Gate All Around FET Technology Market

Gate All Around FET Technology Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700378 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

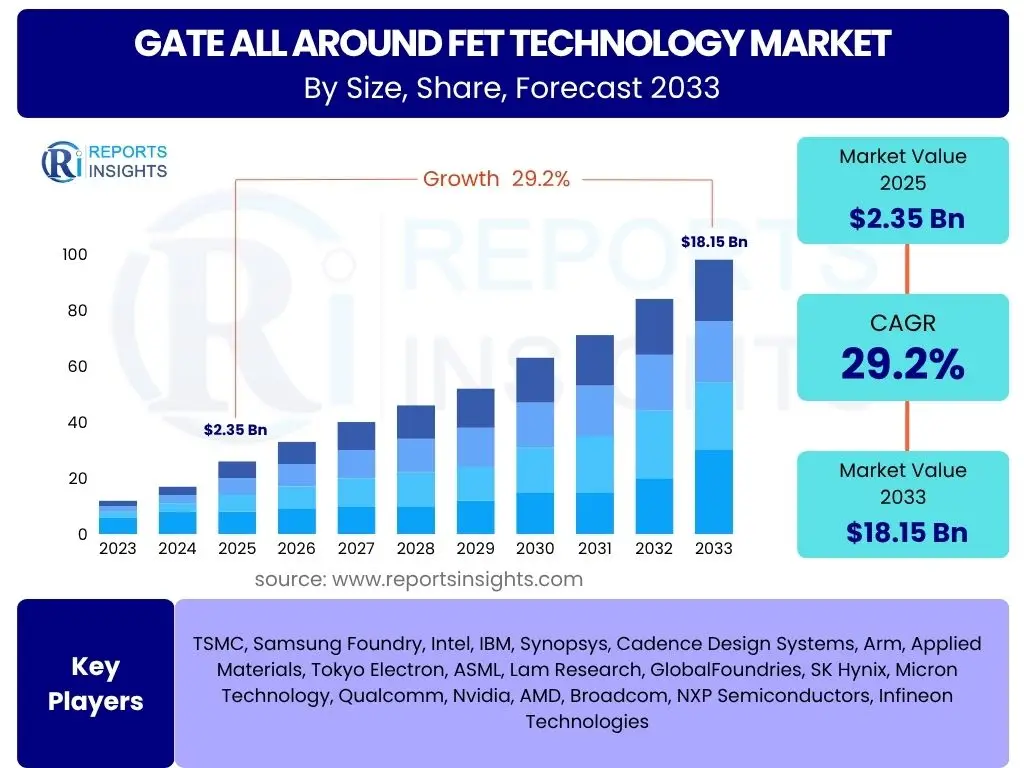

Gate All Around FET Technology Market Size

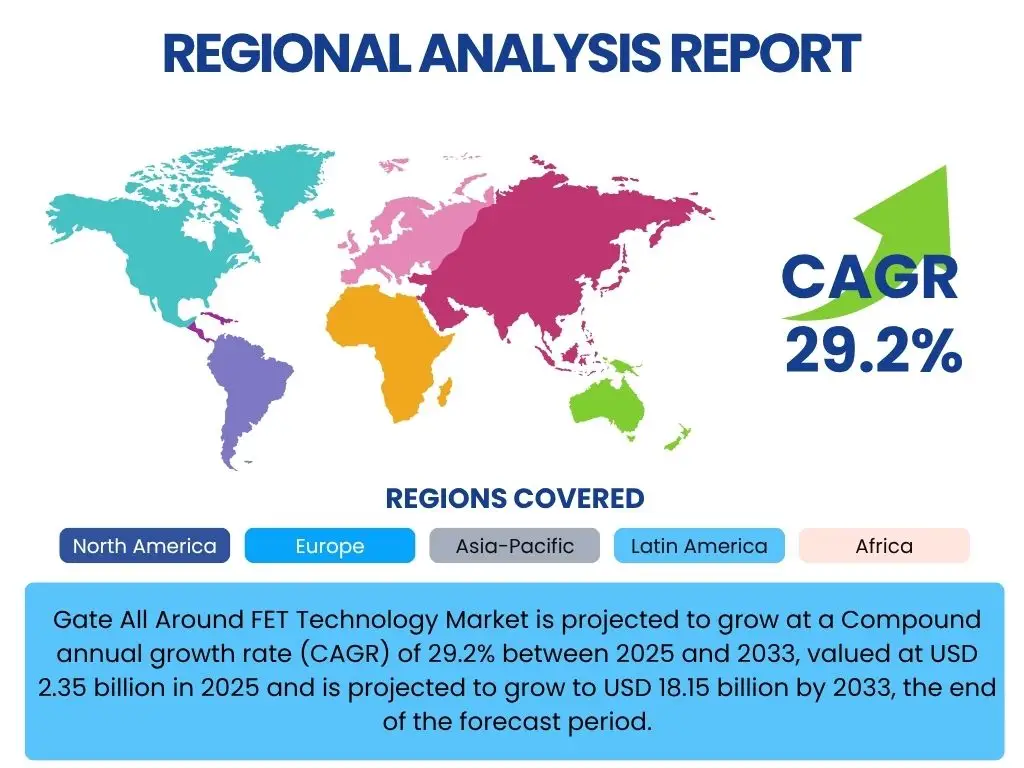

Gate All Around FET Technology Market is projected to grow at a Compound annual growth rate (CAGR) of 29.2% between 2025 and 2033, valued at USD 2.35 billion in 2025 and is projected to grow to USD 18.15 billion by 2033, the end of the forecast period.

Key Gate All Around FET Technology Market Trends & Insights

The Gate All Around FET Technology market is experiencing transformative trends driven by the increasing demand for advanced semiconductor performance, power efficiency, and miniaturization. These innovations are reshaping the landscape of high-performance computing, artificial intelligence, and mobile technology. The shift from FinFET to GAAFET architectures represents a significant technological leap, promising enhanced gate control and reduced leakage current, critical for scaling beyond current limitations. This evolution is underpinned by substantial research and development investments and collaborative efforts across the semiconductor ecosystem to overcome manufacturing complexities and accelerate adoption.

- Transition from FinFET to GAAFET for improved performance and power efficiency.

- Increasing adoption in advanced logic nodes (3nm and beyond).

- Growing demand from AI, machine learning, and high-performance computing applications.

- Emphasis on advanced materials and novel manufacturing techniques.

- Strategic partnerships and collaborations among foundries, fabless companies, and EDA tool providers.

- Development of backside power delivery networks for further density improvements.

- Integration into mobile processors, data center chips, and specialized AI accelerators.

AI Impact Analysis on Gate All Around FET Technology

Artificial Intelligence (AI) profoundly impacts the Gate All Around FET Technology market by creating an insatiable demand for processing power and energy efficiency, pushing the boundaries of semiconductor innovation. AI workloads, characterized by massive data processing and complex neural network computations, necessitate chips with higher transistor density, lower power consumption, and superior performance. GAAFETs are uniquely positioned to meet these stringent requirements, enabling the development of next-generation AI accelerators and specialized silicon for deep learning, inference, and training. Furthermore, AI and machine learning tools are increasingly being utilized in the design and optimization of GAAFETs themselves, accelerating the discovery of new architectures and improving manufacturing yields. This synergistic relationship highlights AI as both a major driver for GAAFET adoption and an enabler of its continued technological advancement, shaping future semiconductor design methodologies and market trajectories.

- AI workloads drive demand for higher transistor density and energy-efficient chips.

- GAAFETs enable superior performance for AI accelerators and specialized silicon.

- AI and machine learning tools optimize GAAFET design, simulation, and manufacturing.

- Increased investment in GAAFETs by companies developing AI-centric hardware.

- Facilitates the development of more complex neural networks and edge AI devices.

- Accelerates the transition to advanced process nodes (3nm, 2nm) for AI compute.

Key Takeaways Gate All Around FET Technology Market Size & Forecast

- The Gate All Around FET Technology market is set for robust growth, driven by an escalating demand for high-performance, energy-efficient semiconductors across various applications.

- The transition from FinFET to GAAFET is a pivotal technological shift, enabling further miniaturization and performance scaling beyond current limitations.

- Key drivers include the proliferation of AI, 5G, IoT, and high-performance computing, all requiring advanced transistor architectures.

- Significant investments in research and development by leading semiconductor foundries and design tool companies are propelling market expansion.

- Challenges such as high manufacturing costs, design complexity, and yield management are being actively addressed through innovation and collaboration.

- Opportunities lie in emerging applications like advanced automotive electronics, quantum computing, and specialized AI hardware, alongside the continuous evolution of mobile and data center segments.

- Asia Pacific is anticipated to dominate the market due to concentrated semiconductor manufacturing capabilities and a high concentration of technology adoption.

- The market's future trajectory is heavily influenced by the speed of technological maturity, standardization efforts, and the ability of the industry to manage supply chain complexities.

Gate All Around FET Technology Market Drivers Analysis

The Gate All Around FET Technology market is propelled by several potent drivers, primarily centered on the relentless pursuit of superior semiconductor performance and efficiency. The exponential growth in data generation and processing across various industries, coupled with the increasing sophistication of computational tasks, necessitates transistors that offer higher speeds, lower power consumption, and greater density than previous generations. This fundamental demand for advanced computing capabilities, driven by applications like artificial intelligence, 5G connectivity, and high-performance computing, is the primary force accelerating the adoption and development of GAAFETs. Furthermore, the inherent limitations of FinFET technology at smaller process nodes are compelling the industry to transition to GAAFETs to sustain Moore's Law and meet future performance benchmarks. These factors collectively create a strong impetus for investment and innovation in GAAFET technology, positioning it as the cornerstone for next-generation electronic devices and infrastructure.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Computing (HPC) | +1.8% | North America, Europe, Asia Pacific (China, South Korea) | Short to Medium Term (2025-2030) |

| Proliferation of Artificial Intelligence (AI) and Machine Learning (ML) | +2.1% | Global, particularly North America, Asia Pacific (China, South Korea, Japan) | Short to Long Term (2025-2033) |

| Transition to Advanced Process Nodes (3nm and below) | +1.5% | Asia Pacific (Taiwan, South Korea), North America | Medium Term (2026-2031) |

| Growing Adoption of 5G and IoT Devices | +1.3% | Global, particularly Asia Pacific, Europe | Medium to Long Term (2026-2033) |

| Need for Enhanced Power Efficiency and Miniaturization | +1.7% | Global | Short to Long Term (2025-2033) |

Gate All Around FET Technology Market Restraints Analysis

Despite its significant advantages, the Gate All Around FET Technology market faces several inherent restraints that could temper its growth trajectory. The most prominent challenge is the exceptionally high manufacturing cost associated with GAAFETs. The advanced fabrication techniques, specialized equipment, and stringent material requirements for these complex structures significantly increase the upfront capital expenditure and per-chip production costs, making them prohibitive for some applications or smaller-volume productions. Furthermore, the design complexity of GAAFETs is considerable, requiring sophisticated Electronic Design Automation (EDA) tools and highly skilled engineers. This complexity can lead to longer design cycles and increased development costs. Yield management is another critical restraint; achieving high yields for such intricate structures at early process nodes is challenging and directly impacts profitability and market readiness. These factors collectively pose significant barriers to entry and widespread adoption, requiring substantial industry investment and collaborative efforts to mitigate their impact and ensure the successful proliferation of GAAFET technology.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital Expenditure | -1.2% | Global, especially for new entrants and smaller players | Short to Medium Term (2025-2030) |

| Complex Design and Fabrication Challenges | -0.9% | Global, impacting R&D and production cycles | Short to Medium Term (2025-2030) |

| Yield Management Difficulties at Advanced Nodes | -0.8% | Global, particularly for leading foundries | Short to Medium Term (2025-2030) |

| Limited Availability of Skilled Workforce and Expertise | -0.6% | Global, but more pronounced in emerging semiconductor regions | Medium to Long Term (2027-2033) |

Gate All Around FET Technology Market Opportunities Analysis

The Gate All Around FET Technology market is brimming with promising opportunities, driven by its potential to unlock unprecedented performance and efficiency gains in the semiconductor industry. A significant opportunity lies in the burgeoning markets for specialized AI hardware, edge computing devices, and advanced automotive electronics, all of which demand highly optimized and power-efficient processors. As these sectors continue their rapid expansion, GAAFETs are uniquely positioned to serve as the foundational technology, enabling the development of more sophisticated and powerful solutions. Furthermore, the continuous advancements in manufacturing technologies, such as extreme ultraviolet (EUV) lithography, are improving the feasibility and scalability of GAAFET production, creating pathways for cost reduction and higher yields over time. The push towards chiplet architectures and heterogeneous integration also presents an opportunity, as GAAFETs can form the core of high-performance chiplets, seamlessly integrated with other specialized components. Strategic collaborations between intellectual property (IP) providers, EDA tool vendors, foundries, and fabless companies are also opening new avenues for innovation and market penetration, accelerating the widespread adoption of this advanced transistor technology.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced AI and Edge Computing Devices | +2.3% | Global, particularly North America, Asia Pacific, Europe | Short to Long Term (2025-2033) |

| Advancements in Automotive Electronics and Autonomous Driving | +1.9% | Europe, North America, Asia Pacific (Japan, South Korea, China) | Medium to Long Term (2027-2033) |

| Development of Chiplet Architectures and Heterogeneous Integration | +1.5% | Global, driven by major semiconductor innovators | Medium Term (2026-2032) |

| Increased R&D in Novel Materials and Manufacturing Processes | +1.2% | Global, focused in regions with strong semiconductor research | Long Term (2028-2033) |

| Expansion into Specialized Applications (e.g., Quantum Computing, Medical Devices) | +1.0% | North America, Europe, select regions in Asia Pacific | Long Term (2030-2033) |

Gate All Around FET Technology Market Challenges Impact Analysis

The Gate All Around FET Technology market, while promising, is not without its significant challenges that could impede widespread adoption and commercial viability. The primary hurdle is the sheer complexity and difficulty of achieving high manufacturing yields at the most advanced process nodes (3nm and below) where GAAFETs are typically implemented. The intricate stacked nanowire or nanosheet structures require extreme precision during deposition, etching, and selective removal steps, making defects more probable and reducing the number of usable chips per wafer. This directly impacts production costs and time-to-market. Additionally, the development and optimization of the necessary Electronic Design Automation (EDA) tools and Intellectual Property (IP) for GAAFET design are ongoing and represent a substantial investment challenge. Ensuring compatibility and seamless integration with existing design flows is critical. The high R&D expenditures required to push the boundaries of materials science and fabrication techniques for GAAFETs also pose a challenge, particularly for companies with limited financial resources. Furthermore, the lengthy design and validation cycles, coupled with the need for highly specialized engineering talent, can slow down the pace of innovation and market introduction. Addressing these multifaceted challenges will be crucial for the sustained growth and maturity of the GAAFET market.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving High Manufacturing Yields at Advanced Nodes | -1.5% | Global, particularly major semiconductor manufacturing hubs | Short to Medium Term (2025-2029) |

| Evolving EDA Tool Ecosystem and IP Development | -1.0% | Global, impacting design houses and foundries | Medium Term (2026-2030) |

| Stringent Metrology and Inspection Requirements | -0.8% | Global, critical for quality control | Short to Medium Term (2025-2029) |

| High Research and Development Expenditures | -0.7% | Global, affecting all industry players | Long Term (2028-2033) |

| Market Adoption Pace and Integration into Existing Systems | -0.6% | Global, impacting fabless companies and end-users | Medium to Long Term (2027-2033) |

Gate All Around FET Technology Market - Updated Report Scope

This updated report provides an in-depth analysis of the Gate All Around FET Technology market, covering historical trends, current market dynamics, and a comprehensive forecast period. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges, providing critical insights for strategic decision-making within the semiconductor industry. The scope includes detailed segmentation analysis by device type, application, end-user, and manufacturing process, along with a thorough regional breakdown to pinpoint key growth areas and competitive landscapes. The report also profiles leading market players, offering a holistic view of their strategies, product portfolios, and recent developments to understand competitive positioning and market evolution.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.35 Billion |

| Market Forecast in 2033 | USD 18.15 Billion |

| Growth Rate | 29.2% |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | TSMC, Samsung Foundry, Intel, IBM, Synopsys, Cadence Design Systems, Arm, Applied Materials, Tokyo Electron, ASML, Lam Research, GlobalFoundries, SK Hynix, Micron Technology, Qualcomm, Nvidia, AMD, Broadcom, NXP Semiconductors, Infineon Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gate All Around FET Technology market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of market dynamics, growth potential, and strategic opportunities across various industry verticals and technological applications. The core segments include the different types of GAAFET devices based on their structural innovations, the diverse applications where this advanced technology is deployed, the primary end-users driving demand, and the specific manufacturing process nodes where GAAFETs are predominantly implemented. This comprehensive breakdown facilitates precise market forecasting and strategic planning for stakeholders.- By Device Type: This segment categorizes GAAFETs based on their specific structural designs, each offering unique performance characteristics and manufacturing complexities.

- Nanowire FET: Early iteration of GAAFET, utilizing multiple nanowires for gate control.

- Nanosheet FET: An evolution offering better current drive and reduced resistance, employing wider nanosheets.

- Forksheet FET: Further optimization allowing denser packing and improved performance for future nodes.

- CFET (Complementary FET): An innovative stacking of n-type and p-type devices for ultimate density and power efficiency.

- By Application: This segmentation focuses on the key areas where GAAFET technology finds its primary usage, reflecting the demand from various industries.

- Mobile Computing: High-performance and power-efficient processors for smartphones and tablets.

- High-Performance Computing (HPC): CPUs and GPUs for data centers, supercomputers, and enterprise servers.

- Artificial Intelligence (AI) Accelerators: Specialized chips for AI training and inference workloads.

- Automotive: Advanced semiconductors for ADAS, infotainment, and autonomous driving systems.

- Internet of Things (IoT): Low-power, high-performance chips for connected devices and edge computing.

- Consumer Electronics: Components for gaming consoles, wearables, and other smart devices.

- By End-User: This segment identifies the primary entities that adopt and integrate GAAFET technology into their products or services.

- Foundries: Companies that manufacture integrated circuits for other fabless companies.

- Fabless Semiconductor Companies: Firms that design and market integrated circuits but outsource fabrication to foundries.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and market their own integrated circuits.

- By Manufacturing Process: This segmentation highlights the specific technology nodes at which GAAFETs are being fabricated, indicating the cutting edge of semiconductor production.

- 3nm Node: The initial commercialization node for GAAFETs, offering significant performance and power improvements.

- 2nm Node: The next generation, pushing further boundaries in transistor density and efficiency.

- Beyond 2nm Nodes: Represents future process nodes, including 1.8nm and smaller, which will heavily rely on advanced GAAFET derivatives and novel architectures.

Regional Highlights

The Gate All Around FET Technology market exhibits distinct regional dynamics, largely influenced by the concentration of semiconductor manufacturing, research and development capabilities, and end-user demand.- Asia Pacific (APAC): Expected to be the leading region in the Gate All Around FET Technology market, primarily driven by the presence of major foundries like TSMC (Taiwan) and Samsung Foundry (South Korea). These countries are at the forefront of advanced process technology development and mass production of cutting-edge chips. Additionally, China's aggressive investments in domestic semiconductor production and its vast market for consumer electronics and AI applications contribute significantly to regional demand. Japan and other Southeast Asian countries also play crucial roles in the supply chain, providing materials and equipment.

- North America: A significant contributor to the GAAFET market, mainly due to its robust ecosystem of fabless semiconductor companies, leading design tool providers, and substantial investments in high-performance computing and artificial intelligence research. Companies in this region drive the innovation and demand for advanced chips that leverage GAAFET technology, particularly for data centers, cloud computing, and specialized AI hardware. Government initiatives and private sector funding for domestic semiconductor manufacturing also bolster this region's importance.

- Europe: Demonstrates steady growth, propelled by its strong automotive industry and increasing focus on industrial IoT and edge computing. European countries are investing in collaborative research initiatives and strengthening their semiconductor supply chains. While not a dominant foundry region, Europe's expertise in specialized applications and design capabilities creates a significant demand for advanced, power-efficient chips, including those enabled by GAAFET technology.

- Latin America, Middle East, and Africa (MEA): These regions are emerging markets for GAAFET technology, primarily driven by the increasing adoption of digital infrastructure, smartphones, and the nascent development of AI and IoT ecosystems. While direct manufacturing is limited, the growing demand for advanced electronic devices and the establishment of local data centers contribute to the overall market expansion through consumption of GAAFET-enabled products.

Top Key Players:

The market research report covers the analysis of key stake holders of the Gate All Around FET Technology Market. Some of the leading players profiled in the report include -- TSMC

- Samsung Foundry

- Intel Corporation

- IBM

- Synopsys

- Cadence Design Systems

- Arm Holdings

- Applied Materials

- Tokyo Electron Limited

- ASML Holding NV

- Lam Research Corporation

- GlobalFoundries

- SK Hynix Inc

- Micron Technology Inc

- Qualcomm Incorporated

- Nvidia Corporation

- Advanced Micro Devices Inc

- Broadcom Inc

- NXP Semiconductors

- Infineon Technologies AG

Frequently Asked Questions:

What is Gate All Around FET (GAAFET) Technology?

Gate All Around FET (GAAFET) is a next-generation transistor architecture where the gate material surrounds the channel on all four sides. This design provides superior electrostatic control over the channel, significantly reducing leakage current and enhancing performance compared to previous FinFET (Fin Field-Effect Transistor) designs, particularly at advanced process nodes like 3nm and below.

Why is GAAFET important for future semiconductor manufacturing?

GAAFET is crucial for future semiconductor manufacturing because it allows for continued transistor scaling beyond the limits of FinFET technology. It addresses the challenges of leakage and performance degradation at smaller geometries, enabling the development of more powerful, energy-efficient, and densely packed chips essential for advancements in artificial intelligence, high-performance computing, 5G, and other demanding applications.

Which process nodes will primarily use GAAFET technology?

GAAFET technology is primarily being adopted for advanced semiconductor manufacturing process nodes, starting with 3nm, and extending to 2nm and beyond. Leading foundries are transitioning to GAAFETs at these nodes to achieve the required performance, power, and density improvements that FinFETs can no longer efficiently provide.

What are the main advantages of GAAFETs over FinFETs?

The main advantages of GAAFETs over FinFETs include superior gate control over the channel, leading to significantly reduced leakage current and improved power efficiency. GAAFETs also offer better scalability, allowing for more aggressive miniaturization and higher transistor density, which translates to enhanced performance for complex integrated circuits.

What are the key applications driving the demand for GAAFETs?

The key applications driving the demand for GAAFETs include high-performance computing (HPC) for data centers, artificial intelligence (AI) and machine learning accelerators, advanced mobile processors, autonomous driving systems, and sophisticated Internet of Things (IoT) devices. These applications require the extreme performance and power efficiency that GAAFET technology provides.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted