Shipbuilding Market

Shipbuilding Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706044 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Shipbuilding Market Size

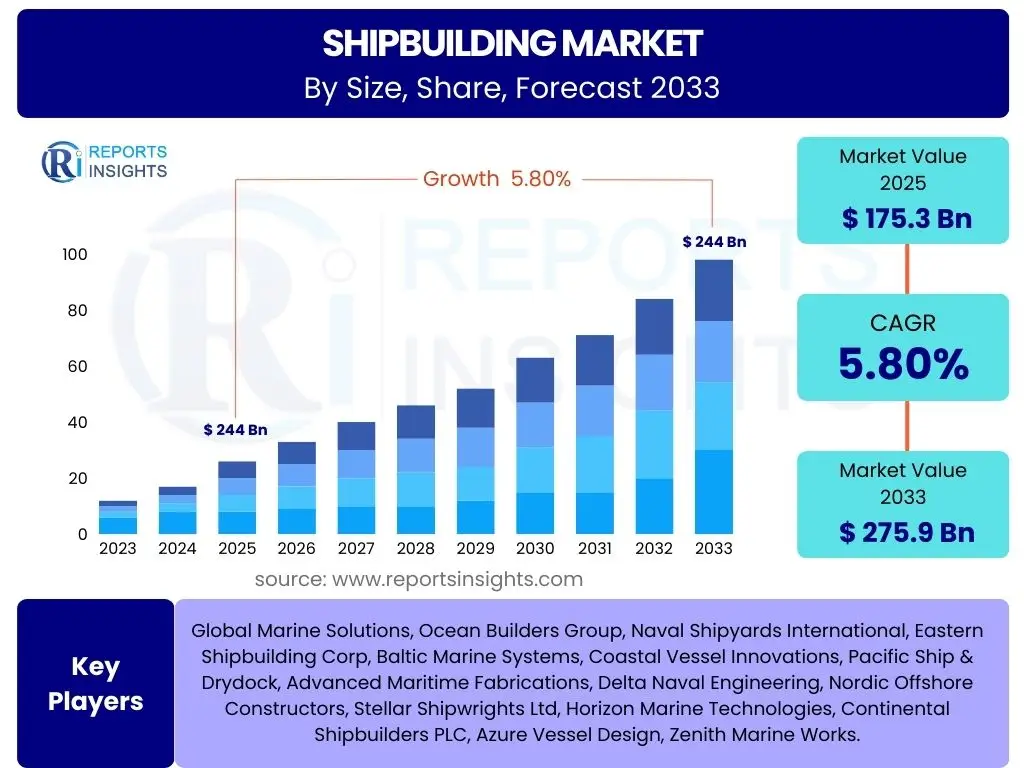

According to Reports Insights Consulting Pvt Ltd, The Shipbuilding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 175.3 billion in 2025 and is projected to reach USD 275.9 billion by the end of the forecast period in 2033.

Key Shipbuilding Market Trends & Insights

The shipbuilding industry is currently navigating a period of significant transformation, driven by a confluence of regulatory pressures, technological advancements, and evolving global trade dynamics. Key trends indicate a decisive shift towards environmental sustainability, with the development of eco-friendly propulsion systems and the adoption of energy-efficient designs becoming paramount. Digitalization is profoundly impacting shipbuilding operations, from design and construction to maintenance and logistics, fostering greater efficiency and precision. Furthermore, geopolitical shifts and the increasing demand for specialized vessels, including those for offshore wind installations and defense, are reshaping market priorities and investment patterns.

Innovation in material science and manufacturing processes, such as additive manufacturing and modular construction, is enabling faster build times and reduced costs. The integration of advanced analytics and Internet of Things (IoT) platforms is enhancing operational intelligence, allowing for predictive maintenance and optimized vessel performance. Workforce development remains a critical aspect, with a focus on upskilling to meet the demands of a highly automated and technologically advanced environment. These trends collectively underscore an industry in constant flux, adapting to meet complex global demands while prioritizing environmental stewardship and operational excellence.

- Decarbonization and Green Shipping Initiatives

- Increased Adoption of Digitalization and Automation

- Growing Demand for Specialized Vessels (e.g., LNG carriers, offshore wind support)

- Emphasis on Modular Construction and Smart Manufacturing

- Advancements in Alternative Fuels and Propulsion Technologies

- Supply Chain Optimization and Reshoring Efforts

- Enhanced Focus on Cybersecurity in Maritime Operations

AI Impact Analysis on Shipbuilding

Artificial Intelligence (AI) is set to revolutionize various facets of the shipbuilding industry, addressing common user concerns regarding efficiency, safety, and environmental compliance. Users frequently inquire about how AI can streamline complex design processes, optimize production schedules, and enhance predictive maintenance capabilities. AI-driven algorithms can analyze vast datasets to identify optimal vessel designs for specific operational profiles, reducing material waste and improving hydrodynamic performance. This translates to more fuel-efficient ships, a critical factor for both economic viability and environmental impact.

Furthermore, AI is instrumental in automating quality control processes through computer vision, detecting defects earlier and with greater precision than traditional methods. In terms of operational intelligence, AI enables advanced analytics for route optimization, real-time performance monitoring, and crew assistance, leading to safer voyages and reduced operational costs. The integration of AI also holds promise for autonomous vessel navigation and remote diagnostics, though regulatory frameworks and human oversight remain central to its widespread adoption. Expectations are high for AI to deliver substantial improvements in productivity, reduce human error, and accelerate the industry's transition towards a more sustainable and intelligent future.

- Optimized Ship Design and Engineering through Generative Design and Simulation

- Enhanced Production Planning and Scheduling via Predictive Analytics

- Automated Quality Control and Defect Detection using Computer Vision

- Predictive Maintenance for Vessel Components and Systems

- Autonomous Navigation and Remote Operations Development

- Supply Chain Management and Logistics Optimization

- Crew Training and Simulation for Complex Scenarios

Key Takeaways Shipbuilding Market Size & Forecast

The shipbuilding market is poised for robust growth, driven by a global push towards fleet modernization and decarbonization, coupled with increasing demand for specialized maritime assets. Key insights reveal that while traditional segments like tankers and bulk carriers will continue to see steady demand, the most dynamic growth will stem from the liquefied natural gas (LNG) carrier market, offshore wind support vessels, and advanced naval platforms. The industry's forecast underscores a strategic pivot towards sustainable solutions and digital integration, transforming how ships are designed, built, and operated. Stakeholders are keen to understand the balance between technological investment and long-term return on investment, particularly concerning green technologies.

Furthermore, the market's trajectory is heavily influenced by international maritime regulations, which are compelling shipyards and owners to invest in new, compliant vessels. The focus on energy efficiency and emissions reduction is not merely a regulatory burden but also a significant market differentiator. Regional dynamics, particularly the dominance of Asian shipyards and the resurgence of specialized European builders, highlight competitive landscapes. The overall takeaway is an industry adapting to complex global challenges by embracing innovation, sustainability, and efficiency, aiming for a future fleet that is cleaner, smarter, and more resilient.

- Steady Market Expansion: Projected CAGR of 5.8% from 2025 to 2033.

- Sustainability as a Core Driver: Strong emphasis on eco-friendly vessels and alternative fuels.

- Digital Transformation: Increasing adoption of AI, IoT, and automation in shipbuilding.

- Specialized Vessel Demand: Growth particularly in LNG carriers, offshore wind, and defense.

- Regulatory Compliance: International emissions regulations driving fleet renewal.

- Asia-Pacific Dominance: Continued leadership from key shipbuilding nations in the region.

Shipbuilding Market Drivers Analysis

The shipbuilding market's expansion is fundamentally propelled by several critical drivers, reflecting global economic shifts, environmental imperatives, and geopolitical dynamics. The increasing volume of international trade necessitates continuous fleet expansion and modernization, particularly for container ships and bulk carriers. A significant driver is the stringent global maritime regulations aimed at reducing carbon emissions and sulfur oxides, compelling shipowners to invest in new, compliant vessels or retrofit existing ones with advanced technologies. This regulatory pressure is fostering innovation in alternative propulsion systems and energy-efficient designs. Furthermore, the burgeoning offshore renewable energy sector, notably offshore wind farms, is creating substantial demand for specialized construction, installation, and maintenance vessels.

Another crucial driver is the ongoing global energy transition, which is boosting demand for liquefied natural gas (LNG) and ammonia carriers, as these fuels are considered transitional or long-term solutions for decarbonizing shipping. Additionally, the increasing focus on maritime security and defense spending by various nations is fueling the demand for advanced naval vessels, including frigates, submarines, and patrol boats. The replacement of aging global fleets, which often lack modern efficiency and environmental standards, also represents a consistent underlying demand. Lastly, technological advancements in design, manufacturing, and operational efficiency are making new vessels more attractive investments, contributing to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Trade Growth & Fleet Modernization | +1.5% | Global, particularly Asia-Pacific, Europe, North America | 2025-2033 (Long-term) |

| Stringent Environmental Regulations (IMO 2020, EEXI, CII) | +1.2% | Global, particularly Europe, Asia-Pacific | 2025-2030 (Medium-term) |

| Growth in Offshore Renewable Energy Sector (Wind) | +0.8% | Europe, North Sea, East Asia, North America | 2025-2033 (Long-term) |

| Transition to Alternative Fuels (LNG, Ammonia, Methanol) | +1.0% | Global, with emphasis on major shipping routes | 2025-2033 (Long-term) |

| Increased Naval Defense Spending & Security Concerns | +0.7% | North America, Europe, Asia-Pacific (China, India, Japan) | 2025-2033 (Long-term) |

Shipbuilding Market Restraints Analysis

While the shipbuilding market exhibits strong growth potential, it also faces several significant restraints that can temper its expansion. One primary concern is the inherent volatility of the global economy, which directly impacts international trade volumes and, consequently, the demand for new vessels. Economic downturns or recessions can lead to reduced shipping activity, resulting in an oversupply of tonnage and deferred newbuild orders. Another substantial restraint is the fluctuating prices of raw materials, particularly steel, which constitute a major component of shipbuilding costs. Unpredictable price increases can erode profit margins for shipyards and inflate the final cost for shipowners, potentially slowing down investment decisions.

Furthermore, the high capital intensity of shipbuilding projects presents a formidable barrier, making financing a critical and sometimes challenging aspect of new construction. Tight credit markets or rising interest rates can significantly impede the ability of shipowners to secure the necessary funds. Intense competition among global shipyards, particularly from dominant players in Asia, can lead to aggressive pricing strategies that depress overall market profitability. Additionally, the shortage of skilled labor, especially for highly specialized roles in advanced shipbuilding and digital technologies, poses a significant operational challenge. Geopolitical uncertainties, trade wars, and protectionist policies can disrupt supply chains and create an unpredictable environment for long-term planning within the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Economic Volatility & Trade Fluctuations | -0.8% | Global | Short to Medium-term (2025-2028) |

| Fluctuating Raw Material Prices (e.g., Steel) | -0.5% | Global, impacting major shipbuilding hubs | Short to Medium-term (2025-2027) |

| High Capital Expenditure & Financing Challenges | -0.4% | Global, particularly for smaller players | 2025-2033 (Long-term) |

| Skilled Labor Shortage & Aging Workforce | -0.3% | Europe, North America, Japan, South Korea | 2025-2033 (Long-term) |

| Geopolitical Instability & Trade Protectionism | -0.6% | Specific trade corridors, global supply chains | Short-term to Medium-term (2025-2029) |

Shipbuilding Market Opportunities Analysis

The shipbuilding market is rich with emerging opportunities driven by innovation, sustainability, and evolving maritime needs. A major avenue for growth lies in the escalating global demand for specialized vessels capable of handling new energy sources, such as LNG, ammonia, and hydrogen. The push for decarbonization is creating a robust market for the development and construction of zero or low-emission ships, equipped with advanced propulsion systems, carbon capture technologies, and energy efficiency solutions. This segment presents significant opportunities for shipyards that can lead in green shipbuilding technologies and meet stringent environmental standards.

The rapid expansion of the offshore wind energy sector offers substantial opportunities for builders of specialized installation vessels, service operation vessels (SOVs), and crew transfer vessels (CTVs). As offshore wind farms grow in scale and move into deeper waters, the complexity and size of required support vessels will increase, driving new design and construction contracts. Furthermore, the digital transformation of the maritime industry, including the adoption of autonomous vessels, smart shipping, and integrated digital platforms, presents opportunities for shipyards to offer value-added services and develop highly automated and data-driven ships. Investment in advanced manufacturing techniques, such as modular construction and additive manufacturing, can also lead to efficiency gains and open new market niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Green Shipping & Alternative Fuel Vessels | +1.8% | Global, particularly Europe, Asia-Pacific | 2025-2033 (Long-term) |

| Expansion of Offshore Wind Energy Sector | +1.5% | Europe, North America, East Asia | 2025-2033 (Long-term) |

| Digitalization & Smart Ship Technologies (Autonomous, IoT) | +1.0% | Global, with technology hubs in Europe, Asia | 2025-2033 (Long-term) |

| Demand for Advanced Naval Vessels & Maritime Security | +0.9% | North America, Europe, Asia-Pacific | 2025-2033 (Long-term) |

| Fleet Replacement & Modernization of Aging Vessels | +0.7% | Global | 2025-2033 (Long-term) |

Shipbuilding Market Challenges Impact Analysis

The shipbuilding market, despite its growth prospects, faces several formidable challenges that require strategic navigation. One significant challenge is the inherent cyclicality of the shipping industry, which leads to unpredictable demand fluctuations and often periods of overcapacity. This volatility makes long-term investment planning difficult for shipyards and can result in periods of reduced newbuild orders. Another critical challenge is the intense global competition, particularly from highly efficient shipyards in certain Asian countries, which can exert downward pressure on prices and profit margins for builders in other regions. This competition often forces shipyards to innovate rapidly or specialize in niche markets to remain competitive.

Regulatory compliance, while a driver for new orders, also presents a complex challenge. Adapting to evolving international maritime regulations regarding emissions, ballast water management, and safety standards requires significant investment in research and development, as well as production adjustments. This can be particularly burdensome for smaller shipyards. Furthermore, the complexity of modern shipbuilding, involving intricate supply chains, advanced technologies, and specialized labor, increases project risks and potential for delays and cost overruns. The availability and retention of a skilled workforce capable of designing, building, and maintaining technologically advanced vessels remains a persistent challenge, particularly in regions facing demographic shifts or lacking robust vocational training programs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industry Cyclicality & Demand Volatility | -0.7% | Global | Short to Medium-term (2025-2029) |

| Intense Global Competition & Price Pressure | -0.6% | Global, impacting Europe, Japan, South Korea | 2025-2033 (Long-term) |

| Navigating Complex & Evolving Regulations | -0.4% | Global, particularly for non-compliant fleets | 2025-2030 (Medium-term) |

| High Research & Development Costs for Green Tech | -0.3% | Europe, Asia-Pacific (leading innovators) | 2025-2033 (Long-term) |

| Supply Chain Disruptions & Geopolitical Risks | -0.5% | Global, impacting key manufacturing regions | Short-term (2025-2027) |

Shipbuilding Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global shipbuilding industry, encompassing its historical performance, current market size, and future growth projections through 2033. The scope includes a detailed examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape. Special attention is given to the impact of emerging technologies, such as artificial intelligence and automation, on shipbuilding processes and vessel capabilities. The report meticulously segments the market by various criteria, including vessel type, technology, and end-use, offering granular insights into each sub-segment's dynamics and growth potential. Furthermore, it provides a thorough regional analysis, highlighting key market trends and competitive landscapes across major geographical areas. The objective is to equip stakeholders with actionable intelligence for strategic decision-making and investment planning within this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 175.3 Billion |

| Market Forecast in 2033 | USD 275.9 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Marine Solutions, Ocean Builders Group, Naval Shipyards International, Eastern Shipbuilding Corp, Baltic Marine Systems, Coastal Vessel Innovations, Pacific Ship & Drydock, Advanced Maritime Fabrications, Delta Naval Engineering, Nordic Offshore Constructors, Stellar Shipwrights Ltd, Horizon Marine Technologies, Continental Shipbuilders PLC, Azure Vessel Design, Zenith Marine Works. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The shipbuilding market is intricately segmented to provide a granular understanding of its diverse components and evolving dynamics. These segmentations allow for a detailed analysis of demand patterns, technological adoption, and regional specificities, offering stakeholders a comprehensive view of where growth opportunities lie. Key segments often include vessel type, which differentiates between commercial, naval, and specialized ships; technology deployed, covering propulsion systems, automation, and digital solutions; and end-use applications, spanning cargo transport, defense, and offshore operations. Understanding these distinct segments is crucial for shipyards to tailor their offerings, for suppliers to target their innovations, and for investors to identify high-potential niches within the broader maritime industry.

Each segment is influenced by unique drivers and faces specific challenges. For instance, the demand for oil tankers is largely dictated by global energy consumption and geopolitics, while container ship orders are tied to international trade volumes. The naval vessels segment is driven by national defense budgets and geopolitical tensions, whereas offshore vessels respond to energy exploration and renewable energy infrastructure development. The propulsion technology segment is witnessing rapid innovation driven by environmental regulations, with a strong shift towards alternative fuels and hybrid systems. Analyzing these segments individually and in relation to each other reveals the complex interplay of factors shaping the future of global shipbuilding.

- By Vessel Type: Oil Tankers, Bulk Carriers, Container Ships, Gas Carriers (LNG, LPG), Chemical Tankers, Passenger Ships (Cruise, Ferry), Naval Vessels (Frigates, Submarines, Aircraft Carriers, Patrol Vessels), Offshore Vessels (OSVs, PSVs, AHTS, Rigs, SOVs, CTVs), Fishing Vessels, Specialized Vessels (Dredgers, Research Vessels, Icebreakers, Tugs).

- By Technology: Propulsion Systems (Diesel, LNG-Electric, Hybrid, Fuel Cell), Automation & Control Systems, Navigation Systems, Communication Systems, Digital Design & Simulation Software, Additive Manufacturing.

- By Material: Steel, Aluminum, Composites, Other Materials.

- By End-Use: Commercial, Defense, Passenger Transport, Offshore Operations.

Regional Highlights

- Asia Pacific (APAC): Dominates the global shipbuilding market, primarily driven by China, South Korea, and Japan. These countries benefit from robust manufacturing capabilities, significant government support, and large domestic and international order books for various vessel types, especially bulk carriers, container ships, and LNG carriers. China is increasingly investing in high-value-added vessels and naval shipbuilding. The region is also a key player in offshore structure fabrication.

- Europe: Known for its specialization in high-value, technologically advanced vessels such as cruise ships, luxury yachts, offshore support vessels, and complex naval vessels. European shipyards excel in innovative design, green technologies, and sophisticated marine equipment, often serving niche markets where technological prowess and quality are paramount. Environmental regulations are a significant driver for new orders in this region.

- North America: Primarily focused on naval shipbuilding and specialized vessels for domestic needs, including Coast Guard vessels, offshore oil and gas support ships, and Great Lakes carriers. Defense spending is a major contributor to this market. There's a growing interest in incorporating advanced digital technologies and automation in new builds.

- Latin America: The shipbuilding market in Latin America is smaller but exhibits potential, particularly in countries like Brazil for offshore and naval vessels. Growth is often tied to resource extraction industries (oil and gas) and regional trade, with efforts to modernize and expand domestic fleets.

- Middle East and Africa (MEA): This region's shipbuilding activities are largely driven by the oil and gas sector, with demand for tankers, offshore support vessels, and repair services. There is also increasing investment in naval capabilities for maritime security. Opportunities are emerging with economic diversification and infrastructure development projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Shipbuilding Market.- Global Marine Solutions

- Ocean Builders Group

- Naval Shipyards International

- Eastern Shipbuilding Corp

- Baltic Marine Systems

- Coastal Vessel Innovations

- Pacific Ship & Drydock

- Advanced Maritime Fabrications

- Delta Naval Engineering

- Nordic Offshore Constructors

- Stellar Shipwrights Ltd

- Horizon Marine Technologies

- Continental Shipbuilders PLC

- Azure Vessel Design

- Zenith Marine Works

Frequently Asked Questions

What is the projected growth rate for the Shipbuilding Market?

The Shipbuilding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by fleet modernization and environmental regulations.

How is AI impacting the Shipbuilding industry?

AI is transforming shipbuilding by optimizing ship design, enhancing production planning, automating quality control, enabling predictive maintenance, and advancing autonomous vessel capabilities, leading to increased efficiency and safety.

What are the primary drivers of the Shipbuilding Market?

Key drivers include global trade growth, stringent environmental regulations pushing for green ships, the expansion of the offshore renewable energy sector, the transition to alternative fuels, and increased naval defense spending worldwide.

Which regions are key players in the global Shipbuilding Market?

Asia Pacific, particularly China, South Korea, and Japan, dominates the market. Europe is prominent for specialized, high-value vessels, while North America focuses on naval and domestic specialized fleets.

What are the main challenges faced by the Shipbuilding Market?

Major challenges include the industry's cyclical nature, intense global competition, navigating complex and evolving environmental regulations, high research and development costs for new technologies, and persistent skilled labor shortages.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted