Cyber Insurance Market

Cyber Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701343 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Cyber Insurance Market Size

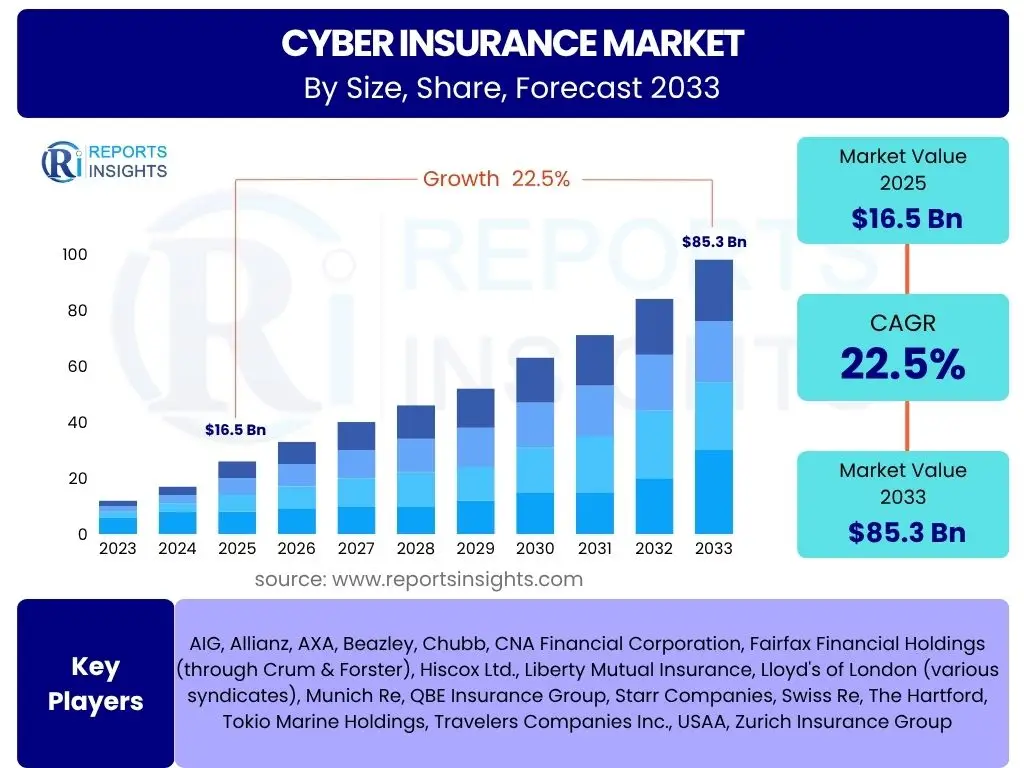

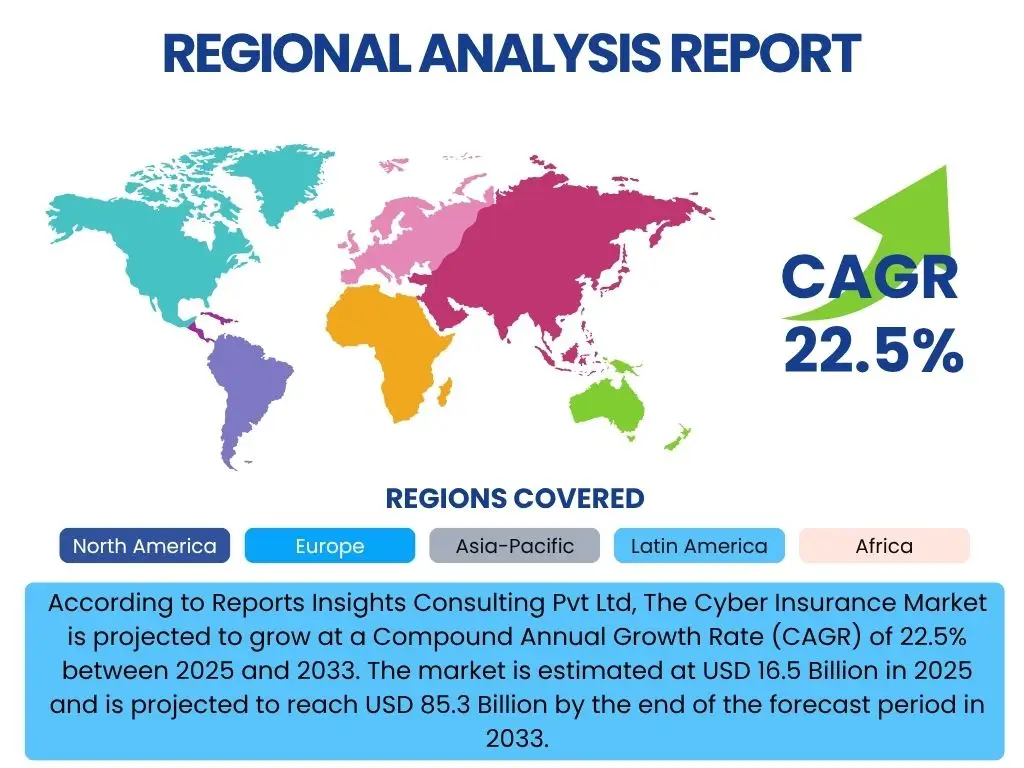

According to Reports Insights Consulting Pvt Ltd, The Cyber Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 16.5 Billion in 2025 and is projected to reach USD 85.3 Billion by the end of the forecast period in 2033.

Key Cyber Insurance Market Trends & Insights

The Cyber Insurance market is undergoing significant transformation, primarily driven by the escalating frequency and sophistication of cyber threats. Common user questions often revolve around understanding the most impactful shifts, such as the rise of ransomware, the increasing focus on supply chain vulnerabilities, and the growing demand for comprehensive, proactive risk management services. Businesses are seeking clarity on how these evolving threats translate into new policy requirements and what proactive measures are now considered standard for insurability. The market is witnessing a shift from simply indemnifying losses to encompassing a broader spectrum of services including pre-breach assessments, incident response planning, and post-incident recovery support, reflecting a more holistic approach to cyber risk management.

Another prominent trend attracting user inquiry is the impact of regulatory frameworks like GDPR, CCPA, and upcoming national cybersecurity laws, which are mandating robust data protection and breach notification protocols. This regulatory pressure is compelling organizations to seek specific coverage that addresses potential fines and legal liabilities, thereby expanding the scope and complexity of cyber insurance offerings. Furthermore, the convergence of cybersecurity solutions with insurance policies is becoming increasingly prevalent, as insurers incentivize clients to adopt advanced security measures, creating a more symbiotic relationship between risk mitigation and financial protection. This trend highlights a proactive stance within the industry, aiming to reduce the likelihood and severity of incidents rather than merely covering the aftermath.

- Escalating ransomware attacks driving demand for extortion and business interruption coverage.

- Increased focus on supply chain cyber risks and third-party vendor exposures.

- Growing integration of pre-breach services, such as risk assessments and vulnerability management, into policies.

- Regulatory mandates (e.g., GDPR, CCPA) increasing demand for compliance-related coverage.

- Emergence of specialized policies tailored for specific industry verticals and SMBs.

- Development of parametric cyber insurance policies for faster claims payout.

AI Impact Analysis on Cyber Insurance

The integration of Artificial Intelligence (AI) is profoundly reshaping the cyber insurance landscape, a topic frequently explored by users seeking to understand its benefits and challenges. Users commonly inquire about AI's role in improving risk assessment accuracy, streamlining underwriting processes, and enhancing fraud detection. AI-driven analytics can process vast amounts of data from various sources, including threat intelligence feeds, network logs, and security posture assessments, to provide a more nuanced and dynamic evaluation of an organization's cyber risk profile. This capability allows insurers to move beyond static questionnaires, enabling more precise pricing and customized policy offerings that reflect real-time threat exposure and an organization's defensive capabilities, thereby offering a competitive edge and more equitable premiums.

Beyond risk assessment, AI is poised to revolutionize claims processing and incident response. Common user concerns include how AI can accelerate claim settlements and identify emerging attack vectors. AI-powered systems can automate the initial stages of claims, verify incident details, and even suggest appropriate response strategies by analyzing historical breach data and threat patterns. Furthermore, AI tools are crucial in developing more sophisticated threat intelligence, identifying anomalies that indicate potential breaches, and predicting future attack trends. However, the adoption of AI also presents challenges, such as ensuring data privacy, addressing algorithmic bias, and establishing clear accountability for AI-driven decisions, which are critical considerations for insurers and policyholders alike to foster trust and ensure fair practices within this evolving domain.

- Enhanced risk assessment and underwriting through predictive analytics and machine learning, leading to more accurate premium pricing.

- Automated threat intelligence and vulnerability scanning for real-time risk monitoring of insured entities.

- Streamlined and accelerated claims processing by analyzing incident data and automating initial assessments.

- Improved fraud detection capabilities through pattern recognition in claim submissions and historical data.

- Development of personalized policy recommendations based on an organization's specific digital footprint and security posture.

- Potential for dynamic policy adjustments based on continuously monitored cyber risk scores.

Key Takeaways Cyber Insurance Market Size & Forecast

The trajectory of the Cyber Insurance market size and forecast underscores a period of robust and sustained growth, driven by an ever-increasing digital dependency across all sectors and the corresponding escalation in cyber threats. Key user questions frequently highlight the overall market outlook, the primary drivers sustaining this growth, and the most promising areas for future expansion. The market's significant Compound Annual Growth Rate (CAGR) to 2033 reflects a widespread realization among businesses that cyber insurance is no longer a luxury but an essential component of their overall risk management strategy. This paradigm shift is fueled by a combination of factors, including the rising financial impact of data breaches, ransomware attacks, and business interruptions, alongside stricter regulatory enforcement.

A crucial takeaway is the expanding scope of cyber insurance, moving beyond mere financial indemnification to encompass a more comprehensive suite of services that include proactive risk assessment, incident response planning, and post-breach recovery support. This evolution is vital for AEO, as users are increasingly searching for information on holistic cyber resilience. The forecast indicates substantial opportunities, particularly within the underserved Small and Medium-sized Enterprises (SME) segment and in emerging economies, where digitalization is rapidly advancing. The market is poised for innovation, with a focus on customizable policies, integration with advanced cybersecurity solutions, and the leveraging of data analytics to offer more precise and value-driven coverage, ensuring that the market continues its upward growth trajectory.

- The market is experiencing exponential growth, reflecting an urgent global need for cyber risk mitigation solutions.

- Increased awareness of financial and reputational impacts of cyber incidents is a primary growth driver.

- Significant opportunities exist in underserved segments, particularly small and medium-sized enterprises (SMEs), and emerging markets.

- The evolution of policies to include pre-breach services and advanced incident response support is crucial for market development.

- Regulatory pressure and a complex threat landscape will continue to drive demand for comprehensive coverage.

Cyber Insurance Market Drivers Analysis

The cyber insurance market's robust expansion is primarily propelled by an escalating and increasingly sophisticated cyber threat landscape. Businesses globally face an unprecedented volume of ransomware attacks, data breaches, and phishing attempts, leading to substantial financial losses and reputational damage. This heightened threat environment inherently drives organizations to seek financial protection and risk transfer mechanisms, making cyber insurance an indispensable component of their resilience strategy. The growing awareness among corporate boards and executive leadership regarding the severe consequences of cyber incidents further solidifies the demand for comprehensive cyber coverage, transitioning it from a discretionary expense to a critical operational imperative.

Complementing the threat landscape, the implementation of stringent data protection regulations across various jurisdictions significantly contributes to market growth. Laws such as the General Data Protection Regulation (GDPR) in Europe, the California Consumer Privacy Act (CCPA) in the United States, and similar frameworks worldwide impose hefty fines for non-compliance and mandate rigorous breach notification procedures. These regulatory pressures compel organizations to invest in cyber insurance to mitigate potential legal liabilities and financial penalties arising from data breaches. Furthermore, the increasing digitalization of businesses, including widespread cloud adoption and remote work models, expands the attack surface, thereby increasing inherent cyber risks and, consequently, the demand for protective insurance solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Frequency and Sophistication of Cyberattacks | +5.0% | Global | Short-term to Long-term |

| Stringent Regulatory Compliance and Data Protection Laws (e.g., GDPR, CCPA) | +4.5% | North America, Europe, Asia Pacific | Ongoing |

| Rising Awareness and Recognition of Cyber Risks by Businesses | +3.8% | Global | Mid-term |

| Increasing Digitalization and Cloud Adoption Across Industries | +3.5% | Global | Long-term |

| Growth in Supply Chain Vulnerabilities and Third-Party Risks | +3.0% | Global | Short-term to Mid-term |

Cyber Insurance Market Restraints Analysis

Despite the significant growth trajectory, the cyber insurance market faces several notable restraints that can impede its full potential. One primary challenge is the high cost of premiums, especially for Small and Medium-sized Enterprises (SMEs) and organizations with perceived higher risk profiles. Many businesses, particularly those operating on tight budgets, find the premiums prohibitive, leading to underinsurance or a complete lack of coverage. This cost barrier is often exacerbated by a lack of clarity regarding the return on investment (ROI) for cyber insurance, as the intangible benefits of risk mitigation are not always immediately apparent or quantifiable, particularly for smaller entities struggling with financial projections and resource allocation.

Another significant restraint stems from the complexity and lack of standardization within cyber insurance policies. The rapidly evolving nature of cyber threats makes it challenging for insurers to consistently define coverage terms, exclusions, and deductibles, leading to policies that can be difficult for buyers to understand and compare. This ambiguity creates uncertainty for policyholders regarding what is truly covered and can lead to disputes during claims. Furthermore, the inherent difficulty in accurately assessing and quantifying cyber risk for underwriting purposes poses a substantial challenge. Insurers often lack comprehensive historical data on cyber incidents, making predictive modeling and fair pricing intricate, which can result in overly conservative pricing or an unwillingness to cover certain high-risk sectors, thereby limiting market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Premiums and Perceived Low ROI | -3.5% | Global, particularly SMEs | Short-term to Mid-term |

| Lack of Standardized Policy Terms and Coverage Clarity | -3.0% | Global | Ongoing |

| Complexity in Underwriting and Accurate Risk Assessment Due to Evolving Threats | -2.8% | Global | Ongoing |

| Limited Historical Data for Actuarial Modeling | -2.5% | Global | Long-term |

Cyber Insurance Market Opportunities Analysis

The cyber insurance market is ripe with opportunities, primarily driven by the vast, underserved Small and Medium-sized Enterprise (SME) segment. While large corporations often have dedicated risk management teams and robust cybersecurity budgets, SMEs frequently lack both, making them highly vulnerable to cyberattacks and thus prime candidates for cyber insurance. Tailoring simplified, affordable, and easily accessible policies specifically for the unique needs of SMEs represents a substantial growth avenue for insurers. Developing bundled solutions that combine basic cyber coverage with essential cybersecurity services could further entice this segment, bridging the gap between risk transfer and proactive protection.

Another significant opportunity lies in the continuous innovation and diversification of cyber insurance products. As the threat landscape evolves, so too must the insurance offerings. This includes the development of highly specialized policies for emerging technologies like IoT, operational technology (OT) in industrial control systems, and artificial intelligence (AI) liabilities. Furthermore, the introduction of parametric insurance, where payouts are triggered by predefined events (e.g., specific downtime duration following an attack) rather than traditional loss assessment, offers the potential for faster claims settlement and greater transparency, appealing to businesses seeking rapid recovery. Expansion into developing economies, where digital transformation is accelerating but cyber defenses are still nascent, also presents immense long-term growth prospects, requiring localized understanding and innovative distribution channels.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Small and Medium-sized Enterprise (SME) Market | +4.0% | Global | Mid-term to Long-term |

| Development of Specialized and Parametric Insurance Products | +3.5% | North America, Europe, Asia Pacific | Mid-term |

| Expansion into Emerging Economies with Rapid Digitalization | +3.2% | Asia Pacific, Latin America, MEA | Long-term |

| Integration of Cyber Insurance with Cybersecurity Services and Solutions | +3.0% | Global | Mid-term |

| Leveraging Data Analytics and AI for Enhanced Risk Prediction and Customization | +2.8% | Global | Long-term |

Cyber Insurance Market Challenges Impact Analysis

The cyber insurance market faces significant challenges primarily due to the extraordinarily dynamic and unpredictable nature of cyber threats. Unlike traditional insurance risks which are relatively stable, cyber vulnerabilities and attack methodologies evolve at an alarming pace, making it difficult for insurers to accurately assess and price risk over the long term. This rapid evolution means that policies written today may become quickly outdated in their scope and coverage tomorrow, creating an ongoing need for policy adaptation and re-evaluation. Furthermore, the global and borderless nature of cyberattacks complicates traditional geographic risk diversification, as a single large-scale event can impact numerous policyholders across different regions simultaneously, posing systemic risk challenges for insurers.

Another profound challenge lies in the scarcity of reliable historical data needed for robust actuarial modeling. Given the relatively nascent stage of the cyber insurance market compared to other insurance lines, and the reluctance of organizations to disclose breach details due to reputational concerns, insurers often operate with insufficient data to precisely quantify exposure, predict loss frequencies, or establish appropriate reserves. This data gap can lead to either overly conservative pricing, deterring potential buyers, or insufficient pricing, exposing insurers to unexpected losses. Additionally, the talent gap in specialized cyber insurance underwriting and claims management further exacerbates these issues, as there is a limited pool of professionals with the dual expertise in both cybersecurity and insurance principles required to navigate this complex domain effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Unpredictable Cyber Threat Landscape | -4.0% | Global | Ongoing |

| Scarcity of Comprehensive Historical Data for Accurate Risk Modeling | -3.5% | Global | Ongoing |

| Talent Shortage in Cyber Underwriting and Claims Management | -3.0% | Global | Mid-term |

| Potential for Systemic Risk and Accumulation of Losses from Widespread Attacks | -2.8% | Global | Long-term |

| Ensuring Policyholder Adherence to Cybersecurity Best Practices | -2.5% | Global | Ongoing |

Cyber Insurance Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Cyber Insurance Market, covering key aspects such as market size, growth trends, drivers, restraints, opportunities, and challenges influencing its trajectory from 2025 to 2033. The report offers detailed segmentation analysis across various dimensions, alongside regional insights and profiles of leading market players, ensuring a holistic understanding of the market dynamics and future outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 16.5 Billion |

| Market Forecast in 2033 | USD 85.3 Billion |

| Growth Rate | 22.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AIG, Allianz, AXA, Beazley, Chubb, CNA Financial Corporation, Fairfax Financial Holdings (through Crum & Forster), Hiscox Ltd., Liberty Mutual Insurance, Lloyd's of London (various syndicates), Munich Re, QBE Insurance Group, Starr Companies, Swiss Re, The Hartford, Tokio Marine Holdings, Travelers Companies Inc., USAA, Zurich Insurance Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cyber Insurance market is extensively segmented to provide a granular understanding of its diverse components and how various factors influence demand and supply. This segmentation helps stakeholders to identify specific market niches, understand varied customer needs, and develop targeted strategies and tailored insurance products. The market is primarily broken down by the type of coverage offered, addressing different facets of cyber risk, which allows businesses to select policies that align with their specific operational vulnerabilities and regulatory obligations. The distinction between first-party and third-party coverages is crucial, as the former deals with direct losses to the insured, while the latter addresses liabilities to external entities.

Further segmentation by enterprise size (SMEs versus Large Enterprises) highlights the vastly different risk profiles, budget constraints, and compliance requirements across organizations of varying scales. This categorization is vital for insurers to design cost-effective and relevant policies for the highly sensitive but often underserved SME segment, which typically lacks dedicated cybersecurity resources. Segmentation by industry vertical (such as BFSI, Healthcare, IT & Telecom, Retail, and Manufacturing) recognizes that each sector faces unique cyber threats and regulatory mandates, necessitating specialized insurance solutions. For instance, healthcare faces strict HIPAA compliance, while BFSI is concerned with financial fraud and data integrity. Lastly, the market is segmented by distribution channel, which illuminates how policies are sold and delivered, from traditional brokers and agents to direct sales and emerging digital platforms, indicating evolving customer preferences and market access strategies.

- By Coverage Type:

- Data Breach Coverage (e.g., notification costs, credit monitoring, forensic investigation)

- Network Security Coverage (e.g., cyber extortion, denial-of-service attacks, malware)

- Business Interruption Coverage (e.g., loss of income, extra expenses due to system downtime)

- Media Liability Coverage (e.g., copyright infringement, defamation related to online content)

- Regulatory & Compliance Coverage (e.g., fines, penalties)

- Extortion Coverage (e.g., ransom payment, investigation costs)

- Funds Transfer Fraud Coverage (e.g., social engineering, phishing scams leading to fraudulent transfers)

- By Enterprise Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical:

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- IT and Telecom

- Retail and E-commerce

- Manufacturing

- Government & Public Sector

- Energy & Utilities

- Other Verticals (e.g., Education, Media, Legal)

- By Distribution Channel:

- Brokers

- Agents

- Direct Sales

- Bancassurance

Regional Highlights

- North America: Dominates the global cyber insurance market, driven by stringent regulatory frameworks (e.g., CCPA, state-specific breach notification laws), a high incidence of sophisticated cyberattacks, and a strong awareness among businesses about the financial and reputational impacts of breaches. The U.S. and Canada are leading adopters, with a mature market offering a wide range of specialized policies and advanced underwriting practices.

- Europe: Exhibits significant growth, largely propelled by the General Data Protection Regulation (GDPR), which mandates robust data protection and imposes substantial penalties for non-compliance. Increased digitalization across industries and a rising number of cyber threats, particularly ransomware, are further stimulating market expansion. Countries like the UK, Germany, and France are key contributors to market development.

- Asia Pacific (APAC): Positioned as the fastest-growing region, fueled by rapid digital transformation, increasing internet penetration, and the burgeoning adoption of cloud technologies across countries like China, India, Japan, and Australia. While the market is relatively nascent compared to North America and Europe, growing awareness of cyber risks and the development of local data protection laws are accelerating the demand for cyber insurance solutions.

- Latin America: Represents an emerging market for cyber insurance, with increasing digitalization initiatives and a growing recognition of cyber threats. Brazil, Mexico, and Argentina are key countries showing increased interest, though market development is still challenged by economic volatility and varying levels of cybersecurity maturity and regulatory frameworks.

- Middle East and Africa (MEA): A nascent but promising market, driven by governmental digital transformation agendas and diversifying economies. The region is witnessing an increase in cyberattacks, prompting organizations to seek insurance coverage. However, challenges such as lower cybersecurity maturity and evolving regulatory landscapes contribute to slower adoption compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cyber Insurance Market.- AIG

- Allianz

- AXA

- Beazley

- Chubb

- CNA Financial Corporation

- Fairfax Financial Holdings (through Crum & Forster)

- Hiscox Ltd.

- Liberty Mutual Insurance

- Lloyd's of London (various syndicates)

- Munich Re

- QBE Insurance Group

- Starr Companies

- Swiss Re

- The Hartford

- Tokio Marine Holdings

- Travelers Companies Inc.

- USAA

- Zurich Insurance Group

Frequently Asked Questions

Analyze common user questions about the Cyber Insurance market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is cyber insurance and why is it essential for businesses?

Cyber insurance, also known as cybersecurity insurance or cyber liability insurance, is a specialized policy designed to protect businesses from financial losses and damages resulting from cyber incidents such as data breaches, ransomware attacks, and network outages. It is essential because it helps cover the significant costs associated with these events, including legal fees, regulatory fines, public relations expenses, and business interruption losses, providing a critical layer of financial protection in an increasingly digital and threat-prone landscape.

What does a typical cyber insurance policy cover?

A typical cyber insurance policy provides comprehensive coverage for both first-party and third-party costs. First-party coverage includes expenses directly incurred by the insured, such as forensic investigation, data restoration, business interruption losses, cyber extortion payments, and public relations costs. Third-party coverage addresses liabilities to external entities, including legal defense costs, settlements, regulatory fines, and damages for privacy breaches or network security failures involving customer data. Coverage specifics vary by policy, making a detailed review crucial.

How are cyber insurance premiums determined?

Cyber insurance premiums are determined by several factors that reflect an organization's specific risk profile and security posture. Key considerations include the industry sector (e.g., healthcare, finance), company size and revenue, the volume and sensitivity of data handled, existing cybersecurity measures (e.g., firewalls, encryption, employee training, incident response plans), claims history, and the desired coverage limits and deductibles. Insurers often conduct thorough assessments of an applicant's IT infrastructure and security practices to accurately price the risk.

Can cyber insurance help with ransomware attacks?

Yes, cyber insurance policies are increasingly designed to provide significant support during ransomware attacks. Coverage typically includes the costs associated with responding to and recovering from ransomware, such as payment of the ransom (if agreed upon with the insurer), forensic investigation to determine the attack's scope, data restoration and recovery efforts, business interruption losses due to downtime, and potential legal or public relations expenses stemming from the incident. Many policies also offer access to expert incident response teams.

How can organizations reduce their cyber insurance costs?

Organizations can reduce cyber insurance costs by implementing robust cybersecurity best practices and demonstrating a proactive approach to risk management. This includes deploying advanced security technologies like multi-factor authentication and endpoint detection and response, regularly updating software, conducting employee cybersecurity training, performing frequent vulnerability assessments and penetration testing, having a well-defined incident response plan, and maintaining strong data backup and recovery protocols. A strong security posture signals lower risk to insurers, leading to more favorable premiums.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted