Semiconductor Fabrication Chemical Market

Semiconductor Fabrication Chemical Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710156 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

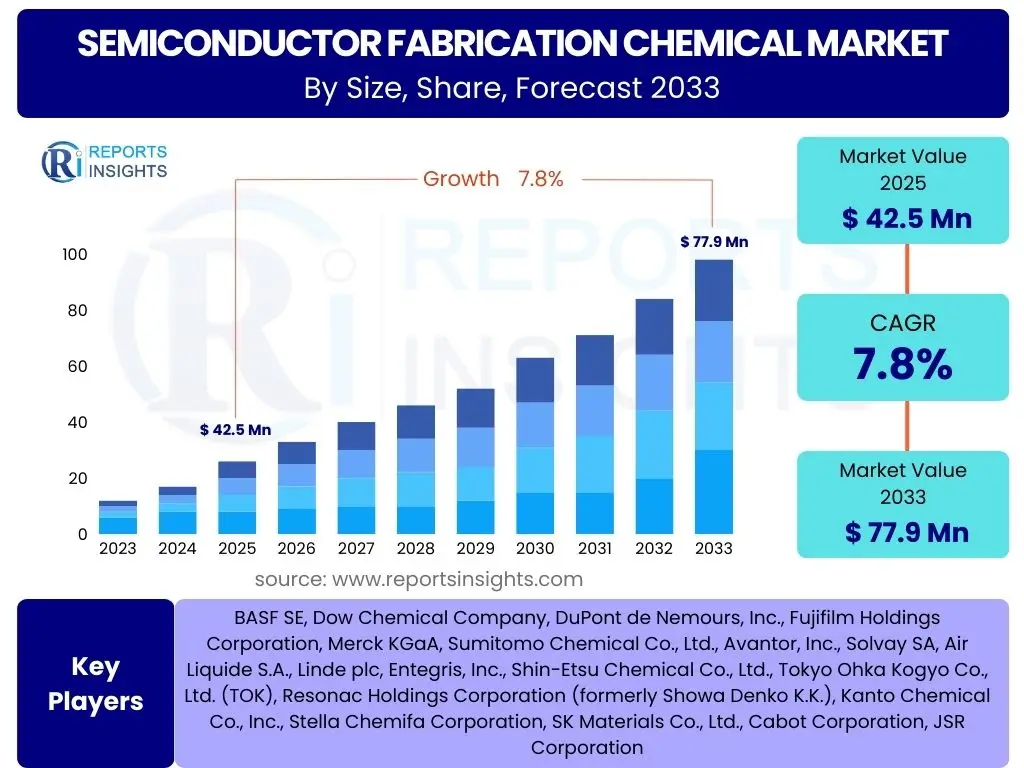

Semiconductor Fabrication Chemical Market Size

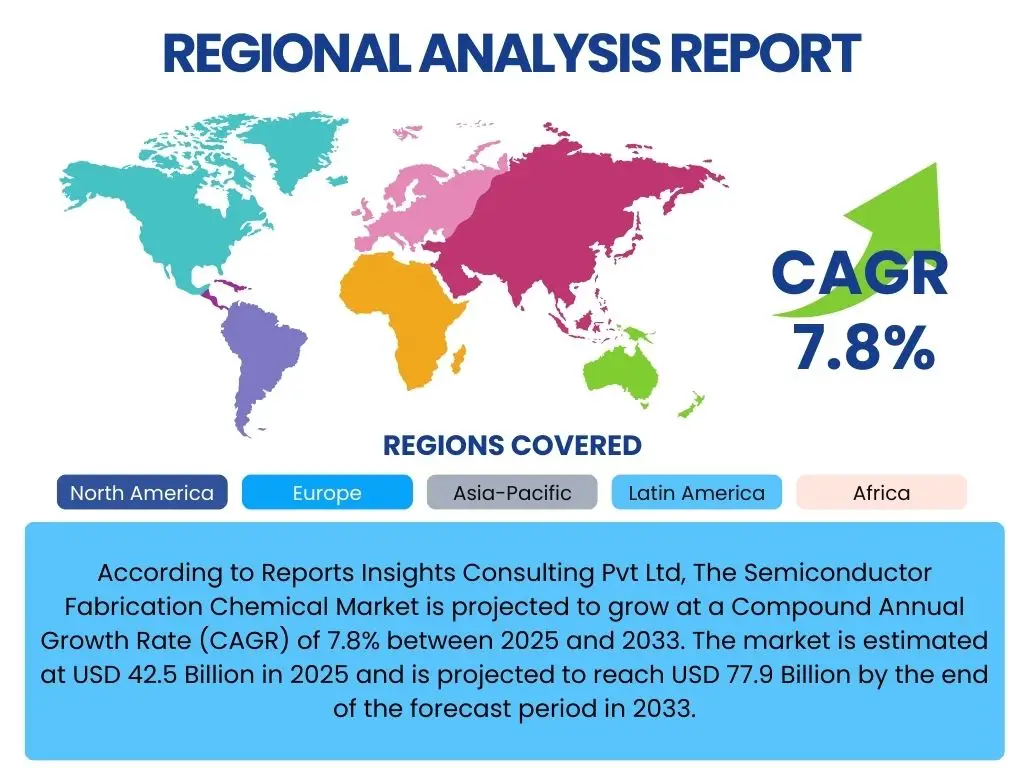

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Fabrication Chemical Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 42.5 Billion in 2025 and is projected to reach USD 77.9 Billion by the end of the forecast period in 2033.

Key Semiconductor Fabrication Chemical Market Trends & Insights

User inquiries frequently highlight several transformative trends shaping the Semiconductor Fabrication Chemical market. A primary focus is on the continuous drive towards miniaturization and higher performance in electronic devices, which necessitates increasingly sophisticated and pure chemical formulations for advanced manufacturing processes. The emergence of new semiconductor materials, such as those used in compound semiconductors and 3D stacking technologies, also represents a significant area of interest, demanding novel chemical solutions for etching, deposition, and cleaning. Furthermore, there is growing attention on sustainable manufacturing practices, driven by environmental regulations and corporate social responsibility, prompting innovation in greener chemicals and recycling processes within the fabrication industry. Geopolitical factors influencing supply chain resilience and regional manufacturing capabilities also frequently surface as critical market considerations.

- Continued miniaturization and increasing complexity of semiconductor devices.

- Rapid advancements in advanced packaging technologies, including 3D ICs and System-in-Package (SiP).

- Growing adoption of Artificial Intelligence (AI) and Machine Learning (ML) for process optimization and material discovery.

- Strong focus on sustainable and eco-friendly chemical solutions and manufacturing processes.

- Increasing demand for ultra-high purity chemicals to reduce defects in advanced nodes.

- Geopolitical shifts influencing regional semiconductor manufacturing capacity expansion and supply chain diversification.

- Development of novel materials for next-generation semiconductors, such as GaN and SiC.

AI Impact Analysis on Semiconductor Fabrication Chemical

Common user questions regarding AI's impact on the Semiconductor Fabrication Chemical sector revolve around its potential to revolutionize efficiency, quality control, and innovation. Many stakeholders are interested in how AI can optimize complex chemical processes, predict material performance, and enhance the precision of fabrication steps. There is significant anticipation for AI-driven improvements in supply chain management, enabling better forecasting of chemical demand, managing inventory more effectively, and mitigating supply disruptions. Furthermore, questions frequently arise about AI's role in accelerating research and development for new chemical formulations, particularly in identifying optimal compositions and processing parameters, thereby reducing time-to-market for advanced materials. Users also express interest in AI's capacity to detect anomalies and predict equipment failures, which could significantly improve operational uptime and reduce waste in chemical usage.

- AI-driven optimization of chemical process parameters, enhancing yield and reducing waste.

- Predictive maintenance for chemical delivery systems and fabrication equipment, ensuring consistent supply and quality.

- Accelerated discovery and development of new chemical formulations and materials through AI-powered simulations and data analysis.

- Enhanced quality control and defect detection in semiconductor manufacturing using AI for real-time monitoring.

- Improved supply chain management and demand forecasting for fabrication chemicals, increasing resilience and efficiency.

- Automation of laboratory testing and data analysis for chemical characterization and performance evaluation.

- Personalized chemical recipes and process flows tailored by AI for specific device architectures and materials.

Key Takeaways Semiconductor Fabrication Chemical Market Size & Forecast

Analysis of common user questions concerning the Semiconductor Fabrication Chemical market size and forecast reveals a strong interest in understanding the core drivers of growth, the resilience of the market against economic fluctuations, and the long-term sustainability of demand. Users frequently seek clarity on the primary technological advancements fueling market expansion, such as advanced lithography and 3D stacking, and how these translate into increased chemical consumption. There is also significant emphasis on identifying key geographical regions that will dominate market growth, particularly Asia Pacific due to its robust semiconductor manufacturing ecosystem. Stakeholders are keen to grasp the strategic implications of these trends for investment decisions, supply chain planning, and competitive positioning within the evolving semiconductor landscape, aiming to leverage the anticipated growth in high-purity and specialized chemical segments.

- The market exhibits robust growth driven by sustained demand for advanced electronics.

- Technological advancements in chip architecture necessitate increasingly specialized and pure chemicals.

- Asia Pacific remains the dominant and fastest-growing region due to significant foundry investments.

- Sustainability and supply chain resilience are becoming critical factors influencing market strategies.

- AI and automation are poised to optimize chemical usage and accelerate material innovation.

Semiconductor Fabrication Chemical Market Drivers Analysis

The Semiconductor Fabrication Chemical market is propelled by a confluence of factors stemming from the escalating global demand for advanced electronic devices and the continuous technological evolution within the semiconductor industry. The pervasive integration of semiconductors into virtually every aspect of modern life, from consumer electronics to automotive, industrial, and telecommunications sectors, creates an inherent and expanding need for the foundational chemicals required in their manufacturing. Furthermore, the relentless pursuit of smaller, faster, and more powerful chips necessitates increasingly complex and precise fabrication processes, which in turn demands a broader array of ultra-high purity and specialized chemicals. Investments in next-generation manufacturing facilities, particularly in response to geopolitical considerations around supply chain security, also significantly bolster the demand for these crucial materials, fostering innovation and market expansion across various chemical segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Advanced Electronics | +2.5% | Global, particularly Asia Pacific (China, Taiwan, South Korea) | Long-term (2025-2033) |

| Technological Advancements in Semiconductor Manufacturing (e.g., advanced lithography, 3D stacking) | +2.0% | Global, especially North America, Asia Pacific (Japan, Taiwan) | Mid to Long-term (2025-2033) |

| Expansion of Semiconductor Manufacturing Capacities and New Fabs | +1.8% | Asia Pacific, North America, Europe | Mid-term (2025-2030) |

| Increased Adoption of AI, IoT, and 5G Technologies | +1.5% | Global | Long-term (2025-2033) |

| Demand for Ultra-High Purity Chemicals to Reduce Defects | +1.0% | Global | Long-term (2025-2033) |

Semiconductor Fabrication Chemical Market Restraints Analysis

Despite its robust growth trajectory, the Semiconductor Fabrication Chemical market faces several significant restraints that could impact its expansion and stability. A primary concern is the escalating cost associated with producing ultra-high purity chemicals, which require advanced manufacturing techniques and stringent quality control, leading to high capital expenditure for chemical manufacturers. Furthermore, the semiconductor industry's stringent environmental regulations and the increasing focus on sustainability exert pressure on chemical suppliers to develop greener, less toxic, and more recyclable alternatives, often involving substantial research and development costs and compliance burdens. Geopolitical tensions and trade disputes also pose a considerable restraint by disrupting global supply chains for critical raw materials and finished chemicals, leading to price volatility and potential shortages. The inherent complexity of chemical interactions in advanced fabrication processes, requiring continuous innovation and significant R&D investment, also presents a barrier to entry and a challenge for sustained profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and R&D Costs for Ultra-High Purity Chemicals | -1.2% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations and Disposal Challenges | -1.0% | Europe, North America, East Asia | Long-term (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Trade Tensions | -0.8% | Global | Mid-term (2025-2030) |

| Fluctuations in Raw Material Prices and Availability | -0.7% | Global | Short to Mid-term (2025-2028) |

Semiconductor Fabrication Chemical Market Opportunities Analysis

The Semiconductor Fabrication Chemical market is ripe with opportunities driven by a paradigm shift towards advanced manufacturing, sustainability, and technological convergence. A significant opportunity lies in the development and commercialization of next-generation chemicals specifically tailored for emerging semiconductor technologies, such as advanced logic nodes below 5nm, novel memory architectures, and compound semiconductors like SiC and GaN, which are crucial for electric vehicles and 5G infrastructure. Furthermore, the increasing global emphasis on environmental stewardship opens avenues for innovative "green chemistry" solutions, including safer solvents, bio-based photoresists, and advanced recycling technologies for spent chemicals, presenting both ecological and economic advantages. The expansion of semiconductor manufacturing into new geographic regions, particularly in Southeast Asia, India, and parts of Europe, also creates fresh demand for localized chemical supply chains and specialized services. Collaborative efforts between chemical suppliers, equipment manufacturers, and chipmakers to co-develop integrated material and process solutions represent another crucial area for market growth and competitive differentiation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Chemicals for Advanced Nodes (e.g., EUV lithography, 3D NAND) | +1.5% | Global | Long-term (2025-2033) |

| Growing Demand for Green and Sustainable Chemical Solutions | +1.2% | Europe, North America, East Asia | Mid to Long-term (2025-2033) |

| Expansion into Emerging Semiconductor Manufacturing Regions | +1.0% | Southeast Asia, India, Europe (e.g., Germany) | Mid-term (2025-2030) |

| Strategic Partnerships and Collaborations with Chip Manufacturers | +0.8% | Global | Long-term (2025-2033) |

Semiconductor Fabrication Chemical Market Challenges Impact Analysis

The Semiconductor Fabrication Chemical market navigates a landscape rife with complex technical and operational challenges that can impede progress and profitability. A significant hurdle is the escalating technological complexity inherent in producing chemicals for advanced semiconductor processes, where even minute impurities or inconsistencies can lead to critical defects and yield losses. This demands continuous investment in sophisticated analytical techniques and ultra-clean manufacturing environments, driving up operational costs. Furthermore, rapid technological obsolescence in the semiconductor industry means that chemical formulations must constantly evolve, requiring chemical suppliers to engage in continuous, high-stakes research and development cycles with uncertain returns. The intense competition within the market, coupled with the capital-intensive nature of chemical manufacturing and the need for global distribution, creates formidable barriers to entry and sustained profitability. Moreover, managing the environmental and health impacts of specialized chemicals, including their safe handling, transportation, and disposal, represents a persistent regulatory and logistical challenge for all market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Technological Complexity and Purity Requirements | -1.5% | Global | Long-term (2025-2033) |

| Rapid Technological Obsolescence in Semiconductor Industry | -1.0% | Global | Mid to Long-term (2025-2033) |

| Intense Competition and Pricing Pressures | -0.9% | Global | Long-term (2025-2033) |

| Managing Environmental, Health, and Safety (EHS) Risks | -0.7% | Global | Long-term (2025-2033) |

Semiconductor Fabrication Chemical Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Semiconductor Fabrication Chemical market, offering detailed insights into its current landscape, historical performance, and future growth projections. The scope encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges influencing the industry. It further delves into extensive market segmentation by various product types, applications, end-use industries, and wafer sizes, delivering a granular view of market trends. A significant portion of the report is dedicated to a regional analysis, highlighting growth hotspots and market contributions from key geographical areas, alongside an exhaustive competitive landscape assessment, profiling major industry players and their strategic initiatives. The report aims to furnish stakeholders with actionable intelligence for informed decision-making, strategic planning, and identifying lucrative investment avenues within the evolving semiconductor chemical ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2033 | USD 77.9 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Dow Chemical Company, DuPont de Nemours, Inc., Fujifilm Holdings Corporation, Merck KGaA, Sumitomo Chemical Co., Ltd., Avantor, Inc., Solvay SA, Air Liquide S.A., Linde plc, Entegris, Inc., Shin-Etsu Chemical Co., Ltd., Tokyo Ohka Kogyo Co., Ltd. (TOK), Resonac Holdings Corporation (formerly Showa Denko K.K.), Kanto Chemical Co., Inc., Stella Chemifa Corporation, SK Materials Co., Ltd., Cabot Corporation, JSR Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Fabrication Chemical market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. This segmentation allows for precise analysis of market dynamics across various product types, applications in the fabrication process, end-use industries, and wafer sizes. Each segment represents distinct market characteristics driven by specific technological requirements, purity standards, and operational considerations within the semiconductor manufacturing ecosystem. Understanding these detailed segmentations is crucial for identifying key growth areas, assessing competitive intensity, and formulating targeted strategies to capitalize on the unique opportunities present in different parts of the chemical supply chain for semiconductor fabrication.

- By Product Type: This segment categorizes chemicals based on their composition and primary function.

- Wet Chemicals: Includes high-volume chemicals like Sulfuric Acid, Hydrogen Peroxide, Ammonium Hydroxide, Hydrofluoric Acid, Phosphoric Acid, Nitric Acid, and Isopropyl Alcohol, primarily used in cleaning and etching.

- Photoresists & Ancillaries: Essential for lithography, comprising Positive Photoresists, Negative Photoresists, Photoresist Developers, Photoresist Strippers, and Etchants.

- CMP Slurries: Critical for planarization, including Silicon CMP Slurry, Tungsten CMP Slurry, Copper CMP Slurry, and Dielectric CMP Slurry.

- Specialty Gases: Gases used for doping, etching, and creating controlled environments, such as Nitrogen, Oxygen, Argon, Hydrogen, Helium, Dopant Gases, and Etch Gases.

- Others: Encompasses other vital materials like Sputtering Targets, Organic Solvents, and Plating Chemicals.

- By Application: This segment outlines the specific fabrication steps where chemicals are utilized.

- Etching: Chemicals used to selectively remove material.

- Cleaning: Solutions for removing contaminants from wafer surfaces.

- Lithography: Materials central to pattern transfer on wafers.

- Doping: Chemicals used to introduce impurities to alter semiconductor properties.

- Deposition: Precursors for laying down thin films.

- Others: Includes processes like packaging and polishing.

- By End-Use Industry: This segment identifies the primary users of these chemicals within the semiconductor ecosystem.

- Foundries: Companies that manufacture integrated circuits for other companies.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own integrated circuits.

- Outsourced Semiconductor Assembly and Test (OSAT): Companies providing assembly and testing services.

- Memory Manufacturers: Companies specialized in producing memory chips.

- By Wafer Size: This segment categorizes chemical consumption based on the size of the silicon wafers.

- 200mm: Older, established fabs.

- 300mm: Predominant wafer size for modern, high-volume production.

- 450mm: Next-generation wafer size, currently in R&D and pilot production phases.

Regional Highlights

- Asia Pacific (APAC): This region dominates the Semiconductor Fabrication Chemical market, driven by the concentration of leading semiconductor manufacturing facilities (foundries and IDMs) in Taiwan, South Korea, China, and Japan. Significant investments in new fabrication plants and the expansion of existing ones, particularly for advanced nodes, solidify APAC's position as the largest and fastest-growing market. Countries like Taiwan and South Korea are at the forefront of advanced chip production, consequently driving high demand for ultra-high purity and specialized chemicals.

- North America: A significant market characterized by strong R&D, innovation, and a growing number of new fab construction projects, particularly in the United States, fueled by government incentives. The region boasts major equipment manufacturers and advanced materials suppliers, contributing substantially to the development and adoption of cutting-edge fabrication chemicals, especially for high-end logic and specialty semiconductors.

- Europe: The European market demonstrates steady growth, supported by investments in automotive, industrial, and power electronics semiconductors. Countries like Germany, France, and Ireland are focal points for manufacturing and research, emphasizing sustainable and environmentally friendly chemical solutions, aligning with stricter regional regulations. There's a concerted effort to increase local manufacturing capabilities to enhance supply chain resilience.

- Latin America, Middle East, and Africa (LAMEA): While smaller in market share compared to other regions, LAMEA is experiencing emerging growth, particularly in areas like Mexico for assembly and testing, and the UAE for potential new investments in semiconductor manufacturing infrastructure. These regions offer long-term growth potential as the global semiconductor supply chain diversifies and expands.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Fabrication Chemical Market.- BASF SE

- Dow Chemical Company

- DuPont de Nemours, Inc.

- Fujifilm Holdings Corporation

- Merck KGaA

- Sumitomo Chemical Co., Ltd.

- Avantor, Inc.

- Solvay SA

- Air Liquide S.A.

- Linde plc

- Entegris, Inc.

- Shin-Etsu Chemical Co., Ltd.

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Resonac Holdings Corporation (formerly Showa Denko K.K.)

- Kanto Chemical Co., Inc.

- Stella Chemifa Corporation

- SK Materials Co., Ltd.

- Cabot Corporation

- JSR Corporation

Frequently Asked Questions

Analyze common user questions about the Semiconductor Fabrication Chemical market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Semiconductor Fabrication Chemical market?

The Semiconductor Fabrication Chemical market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, driven by increasing demand for advanced electronics and technological advancements.

What are the primary drivers fueling the growth of this market?

Key drivers include the global surge in demand for advanced electronic devices, continuous technological advancements in semiconductor manufacturing, expansion of new fabrication capacities worldwide, and the increasing adoption of AI, IoT, and 5G technologies.

How does AI impact the Semiconductor Fabrication Chemical market?

AI significantly impacts the market by optimizing chemical process parameters, accelerating the discovery of new materials, enhancing quality control and defect detection, and improving supply chain management for fabrication chemicals.

Which regions are leading in the Semiconductor Fabrication Chemical market?

Asia Pacific currently dominates the market due to its high concentration of semiconductor manufacturing facilities in countries like Taiwan, South Korea, China, and Japan, with North America and Europe also representing significant and growing markets.

What are the main challenges faced by this market?

The market faces challenges such as increasing technological complexity and ultra-high purity requirements, rapid technological obsolescence in the semiconductor industry, intense competition and pricing pressures, and stringent environmental, health, and safety (EHS) regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted