Electric Axle Drive System Market

Electric Axle Drive System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702402 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

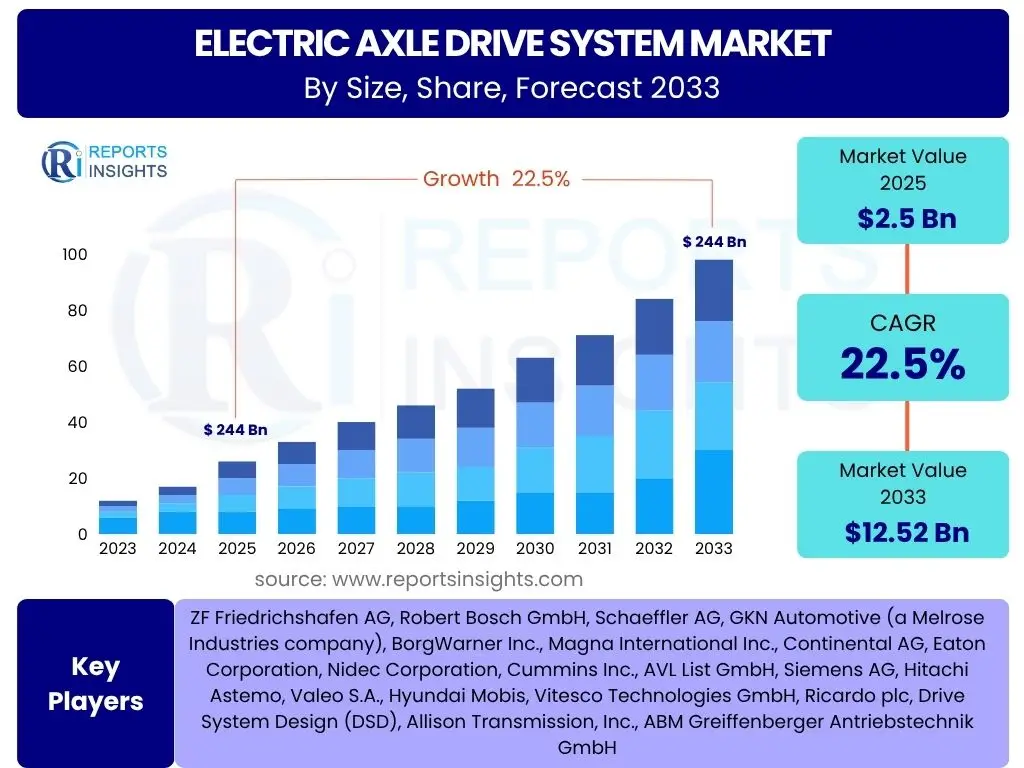

Electric Axle Drive System Market Size

According to Reports Insights Consulting Pvt Ltd, The Electric Axle Drive System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 12.52 Billion by the end of the forecast period in 2033.

Key Electric Axle Drive System Market Trends & Insights

The Electric Axle Drive System (E-Axle) market is rapidly evolving, driven by the global push towards vehicle electrification. Common user inquiries often center on the technological advancements enabling more efficient and compact E-Axle designs, the integration of advanced power electronics, and the industry's shift towards modular and scalable solutions. There is significant interest in understanding how these systems contribute to overall vehicle performance, range, and cost reduction. Furthermore, the increasing adoption of 800V architectures and the growing demand for all-wheel-drive (AWD) electric vehicles are shaping the development landscape of E-Axles.

Another key area of interest revolves around the diversification of E-Axle applications beyond passenger cars, including light and heavy commercial vehicles, and off-highway machinery. Users are keen to know about the impact of stringent emission regulations and government incentives on market growth, as well as the competitive landscape and strategic collaborations between traditional automotive suppliers and new entrants. The market is also witnessing a trend towards enhanced thermal management systems and advanced materials to improve durability and power density, addressing performance and reliability concerns for high-power electric powertrains.

- Miniaturization and integration of components (motor, inverter, gearbox) into a single compact unit.

- Shift towards 800V architectures for faster charging and improved efficiency in high-performance EVs.

- Growing demand for all-wheel-drive (AWD) capabilities, driving the adoption of multiple E-Axles per vehicle.

- Increased focus on modular and scalable E-Axle platforms to serve diverse vehicle segments.

- Development of advanced thermal management solutions for enhanced performance and longevity.

- Expansion of E-Axle applications to commercial vehicles, buses, and off-highway equipment.

- Emphasis on reducing noise, vibration, and harshness (NVH) for improved driving comfort.

AI Impact Analysis on Electric Axle Drive System

Common user questions regarding AI's impact on Electric Axle Drive Systems frequently explore its role in design optimization, manufacturing efficiency, and predictive maintenance. Users are keen to understand how artificial intelligence can accelerate the development cycle of E-Axles, from material selection and topological optimization to simulation and testing. The integration of AI in production lines for quality control and process automation is also a major theme, promising higher precision and reduced waste. Furthermore, there is significant curiosity about AI's potential to enhance the operational performance of E-Axles through real-time data analysis and adaptive control algorithms.

Beyond design and manufacturing, AI is expected to revolutionize the in-use performance and lifespan of Electric Axle Drive Systems. Users often inquire about AI's capabilities in predictive maintenance, where algorithms can analyze sensor data to forecast potential failures, optimize service intervals, and prevent costly downtime. This proactive approach not only improves reliability but also reduces overall cost of ownership. The synergy between AI and E-Axles also extends to vehicle dynamics and energy management, where AI-powered systems can optimize torque distribution, recuperation strategies, and overall efficiency, contributing to extended range and enhanced driving experience. This comprehensive influence positions AI as a transformative force across the E-Axle value chain.

- Design Optimization: AI algorithms enable rapid exploration of design parameters, leading to lighter, more efficient, and structurally robust E-Axle components through generative design and topological optimization.

- Manufacturing Efficiency: AI-powered robotics and vision systems enhance precision manufacturing, automate quality control, and optimize assembly processes, reducing defects and production costs.

- Predictive Maintenance: Machine learning models analyze operational data (temperature, vibration, current) to predict potential failures, enabling proactive maintenance and extending the lifespan of E-Axles.

- Performance Optimization: AI-driven control units can adapt E-Axle performance in real-time based on driving conditions, optimizing torque delivery, energy recuperation, and overall system efficiency.

- Supply Chain Management: AI improves supply chain visibility, demand forecasting, and inventory management for E-Axle components, mitigating risks and ensuring timely production.

- Testing and Validation: AI accelerates virtual testing and simulation processes, identifying design flaws early and reducing the need for extensive physical prototypes.

Key Takeaways Electric Axle Drive System Market Size & Forecast

Common user questions about the key takeaways from the Electric Axle Drive System market forecast highlight a strong consensus around electrification as the primary growth driver. The market's significant Compound Annual Growth Rate (CAGR) underscores the rapid transition from conventional internal combustion engines to electric powertrains across various vehicle segments. Users are particularly interested in the factors contributing to this robust growth, such as supportive government policies, increasing consumer adoption of electric vehicles, and continuous technological advancements in E-Axle design and efficiency. The market is not just expanding in size but also evolving in complexity and integration capabilities, reflecting a broader shift in automotive manufacturing.

Another crucial takeaway is the increasing vertical integration and strategic partnerships among automotive OEMs, Tier 1 suppliers, and specialized E-Axle manufacturers, aimed at securing supply chains and accelerating innovation. The forecast indicates that while passenger vehicles will remain the largest segment, the commercial vehicle sector is poised for substantial E-Axle adoption, opening new avenues for growth. Overall, the market is characterized by intense competition, continuous innovation, and a strong emphasis on achieving higher power density, efficiency, and cost-effectiveness, all of which are critical for the mass-market appeal of electric vehicles. These dynamics suggest a future where E-Axles are a cornerstone of sustainable transportation solutions.

- The Electric Axle Drive System market is experiencing exponential growth, driven by global electrification initiatives and favorable regulatory environments.

- Technological advancements, including higher voltage systems (800V) and integrated designs, are key enablers of market expansion.

- Passenger vehicles remain the dominant application, but commercial vehicles are emerging as a significant growth segment for E-Axle adoption.

- Cost reduction and manufacturing scalability are critical factors for mass market penetration and long-term sustainability.

- Asia Pacific, particularly China, is expected to maintain its leadership in E-Axle deployment due to robust EV production and supportive policies.

Electric Axle Drive System Market Drivers Analysis

The Electric Axle Drive System market is primarily propelled by the accelerating global transition towards electric vehicles (EVs). Stricter emission regulations, such as those in Europe and China, are compelling automotive manufacturers to electrify their fleets, thereby increasing the demand for efficient and compact E-Axle solutions. Government incentives, including subsidies for EV purchases and charging infrastructure development, further stimulate consumer adoption and vehicle production. This regulatory push, combined with growing environmental consciousness among consumers, creates a fertile ground for market expansion.

Beyond regulatory and consumer demand, continuous technological advancements are a significant driver. Innovations in power electronics, motor design, and gearbox integration are leading to E-Axles that are more compact, lighter, more efficient, and capable of higher power output. The development of advanced battery technologies and faster charging capabilities also enhances the appeal of EVs, indirectly boosting the demand for optimized E-Axle systems. As vehicle manufacturers seek to differentiate their EV offerings through superior performance, longer range, and improved driving dynamics, the performance capabilities of E-Axles become a crucial competitive advantage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations & Government Incentives | +5.5% | Global, Europe, China, North America | Short- to Medium-term (2025-2029) |

| Increasing Demand for Electric Vehicles (EVs) | +6.0% | Global | Short- to Long-term (2025-2033) |

| Technological Advancements in E-Axle Design & Efficiency | +4.8% | Global | Medium- to Long-term (2027-2033) |

| Rising Consumer Awareness of Environmental Benefits | +3.2% | Global | Medium-term (2026-2030) |

| Expansion of EV Charging Infrastructure | +3.0% | Global, Urban Areas | Medium- to Long-term (2027-2033) |

Electric Axle Drive System Market Restraints Analysis

Despite robust growth, the Electric Axle Drive System market faces several restraints. A primary concern is the relatively high upfront cost of electric vehicles, which directly impacts the adoption rate of E-Axles. While battery costs are declining, the integrated nature and advanced technology of E-Axles can still contribute significantly to the overall vehicle price, making EVs less accessible for a broader consumer base in some regions. This cost factor is particularly pronounced in emerging markets where purchasing power may be lower, and governments offer fewer incentives to offset the premium.

Another significant restraint is the complexity associated with integrating E-Axles into diverse vehicle platforms and ensuring seamless compatibility with existing automotive architectures. Developing and manufacturing these highly integrated systems requires specialized expertise, sophisticated production processes, and substantial capital investment, posing barriers to entry for new players and challenging established manufacturers. Additionally, the global supply chain for critical components, such as rare earth materials for magnets and semiconductors for power electronics, remains vulnerable to geopolitical tensions and unforeseen disruptions, which can lead to production delays and increased costs for E-Axle manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Electric Vehicles | -3.5% | Global, Developing Economies | Short- to Medium-term (2025-2029) |

| Complexity of E-Axle Integration & Manufacturing | -2.8% | Global | Ongoing, Medium-term (2025-2030) |

| Dependence on Critical Raw Materials & Supply Chain Volatility | -2.0% | Global, Asia Pacific | Ongoing, Short-term (2025-2027) |

| Limited Charging Infrastructure in Some Regions | -1.5% | Africa, Rural Areas of North America/Europe | Short- to Medium-term (2025-2029) |

| Noise, Vibration, and Harshness (NVH) Challenges | -1.0% | Global | Short- to Medium-term (2025-2028) |

Electric Axle Drive System Market Opportunities Analysis

The Electric Axle Drive System market is ripe with opportunities, particularly in the burgeoning commercial vehicle segment. As governments and corporations commit to decarbonizing logistics and public transport, the electrification of light commercial vehicles, trucks, and buses presents a vast untapped market for robust and efficient E-Axles. This shift is driven by operational cost savings (fuel and maintenance) and sustainability mandates, creating a strong business case for fleet electrification. The development of E-Axles tailored for the heavy-duty cycle and higher torque requirements of commercial vehicles offers significant growth potential.

Another promising opportunity lies in the continuous innovation in material science and manufacturing processes. Advancements in wide-bandgap semiconductors (e.g., SiC, GaN) for inverters, novel magnetic materials, and additive manufacturing techniques can lead to even more compact, powerful, and cost-effective E-Axles. Furthermore, the expansion into emerging markets such as India, Southeast Asia, and parts of Latin America, where EV adoption is still in early stages but growing rapidly, represents a long-term growth avenue. Strategic partnerships between established automotive players and technology startups focused on E-Axle development can also accelerate product innovation and market penetration, leveraging diverse expertise and resources.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electrification of Commercial & Off-Highway Vehicles | +4.0% | Global, North America, Europe, Asia Pacific | Medium- to Long-term (2028-2033) |

| Development of Advanced Materials & Manufacturing Technologies | +3.5% | Global | Medium- to Long-term (2027-2033) |

| Growth in Emerging Markets (e.g., India, Southeast Asia) | +3.0% | Asia Pacific, Latin America, Africa | Long-term (2030-2033) |

| Integration with Autonomous Driving Systems | +2.5% | Global, Developed Economies | Long-term (2030-2033) |

| Increasing Demand for High-Performance & AWD EVs | +2.0% | Global, Developed Economies | Short- to Medium-term (2025-2029) |

Electric Axle Drive System Market Challenges Impact Analysis

The Electric Axle Drive System market faces several inherent challenges that could impede its growth trajectory. One significant challenge is the ongoing need to improve power density and efficiency while simultaneously reducing cost. Achieving a balance between high performance, thermal management, and manufacturability at an economical price point remains a complex engineering feat. The continuous demand for lighter, more compact, yet robust E-Axles pushes the boundaries of current material and design capabilities, requiring substantial research and development investment.

Another critical challenge revolves around the standardization and interoperability of E-Axle components and systems across different vehicle platforms and manufacturers. A lack of common standards can lead to fragmentation in the market, increasing development costs and slowing down mass adoption. Furthermore, ensuring the long-term durability and reliability of E-Axles under diverse operating conditions, particularly for commercial vehicles subjected to heavy loads and continuous operation, poses significant engineering hurdles. Addressing these challenges effectively will be crucial for the sustained growth and widespread adoption of Electric Axle Drive Systems globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Cost-Effectiveness & Mass Production Scalability | -3.0% | Global | Ongoing, Medium-term (2025-2030) |

| Thermal Management & Durability in High-Power Applications | -2.5% | Global | Ongoing, Medium-term (2025-2029) |

| Ensuring NVH (Noise, Vibration, Harshness) Performance | -2.0% | Global | Short- to Medium-term (2025-2028) |

| Standardization & Interoperability Across OEMs | -1.8% | Global | Medium- to Long-term (2027-2033) |

| Talent Shortage in EV Powertrain Engineering | -1.2% | Global | Ongoing, Long-term (2025-2033) |

Electric Axle Drive System Market - Updated Report Scope

This comprehensive market research report on the Electric Axle Drive System provides an in-depth analysis of market dynamics, segmentations, competitive landscape, and regional outlook. It covers historical data from 2019 to 2023, offering a robust foundation for understanding past trends, and provides detailed forecasts from 2025 to 2033, projecting future growth opportunities and challenges. The report encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, providing strategic insights for stakeholders across the value chain. It also includes an updated assessment of the impact of artificial intelligence on E-Axle development and deployment, highlighting emerging technological influences.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 12.52 Billion |

| Growth Rate | 22.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ZF Friedrichshafen AG, Robert Bosch GmbH, Schaeffler AG, GKN Automotive (a Melrose Industries company), BorgWarner Inc., Magna International Inc., Continental AG, Eaton Corporation, Nidec Corporation, Cummins Inc., AVL List GmbH, Siemens AG, Hitachi Astemo, Valeo S.A., Hyundai Mobis, Vitesco Technologies GmbH, Ricardo plc, Drive System Design (DSD), Allison Transmission, Inc., ABM Greiffenberger Antriebstechnik GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electric Axle Drive System market is comprehensively segmented to provide a granular understanding of its diverse applications and technological variations. This segmentation enables detailed analysis of market performance across different product types, vehicle categories, and integration levels, offering valuable insights into consumer preferences and industry trends. Understanding these segments is crucial for manufacturers to tailor their product offerings and for investors to identify promising growth areas within the rapidly evolving electric vehicle ecosystem.

- By Component: This segment includes the essential parts that constitute an E-Axle system, such as the Electric Motor (the primary power source), Inverter (converts DC battery power to AC for the motor), Reduction Gear (adjusts motor speed to wheel speed), Power Electronics (manages power flow), Control Unit (manages system operation), Bearings, and Housing. Each component plays a vital role in the E-Axle's overall efficiency, performance, and durability.

- By Drive Type: E-Axles are categorized based on their application in vehicle drivetrains. Front-Wheel Drive (FWD) E-Axles are typically used for compact and efficiency-focused EVs. Rear-Wheel Drive (RWD) E-Axles offer improved traction and performance dynamics. All-Wheel Drive (AWD) E-Axles, often employing multiple E-Axles (front and rear), provide superior traction and handling, particularly for SUVs and high-performance EVs.

- By Vehicle Type: This segmentation differentiates E-Axle applications across various vehicle categories. Passenger Vehicles, including Sedans, SUVs, and Hatchbacks, represent the largest and fastest-growing segment due to increasing consumer adoption of electric cars. Commercial Vehicles, encompassing Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, Buses, and Trucks, are emerging as a significant segment driven by fleet electrification and decarbonization initiatives.

- By Integration Type: This segment distinguishes between different levels of component integration. Integrated Electric Drive Axles combine the electric motor, power electronics, and gearbox into a single, compact unit, offering space savings and simplified assembly. Non-Integrated Electric Drive Axles involve separate components that are then assembled onto the axle, providing more flexibility in design but potentially larger packaging requirements.

- By Voltage Type: E-Axles are classified by their operating voltage. 400V systems are currently standard for most EVs, offering a balance of performance and cost. However, 800V systems are gaining traction, especially in premium and performance EVs, due to their benefits in faster charging times, reduced current losses, and higher power delivery. The 'Others' category may include higher voltage systems or specialized applications.

Regional Highlights

- North America: This region demonstrates strong growth, driven by supportive government policies, increasing consumer interest in electric vehicles, and significant investments in charging infrastructure. The U.S. and Canada are leading the adoption of E-Axles in both passenger and light commercial vehicles, with a focus on advanced technology integration and performance enhancements.

- Europe: Europe is a frontrunner in EV adoption and, consequently, in the Electric Axle Drive System market, propelled by stringent emission regulations and ambitious electrification targets. Countries like Germany, Norway, France, and the UK are witnessing robust growth, emphasizing efficiency, compact designs, and the expansion of E-Axles into commercial fleets and premium vehicle segments.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for Electric Axle Drive Systems, primarily dominated by China. The region's growth is fueled by massive government support for electric mobility, high EV production volumes, and strong consumer demand. India, Japan, and South Korea are also emerging as key contributors, with increasing investments in local manufacturing and R&D for E-Axle technologies.

- Latin America: While currently a smaller market, Latin America is showing nascent growth in EV adoption, particularly in countries like Brazil and Mexico. The market for E-Axles here is expected to gradually pick up as charging infrastructure develops and EV prices become more competitive, driven by regional manufacturing and global partnerships.

- Middle East and Africa (MEA): The MEA region is in the early stages of EV adoption, with market growth for E-Axles being slower compared to other regions. However, increasing government initiatives towards sustainable transportation and diversification of economies away from fossil fuels, particularly in the UAE and Saudi Arabia, are expected to create future opportunities for E-Axle deployment in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electric Axle Drive System Market.- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Schaeffler AG

- GKN Automotive (a Melrose Industries company)

- BorgWarner Inc.

- Magna International Inc.

- Continental AG

- Eaton Corporation

- Nidec Corporation

- Cummins Inc.

- AVL List GmbH

- Siemens AG

- Hitachi Astemo

- Valeo S.A.

- Hyundai Mobis

- Vitesco Technologies GmbH

- Ricardo plc

- Drive System Design (DSD)

- Allison Transmission, Inc.

- ABM Greiffenberger Antriebstechnik GmbH

Frequently Asked Questions

Analyze common user questions about the Electric Axle Drive System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Electric Axle Drive System (E-Axle)?

An Electric Axle Drive System (E-Axle) is a compact, integrated powertrain solution for electric vehicles (EVs) that combines the electric motor, power electronics (inverter), and gearbox into a single, modular unit mounted directly on the vehicle's axle. It simplifies EV architecture, improves efficiency, and frees up space typically occupied by separate components.

How do E-Axles contribute to EV performance and range?

E-Axles optimize EV performance by delivering instantaneous torque and enabling precise power control. Their integrated design reduces energy losses and weight, leading to higher efficiency and extended driving range. Advanced E-Axles also support features like regenerative braking, further enhancing energy recovery and overall vehicle efficiency.

What are the primary benefits of using E-Axles in electric vehicles?

Key benefits include enhanced energy efficiency, leading to longer driving range; reduced complexity and weight due to integrated components; improved packaging space, allowing for more flexible vehicle design; lower noise, vibration, and harshness (NVH) levels; and simplified manufacturing processes, potentially reducing overall production costs.

Which vehicle types primarily utilize Electric Axle Drive Systems?

E-Axles are predominantly used in passenger electric vehicles, including sedans, SUVs, and hatchbacks. Their application is rapidly expanding into commercial vehicles such as light commercial vehicles, medium and heavy-duty trucks, and electric buses, due to the increasing focus on fleet electrification and urban logistics decarbonization.

What are the future trends shaping the Electric Axle Drive System market?

Future trends include a significant shift towards 800V architectures for faster charging and higher power density, increased integration of advanced power electronics (SiC/GaN), the development of modular and scalable E-Axle platforms, and the expansion of applications into off-highway and specialty vehicles. Autonomous driving integration and AI-driven optimization will also play crucial roles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted