Sack Kraft Paper Market

Sack Kraft Paper Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702065 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

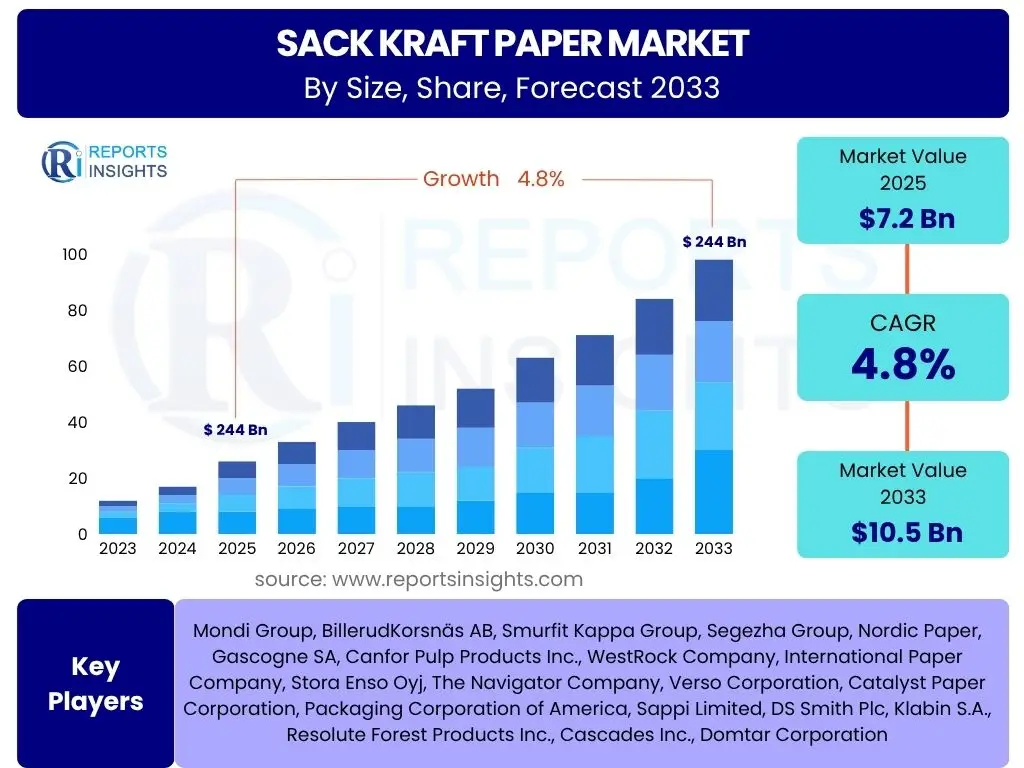

Sack Kraft Paper Market Size

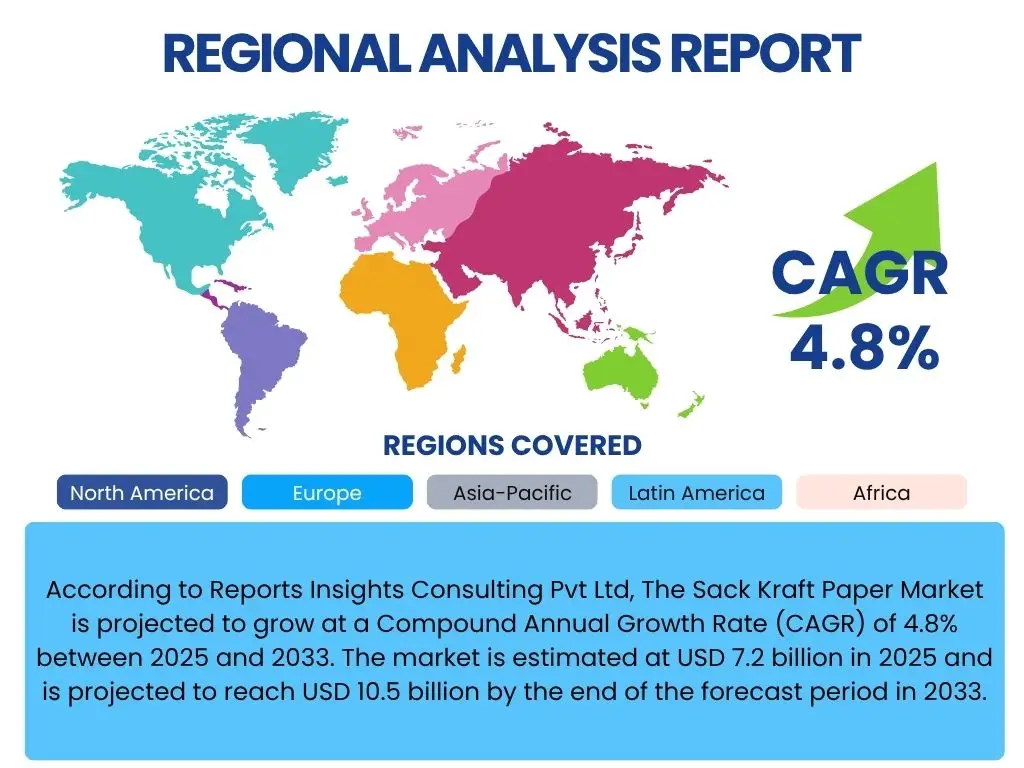

According to Reports Insights Consulting Pvt Ltd, The Sack Kraft Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 7.2 billion in 2025 and is projected to reach USD 10.5 billion by the end of the forecast period in 2033.

Key Sack Kraft Paper Market Trends & Insights

User inquiries into the Sack Kraft Paper market frequently center on its evolving role amidst global sustainability shifts, the impact of e-commerce expansion, and innovations in paper technology. There is significant interest in how manufacturers are adapting to consumer preferences for eco-friendly packaging and the challenges posed by fluctuating raw material costs. Furthermore, stakeholders often seek information on specific industry applications, such as construction materials and food packaging, and the regulatory landscape shaping market dynamics.

A prominent trend involves the increasing adoption of sack kraft paper as a viable and sustainable alternative to plastic and woven bags. This shift is driven by heightened environmental awareness, stricter plastic regulations, and corporate sustainability initiatives. Concurrently, the burgeoning e-commerce sector has fueled demand for robust, recyclable packaging solutions, positioning sack kraft paper as an ideal material for shipping and protection. Technological advancements are also critical, focusing on improving paper strength, moisture resistance, and printability, thereby expanding its utility across diverse industrial and consumer applications.

- Growing demand for sustainable and biodegradable packaging solutions.

- Expansion of e-commerce necessitating durable and eco-friendly shipping materials.

- Technological advancements enhancing paper strength, barrier properties, and printability.

- Increasing application in food and agriculture industries for packaging.

- Rising investments in automation and digitalization across the paper manufacturing process.

- Shift towards lightweighting to reduce material consumption and transportation costs.

AI Impact Analysis on Sack Kraft Paper

User queries regarding the impact of Artificial Intelligence (AI) on the Sack Kraft Paper market predominantly revolve around its potential to optimize manufacturing processes, enhance supply chain efficiency, and contribute to sustainable practices. Users are keen to understand how AI can improve raw material utilization, reduce energy consumption, and ensure consistent product quality. There is also interest in AI's role in demand forecasting, inventory management, and personalized product development, anticipating its transformative effect on operational workflows and market responsiveness.

AI is poised to significantly enhance the operational efficiency and sustainability of sack kraft paper manufacturing. Through predictive analytics, AI can optimize pulp and paper production, minimize waste, and forecast machinery maintenance needs, thereby reducing downtime and operational costs. In the supply chain, AI algorithms can optimize logistics, route planning, and inventory levels, ensuring timely delivery and reducing transportation emissions. Furthermore, AI-powered quality control systems can identify defects in real-time, leading to superior product consistency and customer satisfaction. The integration of AI also facilitates the development of innovative paper grades with enhanced properties, driven by data-driven insights into material science and end-user requirements.

- Optimization of production processes through AI-driven predictive maintenance and process control.

- Enhanced supply chain management and logistics efficiency via AI-powered demand forecasting and route optimization.

- Improved quality control and consistency of sack kraft paper products.

- Accelerated research and development for new paper grades and functionalities.

- Reduced raw material waste and energy consumption, contributing to sustainability goals.

- Data-driven insights for market trend analysis and product innovation.

Key Takeaways Sack Kraft Paper Market Size & Forecast

Common user questions regarding the key takeaways from the Sack Kraft Paper market size and forecast highlight a desire to understand the primary growth drivers, regional market dynamics, and the overarching opportunities for stakeholders. Users frequently inquire about the segments exhibiting the most robust growth, the influence of environmental regulations, and the long-term viability of sack kraft paper as a preferred packaging solution. The focus is on identifying strategic areas for investment and innovation, particularly in light of global sustainability mandates and evolving consumer demands.

The Sack Kraft Paper market is set for sustained growth, largely propelled by the global shift towards eco-friendly packaging and the rapid expansion of e-commerce. The forecast indicates a steady increase in market valuation, signifying the material's increasing relevance across diverse industrial and consumer applications. Key growth segments include food and beverage packaging, building materials, and retail, all driven by the imperative for sustainable and robust solutions. Regional analysis suggests that Asia Pacific will be a significant growth engine due to industrialization and rising consumption, while North America and Europe will continue to lead in innovation and sustainability initiatives.

- The market is on a steady growth trajectory, driven by strong demand for sustainable packaging.

- E-commerce expansion is a pivotal catalyst, increasing the need for durable and recyclable shipping materials.

- Asia Pacific is emerging as a high-growth region, fueled by industrial development and increasing consumption.

- Technological advancements are crucial for enhancing product performance and diversifying applications.

- Sustainability initiatives and regulatory pressures are compelling a shift from plastics to paper-based solutions.

- Investment in R&D for advanced barrier properties and lightweight solutions presents significant opportunities.

Sack Kraft Paper Market Drivers Analysis

The global emphasis on environmental sustainability is a primary driver for the Sack Kraft Paper market. Governments and consumers worldwide are increasingly advocating for and adopting packaging solutions that are biodegradable, recyclable, and derived from renewable resources. Sack kraft paper, being derived from wood pulp, aligns perfectly with these sustainability objectives, positioning it as a preferred alternative to non-biodegradable plastics and other less environmentally friendly materials. This ecological imperative is fostering significant demand across various end-use industries, propelling market expansion.

The rapid growth of the e-commerce sector represents another substantial driver. As online retail continues to expand globally, there is a corresponding surge in demand for reliable, protective, and cost-effective packaging solutions for shipping diverse goods. Sack kraft paper provides excellent strength-to-weight ratio, durability, and a clean aesthetic, making it ideal for mailer bags, protective wrapping, and carton lining. This suitability for e-commerce packaging, coupled with its sustainable profile, solidifies its market position and stimulates further adoption.

Furthermore, the robust performance of the construction and agricultural sectors, particularly in emerging economies, contributes significantly to market growth. Sack kraft paper is extensively used for packaging cement, fertilizers, animal feed, and other bulk materials due to its strength and resistance to tearing. Infrastructure development and increasing agricultural output, particularly in regions with growing populations and economies, directly translate into higher demand for industrial sack packaging, thus fueling the overall market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Sustainable Packaging | +1.2% | Global, particularly Europe and North America | Long-term |

| Growth of E-commerce and Online Retail | +1.0% | Global, notably Asia Pacific and North America | Mid-term |

| Expansion in Construction and Agricultural Sectors | +0.8% | Asia Pacific, Latin America, Middle East & Africa | Mid-term to Long-term |

| Preference for Flexible and Lightweight Packaging | +0.6% | Global | Mid-term |

| Technological Advancements in Paper Production | +0.5% | Developed Regions, gradually spreading globally | Long-term |

Sack Kraft Paper Market Restraints Analysis

One significant restraint on the Sack Kraft Paper market is the volatility of raw material prices, primarily wood pulp. The cost of wood pulp is subject to fluctuations influenced by factors such as forestry policies, weather conditions, global demand, and energy costs. These price instabilities directly impact the production costs of sack kraft paper, subsequently affecting profit margins for manufacturers and potentially leading to higher end-product prices, which can reduce competitiveness against alternative packaging materials.

Competition from alternative packaging materials also poses a considerable restraint. While sack kraft paper is favored for its sustainability, other materials like plastic woven bags, flexible plastics, and jute bags offer different cost structures, barrier properties, and reusability characteristics that might be preferred for specific applications. For instance, in certain bulk goods packaging, the extreme durability and moisture resistance of plastic woven bags may still be prioritized over the eco-friendliness of paper, especially in harsh environments or for very heavy loads.

Furthermore, stringent environmental regulations, while sometimes driving demand for sustainable paper, can also act as a restraint on the supply side. Regulations concerning deforestation, sustainable forest management, water usage, and emissions from paper mills increase operational complexities and capital expenditures for manufacturers. Compliance with these regulations necessitates significant investments in cleaner technologies and sustainable sourcing practices, which can raise production costs and potentially limit the expansion of manufacturing capacities in some regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Wood Pulp) | -0.7% | Global | Short to Mid-term |

| Competition from Alternative Packaging Materials | -0.6% | Global, especially in industrial applications | Mid-term |

| Stringent Environmental Regulations on Production | -0.5% | Europe, North America | Long-term |

| High Energy Consumption in Manufacturing Process | -0.4% | Global | Mid-term |

| Supply Chain Disruptions and Logistics Costs | -0.3% | Global | Short-term |

Sack Kraft Paper Market Opportunities Analysis

The increasing consumer awareness and preference for sustainable products present a significant opportunity for the Sack Kraft Paper market. As environmental concerns escalate, consumers are actively seeking brands that align with eco-friendly values, translating into a higher demand for packaging made from renewable and recyclable materials. This growing eco-conscious consumer base offers manufacturers the opportunity to differentiate their products and expand market share by emphasizing the sustainable attributes of sack kraft paper, fostering brand loyalty and driving sales.

Innovation in barrier coatings and specialty paper grades represents another lucrative opportunity. Traditional sack kraft paper, while strong, may lack adequate barrier properties for certain moisture-sensitive or greasy products. Developing advanced coatings that enhance moisture resistance, grease proofing, and oxygen barriers without compromising recyclability or biodegradability can open up new applications in the food, pharmaceutical, and chemical industries. These advancements allow sack kraft paper to compete in segments traditionally dominated by multi-material or plastic packaging, broadening its market scope.

Furthermore, the global shift towards circular economy models creates substantial opportunities for growth. Initiatives focused on reducing waste, promoting reuse, and enhancing recycling rates align perfectly with the inherent recyclability of sack kraft paper. Manufacturers can capitalize on this by investing in recycling infrastructure, developing products with higher recycled content, and promoting closed-loop systems. This emphasis on circularity not only improves the environmental footprint of sack kraft paper but also supports regulatory compliance and fosters long-term market resilience.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Consumer Preference for Sustainable Solutions | +1.3% | Global | Long-term |

| Innovation in Barrier Coatings and Specialty Papers | +1.1% | Developed Regions, gradually spreading | Mid to Long-term |

| Expansion into New End-use Applications | +0.9% | Global | Mid-term |

| Investments in Enhanced Recycling Infrastructure | +0.7% | Europe, North America, parts of Asia Pacific | Long-term |

| Emerging Markets Industrialization and Urbanization | +0.6% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

Sack Kraft Paper Market Challenges Impact Analysis

One significant challenge facing the Sack Kraft Paper market is managing supply chain disruptions, which can stem from various global events such as geopolitical conflicts, natural disasters, or pandemics. These disruptions can severely impact the availability of raw materials like wood pulp, chemicals, and energy, leading to production delays and increased costs. The globalized nature of the industry means that issues in one region can have a cascading effect across the entire supply chain, making consistent and timely supply a complex endeavor.

The industry also grapples with the challenge of high capital investment requirements for capacity expansion and technological upgrades. Establishing new paper mills or modernizing existing ones requires substantial financial outlay for machinery, infrastructure, and environmental compliance systems. This high barrier to entry and expansion can limit the ability of smaller players to compete effectively and can slow down the overall market's response to rising demand, potentially leading to supply shortages or stifling innovation in regions with limited investment capital.

Moreover, the intensive energy consumption and associated environmental footprint of paper manufacturing present an ongoing challenge. While sack kraft paper is sustainable as a product, its production process can be energy-intensive and contribute to carbon emissions if not managed with renewable energy sources and efficient technologies. Meeting increasingly stringent emission standards and reducing the carbon footprint of production processes requires continuous investment in sustainable practices and technology, adding to operational complexities and costs for manufacturers striving for greener production without compromising profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility and Disruptions | -0.8% | Global | Short-term |

| High Capital Investment for Capacity Expansion | -0.6% | Global | Long-term |

| Managing Energy Consumption and Carbon Footprint | -0.5% | Global, particularly Europe and North America | Long-term |

| Skilled Labor Shortages in Manufacturing | -0.4% | Developed Regions | Mid-term |

| Intense Competition from Established Players | -0.3% | Global | Mid to Long-term |

Sack Kraft Paper Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Sack Kraft Paper market, encompassing historical data, current market dynamics, and future projections. It delves into the key drivers, restraints, opportunities, and challenges influencing market growth across various segments and major geographical regions. The report also highlights technological advancements, competitive landscape analysis, and strategic profiles of key market players, offering stakeholders actionable insights for informed decision-making and strategic planning within the global sack kraft paper industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mondi Group, BillerudKorsnäs AB, Smurfit Kappa Group, Segezha Group, Nordic Paper, Gascogne SA, Canfor Pulp Products Inc., WestRock Company, International Paper Company, Stora Enso Oyj, The Navigator Company, Verso Corporation, Catalyst Paper Corporation, Packaging Corporation of America, Sappi Limited, DS Smith Plc, Klabin S.A., Resolute Forest Products Inc., Cascades Inc., Domtar Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Sack Kraft Paper market is meticulously segmented to provide a granular view of its diverse applications and product variations. This segmentation enables a detailed understanding of market dynamics, identifying specific areas of growth and opportunity based on product characteristics, application requirements, and geographical preferences. The analysis covers various types of sack kraft paper, distinguished by bleaching, basis weight, and ply, reflecting different performance needs and cost considerations. Furthermore, the segmentation by packaging type addresses the specific structural designs of sacks, which are tailored for particular handling and filling processes across industries.

The end-use industry segmentation is particularly crucial, highlighting the extensive adoption of sack kraft paper across sectors such as building & construction, food & beverages, chemicals, and agriculture. Each industry segment has unique requirements for paper strength, barrier properties, and handling characteristics, driving demand for specific sack kraft paper solutions. For instance, cement packaging demands high tear resistance and durability, while food products require food-grade safety and sometimes moisture barriers. This detailed segmentation offers insights into which industries are driving the most significant demand and where future growth is anticipated.

- By Product Type:

- Bleached Sack Kraft Paper

- Unbleached Sack Kraft Paper

- By Basis Weight:

- Less than 70 GSM

- 70-80 GSM

- 80-90 GSM

- More than 90 GSM

- By Ply:

- 1 Ply

- 2 Ply

- 3 Ply and Above

- By Packaging Type:

- Open Mouth Sacks

- Valve Sacks

- Pinch Bottom Sacks

- Sewn End Sacks

- Other Sacks

- By End-Use Industry:

- Building & Construction

- Cement

- Dry Mortar

- Others

- Food & Beverages

- Flour

- Sugar

- Grain

- Animal Feed

- Other Food Products

- Chemicals

- Fertilizers

- Polymers

- Other Chemicals

- Minerals

- Mining

- Aggregates

- Other Minerals

- Consumer Goods

- Agriculture

- Others

- Building & Construction

Regional Highlights

- North America: A mature market characterized by increasing adoption of sustainable packaging and a strong presence of key manufacturers focusing on specialty and high-performance sack kraft paper. The region exhibits steady growth driven by the e-commerce boom and demand for eco-friendly industrial packaging.

- Europe: A leader in sustainability and environmental regulations, driving significant demand for sack kraft paper as an alternative to plastics. Focus on innovation in lightweighting and advanced barrier properties, with strong growth in food packaging and construction sectors.

- Asia Pacific (APAC): The fastest-growing market, fueled by rapid industrialization, urbanization, and increasing infrastructure development in countries like China, India, and Southeast Asian nations. High demand from the construction, food & beverage, and agriculture sectors contributes significantly to market expansion.

- Latin America: Benefits from abundant natural resources and growing industrial and agricultural output. Brazil and Mexico are key contributors, driven by domestic consumption and exports, with increasing awareness of sustainable packaging solutions.

- Middle East and Africa (MEA): Emerging market with potential growth driven by ongoing construction projects, particularly in the Gulf Cooperation Council (GCC) countries, and increasing demand for packaged food and agricultural products. Investments in infrastructure and industrialization are key drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sack Kraft Paper Market.- Mondi Group

- BillerudKorsnäs AB

- Smurfit Kappa Group

- Segezha Group

- Nordic Paper

- Gascogne SA

- Canfor Pulp Products Inc.

- WestRock Company

- International Paper Company

- Stora Enso Oyj

- The Navigator Company

- Verso Corporation

- Catalyst Paper Corporation

- Packaging Corporation of America

- Sappi Limited

- DS Smith Plc

- Klabin S.A.

- Resolute Forest Products Inc.

- Cascades Inc.

- Domtar Corporation

Frequently Asked Questions

What is sack kraft paper used for?

Sack kraft paper is primarily used for packaging bulk materials such as cement, dry mortar, flour, sugar, animal feed, fertilizers, chemicals, and minerals. Its high strength, durability, and tear resistance make it ideal for heavy-duty industrial and agricultural applications, as well as for various consumer goods and e-commerce packaging.

Why is sack kraft paper considered sustainable?

Sack kraft paper is considered sustainable because it is made from renewable wood fibers, is biodegradable, and highly recyclable. Its production often utilizes sustainably managed forests and offers a lower environmental impact compared to plastic alternatives, aligning with global efforts to reduce plastic waste and promote a circular economy.

What are the main drivers of the sack kraft paper market?

The main drivers include the increasing global demand for sustainable and eco-friendly packaging solutions, the rapid expansion of the e-commerce sector, and continued growth in the construction and agricultural industries. Technological advancements enhancing paper performance also significantly contribute to market expansion.

What are the key challenges facing the sack kraft paper market?

Key challenges include volatility in raw material (wood pulp) prices, intense competition from alternative packaging materials, high capital investment requirements for production facilities, and the need to manage energy consumption and environmental footprints during manufacturing processes.

How is AI impacting the sack kraft paper industry?

AI is impacting the sack kraft paper industry by optimizing production processes through predictive maintenance, improving supply chain efficiency with advanced forecasting, enhancing quality control, and accelerating research and development for new paper grades. It also aids in reducing waste and energy consumption, supporting sustainability initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted