Automotive Bumper Beam Market

Automotive Bumper Beam Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710074 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

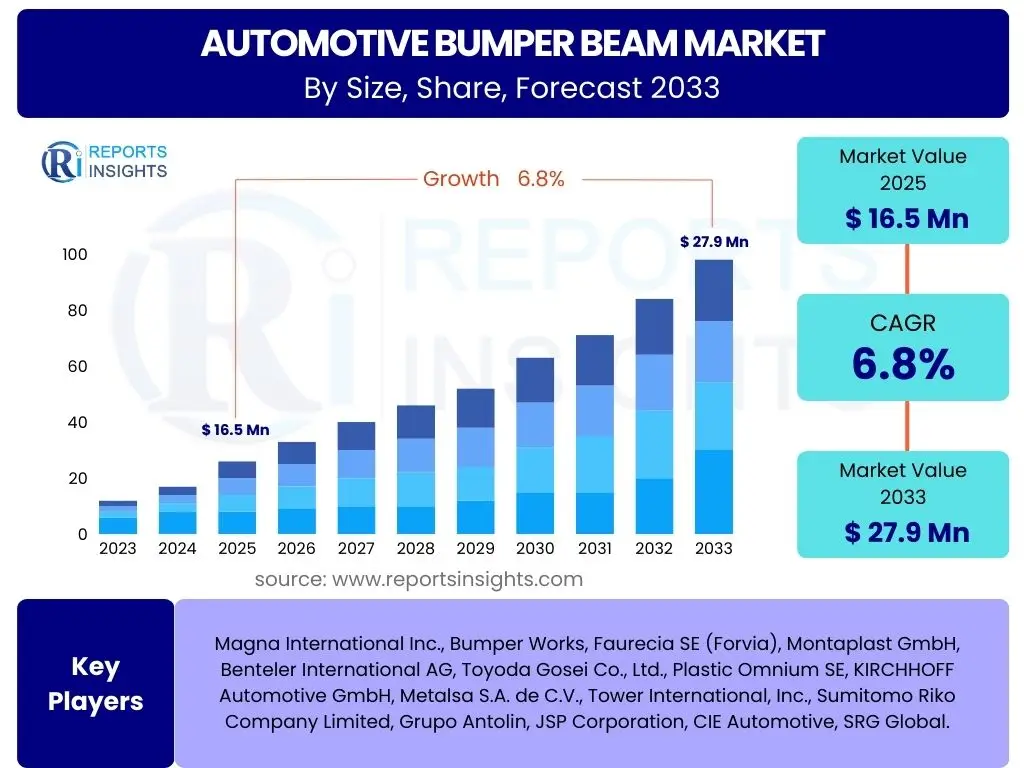

Automotive Bumper Beam Market Size

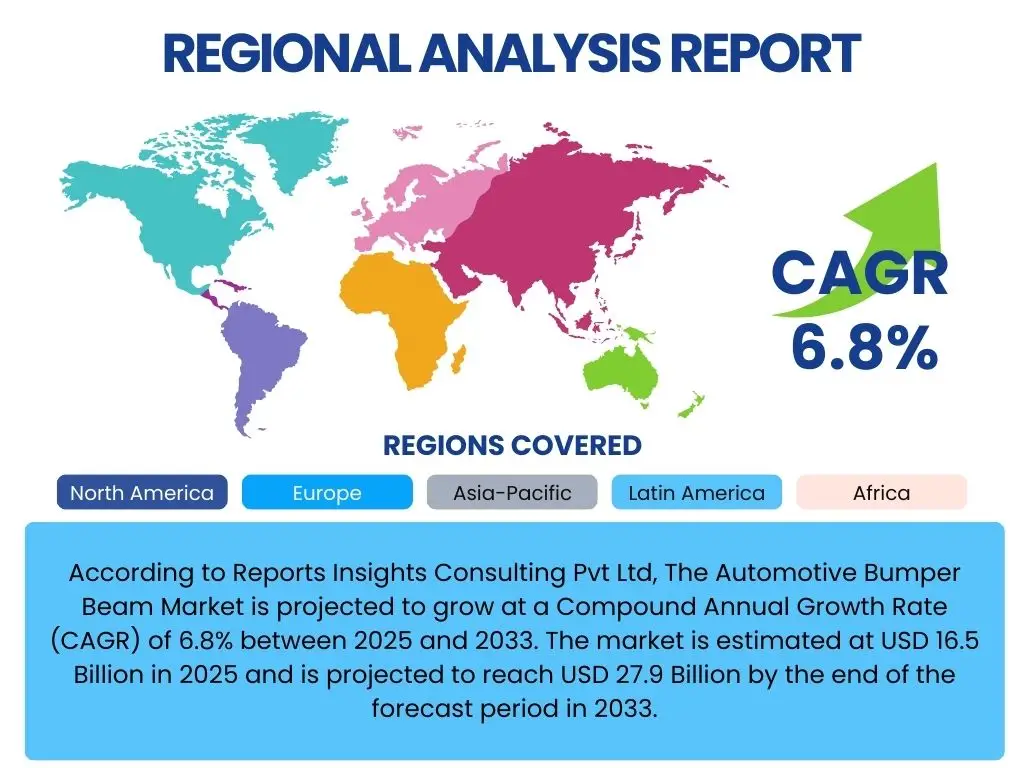

According to Reports Insights Consulting Pvt Ltd, The Automotive Bumper Beam Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 16.5 Billion in 2025 and is projected to reach USD 27.9 Billion by the end of the forecast period in 2033.

The robust growth in the automotive bumper beam market is primarily driven by increasingly stringent global safety regulations, which mandate advanced crash protection features in vehicles. Additionally, the continuous rise in vehicle production, particularly in emerging economies, further contributes to market expansion. Manufacturers are also focusing on material innovation to meet both safety and lightweighting objectives, leading to a steady demand for high-strength steel, aluminum, and composite materials.

Key Automotive Bumper Beam Market Trends & Insights

User inquiries concerning the Automotive Bumper Beam market frequently highlight the evolving landscape of vehicle design, material science, and safety mandates. Common questions revolve around the shift towards lightweight materials, the impact of electric vehicle (EV) proliferation, and the integration of bumper beams with advanced driver-assistance systems (ADAS). Stakeholders are keenly interested in understanding how these trends will influence manufacturing processes, cost structures, and overall market dynamics over the coming decade.

The industry is witnessing a significant move away from traditional heavy materials towards advanced, lighter alternatives that do not compromise structural integrity or crash performance. This material transformation is critical for improving fuel efficiency in internal combustion engine vehicles and extending the range of electric vehicles. Furthermore, the modularization of vehicle platforms and the demand for enhanced pedestrian safety are reshaping bumper beam designs, pushing for more integrated and adaptable solutions. The global emphasis on sustainability also drives research into recyclable and environmentally friendly manufacturing processes for these components.

- Escalating adoption of lightweight materials, including advanced high-strength steel (AHSS), aluminum alloys, and fiber-reinforced composites, to enhance fuel efficiency and EV range.

- Increasing integration of bumper beams with ADAS sensors and radar systems, necessitating design modifications for optimal performance and protection of sensitive electronics.

- Growing demand for modular bumper beam designs that allow for greater flexibility in vehicle platform development and simplify assembly processes.

- Heightened focus on pedestrian safety regulations, driving innovations in energy-absorbing structures and materials within bumper systems.

- Technological advancements in manufacturing processes, such as hydroforming and roll forming, to produce complex shapes with improved strength-to-weight ratios.

- Shift towards sustainable and recyclable materials, aligning with global environmental objectives and circular economy principles in the automotive sector.

- Proliferation of electric vehicles (EVs) influencing bumper beam designs to protect battery packs and accommodate new crash load pathways.

AI Impact Analysis on Automotive Bumper Beam

Common user questions regarding AI's impact on the Automotive Bumper Beam market often revolve around its potential to revolutionize design, manufacturing, and material selection. Users are curious about how AI can optimize crash simulations, predict material performance, and streamline production processes, ultimately leading to safer, lighter, and more cost-effective bumper beams. There is also significant interest in AI's role in supply chain management and quality control, ensuring high-precision manufacturing in an increasingly complex automotive ecosystem.

Artificial intelligence is poised to significantly transform the Automotive Bumper Beam industry by enabling more sophisticated and rapid product development cycles. Through advanced simulation and generative design, AI can explore thousands of design iterations to achieve optimal strength-to-weight ratios, material usage, and crashworthiness in a fraction of the time traditionally required. In manufacturing, AI-powered systems can enhance predictive maintenance, optimize robotic assembly, and improve quality assurance by detecting subtle defects, thereby reducing waste and increasing operational efficiency. This technological integration promises to drive innovation, reduce lead times, and deliver superior bumper beam solutions to the market.

- AI-driven generative design for optimal bumper beam structures, minimizing material usage while maximizing crash energy absorption and safety performance.

- Enhanced crash simulation and virtual testing capabilities through AI algorithms, significantly reducing the need for physical prototypes and accelerating development cycles.

- Predictive analytics for material performance and degradation, enabling better selection of materials and coatings for durability and longevity.

- AI-powered quality control systems in manufacturing, using computer vision and machine learning to detect defects with higher accuracy and speed.

- Optimization of manufacturing processes through AI, including robotic welding, stamping, and assembly, leading to increased efficiency, reduced waste, and lower production costs.

- Supply chain optimization using AI to predict demand, manage inventory, and mitigate disruptions, ensuring a steady flow of raw materials and components.

- Development of smart bumper systems with integrated AI for real-time impact detection and adaptive safety features, though this remains an advanced research area.

Key Takeaways Automotive Bumper Beam Market Size & Forecast

Analysis of common user questions regarding the Automotive Bumper Beam market size and forecast reveals a strong interest in understanding the core growth drivers, the influence of regulatory frameworks, and the long-term impact of technological advancements. Users seek clarity on how material innovations and the evolving vehicle landscape, particularly the rise of EVs, will shape the market's trajectory. Furthermore, there is a consistent demand for insights into regional market variations and the competitive landscape, indicating a need for a comprehensive outlook on market opportunities and potential challenges.

The market for automotive bumper beams is poised for substantial expansion, primarily fueled by the unwavering commitment to enhancing vehicle and pedestrian safety through stricter global regulations. This mandates continuous innovation in bumper beam design and material science, pushing manufacturers to develop solutions that are not only robust but also lightweight and integrated with modern vehicle architectures. The electrification of the automotive industry and the proliferation of advanced driver-assistance systems will further dictate the evolution of bumper beams, requiring adaptive designs that accommodate new structural demands and sensor placements. Consequently, investments in research and development, alongside strategic partnerships, will be critical for companies to capitalize on this growth and maintain a competitive edge.

- The Automotive Bumper Beam Market is projected for significant growth, reaching nearly USD 27.9 Billion by 2033, driven by safety regulations and vehicle production increases.

- Lightweighting initiatives remain a primary focus, with advanced materials like AHSS, aluminum, and composites gaining traction to improve fuel efficiency and EV range.

- Stringent global safety standards (e.g., NCAP ratings, pedestrian protection) are the fundamental catalysts for design evolution and material innovation in bumper beams.

- The integration of ADAS technologies necessitates sophisticated bumper beam designs to protect sensors and ensure their optimal functionality.

- Growth in emerging markets, particularly in Asia Pacific, will significantly contribute to market expansion due to rising vehicle ownership and manufacturing capacities.

- Technological advancements in manufacturing processes and material engineering are crucial for meeting diverse performance, cost, and weight requirements.

- Electric Vehicle (EV) adoption will increasingly influence bumper beam design, requiring solutions that protect high-voltage components and adapt to new crash energy absorption pathways.

Automotive Bumper Beam Market Drivers Analysis

The Automotive Bumper Beam Market is primarily propelled by the global emphasis on vehicle and pedestrian safety. Governments worldwide are implementing and tightening crash safety standards, compelling automakers to integrate more robust and technologically advanced bumper systems. This regulatory push directly fuels demand for innovative materials and design solutions that can effectively absorb impact energy and minimize injury. Concurrently, the increasing production of vehicles across all segments, particularly in rapidly industrializing economies, naturally expands the market for essential components like bumper beams. These factors combine to create a sustained demand environment for advanced bumper beam technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Vehicle Safety Regulations | +1.5% | Global (EU, North America, APAC) | Long-term (2025-2033) |

| Increasing Automotive Production | +1.2% | Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Demand for Lightweight Vehicles | +1.0% | Global | Long-term (2025-2033) |

| Technological Advancements in Materials | +0.8% | Global | Mid to Long-term (2025-2033) |

| Growing Integration of ADAS | +0.7% | North America, Europe, China | Mid-term (2025-2029) |

Automotive Bumper Beam Market Restraints Analysis

Despite robust growth drivers, the Automotive Bumper Beam Market faces several significant restraints. The volatility and high cost of raw materials, particularly for advanced steels, aluminum, and composites, pose a consistent challenge to manufacturers' profitability and pricing strategies. Additionally, the complexity involved in the design and manufacturing of bumper beams, especially those integrating ADAS sensors or employing multi-material constructions, can lead to higher production costs and longer development cycles. These factors necessitate careful supply chain management and innovative engineering solutions to mitigate their impact on market expansion and competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Raw Material Costs | -0.9% | Global | Long-term (2025-2033) |

| Complexity in Design and Manufacturing | -0.7% | Global | Mid to Long-term (2025-2033) |

| Supply Chain Disruptions | -0.6% | Global (esp. Asia Pacific, Europe) | Short to Mid-term (2025-2027) |

| Cost Pressures from OEMs | -0.5% | Global | Long-term (2025-2033) |

| Recycling Challenges for Composite Materials | -0.4% | Europe, North America | Mid to Long-term (2025-2033) |

Automotive Bumper Beam Market Opportunities Analysis

Significant opportunities exist within the Automotive Bumper Beam Market, particularly driven by the global transition towards electric vehicles and the continuous advancement of ADAS technologies. The unique structural requirements and battery protection needs of EVs necessitate specialized bumper beam designs, opening new avenues for innovation in materials and configurations. Furthermore, the integration of an increasing number of sensors for autonomous driving functions means bumper beams must evolve to house and protect these critical components effectively. Beyond technological shifts, the burgeoning automotive markets in developing regions present substantial growth potential for manufacturers capable of offering cost-effective and compliant solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Electric Vehicle (EV) Market | +1.3% | Global (EU, China, North America) | Long-term (2025-2033) |

| Development of Advanced & Sustainable Materials | +1.1% | Global | Mid to Long-term (2025-2033) |

| Expansion in Emerging Automotive Markets | +0.9% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Integration with Advanced Driver-Assistance Systems (ADAS) | +0.8% | Global | Mid-term (2025-2029) |

| Aftermarket Demand for Replacement & Upgrades | +0.5% | Global | Long-term (2025-2033) |

Automotive Bumper Beam Market Challenges Impact Analysis

The Automotive Bumper Beam Market is confronted by several complex challenges that demand innovative solutions and strategic foresight. Achieving optimal balance between lightweighting requirements, stringent safety standards, and cost-effectiveness remains a perpetual hurdle for manufacturers. Furthermore, the rapid pace of technological advancements, particularly in vehicle electrification and autonomous driving, necessitates continuous adaptation in design and manufacturing processes, which can be capital-intensive. Global trade policies, regional manufacturing capabilities, and the environmental impact of material choices also add layers of complexity, requiring a holistic approach to address these multifaceted obstacles effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Lightweighting with Safety Standards | -0.8% | Global | Long-term (2025-2033) |

| High Investment in R&D for New Materials | -0.7% | Global | Mid to Long-term (2025-2033) |

| Fluctuating Raw Material Prices | -0.6% | Global | Short to Mid-term (2025-2027) |

| Meeting Diverse Regional Regulations | -0.5% | Global | Long-term (2025-2033) |

| Competition from Alternative Safety Systems | -0.4% | Global | Mid to Long-term (2025-2033) |

Automotive Bumper Beam Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Bumper Beam market, covering historical data, current market trends, and future growth projections from 2025 to 2033. It meticulously examines the market size, segmented by material type, vehicle type, and sales channel, across key geographical regions. The report further delves into the competitive landscape, identifying key players, analyzing their strategies, and assessing the impact of market drivers, restraints, opportunities, and challenges. Strategic insights are offered to aid stakeholders in making informed business decisions and navigating the evolving market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 16.5 Billion |

| Market Forecast in 2033 | USD 27.9 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Magna International Inc., Bumper Works, Faurecia SE (Forvia), Montaplast GmbH, Benteler International AG, Toyoda Gosei Co., Ltd., Plastic Omnium SE, KIRCHHOFF Automotive GmbH, Metalsa S.A. de C.V., Tower International, Inc., Sumitomo Riko Company Limited, Grupo Antolin, JSP Corporation, CIE Automotive, SRG Global. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Bumper Beam Market is segmented to provide a granular understanding of its diverse components and influencing factors. This segmentation allows for targeted analysis of market dynamics across different material types, which include traditional steel, lightweight aluminum alloys, and advanced composites, each offering distinct advantages in terms of strength, weight, and cost. Furthermore, the market is categorized by vehicle type, differentiating demand and design requirements between passenger cars and various commercial vehicles. Finally, the distinction between OEM and aftermarket sales channels highlights the primary market for new vehicle production versus the robust demand for replacement and upgrade components, offering a comprehensive view of the industry's structure and revenue streams.

Understanding these segments is crucial for stakeholders to identify specific growth areas, adapt product development strategies, and tailor marketing efforts. The continuous innovation in material science is particularly impacting the "By Material Type" segment, as manufacturers seek to meet stringent safety and emissions targets simultaneously. The "By Vehicle Type" segment reflects the diverse needs of different automotive categories, where luxury vehicles might prioritize advanced composites for superior performance, while commercial vehicles might opt for high-strength steel for durability and cost-efficiency. The OEM segment remains dominant, but the aftermarket is a significant revenue generator, influenced by accident rates and vehicle longevity.

- By Material Type:

- Steel (High-Strength Steel, Ultra-High-Strength Steel): Predominantly used for its cost-effectiveness, high strength, and ease of manufacturing.

- Aluminum Alloys: Preferred for lightweighting benefits, offering good strength-to-weight ratio, crucial for fuel efficiency and EV range.

- Composites (Fiber-reinforced plastics): Increasingly adopted for superior lightweighting and complex design capabilities, though typically at a higher cost.

- Plastics (Polypropylene, Polycarbonate): Often used for aesthetic outer coverings but also in energy-absorbing structures behind the bumper beam.

- By Vehicle Type:

- Passenger Cars (Hatchback, Sedan, SUV): The largest segment, driven by high production volumes and diverse safety requirements.

- Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles): Focus on durability, load-bearing capacity, and robust protection.

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Dominant segment, driven by new vehicle production and direct integration into manufacturing lines.

- Aftermarket: Significant segment for replacement parts due to accidents, wear-and-tear, and vehicle customization.

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for automotive bumper beams, primarily driven by robust automotive production in China, India, Japan, and South Korea. Rapid urbanization, rising disposable incomes, and the expansion of vehicle manufacturing facilities in these countries are key contributors. Stringent local safety regulations and the increasing adoption of electric vehicles also fuel demand for advanced bumper beam solutions.

- Europe: A mature market characterized by stringent safety and environmental regulations. Countries like Germany, France, and the UK are at the forefront of automotive innovation, demanding advanced lightweight materials and sophisticated bumper beam designs integrated with ADAS. The region's strong focus on premium and electric vehicles further drives the adoption of high-performance components.

- North America: A significant market driven by high vehicle ownership, a strong emphasis on vehicle safety standards (e.g., NHTSA, IIHS), and a growing preference for SUVs and pickup trucks, which often require robust bumper systems. The increasing shift towards electric vehicles and the continuous demand for advanced driver-assistance systems contribute to market expansion.

- Latin America: An emerging market experiencing steady growth, propelled by increasing vehicle sales and manufacturing activities in countries like Brazil and Mexico. While cost-effectiveness remains a critical factor, evolving safety standards and increasing foreign investment in the automotive sector are gradually driving the adoption of more advanced bumper beam technologies.

- Middle East and Africa (MEA): A developing market with growth influenced by expanding vehicle fleets, urbanization, and improving economic conditions in key countries. The demand for new vehicles and the gradual implementation of enhanced safety regulations are contributing to the moderate but consistent growth of the automotive bumper beam market in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Bumper Beam Market.- Magna International Inc.

- Bumper Works

- Faurecia SE (Forvia)

- Montaplast GmbH

- Benteler International AG

- Toyoda Gosei Co., Ltd.

- Plastic Omnium SE

- KIRCHHOFF Automotive GmbH

- Metalsa S.A. de C.V.

- Tower International, Inc.

- Sumitomo Riko Company Limited

- Grupo Antolin

- JSP Corporation

- CIE Automotive

- SRG Global

Frequently Asked Questions

What are the primary materials used in automotive bumper beams?

The primary materials include high-strength steel, ultra-high-strength steel, aluminum alloys, and various fiber-reinforced composites. These materials are chosen for their superior energy absorption, lightweight properties, and ability to meet stringent crash safety standards.

How do safety regulations impact the design and manufacturing of bumper beams?

Safety regulations, such as those from NCAP and regional bodies, significantly influence bumper beam design by mandating higher crash energy absorption capabilities, improved pedestrian protection, and structural integrity during impacts. This drives innovation in materials, design geometries, and testing protocols.

What role do bumper beams play in electric vehicles (EVs)?

In EVs, bumper beams are crucial for protecting the vehicle's structural integrity and, importantly, the high-voltage battery pack during a collision. Designs often need to accommodate new crash load pathways and integrate with EV-specific architectures while maintaining lightweight properties for range optimization.

What are the key trends shaping the future of the automotive bumper beam market?

Key trends include the increasing adoption of lightweight and multi-material solutions, seamless integration with advanced driver-assistance systems (ADAS) sensors, modular design for manufacturing efficiency, enhanced pedestrian safety features, and the growing demand for sustainable and recyclable materials.

Which region dominates the automotive bumper beam market, and why?

The Asia Pacific region currently dominates the automotive bumper beam market, primarily due to high vehicle production volumes in countries like China, India, and Japan. Robust economic growth, expanding automotive manufacturing bases, and increasing vehicle sales in the region contribute to its leading market position.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted