, Asia Pacific (China, Japan), Europe | Mid to Long-term (2025-2030) |

| Government Initiatives & Strategic Investments in Domestic Manufacturing | +1.5% | North America (US), Europe (EU), Asia Pacific (Japan, India) | Mid-term (2025-2028) |

| Transition to Advanced Packaging Technologies | +1.0% | Global, concentrated in Taiwan, South Korea, US | Mid to Long-term (2026-2033) |

Semiconductor Capital Equipment Market Restraints Analysis

Despite robust growth prospects, the Semiconductor Capital Equipment market faces several significant restraints that could temper its expansion. One primary concern is the escalating cost of developing and acquiring cutting-edge equipment. As semiconductor technology progresses to smaller nodes and more complex architectures, the R&D expenditure for equipment manufacturers and the capital investment required by chipmakers become astronomical. This high cost of entry and continuous upgrade cycle can limit market participation and slow down technology adoption, particularly for smaller players or in times of economic uncertainty.

Geopolitical tensions and trade disputes represent another substantial restraint. The highly globalized nature of the semiconductor supply chain makes it vulnerable to political shifts, tariffs, and export controls. Restrictions on technology transfer or access to specific markets can disrupt supply chains, reduce investment, and create uncertainty, directly impacting equipment sales and deployment. Furthermore, the semiconductor industry is inherently cyclical, prone to boom-and-bust cycles driven by global economic conditions and inventory fluctuations. While the long-term outlook remains positive, these cyclical downturns can lead to temporary overcapacity, reduced capital expenditure by chip manufacturers, and slower growth rates for equipment providers, posing a challenge for consistent market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure & R&D Costs | -1.2% | Global, impacts new entrants and smaller players heavily | Long-term (2025-2033) |

| Geopolitical Tensions & Trade Restrictions | -1.0% | Global, particularly US-China, Europe-Asia trade routes | Mid-term (2025-2028) |

| Industry Cyclicality & Economic Downturns | -0.8% | Global, reflects macroeconomic trends | Short to Mid-term (2025-2027) |

| Supply Chain Vulnerabilities & Raw Material Shortages | -0.5% | Global, critical materials sourced from specific regions | Short-term (2025-2026) |

Semiconductor Capital Equipment Market Opportunities Analysis

The Semiconductor Capital Equipment market is rich with opportunities arising from both technological evolution and expanding application landscapes. The continuous drive towards miniaturization and enhanced performance in semiconductors creates a perpetual need for next-generation lithography, etching, and deposition tools. Investments in Extreme Ultraviolet (EUV) lithography and beyond, as well as advancements in atomic layer deposition (ALD) and advanced dry etching, represent significant avenues for growth as chipmakers strive for sub-5nm and even sub-2nm nodes. This technological frontier ensures sustained demand for highly specialized and innovative equipment.

Another major opportunity lies in the burgeoning field of advanced packaging. As traditional scaling approaches face physical limits, heterogenous integration, 3D stacking, and chiplet architectures are becoming critical for achieving higher performance and functionality. This shift necessitates new types of back-end equipment for bonding, inspection, and testing that can handle the increased complexity and precision required for these advanced packages. Furthermore, the growing focus on sustainability and energy efficiency across the industry presents opportunities for equipment manufacturers to develop more environmentally friendly and power-optimized solutions, aligning with global regulatory trends and corporate ESG goals. The expansion into emerging markets, particularly in Southeast Asia and India, as these regions seek to establish or expand their domestic semiconductor manufacturing capabilities, also offers substantial growth potential for equipment sales and service.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced Packaging Technologies | +1.8% | Global, particularly Taiwan, South Korea, US, Japan | Mid to Long-term (2025-2033) |

| Development of Next-Gen Lithography & Metrology | +1.5% | Global, concentrated in Netherlands, US, Japan, Germany | Long-term (2026-2033) |

| Expansion into Emerging Markets & Regional Hubs | +1.2% | India, Southeast Asia (Vietnam, Malaysia), Europe | Mid-term (2025-2030) |

| Focus on Fab Automation & Smart Manufacturing | +0.8% | Global, especially leading semiconductor manufacturing regions | Mid-term (2025-2029) |

Semiconductor Capital Equipment Market Challenges Impact Analysis

The Semiconductor Capital Equipment market, while promising, faces inherent challenges that demand strategic navigation. One significant hurdle is the escalating complexity and cost of R&D, particularly for cutting-edge technologies like EUV lithography. Developing equipment for smaller process nodes requires immense financial investment and specialized expertise, leading to extended development cycles and higher unit costs. This can strain manufacturers' resources and increase the risk associated with bringing new products to market, potentially slowing down the pace of technological adoption across the industry.

Another critical challenge is the intense technological obsolescence rate. The semiconductor industry evolves rapidly, with new process technologies and chip architectures emerging frequently. This rapid pace means that capital equipment can become outdated quickly, necessitating continuous upgrades or replacement cycles for chip manufacturers, and forcing equipment providers to maintain a constant innovation pipeline. Furthermore, ensuring a robust and resilient global supply chain for critical components and raw materials remains a persistent challenge, exacerbated by geopolitical dynamics and unforeseen events like pandemics, leading to potential delays in equipment delivery and increased operational costs. Attracting and retaining highly skilled talent, particularly engineers with expertise in complex equipment design and manufacturing, is also a growing concern, impacting innovation and operational efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D Investment & Technological Complexity | -1.5% | Global, particularly for leading-edge equipment providers | Long-term (2025-2033) |

| Rapid Technological Obsolescence | -1.0% | Global, affects all equipment types and end-users | Continuous |

| Supply Chain Disruptions & Geopolitical Risks | -0.8% | Global, impacts critical components and logistics | Short to Mid-term (2025-2027) |

| Skilled Labor Shortages & Talent Acquisition | -0.7% | Global, particularly in specialized engineering fields | Long-term (2025-2033) |

Semiconductor Capital Equipment Market - Updated Report Scope

This report offers an in-depth analysis of the Semiconductor Capital Equipment Market, encompassing a comprehensive evaluation of its current size, historical performance, and future growth projections. It delves into the critical market trends, identifies key growth drivers, assesses potential restraints, and highlights emerging opportunities and persistent challenges that shape the industry landscape. The scope includes detailed segmentation analysis by equipment type, application, and end-user, providing granular insights into various market segments. Furthermore, a thorough regional analysis outlines the dynamics across major geographical areas, complementing profiles of leading market players to provide a holistic view of the competitive environment and strategic considerations for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 105.0 Billion |

| Market Forecast in 2033 | USD 210.0 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML Holding NV, Applied Materials Inc., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited, Advantest Corporation, Teradyne Inc., SCREEN Holdings Co., Ltd., Nikon Corporation, Canon Inc., Hitachi High-Tech Corporation, ASM International NV, Veeco Instruments Inc., FormFactor Inc., Rudolph Technologies Inc., Cohu Inc., Nordson Corporation, EV Group, SPTS Technologies Ltd. (a KLA Company), Kulicke & Soffa Industries Inc. |

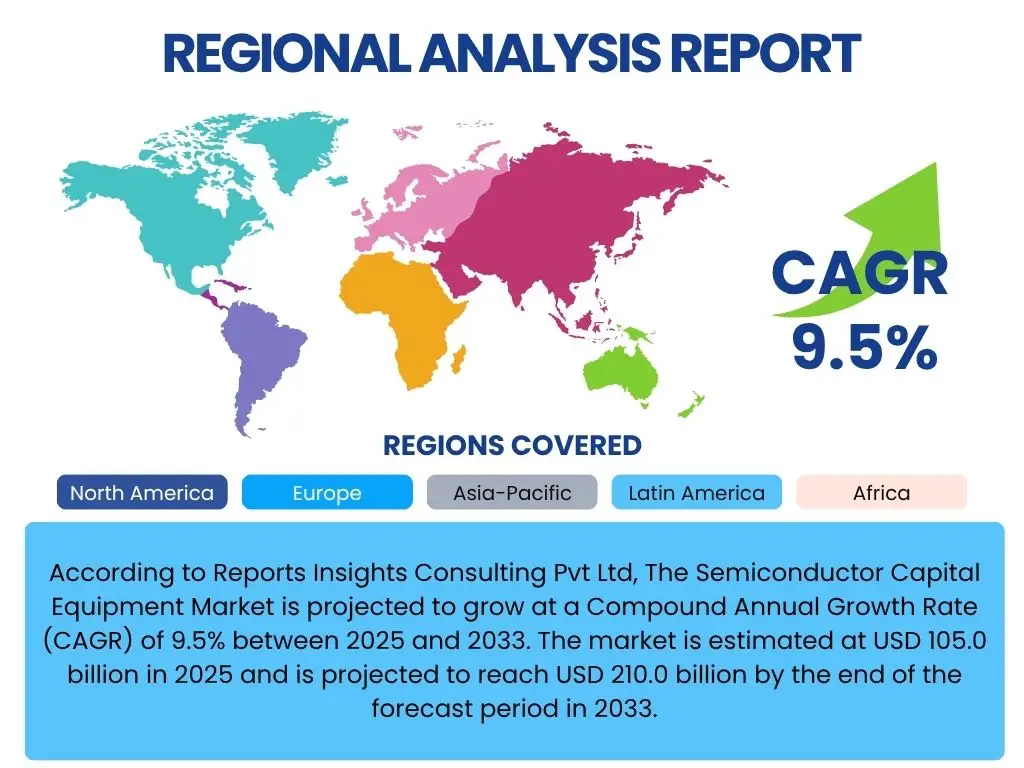

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Capital Equipment market is extensively segmented to provide a detailed understanding of its diverse components and drivers. These segmentations allow for a granular analysis of market dynamics, revealing specific growth areas and investment opportunities across various technologies, applications, and end-user industries. Understanding these segments is crucial for stakeholders to tailor their strategies, identify niche markets, and respond effectively to evolving industry demands.

- By Equipment Type: This segment includes Wafer Processing Equipment (such as Lithography Equipment, Etching Equipment, Deposition Equipment, Ion Implantation Equipment, Cleaning Equipment, and Others), Assembly & Packaging Equipment (covering Dicing, Bonding, Inspection, Test & Metrology Equipment), and Test Equipment (including Automatic Test Equipment (ATE), Probers, and Handlers).

- By Application: This segment differentiates between Foundry operations, which produce chips for other companies, and Integrated Device Manufacturers (IDMs), which design and manufacture their own chips.

- By End-User: This segment categorizes the market based on the type of semiconductor devices produced, including Memory (DRAM, NAND), Logic (CPUs, GPUs), Foundry (services for fabless companies), Power (power management ICs), MEMS (Micro-Electro-Mechanical Systems), and other specialized semiconductor applications.

Regional Highlights

- Asia Pacific (APAC): Dominates the semiconductor capital equipment market, driven by significant investments in fabrication facilities in countries like Taiwan, South Korea, China, and Japan. This region is home to the largest foundries and memory manufacturers, consistently driving demand for advanced wafer processing and packaging equipment. Government incentives and a robust electronics manufacturing ecosystem further solidify APAC's leading position.

- North America: A major hub for semiconductor R&D and advanced manufacturing, particularly in leading-edge process technology and high-performance computing. Substantial investments under initiatives like the CHIPS Act are fueling new fab construction and expansion, creating strong demand for all types of capital equipment, especially for cutting-edge lithography and test solutions.

- Europe: Characterized by strong innovation in automotive, industrial, and specialized semiconductor applications. Countries such as Germany, the Netherlands, and France are investing in advanced manufacturing capabilities and R&D, particularly in areas like advanced lithography (e.g., ASML) and specialized process equipment, contributing significantly to the market.

- Latin America, Middle East, and Africa (MEA): While currently smaller markets, these regions are showing increasing interest in establishing or expanding their semiconductor ecosystems. Initiatives in countries like India (often grouped with APAC for semiconductor market analysis but strategically distinct in its growth phase) and parts of the Middle East suggest emerging opportunities for equipment providers as these regions aim for greater technological self-sufficiency and industrial development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Capital Equipment Market.- ASML Holding NV

- Applied Materials Inc.

- Lam Research Corporation

- KLA Corporation

- Tokyo Electron Limited

- Advantest Corporation

- Teradyne Inc.

- SCREEN Holdings Co., Ltd.

- Nikon Corporation

- Canon Inc.

- Hitachi High-Tech Corporation

- ASM International NV

- Veeco Instruments Inc.

- FormFactor Inc.

- Rudolph Technologies Inc.

- Cohu Inc.

- Nordson Corporation

- EV Group

- SPTS Technologies Ltd. (a KLA Company)

- Kulicke & Soffa Industries Inc.

Frequently Asked Questions

What is the projected growth rate of the Semiconductor Capital Equipment Market?

The Semiconductor Capital Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, reaching USD 210.0 billion by 2033.

What are the primary drivers for the Semiconductor Capital Equipment Market?

Key drivers include the surging global demand for advanced electronics, rapid adoption of AI, 5G, and IoT technologies, significant government initiatives supporting domestic manufacturing, and the ongoing transition to advanced packaging solutions.

How does AI impact the Semiconductor Capital Equipment industry?

AI significantly impacts the market by driving demand for high-performance chips, necessitating cutting-edge equipment, and by being integrated into manufacturing processes to optimize efficiency, enhance predictive maintenance, and improve yield management in fabs.

Which regions are key contributors to the Semiconductor Capital Equipment Market?

Asia Pacific (APAC), particularly Taiwan, South Korea, China, and Japan, dominates the market due to extensive manufacturing investments. North America and Europe are also significant contributors, driven by R&D, advanced manufacturing, and strategic government initiatives.

What are the main challenges faced by the Semiconductor Capital Equipment Market?

Major challenges include high R&D investment costs, rapid technological obsolescence, potential supply chain disruptions due to geopolitical factors, and the persistent shortage of highly skilled labor within the industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted