Mobile Phone Insurance Market

Mobile Phone Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705449 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

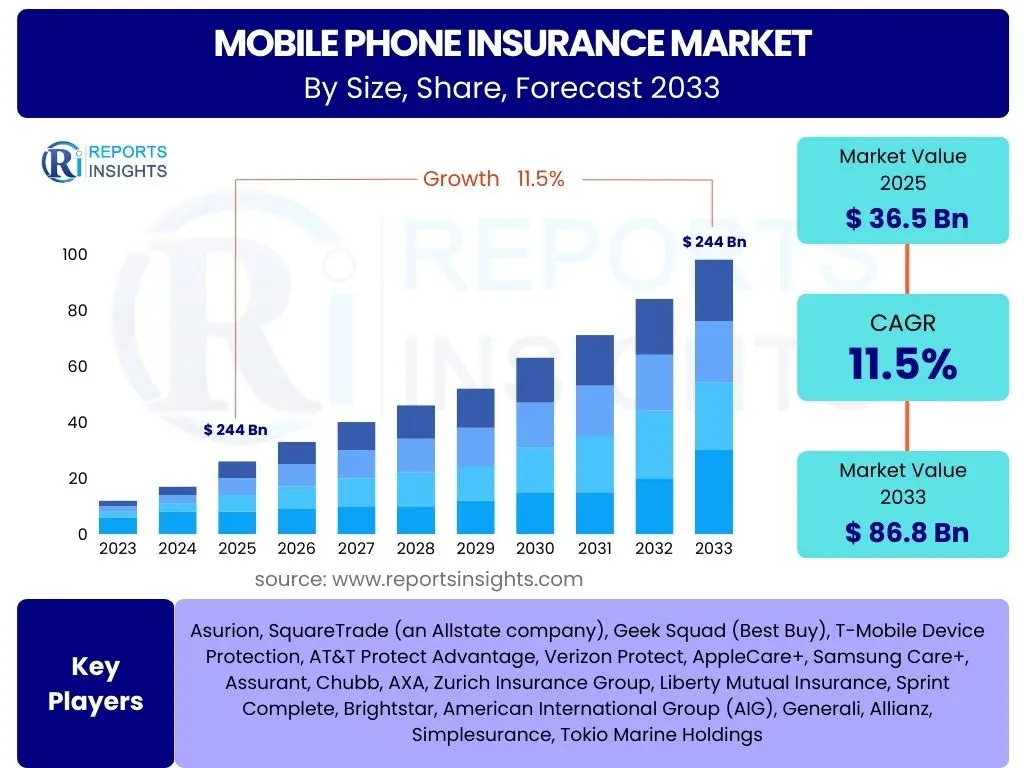

Mobile Phone Insurance Market Size

According to Reports Insights Consulting Pvt Ltd, The Mobile Phone Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 36.5 billion in 2025 and is projected to reach USD 86.8 billion by the end of the forecast period in 2033.

Key Mobile Phone Insurance Market Trends & Insights

User inquiries frequently focus on the evolving landscape of mobile phone insurance, seeking to understand the primary forces shaping its growth and adoption. Common questions revolve around the increasing sophistication of mobile devices, which often come with higher price tags, making their protection more critical. Additionally, consumers are keenly interested in how insurance offerings are adapting to new device features, changing ownership models, and the demand for more flexible and transparent coverage options. The shift towards bundled services and subscription-based models is also a recurring theme, highlighting a desire for convenience and integrated solutions that go beyond traditional break-fix policies.

Another area of significant user interest concerns the impact of digitalization and enhanced customer experience on the insurance sector. Users are looking for insights into how technology is simplifying the claims process, personalizing policy offerings, and improving overall customer engagement. There is a clear trend towards preventative measures and value-added services, such as data recovery, cybersecurity protection, and technical support, which are increasingly being sought alongside standard damage coverage. This indicates a market moving beyond simple replacement policies to comprehensive digital device protection ecosystems, driven by consumer expectations for seamless, end-to-end device management solutions.

- Rising average selling price (ASP) of smartphones, increasing replacement costs.

- Growing consumer awareness regarding device protection and cybersecurity risks.

- Shift towards bundled insurance offerings with device purchases or network plans.

- Adoption of subscription-based insurance models for enhanced flexibility.

- Integration of advanced technologies for quicker claims processing and fraud detection.

- Demand for comprehensive coverage including accidental damage, theft, loss, and technical support.

- Expansion of global smartphone penetration, particularly in emerging markets.

AI Impact Analysis on Mobile Phone Insurance

User questions regarding the impact of Artificial Intelligence (AI) on mobile phone insurance often center on efficiency, personalization, and risk assessment. Consumers and industry stakeholders are eager to understand how AI can streamline the claims process, moving away from manual, time-consuming assessments to automated, rapid evaluations. Concerns are also raised about AI's potential to personalize insurance premiums and policy terms based on individual user behavior and device usage patterns, questioning the balance between tailored services and privacy implications. The expectation is that AI will enhance speed and accuracy in claims, but there is also curiosity about its role in predictive analytics for fraud detection and proactive risk management.

Furthermore, discussions frequently explore AI's contribution to improving customer service and engagement within the mobile phone insurance sector. Users envision AI-powered chatbots and virtual assistants providing instant policy information, guiding through claims initiation, and resolving common queries, thereby enhancing the overall customer experience. There's also an interest in how AI can analyze vast datasets to identify emerging trends in device damage or loss, allowing insurers to develop more responsive and competitive products. The underlying theme is a desire for a more intelligent, responsive, and user-centric insurance ecosystem, leveraging AI to transform traditional operational models and deliver superior value to policyholders.

- Automated claims processing through AI-powered image recognition and damage assessment, reducing processing time.

- Enhanced fraud detection capabilities utilizing machine learning algorithms to identify suspicious claim patterns.

- Personalized premium pricing and policy recommendations based on user behavior and device history.

- AI-driven chatbots and virtual assistants for instant customer support and claims initiation, improving user experience.

- Predictive analytics for risk assessment, allowing insurers to anticipate potential issues and offer proactive solutions.

- Streamlined underwriting processes with AI evaluating customer data for faster policy issuance.

- Development of new, usage-based insurance products enabled by AI's data analysis capabilities.

Key Takeaways Mobile Phone Insurance Market Size & Forecast

User inquiries about the key takeaways from the mobile phone insurance market size and forecast consistently point to an underlying interest in the market's robust growth trajectory and its resilience. There is a strong emphasis on understanding the primary drivers behind the projected expansion, such as the increasing global adoption of premium smartphones and the rising cost of device repairs or replacements. Users want to discern if the market is stable for investment and if there are significant opportunities for new entrants or existing players to innovate. The recurring theme is a quest for clarity on the market's future potential and the essential factors that will contribute to its continued upward trend over the forecast period.

Furthermore, there is significant interest in the strategic implications of the market forecast, particularly concerning segmentation and regional performance. Users frequently ask about which types of coverage or distribution channels are expected to exhibit the strongest growth and which geographical areas will lead the market. They are also keen to identify any potential shifts in consumer behavior or technological advancements that might alter the forecast. The aim is to gain a concise, actionable understanding of the market's most critical characteristics, enabling stakeholders to make informed decisions regarding product development, market entry, and strategic partnerships, ultimately leveraging the identified growth opportunities effectively.

- The market is poised for significant expansion, driven by high smartphone penetration and increasing device value.

- Technological integration, particularly AI, will be crucial for efficiency and customer experience.

- Emerging markets offer substantial untapped growth potential.

- Comprehensive and bundled policies are gaining traction over basic coverage.

- Customer retention strategies and seamless claims processes are critical for market leadership.

Mobile Phone Insurance Market Drivers Analysis

The increasing average selling price (ASP) of smartphones globally is a primary driver for the mobile phone insurance market. As mobile devices become more technologically advanced, featuring sophisticated cameras, processors, and display technologies, their retail prices have surged. This elevation in device cost makes consumers more inclined to protect their substantial investment against accidental damage, theft, or loss. The perceived financial risk associated with replacing a high-value smartphone often outweighs the annual insurance premium, thus stimulating demand for robust protection plans. This trend is particularly pronounced in developed economies where premium smartphone adoption is widespread, but it is rapidly expanding into developing regions as affordability improves and consumer aspirations rise.

Another significant driver is the growing consumer awareness regarding the necessity of device protection and the financial burden of unexpected repairs or replacements. Marketing efforts by mobile network operators, retailers, and insurance providers have played a crucial role in educating consumers about the benefits of insurance. Furthermore, the prevalence of smartphone accidents, such as screen cracks, liquid damage, or theft, is a common occurrence, making the perceived need for insurance tangible for many users. The convenience of having a device repaired or replaced quickly through an insurance policy, rather than incurring significant out-of-pocket expenses or being without a device for an extended period, significantly contributes to the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Average Selling Price of Smartphones | +1.8% | Global, particularly North America, Europe, APAC | Short to Mid-term (2025-2030) |

| Rising Smartphone Penetration in Emerging Markets | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Growing Incidences of Accidental Damage and Theft | +1.2% | Global | Short to Long-term (2025-2033) |

| Demand for Comprehensive Coverage and Value-Added Services | +1.0% | North America, Europe, Developed APAC | Mid-term (2026-2031) |

| Bundling of Insurance with Device Sales and Network Plans | +0.9% | Global | Short to Mid-term (2025-2030) |

Mobile Phone Insurance Market Restraints Analysis

One significant restraint impacting the mobile phone insurance market is the perception of high premiums relative to the perceived value of coverage, especially for mid-range or older devices. Consumers often weigh the annual cost of insurance against the depreciating value of their smartphone and the likelihood of making a claim. If the premium approaches a significant percentage of the device's original cost, or if deductibles are high, many users opt to forgo insurance, particularly as their device ages. This cost-benefit analysis often leads to a segment of the market choosing self-insurance or relying on manufacturer warranties for limited periods, thus limiting the overall market penetration of dedicated insurance policies.

Another challenge stems from the complexity and lack of transparency in policy terms and conditions. Consumers frequently express confusion regarding what is covered, what constitutes an eligible claim, and the process for filing one. Exclusions for certain types of damage, specific clauses regarding loss or theft, and the varying deductible amounts can deter potential customers. This lack of clarity can lead to customer dissatisfaction and a general distrust of insurance products, making it difficult for providers to expand their customer base. Simplifying policy language, increasing transparency, and offering flexible, understandable coverage options are crucial for overcoming this restraint.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Premium Costs and Deductibles | -1.5% | Global, particularly price-sensitive markets | Short to Long-term (2025-2033) |

| Lack of Awareness and Understanding of Policy Terms | -1.3% | Emerging Markets, segments with lower digital literacy | Short to Mid-term (2025-2030) |

| Manufacturer Warranties and Extended Service Plans | -1.0% | Global, particularly for new devices | Short-term (2025-2027) |

| Perceived Low Likelihood of Claiming for Minor Damages | -0.8% | Developed Markets | Short to Mid-term (2025-2030) |

| Complex Claims Process and Customer Dissatisfaction | -0.7% | Global | Mid-term (2026-2031) |

Mobile Phone Insurance Market Opportunities Analysis

The rapid advancement in smartphone technology, including the introduction of foldable phones, augmented reality capabilities, and specialized features, presents a significant opportunity for the mobile phone insurance market. These innovative devices often come with significantly higher price points and more delicate components, making them more vulnerable to damage and more expensive to repair. Insurance providers can capitalize on this by developing tailored policies specifically designed for these high-end, complex devices, offering specialized coverage for their unique characteristics and higher repair costs. This niche market segment, driven by early adopters and tech enthusiasts, represents a premium opportunity for insurers to offer value-added protection plans that justify higher premiums, aligning with the advanced nature of the devices.

Furthermore, the expansion of smartphone penetration into emerging and underserved markets offers vast growth opportunities. As disposable incomes rise and access to affordable smartphones increases in regions such as Southeast Asia, Latin America, and Africa, a new demographic of first-time smartphone owners emerges. Many of these consumers may lack established financial safety nets or easy access to repair services, making insurance an appealing proposition. Insurers can develop simplified, micro-insurance products or pay-as-you-go models that cater to the specific economic conditions and needs of these populations, fostering long-term customer relationships and tapping into previously unaddressed market segments. Strategic partnerships with local mobile operators and retailers will be key to unlocking this potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Policies for High-End and Innovative Devices | +1.7% | Developed Markets (North America, Europe, East Asia) | Short to Mid-term (2025-2030) |

| Expansion into Emerging and Underserved Markets | +1.6% | Asia Pacific (excl. China/Japan), Latin America, MEA | Mid to Long-term (2027-2033) |

| Integration of Value-Added Services (e.g., Cybersecurity, Data Recovery) | +1.4% | Global, particularly privacy-conscious regions | Mid-term (2026-2031) |

| Leveraging AI and Big Data for Personalized Offers and Claims | +1.2% | Global | Short to Long-term (2025-2033) |

| Partnerships with Mobile Network Operators and Device Manufacturers | +1.0% | Global | Short to Mid-term (2025-2030) |

Mobile Phone Insurance Market Challenges Impact Analysis

One significant challenge for the mobile phone insurance market is the issue of fraud and moral hazard. The high value of claims, especially for total loss or theft, can incentivize fraudulent activities, leading to inflated repair costs or staged incidents. Detecting and preventing such fraud requires sophisticated analytical tools and robust verification processes, which add operational complexity and cost for insurers. The ease with which mobile devices can be reported lost or stolen, combined with the difficulty in proving the veracity of such claims, puts pressure on insurers to maintain a delicate balance between efficient claims processing and stringent fraud detection. This challenge can erode profitability and increase premiums for legitimate policyholders if not effectively managed.

Another substantial challenge stems from intense market competition and price sensitivity. The market features a diverse range of players, including traditional insurers, mobile network operators, device manufacturers, and specialized third-party providers, all vying for market share. This competitive landscape often leads to price wars, forcing premiums down and squeezing profit margins. Consumers, particularly in developed markets, are highly price-sensitive and compare offerings extensively, making it difficult for providers to differentiate solely on price. The commoditization of basic insurance policies necessitates innovation in terms of service quality, policy flexibility, and value-added features to stand out in a crowded market, placing continuous pressure on providers to evolve their offerings.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Fraud and Moral Hazard | -1.8% | Global | Short to Long-term (2025-2033) |

| Intense Market Competition and Price Sensitivity | -1.5% | Developed Markets (North America, Europe, East Asia) | Short to Long-term (2025-2033) |

| Rapid Technological Obsolescence of Devices | -1.2% | Global | Short to Mid-term (2025-2030) |

| Maintaining Profitability Amidst High Repair/Replacement Costs | -1.0% | Global | Short to Mid-term (2025-2030) |

| Regulatory Compliance and Data Privacy Concerns | -0.9% | Europe (GDPR), North America, APAC | Long-term (2028-2033) |

Mobile Phone Insurance Market - Updated Report Scope

This report provides a comprehensive analysis of the mobile phone insurance market, covering historical performance, current market dynamics, and future projections from 2025 to 2033. It delves into critical market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope encompasses detailed segmentation analysis by coverage type, distribution channel, device type, and pricing model, alongside regional insights across major global geographies. Furthermore, the report assesses the competitive landscape, profiling key market players and their strategic initiatives, offering a holistic view for stakeholders seeking to understand and capitalize on market growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 36.5 billion |

| Market Forecast in 2033 | USD 86.8 billion |

| Growth Rate | 11.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Asurion, SquareTrade (an Allstate company), Geek Squad (Best Buy), T-Mobile Device Protection, AT&T Protect Advantage, Verizon Protect, AppleCare+, Samsung Care+, Assurant, Chubb, AXA, Zurich Insurance Group, Liberty Mutual Insurance, Sprint Complete, Brightstar, American International Group (AIG), Generali, Allianz, Simplesurance, Tokio Marine Holdings |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The mobile phone insurance market is meticulously segmented to provide a granular understanding of consumer preferences, distribution dynamics, and product offerings. This segmentation allows for targeted analysis of various market niches, revealing distinct growth patterns and competitive landscapes within each category. Understanding these segments is crucial for stakeholders to tailor their product development, marketing strategies, and distribution networks effectively, ensuring that offerings align with specific consumer needs and market opportunities. The diverse segments reflect the evolving nature of mobile device ownership and the varied approaches consumers take to protect their valuable investments.

Further analysis within these segments uncovers trends such as the increasing demand for comprehensive coverage that extends beyond basic physical damage to include cyber protection and data recovery, driven by the growing reliance on smartphones for personal and professional activities. The shifting landscape of distribution channels, with a notable rise in online sales and direct-to-consumer models, also highlights the importance of digital presence and seamless customer journeys. Moreover, the distinction between new and refurbished device insurance indicates different risk profiles and price sensitivities, necessitating varied actuarial approaches. Overall, this detailed segmentation provides a roadmap for navigating the complexities of the mobile phone insurance ecosystem and identifying areas for strategic expansion and innovation.

- By Coverage Type: This segment includes policies for physical damage (accidental, liquid, screen), theft & loss, extended warranty, and other value-added services such as cybersecurity and data recovery. Physical damage remains the most common claim, while demand for comprehensive protection covering digital risks is increasing.

- By Distribution Channel: Key channels include mobile network operators (MNOs), device manufacturers, retailers, traditional insurance providers (direct or via brokers/agents), and dedicated online platforms. MNOs and retailers historically dominate due to point-of-sale integration, but online channels are gaining significant traction.

- By Device Type: Differentiates between insurance for new devices and refurbished devices. Insurance for new, high-value smartphones typically offers broader coverage, while policies for refurbished devices often focus on functionality protection and are more price-sensitive.

- By Pricing Model: This segment categorizes offerings into monthly subscription plans, annual plans, and single premium payments. Monthly subscriptions offer flexibility and are increasingly preferred by consumers, aligning with modern service consumption patterns.

Regional Highlights

- North America: North America represents a mature and significant market for mobile phone insurance, driven by high smartphone penetration rates, consumer propensity for purchasing premium devices, and a robust insurance industry infrastructure. The region benefits from strong partnerships between mobile network operators, device manufacturers, and insurance providers, leading to high attachment rates of insurance at the point of sale. Consumers in North America are increasingly seeking comprehensive coverage that includes accidental damage, theft, and value-added services like cybersecurity protection and technical support. The market is also characterized by strong brand loyalty and a competitive landscape that encourages continuous innovation in policy offerings and customer service. Urbanization and higher disposable incomes further contribute to the region's market dominance.

- Europe: Europe exhibits a diverse mobile phone insurance market, influenced by varying regulatory landscapes, consumer preferences, and economic conditions across countries. Western European countries like the UK, Germany, and France are leading contributors due to high smartphone adoption and a strong awareness of device protection. The market here is characterized by a mix of direct insurance sales, partnerships with mobile operators, and a growing emphasis on digital channels for policy purchase and claims management. Eastern European countries are experiencing rapid growth as smartphone penetration increases and consumers become more affluent. The region also sees a strong trend towards sustainable practices, leading to increased interest in repair-focused policies and refurbished device insurance.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market, primarily due to the massive and expanding smartphone user base, particularly in emerging economies like India, Indonesia, and Vietnam. While overall market penetration for insurance might be lower compared to Western counterparts, the sheer volume of new smartphone sales and increasing disposable incomes present immense opportunities. China and Japan are highly developed markets within APAC, characterized by advanced insurance solutions and tech-savvy consumers. The region is seeing a rapid shift towards online insurance platforms and mobile-first strategies to reach a vast, digitally connected population. Challenges include price sensitivity and varying levels of consumer awareness, necessitating localized and affordable insurance solutions.

- Latin America: Latin America is an emerging market for mobile phone insurance, driven by increasing smartphone adoption and rising awareness of device protection in countries like Brazil, Mexico, and Argentina. The region faces challenges such as high rates of device theft and economic volatility, which paradoxically also drive the need for insurance. The market is often characterized by a focus on basic coverage for theft and accidental damage, with a growing interest in more comprehensive plans as economies stabilize. Distribution is heavily reliant on mobile network operators and large retailers, who are key in educating consumers and integrating insurance offerings into device sales. Digital payment solutions and accessible policy terms are crucial for market expansion.

- Middle East and Africa (MEA): The MEA region represents a nascent but rapidly growing market for mobile phone insurance, propelled by surging smartphone penetration, particularly in the Gulf Cooperation Council (GCC) countries and parts of Africa. Urbanization and a young, tech-savvy population are significant growth factors. While premium device sales drive demand for insurance in the GCC, affordability and basic coverage remain key considerations in many African countries. The market is characterized by a high incidence of theft in some areas, which underscores the demand for protective policies. Partnerships between local insurers, mobile operators, and international providers are crucial for developing relevant products and expanding reach within this diverse region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mobile Phone Insurance Market.- Asurion

- SquareTrade (an Allstate company)

- Geek Squad (Best Buy)

- T-Mobile Device Protection

- AT&T Protect Advantage

- Verizon Protect

- AppleCare+

- Samsung Care+

- Assurant

- Chubb

- AXA

- Zurich Insurance Group

- Liberty Mutual Insurance

- Sprint Complete

- Brightstar

- American International Group (AIG)

- Generali

- Allianz

- Simplesurance

- Tokio Marine Holdings

Frequently Asked Questions

Analyze common user questions about the Mobile Phone Insurance market and generate a concise list of summarized FAQs reflecting key topics and concerns.What types of coverage are typically included in mobile phone insurance?

Mobile phone insurance generally covers accidental damage (e.g., screen cracks, liquid damage), theft, and loss. Many policies also offer extended warranty beyond the manufacturer's guarantee, and some comprehensive plans include protection against cybersecurity threats, data recovery, and technical support services.

How do I purchase mobile phone insurance?

Mobile phone insurance can be purchased through various channels including your mobile network operator, directly from the device manufacturer, at retail stores where you buy your phone, through independent insurance providers, or via online insurance platforms. Many options allow for immediate coverage upon device purchase.

Is mobile phone insurance worth the cost?

The value of mobile phone insurance depends on your device's cost, your personal risk tolerance, and your ability to afford replacement or repair out-of-pocket. For high-value smartphones, insurance can provide significant financial protection against costly repairs or complete loss, often proving worthwhile for peace of mind.

How does the claims process work for mobile phone insurance?

The claims process typically involves reporting the incident to your insurer, often online or via phone. You will usually need to provide details of the incident, proof of ownership, and potentially a police report for theft. After approval, the insurer will arrange for repair, replacement, or provide a cash settlement, often after a deductible is paid.

What is the impact of AI on mobile phone insurance?

AI is transforming mobile phone insurance by automating claims processing, enhancing fraud detection through sophisticated algorithms, and enabling personalized policy recommendations. It also improves customer service through AI-powered chatbots and provides predictive analytics for more accurate risk assessment and pricing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted