Semiconductor Material Market

Semiconductor Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700765 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

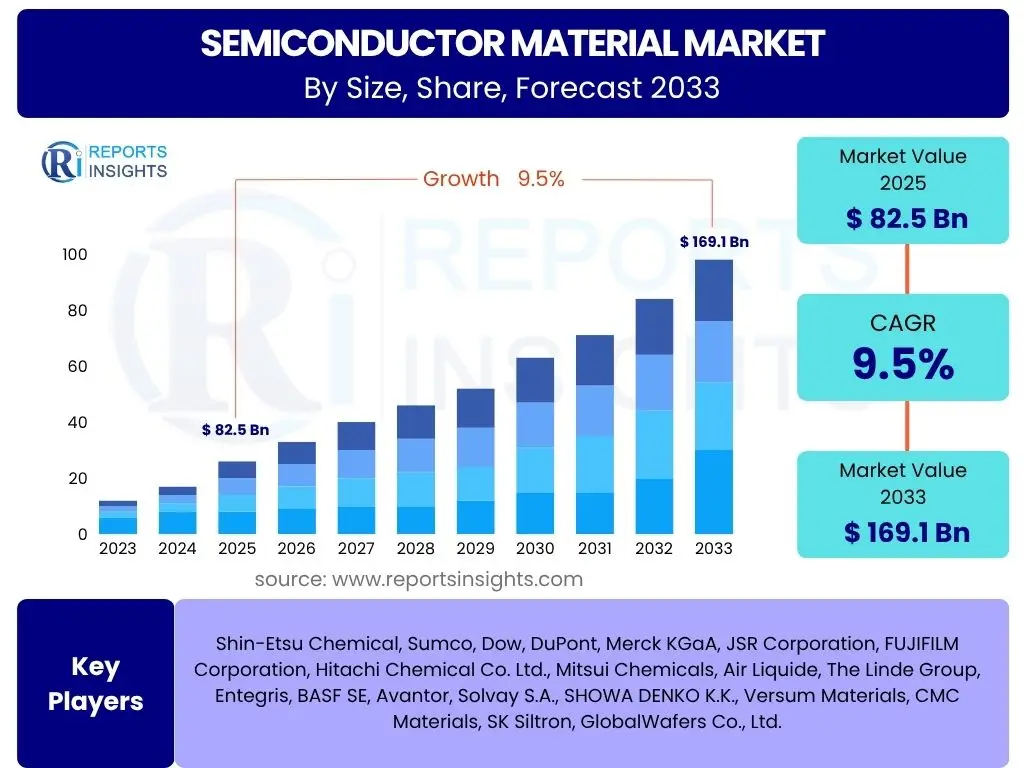

Semiconductor Material Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 82.5 billion in 2025 and is projected to reach USD 169.1 billion by the end of the forecast period in 2033.

The robust expansion of the semiconductor material market is primarily driven by the escalating global demand for advanced electronic devices. This includes not only consumer electronics but also the burgeoning sectors of artificial intelligence, high-performance computing, 5G technology, and electric vehicles, all of which rely heavily on sophisticated semiconductor components. The underlying growth in chip manufacturing capacity worldwide necessitates a continuous and increasing supply of high-purity and specialized materials.

Furthermore, the ongoing digitalization across various industries, coupled with significant investments in fab expansion and new technology development, consistently fuels the demand for a diverse range of semiconductor materials. The market's trajectory reflects a global commitment to technological advancement, emphasizing both the volume and the complexity of materials required for next-generation semiconductor fabrication.

Key Semiconductor Material Market Trends & Insights

Analysis of common user questions reveals a strong interest in the evolving landscape of semiconductor material trends, particularly concerning innovation, sustainability, and supply chain resilience. Users frequently inquire about the materials driving next-generation chip designs, the industry's response to environmental concerns, and strategies for mitigating supply disruptions. There is significant curiosity regarding the adoption of novel materials for enhanced performance and the impact of geopolitical factors on material availability.

The market is witnessing a profound shift towards advanced materials that can support smaller process nodes and complex packaging technologies, such as 3D integration and chiplets. This includes a heightened focus on high-purity chemicals, specialty gases, and novel substrates. Concurrently, sustainability is becoming a core consideration, with increasing efforts towards reducing waste, optimizing resource usage, and developing eco-friendly manufacturing processes for semiconductor materials. Geopolitical dynamics are also shaping regional supply chain diversification strategies, emphasizing the importance of localized or resilient material sourcing.

- Growing adoption of advanced packaging materials, including those for chiplets and heterogeneous integration.

- Rising demand for high-purity process chemicals and specialty gases critical for sub-7nm fabrication processes.

- Increasing focus on sustainable and green manufacturing practices within the material supply chain.

- Development and commercialization of novel materials such as Gallium Nitride (GaN) and Silicon Carbide (SiC) for power electronics and RF applications.

- Emphasis on supply chain diversification and regionalization to enhance resilience against geopolitical risks.

AI Impact Analysis on Semiconductor Material

User inquiries regarding the impact of Artificial Intelligence (AI) on the Semiconductor Material market frequently center on how AI's exponential growth translates into specific material demands, particularly for high-performance computing (HPC) and advanced memory solutions. Common concerns include the need for enhanced thermal management materials, the purity requirements for AI-optimized silicon, and the implications for packaging innovations driven by AI chip architectures. Users also express interest in how AI itself might optimize material discovery and manufacturing processes.

The proliferation of AI applications, from data centers to edge devices, is a primary catalyst for increased demand for specialized semiconductor materials. AI workloads necessitate chips with higher transistor densities, faster processing speeds, and superior power efficiency, which directly translates to a need for ultra-pure silicon wafers, advanced photoresists for intricate lithography, and innovative materials for thermal interface management. Furthermore, the push for AI accelerators and dedicated neural processing units (NPUs) drives the adoption of advanced packaging materials to enable multi-chip module and system-in-package solutions, facilitating greater computational density.

- Accelerated demand for high-performance silicon wafers, optimized for AI processors and memory.

- Increased need for advanced thermal management materials (e.g., thermal interface materials, heat sinks) to dissipate heat from powerful AI chips.

- Surge in consumption of high-purity process chemicals and specialty gases for advanced logic and memory fabrication processes.

- Stimulus for innovation in advanced packaging materials, supporting multi-die integration and chiplet architectures crucial for AI hardware.

- Potential for AI algorithms to optimize material design, synthesis, and quality control, leading to more efficient material production.

Key Takeaways Semiconductor Material Market Size & Forecast

Analysis of common user questions about the Semiconductor Material market size and forecast highlights primary interests in the sustainability of market growth, the key drivers underpinning this expansion, and the potential for new entrants or disruptive technologies. Users are keen to understand if the current growth trajectory is sustainable given global economic fluctuations, and which technological advancements or end-use sectors will contribute most significantly to market value over the forecast period. There is also a notable interest in the strategic importance of this market to the broader technology ecosystem.

The forecast indicates sustained robust growth for the semiconductor material market, fundamentally driven by the pervasive digitalization across all sectors and continuous innovation in semiconductor technology. This growth is not merely volumetric but also reflects a shift towards more complex and specialized materials required for smaller nodes and advanced packaging. The strategic importance of secure and diverse material supply chains has become paramount, influencing investment decisions and geopolitical considerations. The market is poised for continued expansion, underpinned by technological evolution and increasing global connectivity.

- The semiconductor material market exhibits consistent growth, projected to nearly double by 2033, underscoring its foundational role in the global technology industry.

- Technological advancements in AI, 5G, IoT, and automotive electronics are the primary catalysts for the escalating demand for highly specialized and ultra-pure materials.

- Investments in new fab capacity and R&D for advanced process nodes directly translate to increased material consumption and innovation requirements.

- Supply chain resilience and the strategic localization of material production are critical factors influencing market stability and future growth.

- The market's expansion is intrinsically linked to the overall health and innovation cycles of the global semiconductor industry, particularly in advanced manufacturing regions.

Semiconductor Material Market Drivers Analysis

The semiconductor material market is propelled by a confluence of technological advancements and increasing global demand for electronic devices. The proliferation of digital technologies across various sectors mandates a continuous evolution in semiconductor capabilities, directly impacting the demand for sophisticated materials. This extends beyond consumer electronics to critical infrastructure and emerging applications, creating a robust and expanding requirement for a diverse range of semiconductor materials.

Innovation in chip design, coupled with government initiatives aimed at strengthening domestic semiconductor supply chains, further stimulates market growth. As process nodes shrink and chip architectures become more complex, the need for ultra-pure, high-performance, and novel materials intensifies. This technological imperative, combined with strategic economic policies, forms the bedrock of the market's positive trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rise of AI, IoT, and 5G Technologies | +1.8% | Global | Short to Mid-term (2025-2029) |

| Increasing Demand for Advanced Packaging | +1.4% | Global | Mid-term (2027-2033) |

| Growth in Electric Vehicles (EVs) and Automotive Electronics | +1.1% | North America, Europe, Asia Pacific | Mid to Long-term (2028-2033) |

| Government Initiatives and Investments in Domestic Manufacturing | +0.9% | US, EU, China, Japan, South Korea | Short to Mid-term (2025-2030) |

| Expansion of Data Centers and Cloud Computing Infrastructure | +0.7% | Global | Short to Mid-term (2025-2029) |

Semiconductor Material Market Restraints Analysis

While the semiconductor material market exhibits strong growth potential, it is not without significant impediments. The highly specialized nature of these materials and the intricate global supply chains make the market susceptible to various external pressures. Geopolitical tensions, for instance, can swiftly disrupt the flow of essential raw materials or impede cross-border trade, leading to supply shortages and price volatility.

Moreover, the substantial capital investments required for research, development, and advanced manufacturing facilities pose a barrier to entry and can limit rapid expansion. The inherent volatility in raw material prices, influenced by global commodity markets and unexpected events, also introduces uncertainty for material suppliers and chip manufacturers alike. Navigating these restraints requires strategic foresight and collaborative efforts across the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Tensions and Trade Barriers | -1.0% | Global | Short to Mid-term (2025-2029) |

| High Capital Expenditure and R&D Costs | -0.7% | Global | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.5% | Global | Short-term (2025-2027) |

| Stringent Environmental Regulations and Sustainability Pressures | -0.3% | Developed Regions (Europe, North America) | Long-term (2028-2033) |

Semiconductor Material Market Opportunities Analysis

The semiconductor material market is rife with opportunities stemming from ongoing technological innovation and a global push for advanced manufacturing capabilities. The continuous evolution of semiconductor devices towards greater performance and efficiency necessitates the development and adoption of entirely new material solutions. This provides fertile ground for material science companies to innovate and capture new market segments.

Furthermore, the increasing focus on supply chain resilience and environmental sustainability presents significant avenues for growth. Efforts to localize material production and to implement circular economy principles offer distinct competitive advantages. Collaborations across the value chain, from material suppliers to chip manufacturers, will be crucial in unlocking these opportunities and driving the next wave of material innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Materials for Emerging Technologies (e.g., Quantum Computing, Neuromorphic Chips) | +1.3% | Global (R&D Hubs) | Long-term (2030-2033) |

| Increased Focus on Recycling and Circular Economy for Materials | +0.7% | Developed Regions | Mid to Long-term (2028-2033) |

| Localization and Diversification of Supply Chains | +0.8% | North America, Europe, India | Mid-term (2027-2031) |

| Collaboration Between Material Suppliers, Chip Manufacturers, and Research Institutions | +0.6% | Global | Mid to Long-term (2027-2033) |

Semiconductor Material Market Challenges Impact Analysis

Despite its dynamic growth, the semiconductor material market faces inherent challenges that can impede its progress and increase operational complexities. The highly intricate manufacturing processes involved in producing ultra-pure and specialized materials require meticulous control and substantial expertise. Any deviation can lead to significant production losses and quality issues, directly impacting supply.

Furthermore, the global nature of the industry means it is susceptible to intellectual property theft and talent shortages, particularly in highly specialized fields like material science. Addressing these challenges necessitates continuous investment in talent development, robust intellectual property protection strategies, and innovative waste management solutions to ensure sustainable and secure market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Talent Shortage in Material Science and Engineering | -0.8% | Global | Long-term (2025-2033) |

| Complex Manufacturing Processes and Stringent Quality Requirements | -0.6% | Global | Ongoing |

| Intellectual Property Disputes and Technological Espionage | -0.4% | Global | Ongoing |

| Managing Waste and Byproducts from Material Production | -0.3% | Global | Long-term (2028-2033) |

Semiconductor Material Market - Updated Report Scope

This report provides a comprehensive analysis of the Semiconductor Material Market, offering insights into its current size, historical performance, and future growth projections. It delves into the critical factors influencing market dynamics, including drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation by material type, application, and end-use industry, providing a granular view of market trends across key regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making in this vital industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 82.5 billion |

| Market Forecast in 2033 | USD 169.1 billion |

| Growth Rate | 9.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical, Sumco, Dow, DuPont, Merck KGaA, JSR Corporation, FUJIFILM Corporation, Hitachi Chemical Co. Ltd., Mitsui Chemicals, Air Liquide, The Linde Group, Entegris, BASF SE, Avantor, Solvay S.A., SHOWA DENKO K.K., Versum Materials, CMC Materials, SK Siltron, GlobalWafers Co., Ltd. |

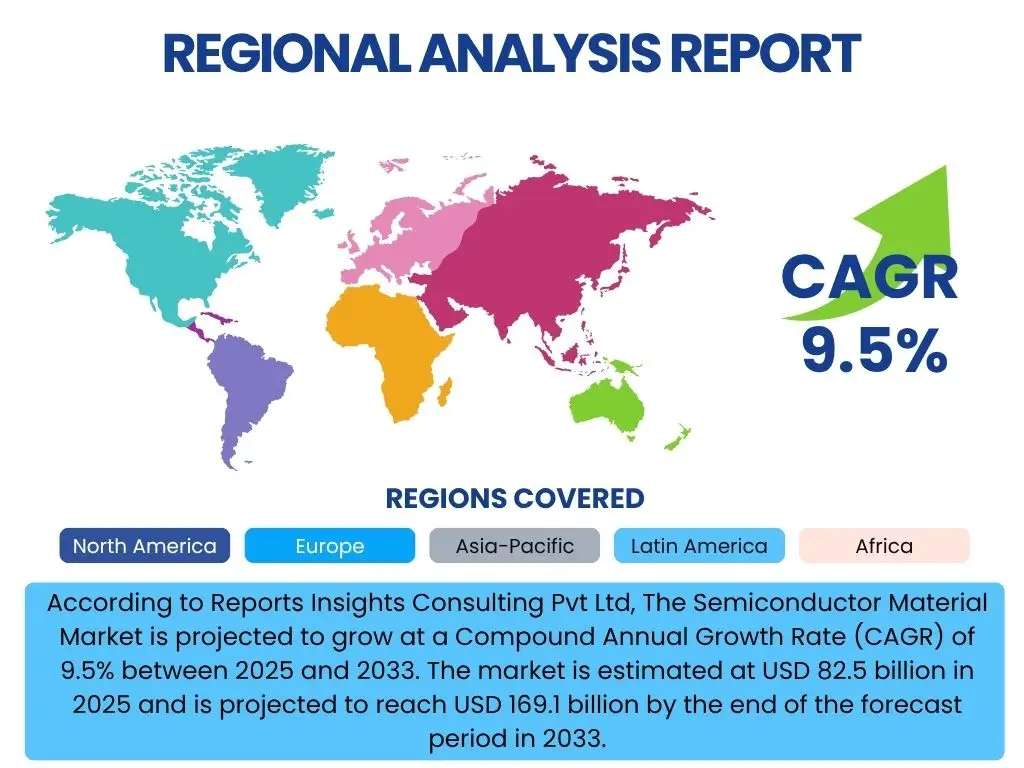

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor material market is extensively segmented to reflect the diverse range of materials required for modern chip manufacturing, the various stages of the fabrication process where these materials are used, and the broad spectrum of industries that rely on advanced semiconductors. This granular segmentation provides a detailed understanding of market dynamics, enabling stakeholders to identify specific growth areas and strategic opportunities within the complex semiconductor ecosystem.

Categorization by material type allows for an analysis of the demand trends for foundational elements like silicon wafers, as well as specialized inputs such as photoresists and process chemicals essential for lithography and etching. Application-based segmentation highlights the material needs of different players in the semiconductor value chain, including integrated device manufacturers and outsourced assembly and test providers. Furthermore, breaking down the market by end-use industry provides insights into how macro-level shifts in sectors like automotive or consumer electronics translate into specific material demands.

- By Material Type:

- Silicon Wafer

- Photoresist & Ancillaries

- Process Chemicals

- CMP Slurry

- Sputtering Targets

- Electronic Gases

- Others (e.g., Advanced Ceramics, Packaging Materials)

- By Application:

- Foundries

- IDMs (Integrated Device Manufacturers)

- OSATs (Outsourced Semiconductor Assembly and Test)

- Others (e.g., R&D, Equipment Manufacturers)

- By End-use Industry:

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- IT & Telecom

- Defense & Aerospace

Regional Highlights

- Asia Pacific (APAC): Dominates the semiconductor material market due to the concentration of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. The region benefits from significant investments in new fabrication facilities and advanced packaging capabilities, driving a high volume and diversity of material consumption. It is expected to continue leading in growth due to ongoing government support and a robust electronics ecosystem.

- North America: A significant market driven by strong research and development activities, particularly in cutting-edge technologies like AI, HPC, and advanced logic. The region is seeing renewed investment in domestic fab expansion and material production as part of strategic initiatives to enhance supply chain resilience, focusing on high-value, specialized materials.

- Europe: Characterized by a strong presence in automotive electronics, industrial applications, and power semiconductors. Europe is increasingly investing in localized material production and emphasizing sustainable manufacturing processes. The region's focus on GaN and SiC materials for electric vehicles and renewable energy applications presents unique growth opportunities.

- Latin America: An emerging market for semiconductor materials, primarily driven by growing electronics manufacturing and assembly operations, particularly in countries like Mexico and Brazil. While smaller in comparison to other regions, it represents a developing market with potential for increased material demand as local industries mature.

- Middle East and Africa (MEA): Currently a nascent market for semiconductor materials, but with long-term potential. Investments in digitalization, infrastructure development, and nascent technology hubs in certain countries could foster growth in electronics manufacturing and, consequently, demand for semiconductor materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Material Market.- Shin-Etsu Chemical

- Sumco Corporation

- Dow Inc.

- DuPont de Nemours, Inc.

- Merck KGaA

- JSR Corporation

- FUJIFILM Corporation

- Hitachi Chemical Co. Ltd. (now Showa Denko Materials)

- Mitsui Chemicals, Inc.

- Air Liquide S.A.

- The Linde Group

- Entegris, Inc.

- BASF SE

- Avantor, Inc.

- Solvay S.A.

- SHOWA DENKO K.K.

- SK Siltron Inc.

- GlobalWafers Co., Ltd.

- CMC Materials (now part of Entegris)

- Tokyo Ohka Kogyo Co., Ltd.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary types of materials used in semiconductor manufacturing?

The primary materials include silicon wafers (the foundational substrate), photoresists and their ancillaries (for lithography), process chemicals (for etching, cleaning), CMP slurries (for planarization), sputtering targets (for thin-film deposition), and electronic gases (for deposition and etching processes). Advanced packaging also utilizes specialized polymers and metals.

How does the growth of AI and 5G influence the semiconductor material market?

The expansion of AI and 5G significantly drives demand for advanced semiconductor materials by requiring higher performance, greater power efficiency, and increased integration in chips. This necessitates ultra-pure silicon, novel materials for thermal management, and sophisticated packaging materials to support complex architectures and high data throughput.

What are the main challenges faced by the semiconductor material market?

Key challenges include geopolitical tensions impacting supply chains, the high capital expenditure required for R&D and manufacturing, volatility in raw material prices, stringent environmental regulations, and a persistent talent shortage in specialized material science and engineering fields.

Which region dominates the semiconductor material market, and what are its key drivers?

The Asia Pacific (APAC) region currently dominates the semiconductor material market. This is primarily driven by the concentration of major semiconductor manufacturing facilities (fabs) in countries like Taiwan, South Korea, China, and Japan, coupled with continuous investments in expanding production capacities and advancing technological capabilities.

What innovations are expected in semiconductor materials over the next decade?

Over the next decade, innovations are expected in materials for advanced logic (e.g., GAAFETs), novel substrates beyond silicon (e.g., GaN, SiC for power/RF), and materials for heterogeneous integration and advanced packaging. There will also be a strong focus on sustainable materials, recycling technologies, and AI-driven material discovery to enhance performance and environmental footprint.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted