School Bus Market

School Bus Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707677 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

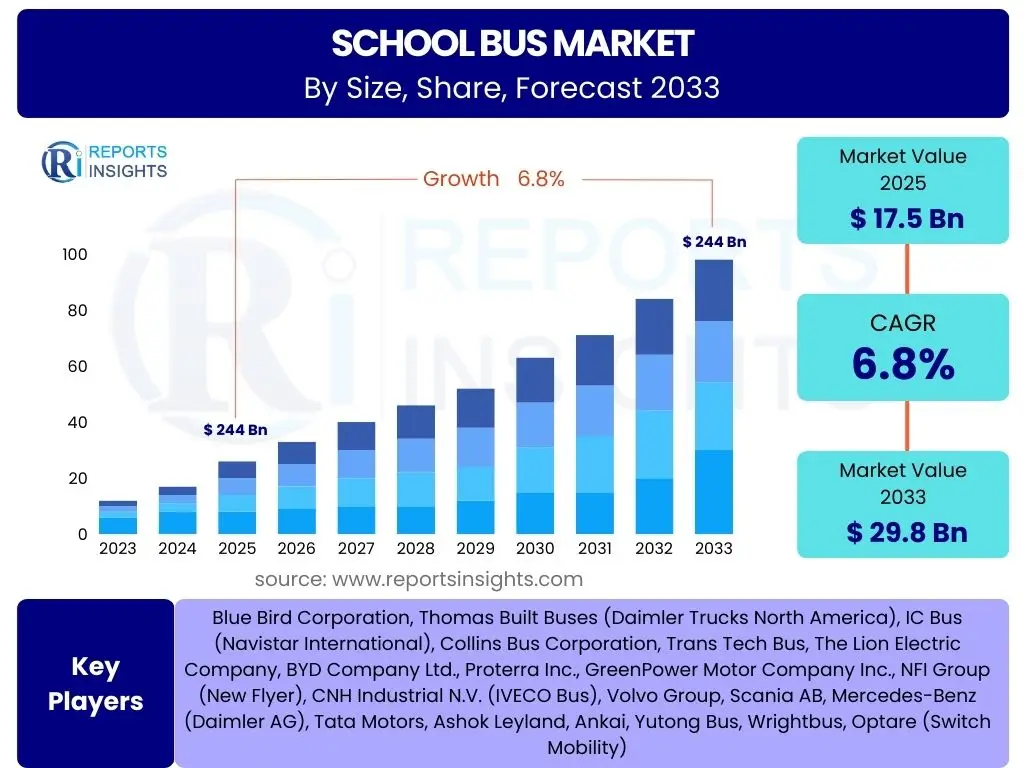

School Bus Market Size

According to Reports Insights Consulting Pvt Ltd, The School Bus Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This robust growth trajectory is underpinned by increasing global student enrollments, evolving safety regulations, and a growing emphasis on sustainable transportation solutions. The market dynamics are also influenced by continuous technological advancements aimed at enhancing fleet efficiency and passenger security.

The market is estimated at USD 17.5 billion in 2025 and is projected to reach USD 29.8 billion by the end of the forecast period in 2033. This significant expansion reflects a rising demand for specialized student transportation, especially in emerging economies, coupled with significant investments in fleet modernization in developed regions. The adoption of electric and alternative fuel buses is a key factor contributing to this market valuation increase, as schools and districts increasingly prioritize environmental sustainability and reduced operational costs.

Key School Bus Market Trends & Insights

Common user inquiries about school bus market trends frequently center on the adoption of green technologies, the integration of advanced safety features, and the impact of connectivity on fleet management. Users are particularly interested in understanding the pace of electric bus deployment, the latest advancements in driver assistance systems, and how digital tools are optimizing operations. There is also significant curiosity regarding the long-term implications of these trends on operational costs, regulatory compliance, and overall student welfare, signaling a broad interest in both environmental and safety-centric innovations within the sector.

The school bus market is undergoing a transformative period marked by several pivotal trends. A prominent shift is observed towards electrification, driven by environmental mandates, government incentives, and the long-term operational cost benefits of electric vehicles. This transition necessitates significant investments in charging infrastructure and presents opportunities for new technological integrations.

Another key trend involves the widespread adoption of advanced safety and telematics systems. These technologies, including AI-powered monitoring, GPS tracking, and collision avoidance systems, are becoming standard features, enhancing student safety and improving fleet management efficiency. Furthermore, there's a growing focus on integrating smart fleet management solutions that offer real-time data on bus performance, driver behavior, and route optimization, thereby revolutionizing traditional school transportation logistics.

- Accelerated adoption of Electric School Buses (ESBs) due to environmental regulations and cost efficiencies.

- Integration of Advanced Driver Assistance Systems (ADAS) and comprehensive safety technologies.

- Expansion of telematics and smart fleet management solutions for real-time monitoring and optimization.

- Increasing demand for alternative fuel vehicles, including CNG and propane buses.

- Focus on enhanced connectivity and cybersecurity measures within school bus fleets.

AI Impact Analysis on School Bus

User queries regarding the impact of AI on school buses often revolve around questions of autonomy, safety enhancements, and operational efficiencies. Common concerns include the potential for job displacement for drivers, the reliability of AI systems in critical safety situations, and the data privacy implications of real-time monitoring. Conversely, users express significant interest in AI's ability to optimize routes, predict maintenance needs, and provide unprecedented levels of student safety and tracking, highlighting a dual perspective of caution and anticipation regarding AI's transformative potential in the sector.

Artificial intelligence is set to profoundly impact the school bus market by enhancing operational efficiency and safety. AI algorithms can optimize bus routes, considering real-time traffic, weather conditions, and student locations, leading to significant fuel savings and reduced travel times. This optimization extends beyond mere mapping, potentially dynamic adjustments to daily schedules to account for unforeseen circumstances, improving overall logistical precision.

Moreover, AI plays a crucial role in predictive maintenance, analyzing vehicle performance data to anticipate mechanical failures before they occur. This proactive approach minimizes downtime, extends vehicle lifespan, and ensures consistent service reliability. In terms of safety, AI-powered systems can monitor driver behavior, detect fatigue, and provide alerts for risky driving patterns. They can also enhance student safety through intelligent camera systems that monitor boarding/unboarding procedures, detect unauthorized individuals, and ensure all students have exited the bus at the end of a route, contributing to a safer transportation environment for children.

- Route Optimization: AI algorithms streamline routes, reducing fuel consumption and travel times based on real-time data.

- Predictive Maintenance: AI analyzes vehicle data to forecast maintenance needs, minimizing breakdowns and maximizing uptime.

- Driver Behavior Monitoring: AI-powered cameras and sensors monitor driver performance, identifying and addressing unsafe driving habits.

- Student Tracking and Safety: AI systems enhance student safety by tracking student presence, ensuring all students exit the bus, and identifying potential threats.

- Autonomous Piloting: Long-term potential for AI to facilitate autonomous driving capabilities, increasing efficiency and potentially addressing driver shortages.

Key Takeaways School Bus Market Size & Forecast

Common user questions about key takeaways from the school bus market size and forecast often focus on understanding the primary growth drivers, the most significant emerging technologies, and the overall trajectory of the industry. Users frequently inquire about the role of electrification in future market expansion, the importance of safety regulations, and how market dynamics differ across various global regions. The synthesis of these insights reveals a market poised for sustainable growth, driven by an imperative for enhanced safety, environmental stewardship, and operational efficiency through technological integration.

The school bus market is on a steady growth trajectory, projected to reach nearly USD 30 billion by 2033, driven largely by the confluence of increasing student populations and a global push for enhanced safety and environmental standards. A paramount takeaway is the accelerating shift towards electric and alternative fuel buses, which represents not just a regulatory compliance measure but a significant long-term investment opportunity for manufacturers and fleet operators alike. This green transition is poised to redefine the manufacturing landscape and operational paradigms within the sector.

Furthermore, the integration of advanced technologies, including telematics, ADAS, and AI-powered solutions, is fundamental to the market's evolution. These technologies are not merely incremental improvements but represent a foundational change in how school bus fleets are managed, monitored, and optimized for safety and efficiency. The market's future will increasingly be defined by how effectively these technological advancements are adopted and integrated across diverse operational environments, reinforcing the importance of innovation in maintaining a competitive edge and meeting evolving stakeholder expectations.

- The School Bus Market is set for substantial growth, driven by increasing student enrollments and a global focus on safety.

- Electrification of fleets is a critical determinant of future market expansion, fueled by government incentives and environmental mandates.

- Technological advancements in safety features, telematics, and AI-driven fleet management are transforming operational efficiencies.

- Regulatory landscapes globally are influencing design, manufacturing, and operational standards, particularly for emissions and safety.

- Emerging markets present significant growth opportunities due to expanding educational infrastructure and improving economic conditions.

School Bus Market Drivers Analysis

The growth of the school bus market is propelled by a combination of demographic shifts, heightened safety awareness, and progressive regulatory frameworks. Increasing student enrollment rates globally, especially in developing regions, directly translate into a higher demand for dedicated student transportation services. This demographic expansion forms a foundational driver, ensuring a continuous need for school buses to facilitate educational access.

Concurrent with population growth, stringent safety regulations imposed by various governmental bodies play a pivotal role. These mandates often necessitate the adoption of newer, safer bus models equipped with advanced features, thereby stimulating fleet modernization and new vehicle purchases. Furthermore, the rising parental concern for children's safety during transit has pressured educational institutions and transport providers to invest in cutting-edge safety technologies and reliable transportation solutions, thereby underpinning market expansion.

Technological advancements, particularly in areas such as vehicle telematics, advanced driver assistance systems (ADAS), and the development of electric and alternative fuel powertrains, also serve as significant market drivers. These innovations enhance operational efficiency, reduce environmental impact, and improve overall safety, making new bus acquisitions more appealing and economically viable in the long run. Government initiatives promoting green transportation and providing subsidies for electric vehicles further accelerate this transition, driving demand for technologically advanced and environmentally friendly school buses.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Student Enrollment & Urbanization | +1.0-1.5% | Global, especially APAC & LATAM | Long-term |

| Stringent School Bus Safety Regulations & Standards | +1.2-1.8% | North America, Europe | Mid-term |

| Government Initiatives & Funding for Green Transport | +1.5-2.0% | North America, Europe, China | Mid to Long-term |

| Technological Advancements in ADAS & Telematics | +0.8-1.2% | Global | Mid-term |

| Growing Parental Awareness & Demand for Safe Transit | +0.7-1.0% | Global | Ongoing |

School Bus Market Restraints Analysis

Despite robust growth drivers, the school bus market faces several significant restraints that could impede its full potential. A primary constraint is the high upfront cost associated with acquiring new school buses, particularly those equipped with advanced technologies or electric powertrains. For many school districts operating under tight budgetary constraints, the initial investment required for fleet modernization or transition to cleaner energy buses can be prohibitive, often leading to delayed upgrades or reliance on older, less efficient models.

Furthermore, the inadequacy of charging infrastructure for electric school buses in many regions presents a considerable barrier to widespread adoption. While the desire to electrify fleets is strong, the lack of accessible and robust charging stations, especially in rural areas or older school properties, complicates the transition. This infrastructure deficit necessitates substantial preliminary investments in electrical grid upgrades and charging station deployment, adding to the financial burden for potential adopters.

Another persistent restraint is the ongoing shortage of qualified school bus drivers across various geographies. This labor challenge directly impacts service capacity and efficiency, sometimes forcing school districts to reduce routes or operate with increased delays. Supply chain disruptions, often leading to delays in vehicle delivery and price volatility of components, also pose a recurring challenge for manufacturers and operators, disrupting planned expansions and fleet replacements.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Costs of New & Electric Buses | -1.0-1.5% | Global, particularly developing nations | Mid to Long-term |

| Inadequate Charging Infrastructure for EVs | -0.8-1.2% | Emerging Markets, Rural Areas | Long-term |

| Shortage of Qualified School Bus Drivers | -0.7-1.0% | North America, Europe | Ongoing |

| Budgetary Constraints of School Districts | -0.6-0.9% | Global | Ongoing |

| Supply Chain Disruptions & Component Shortages | -0.5-0.8% | Global | Short to Mid-term |

School Bus Market Opportunities Analysis

The school bus market is rich with opportunities, particularly stemming from the accelerating global transition towards sustainable transportation and the continuous evolution of vehicle technologies. The most prominent opportunity lies in the widespread adoption of electric and zero-emission school buses. As environmental concerns heighten and regulatory mandates for reduced emissions become stricter, there is a significant push for schools and transport operators to replace their diesel fleets with electric alternatives. Government incentives, grants, and favorable policies further amplify this opportunity, making the transition financially more viable and appealing for districts seeking long-term operational savings and improved air quality.

Beyond electrification, the increasing integration of smart fleet management systems and advanced connectivity solutions presents another substantial avenue for growth. These technologies enable real-time tracking, optimize routes, monitor driver performance, and facilitate predictive maintenance, leading to enhanced operational efficiency, reduced costs, and improved safety protocols. The data generated from such systems can also be leveraged for strategic planning and resource allocation, offering a comprehensive approach to modernizing school transportation logistics.

Furthermore, emerging markets, particularly in Asia Pacific and Latin America, offer significant untapped potential. With burgeoning student populations, increasing government investment in education infrastructure, and a growing emphasis on organized and safe student transportation, these regions are poised for substantial growth. Manufacturers and service providers can capitalize on these opportunities by offering tailored, cost-effective, and technologically advanced solutions that cater to the specific needs and regulatory environments of these diverse markets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Transition to Electric & Zero-Emission Buses | +1.8-2.5% | North America, Europe, China | Long-term |

| Integration of Smart Fleet Management & Telematics | +1.2-1.8% | Global | Mid-term |

| Expansion into Emerging Economies (APAC, LATAM, MEA) | +1.0-1.5% | APAC, LATAM, MEA | Long-term |

| Development & Deployment of Autonomous School Buses | +0.8-1.2% | Developed Markets (Future) | Long-term |

| Public-Private Partnerships (PPP) for Fleet Funding | +0.7-1.0% | Global | Mid-term |

School Bus Market Challenges Impact Analysis

The school bus market, while experiencing growth, faces several operational and strategic challenges that demand innovative solutions. One significant challenge is managing the transition from traditional fossil fuel-powered buses to electric ones. This transition is not merely about vehicle replacement but involves complex infrastructure development, including the installation of charging stations, upgrades to electrical grids, and substantial capital investment, which can be particularly daunting for smaller school districts or private operators with limited financial resources.

Furthermore, the rising cost of fuel for conventional diesel and gasoline buses continues to be a persistent operational challenge, directly impacting the profitability and budget allocations of school districts and private transportation companies. This volatility in fuel prices often necessitates budget reallocations or leads to increased operational expenses, which can be difficult to absorb. Additionally, the increasing complexity of integrating new technologies like advanced driver assistance systems (ADAS) and comprehensive telematics solutions poses a challenge in terms of technical expertise, training for staff, and ensuring seamless interoperability across diverse fleet systems.

The regulatory environment, while often a driver, can also present challenges due to its varying nature across regions and the continuous evolution of safety and emissions standards. Adapting to these changing regulations requires ongoing investment in research and development, manufacturing adjustments, and compliance adherence, which can be burdensome. Cybersecurity risks also emerge as a growing concern with the increased connectivity of modern school buses, demanding robust protection measures to safeguard sensitive data and prevent unauthorized access to vehicle systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment for Fleet Electrification | -1.0-1.5% | Global | Mid to Long-term |

| Rising Fuel Costs for Traditional Bus Fleets | -0.8-1.2% | Global | Short to Mid-term |

| Cybersecurity Risks in Connected Bus Systems | -0.7-1.0% | Global | Ongoing |

| Complexity of Integrating & Maintaining New Technologies | -0.6-0.9% | Global | Mid-term |

| Regulatory Hurdles & Variances Across Regions | -0.5-0.8% | Global | Ongoing |

School Bus Market - Updated Report Scope

This report offers an in-depth, comprehensive analysis of the global School Bus Market, providing a detailed understanding of its current landscape, historical performance, and future growth trajectories. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry. Key insights are derived from extensive market research, incorporating both quantitative data for market valuation and qualitative analysis of market dynamics across various segments and geographical regions. The report is designed to provide stakeholders with actionable intelligence to make informed strategic decisions.

It delineates the market by various segmentation categories including vehicle type, fuel type, seating capacity, technology adopted, and end-user segments, offering a granular view of market composition and potential growth areas. A particular focus is placed on the evolving impact of technological advancements, such as electrification, ADAS, and AI, on the market. Furthermore, the report provides regional highlights, identifying key growth regions and their respective market characteristics, along with profiles of leading market players, offering a competitive landscape analysis. The report serves as an essential resource for manufacturers, suppliers, fleet operators, investors, and policymakers seeking to navigate the complexities and capitalize on the opportunities within the school bus industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.5 Billion |

| Market Forecast in 2033 | USD 29.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Blue Bird Corporation, Thomas Built Buses (Daimler Trucks North America), IC Bus (Navistar International), Collins Bus Corporation, Trans Tech Bus, The Lion Electric Company, BYD Company Ltd., Proterra Inc., GreenPower Motor Company Inc., NFI Group (New Flyer), CNH Industrial N.V. (IVECO Bus), Volvo Group, Scania AB, Mercedes-Benz (Daimler AG), Tata Motors, Ashok Leyland, Ankai, Yutong Bus, Wrightbus, Optare (Switch Mobility) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The School Bus Market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper analysis of market trends, consumer preferences, and technological adoption rates across different categories. Each segment represents distinct market characteristics driven by specific regulations, operational requirements, and end-user needs, allowing for targeted strategic planning and investment decisions.

Understanding these segments is crucial for manufacturers to tailor their product offerings, for operators to optimize their fleet management, and for policymakers to formulate effective regulations and incentive programs. The interplay between vehicle types, fuel sources, passenger capacities, and technological integrations shapes the competitive landscape and dictates future growth avenues within the global school bus industry. The detailed breakdown provides a roadmap for navigating the complexities of this evolving market, ensuring that all aspects of demand and supply are thoroughly addressed.

- By Type:

- Type A: Smaller school buses, often built on cutaway van chassis.

- Type B: Larger than Type A, with a portion of the engine ahead of the windshield.

- Type C: Conventional school buses, with the engine in front of the windshield.

- Type D: Transit-style school buses, with the engine mounted in the front, middle, or rear.

- By Fuel Type:

- Diesel: Traditional fuel source, still dominant globally.

- Gasoline: Primarily used in smaller buses, especially in North America.

- Electric (BEV, FCEV): Battery Electric Vehicles and Fuel Cell Electric Vehicles, gaining significant traction.

- CNG/LPG: Compressed Natural Gas and Liquefied Petroleum Gas, offering cleaner burning alternatives.

- Hybrid: Combines a conventional internal combustion engine with an electric motor.

- By Seating Capacity:

- Small (up to 30 passengers): Typically Type A or smaller Type B buses.

- Medium (31-60 passengers): Commonly Type B and Type C buses.

- Large (above 60 passengers): Predominantly Type C and Type D buses.

- By Technology:

- Conventional: Basic operational and safety features.

- Advanced Driver Assistance Systems (ADAS): Includes features like collision avoidance, lane departure warning, and blind-spot monitoring.

- Telematics & Connectivity: GPS tracking, remote diagnostics, Wi-Fi, and real-time data transmission.

- Autonomous Ready: Buses equipped with hardware and software for future autonomous operations.

- By End-User:

- Public Schools: Largest segment, driven by state and local government contracts.

- Private Schools: Demand for premium features and customized routes.

- Special Needs Transport: Specialized buses with accessibility features for students with disabilities.

- Daycare Centers: Smaller buses for transporting young children.

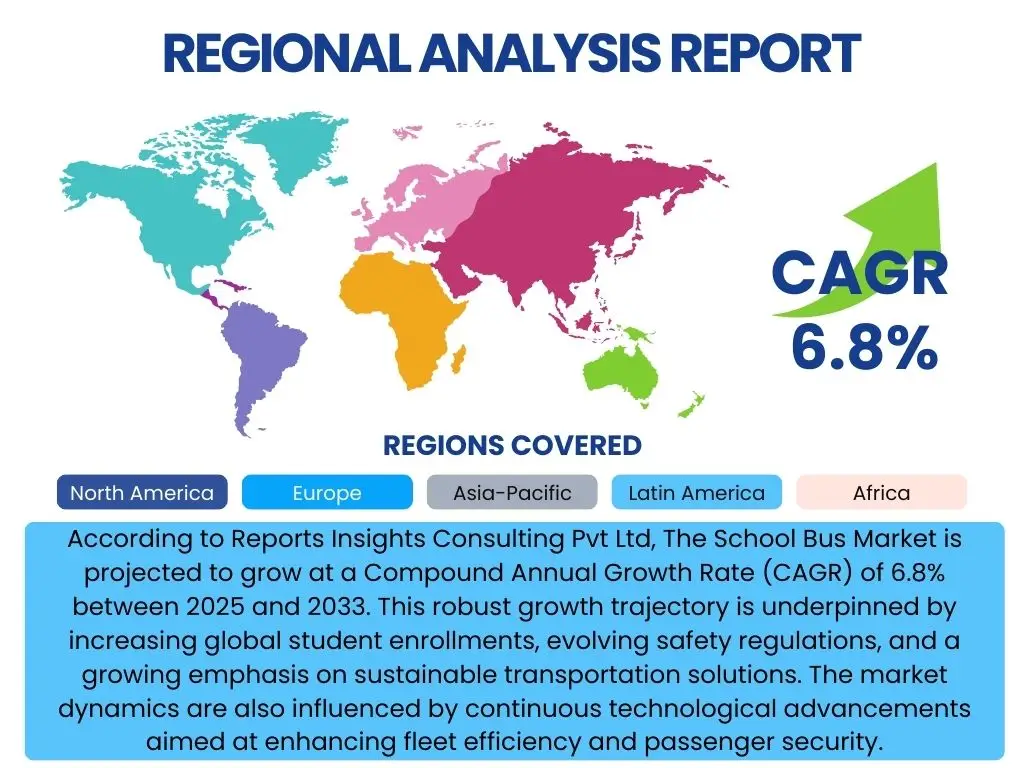

Regional Highlights

- North America: This region holds a significant market share, driven by a large existing fleet, stringent safety regulations, and proactive government initiatives supporting the transition to electric school buses. The United States and Canada are leading the charge in fleet modernization and the adoption of advanced safety and telematics systems. Significant investments in charging infrastructure and incentives for zero-emission vehicles further bolster market growth.

- Europe: Europe is characterized by a strong emphasis on environmental sustainability and advanced vehicle technologies. Countries like the UK, Germany, and France are increasingly investing in electric and hybrid school buses to meet stringent emission standards and reduce urban pollution. The market here is also influenced by robust safety protocols and a growing demand for smart fleet management solutions to optimize operations across diverse urban and rural landscapes.

- Asia Pacific (APAC): The APAC region is poised for substantial growth, fueled by rapidly increasing student populations, urbanization, and rising disposable incomes leading to greater investment in educational infrastructure. China and India are emerging as key markets, with a growing awareness of student safety and a burgeoning manufacturing base for electric vehicles. Government support for clean transportation and increasing urbanization drive the demand for organized and safe school transportation solutions.

- Latin America: This region presents considerable growth potential due to improving economic conditions, increased government spending on education, and the expansion of organized school transportation systems. While diesel buses remain prevalent, there is a nascent but growing interest in more fuel-efficient and environmentally friendly alternatives. Investments in infrastructure development and partnerships with private operators are key to market expansion.

- Middle East & Africa (MEA): The MEA region is witnessing a steady increase in demand for school buses, primarily driven by a growing young population and significant investments in the education sector. Countries in the Gulf Cooperation Council (GCC) are modernizing their fleets and exploring sustainable transport options. While adoption of advanced technologies is slower compared to developed regions, there is a clear trend towards enhancing student safety and improving logistical efficiency.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the School Bus Market.- Blue Bird Corporation

- Thomas Built Buses (Daimler Trucks North America)

- IC Bus (Navistar International)

- Collins Bus Corporation

- Trans Tech Bus

- The Lion Electric Company

- BYD Company Ltd.

- Proterra Inc.

- GreenPower Motor Company Inc.

- NFI Group (New Flyer)

- CNH Industrial N.V. (IVECO Bus)

- Volvo Group

- Scania AB

- Mercedes-Benz (Daimler AG)

- Tata Motors

- Ashok Leyland

- Ankai

- Yutong Bus

- Wrightbus

- Optare (Switch Mobility)

Frequently Asked Questions

What is the projected growth rate of the School Bus Market?

The School Bus Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 29.8 billion by the end of the forecast period.

What are the primary drivers of the School Bus Market?

Key drivers include increasing student enrollments, stringent safety regulations, government initiatives promoting green transportation, and technological advancements in ADAS and telematics.

How is artificial intelligence impacting school bus operations?

AI is significantly impacting operations through route optimization, predictive maintenance, driver behavior monitoring, and enhanced student tracking for improved safety and efficiency.

Which regions are expected to exhibit significant growth in the School Bus Market?

North America is a dominant market, while Asia Pacific (APAC) and Latin America are expected to exhibit significant growth due to increasing student populations and developing educational infrastructure.

What are the key challenges facing the school bus industry?

Major challenges include the high upfront cost of new and electric buses, inadequate charging infrastructure, the ongoing shortage of qualified drivers, and supply chain disruptions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted