3D Printing Polymer Market

3D Printing Polymer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705477 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

3D Printing Polymer Market Size

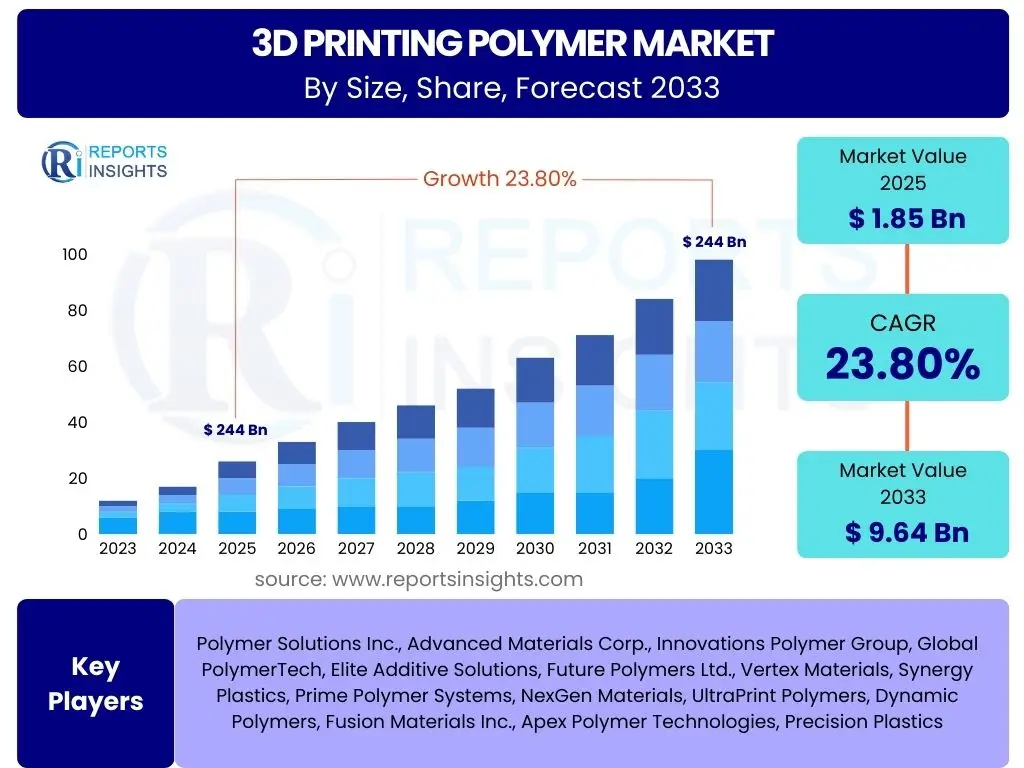

According to Reports Insights Consulting Pvt Ltd, The 3D Printing Polymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 9.64 Billion by the end of the forecast period in 2033.

Key 3D Printing Polymer Market Trends & Insights

The 3D Printing Polymer market is experiencing rapid evolution driven by advancements in material science, additive manufacturing technologies, and growing industrial applications. Key user questions frequently revolve around the emergence of novel polymer formulations, the integration of smart materials, and the increasing focus on sustainable solutions. Users are also keen to understand how customization demands across various sectors, such as healthcare and automotive, are shaping material development and adoption. Furthermore, the trend towards high-performance polymers capable of withstanding extreme conditions is a significant area of interest, reflecting the market's maturation beyond prototyping to end-use parts production.

Another major trend attracting user attention is the democratization of 3D printing technology, making it more accessible to small and medium-sized enterprises (SMEs) and even prosumers. This accessibility is driving demand for user-friendly and versatile polymer options. The convergence of hardware, software, and material innovation is fostering an ecosystem where custom material development is becoming more streamlined. This allows for tailoring polymer properties to specific application requirements, from flexible elastomers for wearables to rigid, heat-resistant polymers for industrial tooling. The growing emphasis on supply chain resilience and localized manufacturing is also propelling the adoption of 3D printing, with polymers playing a crucial role in enabling on-demand production and reducing lead times.

- Development of high-performance and specialized polymer materials.

- Increasing adoption of sustainable and bio-based polymers.

- Expansion of 3D printing into mass production and end-use part manufacturing.

- Rising demand for custom and personalized products across industries.

- Integration of smart and multi-functional polymers.

- Advancements in composite polymer materials for enhanced strength and durability.

- Growth of distributed manufacturing models leveraging localized production.

AI Impact Analysis on 3D Printing Polymer

User inquiries concerning the impact of Artificial Intelligence (AI) on 3D printing polymers often center on its potential to revolutionize material discovery, optimization, and process control. Many users seek to understand how AI algorithms can accelerate the development of new polymer formulations with desired properties, predicting material performance and identifying optimal compositions. There is significant interest in AI's role in streamlining the design-to-print workflow, from generative design of polymer structures to real-time monitoring and adaptive control of the printing process itself. Users are looking for solutions that reduce trial-and-error, minimize waste, and enhance the predictability and quality of printed polymer parts, all of which AI promises to address.

Furthermore, users frequently question AI's capacity to optimize print parameters for specific polymer types, addressing challenges such as warping, shrinkage, and layer adhesion. AI-driven predictive maintenance for 3D printers and material handling systems is another area of inquiry, aiming to improve operational efficiency and reduce downtime. The integration of AI with machine vision systems for quality assurance and defect detection in polymer prints is also a topic of high relevance, ensuring consistency and reliability in manufacturing. Overall, the expectation is that AI will unlock new levels of precision, speed, and material innovation within the 3D printing polymer ecosystem, pushing the boundaries of what is currently achievable.

- AI-driven material discovery and property prediction for novel polymers.

- Optimization of print parameters and process control through machine learning.

- Generative design of complex polymer structures and lattice geometries.

- Real-time quality control and defect detection using AI and computer vision.

- Predictive maintenance for 3D printers and material management systems.

- Enhanced supply chain optimization and inventory management for polymer materials.

Key Takeaways 3D Printing Polymer Market Size & Forecast

Common user questions regarding key takeaways from the 3D Printing Polymer market size and forecast consistently highlight the significant growth trajectory and the underlying drivers of this expansion. Users want to understand where the most substantial growth opportunities lie, whether in specific polymer types, applications, or geographic regions. The rapid increase in market valuation from 2025 to 2033 indicates a maturing industry moving beyond niche applications to become a more integral part of global manufacturing. This growth is heavily influenced by sustained innovation in materials science, which continues to unlock new possibilities for end-use parts and functional prototypes.

Another crucial takeaway is the increasing diversification of polymer applications, extending beyond traditional sectors like automotive and aerospace into burgeoning areas such as healthcare, consumer goods, and construction. The forecast underscores the rising demand for customized solutions and on-demand manufacturing, which 3D printing polymers are uniquely positioned to fulfill. Despite potential challenges, the market's robust projected CAGR suggests strong industry confidence and a continuous influx of investment into research and development, aiming to overcome existing limitations and broaden the scope of polymer additive manufacturing. The shift towards sustainable and high-performance materials is also a defining characteristic, shaping the market's future direction and attracting both industrial and environmental stakeholders.

- Significant market expansion with a strong double-digit CAGR.

- Healthcare and industrial sectors are primary growth drivers for polymer demand.

- Continued innovation in polymer material properties is crucial for market advancement.

- Increasing shift from prototyping to functional end-use parts production.

- Asia Pacific is expected to exhibit the highest growth rate due to expanding manufacturing bases.

3D Printing Polymer Market Drivers Analysis

The 3D Printing Polymer market is significantly driven by the increasing adoption of additive manufacturing across various industrial sectors. This surge is fueled by the inherent benefits of 3D printing, such as design flexibility, rapid prototyping capabilities, and the ability to produce complex geometries that are otherwise challenging or impossible with traditional manufacturing methods. Industries like automotive, aerospace, healthcare, and consumer goods are increasingly leveraging 3D printing for both prototyping and end-use part production, which directly escalates the demand for diverse and specialized polymer materials. Furthermore, the continuous reduction in the cost of 3D printers and materials, coupled with improved print quality and speed, makes additive manufacturing a more viable and attractive option for a broader range of applications and businesses, including small and medium-sized enterprises (SMEs).

Another major driver is the ongoing innovation in polymer material science. Researchers and manufacturers are consistently developing new types of polymers with enhanced properties, such as increased strength, heat resistance, flexibility, biocompatibility, and sustainability. This expansion of the material portfolio enables 3D printing to meet the stringent requirements of high-performance applications, pushing its boundaries beyond mere aesthetics or non-functional prototypes. The growing demand for customized products, particularly in the medical and dental fields for prosthetics, implants, and surgical guides, also heavily influences the market, as polymers can be precisely tailored to individual patient needs. The increasing focus on localized and on-demand manufacturing, driven by supply chain disruptions and a desire for greater agility, further boosts the adoption of 3D printing polymers as a versatile solution for agile production.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption in End-Use Industries | +5.2% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Advancements in Polymer Material Science | +4.8% | Global, especially developed economies | Mid to Long-term (2027-2033) |

| Growing Demand for Customized Products | +4.5% | Healthcare (North America, Europe), Consumer Goods (Global) | Short to Mid-term (2025-2030) |

| Reduced Cost of 3D Printing Technology | +3.9% | Emerging economies, SMEs (Global) | Short to Mid-term (2025-2028) |

| Focus on Localized and On-Demand Manufacturing | +3.4% | Global, particularly post-pandemic supply chain adjustments | Mid-term (2026-2031) |

3D Printing Polymer Market Restraints Analysis

Despite its significant growth potential, the 3D Printing Polymer market faces several restraints that could impede its accelerated expansion. One primary concern is the relatively high cost of certain specialized polymer materials, especially those designed for high-performance or specific industrial applications. While printer costs have decreased, the per-unit cost of advanced polymer filaments, resins, and powders can still be prohibitive for mass production compared to traditional manufacturing materials. This economic barrier limits widespread adoption, particularly in cost-sensitive industries or for large-volume production runs. Additionally, the limited availability of certain engineering-grade polymers with specific properties, such as extreme heat resistance or high mechanical strength comparable to traditional metals, presents a challenge for expanding into highly demanding applications.

Another significant restraint involves the technical complexities and post-processing requirements often associated with 3D printed polymer parts. Achieving desired surface finish, dimensional accuracy, and mechanical properties frequently necessitates extensive post-processing steps like curing, sanding, or chemical treatments, which add to the overall production time and cost. The lack of standardized testing protocols and certifications for 3D printed polymer components also creates uncertainty for end-users, especially in regulated industries like aerospace and medical, where material reliability and consistent performance are paramount. Furthermore, intellectual property concerns related to digital designs and the ease of replication can deter manufacturers from fully embracing additive manufacturing for sensitive components, impacting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Material and Production Costs for Mass Production | -2.8% | Global, especially for large-scale industrial adoption | Short to Mid-term (2025-2029) |

| Limited Material Portfolio for High-Performance Applications | -2.5% | Global, specific industrial sectors (Aerospace, Automotive) | Mid-term (2026-2031) |

| Complexities of Post-Processing | -2.1% | Global, impacts production efficiency | Short to Mid-term (2025-2028) |

| Lack of Standardization and Certification | -1.8% | Global, particularly regulated industries | Mid to Long-term (2027-2033) |

| Intellectual Property and Data Security Concerns | -1.5% | Global, affects sensitive component manufacturing | Short to Mid-term (2025-2030) |

3D Printing Polymer Market Opportunities Analysis

The 3D Printing Polymer market presents numerous growth opportunities stemming from evolving technological capabilities and expanding application landscapes. One significant opportunity lies in the burgeoning healthcare sector, particularly for customized medical devices, prosthetics, and anatomical models. The ability of 3D printing to create patient-specific solutions with complex geometries and biocompatible polymers offers a substantial advantage over traditional methods, leading to improved patient outcomes and reduced surgical times. Furthermore, the pharmaceutical industry is exploring 3D printing for personalized drug delivery systems, presenting a niche but high-growth area for specialized polymer formulations. The continued development of bioprinting technologies, utilizing advanced polymers to create tissues and organs, represents a long-term, transformative opportunity.

Another compelling opportunity resides in the automotive and aerospace industries, where the demand for lightweight, high-strength, and durable components is constant. 3D printed polymers can replace traditional metal parts in certain applications, leading to significant weight reductions and improved fuel efficiency. The ability to consolidate multiple parts into a single, complex 3D printed component also streamlines assembly processes and reduces manufacturing complexity. The growing emphasis on sustainable manufacturing practices creates opportunities for the development and adoption of bio-based, recycled, and recyclable polymers, aligning with global environmental objectives and attracting environmentally conscious consumers and businesses. The emergence of multi-material 3D printing also offers new avenues for innovation, allowing the creation of parts with varying properties within a single print, opening doors for advanced functional prototypes and end-use components in electronics and consumer goods.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Healthcare and Medical Devices | +6.0% | North America, Europe, rapidly growing in Asia Pacific | Short to Long-term (2025-2033) |

| Development of Sustainable and Bio-based Polymers | +5.5% | Global, driven by regulatory and consumer demand | Mid to Long-term (2027-2033) |

| Increasing Use in Automotive and Aerospace for Lightweighting | +4.9% | Europe, North America, Japan, China | Short to Mid-term (2025-2030) |

| Advancements in Multi-Material 3D Printing | +4.2% | Global, academic and industrial R&D hubs | Mid-term (2026-2032) |

| Emergence of New Applications in Consumer Goods and Electronics | +3.8% | Asia Pacific, North America, Europe | Short to Mid-term (2025-2029) |

3D Printing Polymer Market Challenges Impact Analysis

The 3D Printing Polymer market faces several challenges that require innovative solutions for sustained growth. One significant challenge is scalability, particularly for large-volume industrial production. While 3D printing excels at customization and rapid prototyping, achieving economic viability for mass manufacturing of polymer parts remains an obstacle due to slower production speeds compared to injection molding or other traditional methods. This limits its competitive edge in applications requiring millions of units, forcing manufacturers to balance the benefits of customization against the higher per-part cost and longer production times. Additionally, the consistency and reproducibility of parts, especially when scaling up, can be difficult to maintain, leading to quality control issues that need robust monitoring systems and advanced process optimization.

Another major challenge revolves around material property limitations and the inherent anisotropic nature of 3D printed polymer parts. While polymer science is advancing, some 3D printed polymers may not yet achieve the mechanical properties, surface finish, or long-term durability required for all high-stress or demanding end-use applications, particularly when compared to traditionally manufactured counterparts. The layer-by-layer deposition process can also introduce weaknesses along build lines, affecting part strength and structural integrity. Furthermore, managing the complexity of diverse polymer types and their specific processing requirements, including optimal printing temperatures, support removal, and post-curing, poses an ongoing technical challenge for operators and system developers. Regulatory hurdles and environmental concerns associated with certain polymer waste streams also present a compliance challenge for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability for Mass Production | -3.2% | Global, affects industrial adoption | Short to Mid-term (2025-2029) |

| Material Property Limitations and Anisotropy | -2.9% | Global, high-performance applications | Mid to Long-term (2027-2033) |

| Complex Post-Processing Requirements | -2.3% | Global, impacts production efficiency | Short to Mid-term (2025-2028) |

| Regulatory Frameworks and Environmental Compliance | -1.7% | Europe, North America, specific industries | Mid-term (2026-2032) |

| Data Management and Cybersecurity for Digital Designs | -1.4% | Global, affects sensitive intellectual property | Short to Mid-term (2025-2030) |

3D Printing Polymer Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global 3D Printing Polymer Market, covering historical data, current market dynamics, and future projections. It segments the market by polymer type, form, application, and end-use industry, offering granular insights into growth drivers, restraints, opportunities, and challenges. The report also includes a detailed regional analysis and profiles of key market players, helping stakeholders understand market competitive landscape and strategic positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 9.64 Billion |

| Growth Rate | 23.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Polymer Solutions Inc., Advanced Materials Corp., Innovations Polymer Group, Global PolymerTech, Elite Additive Solutions, Future Polymers Ltd., Vertex Materials, Synergy Plastics, Prime Polymer Systems, NexGen Materials, UltraPrint Polymers, Dynamic Polymers, Fusion Materials Inc., Apex Polymer Technologies, Precision Plastics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 3D Printing Polymer market is meticulously segmented to provide a granular view of its diverse landscape and growth opportunities. These segments are primarily defined by the chemical composition and physical form of the polymers, as well as their end applications and the industries they serve. Understanding these segmentations is critical for stakeholders to identify niche markets, tailor product development, and formulate targeted business strategies, aligning with specific market demands and technological capabilities. The continuous innovation within each segment, from novel material development to specialized application techniques, drives the overall market expansion.

The segmentation by polymer type distinguishes between thermoplastics, thermosets, and elastomers, each offering distinct properties suitable for varied applications. Thermoplastics like ABS, PLA, and Nylon are widely used due to their versatility and ease of processing, while high-performance options like PEEK cater to demanding industrial needs. Thermosets, including epoxies and photopolymers, are crucial for applications requiring high stiffness and thermal stability, often found in resin-based printing. Elastomers, such as TPU, provide flexibility and elasticity for consumer goods and medical devices. Furthermore, the segmentation by form (filament, resin, powder) reflects the different 3D printing technologies and their material inputs, highlighting the preferences and technical requirements of various users and industrial processes. The application and end-use industry segments further refine the market analysis, showcasing how these advanced polymers are transforming sectors from healthcare to aerospace, enabling customization, rapid prototyping, and the production of complex, functional parts.

- By Type: Thermoplastics, Thermosets, Elastomers.

- By Form: Filament, Resin, Powder, Pellets.

- By Application: Prototyping, Tooling, Functional Parts, Personalization, Visualisation.

- By End-Use Industry: Healthcare & Medical, Automotive, Aerospace & Defense, Consumer Goods & Electronics, Industrial, Construction & Architecture, Education & Research, Others.

Regional Highlights

- North America: Expected to hold a significant market share due to substantial investments in research and development, early adoption of advanced manufacturing technologies, and a robust presence of key industry players in the automotive, aerospace, and healthcare sectors. The region benefits from a strong innovation ecosystem and high demand for customized solutions.

- Europe: A prominent region in the 3D printing polymer market, driven by stringent regulatory standards for product quality, a strong focus on sustainable manufacturing, and significant government funding for additive manufacturing initiatives. Countries like Germany and France are leaders in industrial and automotive applications, fostering demand for high-performance polymers.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by rapid industrialization, expanding manufacturing bases, and increasing foreign direct investments in countries like China, India, Japan, and South Korea. The growing electronics and consumer goods industries, coupled with rising adoption in healthcare, are key contributors to market expansion.

- Latin America: Showing nascent growth, primarily driven by increasing awareness and initial adoption of 3D printing technologies in automotive and medical sectors. Economic development and infrastructure improvements are gradually opening up new opportunities for polymer demand.

- Middle East and Africa (MEA): Expected to witness steady growth, particularly in the oil and gas, construction, and healthcare sectors. Government initiatives to diversify economies and invest in technological advancements are contributing to the emerging demand for 3D printing polymers in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 3D Printing Polymer Market.- Polymer Solutions Inc.

- Advanced Materials Corp.

- Innovations Polymer Group

- Global PolymerTech

- Elite Additive Solutions

- Future Polymers Ltd.

- Vertex Materials

- Synergy Plastics

- Prime Polymer Systems

- NexGen Materials

- UltraPrint Polymers

- Dynamic Polymers

- Fusion Materials Inc.

- Apex Polymer Technologies

- Precision Plastics

Frequently Asked Questions

What are the primary types of polymers used in 3D printing?

The primary types of polymers used in 3D printing include thermoplastics (such as ABS, PLA, Nylon, PEEK), thermosets (like epoxy resins, photopolymers), and elastomers (such as TPU and TPE). Each type offers distinct mechanical properties and is suitable for various 3D printing technologies and applications.

Which industries are driving the demand for 3D printing polymers?

The demand for 3D printing polymers is primarily driven by the healthcare and medical sector, automotive industry, aerospace and defense, and consumer goods. These industries leverage 3D printing for rapid prototyping, customized parts, lightweight components, and complex functional designs.

What are the key advantages of using polymers in 3D printing?

Key advantages include design flexibility, the ability to produce highly complex and customized geometries, lightweighting of parts, rapid prototyping capabilities, and reduced material waste compared to traditional manufacturing. Polymers also offer diverse material properties from flexible to rigid, and biocompatible options.

What challenges does the 3D printing polymer market face?

Challenges include the relatively high cost of specialized polymers for mass production, limitations in material properties for high-stress applications, complexities of post-processing, and a current lack of universal standardization and certification for printed polymer parts.

How is sustainability impacting the 3D printing polymer market?

Sustainability is increasingly impacting the market by driving the development and adoption of bio-based, recycled, and recyclable polymers. This trend addresses environmental concerns, reduces carbon footprint, and aligns with growing consumer and regulatory demands for eco-friendly manufacturing solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted