Automotive Air Duct Market

Automotive Air Duct Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710190 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

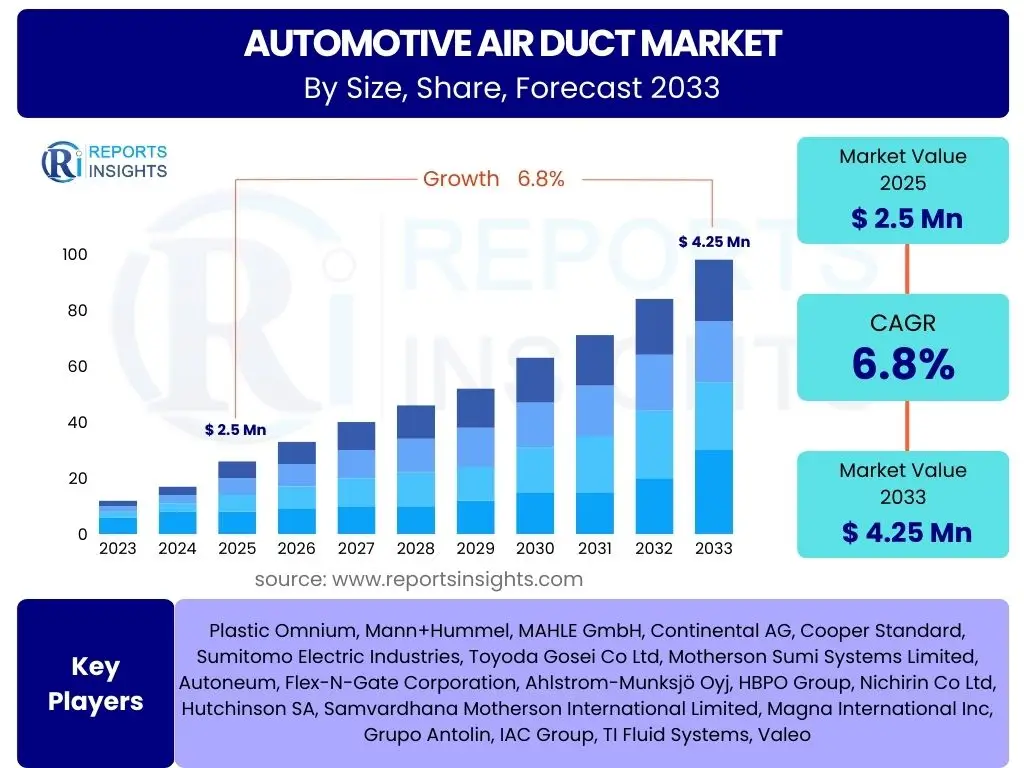

Automotive Air Duct Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Air Duct Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.25 Billion by the end of the forecast period in 2033.

Key Automotive Air Duct Market Trends & Insights

The automotive air duct market is undergoing significant transformation driven by advancements in vehicle technology, evolving consumer demands, and stringent environmental regulations. A primary trend involves the relentless pursuit of lightweighting solutions, where manufacturers are increasingly adopting advanced polymer composites and multi-material designs. This strategic shift aims to reduce overall vehicle weight, directly contributing to improved fuel efficiency in internal combustion engine (ICE) vehicles and extended range for electric vehicles (EVs), while maintaining crucial structural integrity and thermal performance.

Furthermore, the proliferation of electric and hybrid electric vehicles is fundamentally reshaping air duct requirements. EVs necessitate sophisticated thermal management systems for critical components such as battery packs, power electronics, and electric motors. This drives innovation in air duct design, requiring specialized ducts capable of efficiently channeling air for cooling or heating these components, thereby optimizing performance and prolonging their lifespan. The intricate packaging within EVs also promotes the development of more compact, efficient, and application-specific ducting solutions.

Another prominent insight revolves around the growing emphasis on cabin air quality and passenger comfort. Modern automotive air ducts are designed not just for functional airflow but also to enhance acoustic performance, minimize vibrations, and ensure precise distribution of conditioned air throughout the cabin. This trend is fueled by rising consumer expectations for premium in-car experiences and the increasing integration of advanced sensor technologies within HVAC systems to provide adaptive climate control, which relies on optimized air delivery channels for effective operation.

- Lightweighting initiatives through advanced materials like polypropylene and composites.

- Increasing demand for specialized air ducts in Electric Vehicles (EVs) for battery and power electronics thermal management.

- Focus on enhanced cabin air quality, comfort, and noise reduction.

- Integration of modular and multi-functional air duct designs to simplify assembly.

- Development of smart air ducts with integrated sensors for real-time monitoring and control.

AI Impact Analysis on Automotive Air Duct

Artificial Intelligence (AI) is progressively influencing the automotive air duct sector, primarily through optimized design and manufacturing processes. Users are keenly interested in how AI can streamline the complex design phase of air ducts, particularly for intricate geometries required in modern vehicles with limited space. AI-powered generative design tools enable engineers to explore thousands of design iterations based on specified performance criteria, such as airflow efficiency, weight reduction, and material strength, far more rapidly than traditional methods. This capability reduces development time and costs while simultaneously enhancing the functional performance of the air ducts, directly addressing the industry's need for innovation under tight deadlines.

Beyond design, AI is significantly impacting the manufacturing and quality control aspects of air duct production. Machine learning algorithms can analyze data from production lines to predict potential defects, optimize molding parameters, and ensure consistent quality, thus minimizing waste and improving overall manufacturing efficiency. Furthermore, AI-driven predictive maintenance can monitor the operational performance of air ducts within vehicles, identifying potential issues before they lead to failures. This enhances vehicle reliability and reduces maintenance costs for end-users, reflecting a growing user expectation for more robust and intelligent automotive components.

The integration of AI also extends to supply chain management and inventory optimization for air duct components. AI analytics can forecast demand fluctuations, optimize logistics, and manage supplier relationships more effectively, ensuring a steady and cost-efficient supply of materials and finished products. For the end product, AI could eventually contribute to adaptive in-cabin climate control systems where smart air ducts, guided by AI, adjust airflow and temperature based on real-time occupant preferences and environmental conditions, moving towards a more personalized and energy-efficient driving experience. Users are increasingly expecting such intelligent features to be integrated into automotive systems, enhancing comfort and efficiency.

- AI-powered generative design for optimized airflow, lightweighting, and space utilization.

- Predictive analytics in manufacturing for quality control and defect reduction.

- Enhanced supply chain efficiency and demand forecasting for materials.

- Potential for adaptive, AI-driven in-cabin climate control systems.

- Automated inspection and testing processes for improved reliability.

Key Takeaways Automotive Air Duct Market Size & Forecast

The automotive air duct market is poised for steady growth, driven by fundamental shifts in the global automotive landscape. A key takeaway is the sustained demand across both traditional internal combustion engine vehicles, which continue to require efficient air management for engine performance and cabin comfort, and the rapidly expanding electric vehicle segment. The significant projected CAGR indicates that despite the evolutionary changes in vehicle propulsion, air ducts remain an indispensable component, albeit with evolving design and material specifications to meet new functional demands. Stakeholders should recognize the underlying resilience and adaptability of this market segment.

Another crucial insight is the dual impact of regulatory pressures and technological advancements. Stricter emission standards globally compel manufacturers to seek highly efficient air management solutions for ICE vehicles, while the push for greater EV range and safety necessitates innovative thermal management systems that heavily rely on advanced air ducts. This environment fosters continuous innovation in material science and manufacturing processes, suggesting that companies capable of offering lightweight, durable, and highly optimized solutions will secure a competitive advantage in the forecast period.

Ultimately, the market's trajectory is characterized by a strategic focus on integrating air duct systems into broader thermal management and acoustic solutions. The future success of market participants will hinge on their ability to provide comprehensive, integrated solutions that address multiple performance criteria—from enhancing vehicle efficiency and extending EV battery life to improving passenger comfort and reducing cabin noise. The market forecast underscores the opportunity for companies to invest in R&D for next-generation air duct technologies that align with the automotive industry's electrification and autonomy trends.

- Robust market growth projected, indicating sustained demand for air management solutions.

- Electrification of vehicles significantly influences design and functional requirements for air ducts.

- Material innovation, especially lightweight and high-performance plastics, is critical for market competitiveness.

- Increased focus on integrated thermal management and acoustic performance solutions.

- Global regulations and consumer demand for comfort are key drivers for product development.

Automotive Air Duct Market Drivers Analysis

The automotive air duct market is primarily propelled by several synergistic factors, reflecting the dynamic nature of the global automotive industry. Foremost among these is the sustained global increase in vehicle production, particularly in emerging economies where rising disposable incomes fuel higher demand for passenger and commercial vehicles. This broad-based growth in vehicle output directly translates into a greater need for essential components like air ducts, which are integral to both engine performance and cabin climate control systems.

A significant driver also stems from the stringent emission regulations being implemented worldwide. These regulations compel automotive manufacturers to develop more efficient engine systems and adopt technologies that reduce pollutant output. Consequently, advanced air ducts designed for optimized airflow, reduced turbulence, and improved filtration become critical for enhancing engine efficiency, contributing to lower emissions, and meeting compliance standards. This regulatory pressure fosters innovation in air duct design and materials, driving market expansion.

Moreover, the growing consumer demand for enhanced in-cabin comfort and air quality is a pivotal market driver. Modern vehicles are expected to provide sophisticated climate control, precise temperature regulation, and effective cabin air filtration. This necessitates complex and efficiently designed air duct systems that can distribute conditioned air uniformly, quietly, and effectively throughout the passenger compartment, often including multi-zone climate capabilities that rely heavily on advanced ducting networks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Global Vehicle Production and Sales | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium Term |

| Stringent Emission Regulations and Fuel Efficiency Norms | +1.2% | Europe, North America, China, India | Medium to Long Term |

| Growing Demand for Enhanced Cabin Comfort and Air Quality | +1.0% | Global, especially premium segments | Short to Medium Term |

| Increasing Penetration of Electric and Hybrid Vehicles | +1.8% | Global, particularly China, Europe, North America | Medium to Long Term |

| Technological Advancements in HVAC Systems | +1.3% | Global | Short to Medium Term |

Automotive Air Duct Market Restraints Analysis

Despite robust growth drivers, the automotive air duct market faces several notable restraints that could temper its expansion. One significant challenge is the inherent volatility and fluctuations in the prices of raw materials, particularly plastics and certain metals used in air duct manufacturing. These price instabilities directly impact production costs, potentially narrowing profit margins for manufacturers and leading to increased end-product costs, which can ultimately affect vehicle affordability and sales volumes, especially in cost-sensitive market segments.

Another considerable restraint involves the intense competitive landscape and subsequent pricing pressures within the automotive components industry. The market for air ducts is characterized by numerous established players and new entrants, leading to aggressive pricing strategies to secure contracts from Original Equipment Manufacturers (OEMs). This competitive environment can hinder innovation investments for smaller players and exert downward pressure on average selling prices, impacting the overall revenue growth of the market.

Furthermore, the ongoing transition towards electric vehicles (EVs), while an opportunity in some segments, also presents a restraint for traditional engine air intake ducts. As the propulsion systems shift from internal combustion to electric motors, certain air duct applications related to engine combustion and exhaust systems become obsolete. While new thermal management ducts for batteries and power electronics emerge, the overall shift requires significant retooling and design changes, posing a challenge for manufacturers heavily invested in legacy ICE-specific ducting.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (e.g., plastics, steel) | -0.8% | Global | Short to Medium Term |

| Intense Competition and Pricing Pressures | -0.7% | Global | Short to Medium Term |

| Complex Design and Manufacturing Challenges | -0.5% | Global | Medium Term |

| Reduced Demand for Traditional ICE-Specific Ducts with EV Transition | -1.0% | Global, particularly developed markets | Medium to Long Term |

| Supply Chain Disruptions and Geopolitical Instabilities | -0.6% | Global | Short Term |

Automotive Air Duct Market Opportunities Analysis

The automotive air duct market is presented with numerous growth opportunities, primarily driven by ongoing technological evolution and a strategic focus on sustainability. A significant opportunity lies in the continuous innovation and adoption of lightweight and advanced materials. The drive to reduce vehicle weight for fuel efficiency and extended EV range creates a strong demand for air ducts made from high-performance polymers, composites, and bio-based plastics. Manufacturers capable of developing and scaling production of these innovative materials stand to gain substantial market share, as they address core industry needs for performance and environmental responsibility.

Furthermore, the rapid expansion of the electric vehicle (EV) segment opens up entirely new applications for air ducts, particularly within battery thermal management systems. Unlike traditional ICE vehicles, EVs require sophisticated ducting to manage the temperature of battery packs, electric motors, and power electronics, which is crucial for optimal performance, safety, and longevity. This niche but high-growth area presents a significant opportunity for manufacturers to specialize in designing and producing robust, high-tolerance air ducts specifically tailored for EV thermal architecture, often incorporating advanced cooling or heating elements.

Another promising avenue is the development of intelligent and integrated air duct solutions. As vehicles become more connected and autonomous, there is an increasing potential to embed sensors and smart functionalities directly into air ducts. These "smart" ducts could monitor airflow, temperature, and air quality in real-time, feeding data into sophisticated climate control systems or vehicle diagnostics. This integration moves beyond simple air channeling to offer value-added features, enhancing cabin comfort, system efficiency, and overall vehicle intelligence, appealing to consumers seeking advanced technological features.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Lightweight and Sustainable Materials | +1.5% | Global | Medium to Long Term |

| Expansion into EV Battery Thermal Management Systems | +1.7% | Global, especially APAC and Europe | Medium to Long Term |

| Integration of Smart Sensors and Advanced HVAC Features | +1.0% | North America, Europe, Asia Pacific (Premium Segment) | Medium Term |

| Growth in Aftermarket and Replacement Parts Segment | +0.8% | Emerging Economies, Global | Short to Medium Term |

| Customization and Design for Premium Vehicle Segments | +0.9% | Europe, North America, China | Short to Medium Term |

Automotive Air Duct Market Challenges Impact Analysis

The automotive air duct market encounters several significant challenges that require strategic navigation for sustained growth and profitability. A paramount challenge is the need for continuous innovation to keep pace with rapidly evolving vehicle architectures, particularly the shift towards electric vehicle platforms. This requires manufacturers to invest heavily in research and development to design air ducts that fit new chassis designs, accommodate battery packs, and manage complex thermal loads. Failing to adapt swiftly to these architectural changes can lead to market obsolescence and lost opportunities.

Another considerable challenge revolves around achieving cost optimization while simultaneously maintaining or improving product performance and quality. Automotive OEMs continually exert pressure on suppliers to reduce component costs, often without compromising on durability, efficiency, or adherence to stringent performance specifications. This balancing act demands sophisticated manufacturing processes, efficient supply chain management, and smart material selection to deliver competitive products that meet both cost targets and high-quality standards.

Furthermore, global regulatory compliance, especially concerning material usage, environmental impact, and vehicle safety, presents a complex challenge. Manufacturers must ensure their air duct products adhere to diverse and often evolving international standards, including those related to recyclability, flame retardancy, and restriction of hazardous substances. Navigating this intricate web of regulations across different regions adds layers of complexity to product development and market entry, requiring continuous monitoring and adaptation to maintain legal compliance and market access.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Need for Continuous Innovation to Meet Evolving Vehicle Architectures | -0.9% | Global | Medium to Long Term |

| Balancing Cost Optimization with Performance and Quality Demands | -0.8% | Global | Short to Medium Term |

| Compliance with Stringent Global Safety and Environmental Standards | -0.7% | Europe, North America, China | Medium Term |

| Raw Material Scarcity and Supply Chain Vulnerabilities | -0.6% | Global | Short Term |

| Threat from Counterfeit Products and Intellectual Property Infringement | -0.5% | Emerging Economies | Long Term |

Automotive Air Duct Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Air Duct Market, offering a detailed understanding of its current size, growth trajectory, key trends, and future projections. It covers a meticulous examination of market drivers, restraints, opportunities, and challenges that influence the industry landscape. The scope encompasses detailed segmentation analysis by material, vehicle type, application, and sales channel, alongside a thorough regional and competitive landscape assessment to provide actionable market intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.25 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Plastic Omnium, Mann+Hummel, MAHLE GmbH, Continental AG, Cooper Standard, Sumitomo Electric Industries, Toyoda Gosei Co Ltd, Motherson Sumi Systems Limited, Autoneum, Flex-N-Gate Corporation, Ahlstrom-Munksjö Oyj, HBPO Group, Nichirin Co Ltd, Hutchinson SA, Samvardhana Motherson International Limited, Magna International Inc, Grupo Antolin, IAC Group, TI Fluid Systems, Valeo |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Air Duct Market is comprehensively segmented to provide a granular understanding of its various facets, enabling stakeholders to identify specific growth areas and market dynamics. These segmentations are critical for analyzing the market's structure, understanding consumer preferences, and evaluating the competitive landscape across different product types, vehicle categories, and end-use applications. This detailed breakdown allows for targeted strategic planning and informed decision-making.

- By Material: This segment distinguishes air ducts based on the primary materials used in their construction. It includes Plastic (Polypropylene (PP), Polyamide (PA), Polyethylene (PE)), which are widely favored for their lightweight properties, cost-effectiveness, and design flexibility. Other materials like Rubber, often used for flexible connections and vibration dampening, Composites for enhanced strength-to-weight ratios in high-performance applications, and Metal for high-temperature resistance and durability, are also analyzed.

- By Vehicle Type: This segmentation categorizes the market by the type of vehicle the air ducts are designed for. It includes Passenger Cars (PC), which represent the largest volume segment; Light Commercial Vehicles (LCV) and Heavy Commercial Vehicles (HCV), which require robust and high-capacity ducting systems; and Electric Vehicles (EV), a rapidly growing segment with unique thermal management requirements for batteries and power electronics.

- By Application: This segment focuses on the specific function or area within the vehicle where the air ducts are utilized. Key applications include Engine Air Intake systems for optimal combustion, HVAC (Cabin Air) for passenger comfort and climate control, Brake Cooling to maintain performance, and Battery Thermal Management in EVs to ensure battery longevity and safety. Other specialized applications are also considered.

- By Sales Channel: This segmentation differentiates between the primary sales avenues for automotive air ducts. The Original Equipment Manufacturer (OEM) channel involves direct supply to vehicle manufacturers for new vehicle assembly, representing the largest share. The Aftermarket channel caters to replacement parts and upgrades for vehicles already in operation, offering a steady revenue stream due to maintenance and repair needs.

Regional Highlights

- Asia Pacific (APAC): This region is anticipated to be the largest and fastest-growing market for automotive air ducts, primarily driven by robust growth in vehicle production and sales in countries like China, India, and Japan. The increasing adoption of electric vehicles, coupled with supportive government policies and significant investments in automotive manufacturing infrastructure, positions APAC as a critical hub for both demand and supply. The presence of major automotive OEMs and a burgeoning consumer base for new vehicles contribute significantly to its market dominance.

- Europe: Europe represents a mature but technologically advanced market, characterized by stringent emission regulations and a strong emphasis on premium vehicle segments. The region is a leader in adopting lightweight materials and advanced HVAC technologies, driving demand for high-performance and innovative air duct solutions. The rapid transition to electric vehicles in European countries further fuels the need for specialized thermal management ducts for EV components.

- North America: North America demonstrates consistent demand, driven by a stable automotive production base and high consumer expectations for vehicle comfort and performance. The region's focus on larger SUVs and light trucks, along with the growing adoption of electric vehicles, necessitates durable and efficient air duct systems. Technological innovation and strategic partnerships among key players also define this market.

- Latin America: This region is an emerging market with steady growth, influenced by increasing industrialization and automotive manufacturing investments, particularly in countries like Brazil and Mexico. The demand for cost-effective yet reliable air duct solutions is prevalent, with market expansion tied closely to economic stability and rising vehicle ownership.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, primarily due to increasing urbanization, infrastructure development, and a rising demand for vehicles. The market is influenced by both local manufacturing capacities and imports, with a growing emphasis on climate-appropriate HVAC solutions and robust engine air intake systems to withstand harsh environmental conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Air Duct Market.- Plastic Omnium

- Mann+Hummel

- MAHLE GmbH

- Continental AG

- Cooper Standard

- Sumitomo Electric Industries

- Toyoda Gosei Co Ltd

- Motherson Sumi Systems Limited

- Autoneum

- Flex-N-Gate Corporation

- Ahlstrom-Munksjö Oyj

- HBPO Group

- Nichirin Co Ltd

- Hutchinson SA

- Samvardhana Motherson International Limited

- Magna International Inc

- Grupo Antolin

- IAC Group

- TI Fluid Systems

- Valeo

Frequently Asked Questions

What drives the growth of the automotive air duct market?

The market's growth is primarily driven by increasing global vehicle production, stringent emission regulations demanding more efficient engine systems, and rising consumer demand for enhanced in-cabin comfort and air quality. The proliferation of electric vehicles also creates new demand for specialized thermal management air ducts.

How are electric vehicles impacting air duct demand?

Electric vehicles are significantly impacting demand by shifting the focus from traditional engine air intake to new applications such as battery thermal management, cooling for power electronics, and efficient cabin heating/cooling, requiring innovative and specialized air duct designs to manage these critical thermal loads.

What materials are commonly used for automotive air ducts?

Common materials include various plastics like Polypropylene (PP), Polyamide (PA), and Polyethylene (PE) due to their lightweight and cost-effectiveness. Rubber is used for flexible connections, while composites and metals are employed for high-performance or high-temperature applications requiring enhanced durability and strength.

What are the key technological advancements in air duct design?

Key advancements include the use of lightweight and sustainable materials, integration of advanced design software for optimized airflow and space utilization (e.g., generative design), modular and multi-functional designs for easier assembly, and the potential for smart air ducts with embedded sensors for real-time monitoring and control.

Which regions are major contributors to the automotive air duct market?

Asia Pacific, particularly China and India, is the largest and fastest-growing market due to high vehicle production and EV adoption. Europe is also a significant contributor, driven by stringent regulations and advanced vehicle technology. North America maintains a strong presence with its robust automotive industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted