Opto Electronic Packaging Market

Opto Electronic Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701363 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Opto Electronic Packaging Market Size

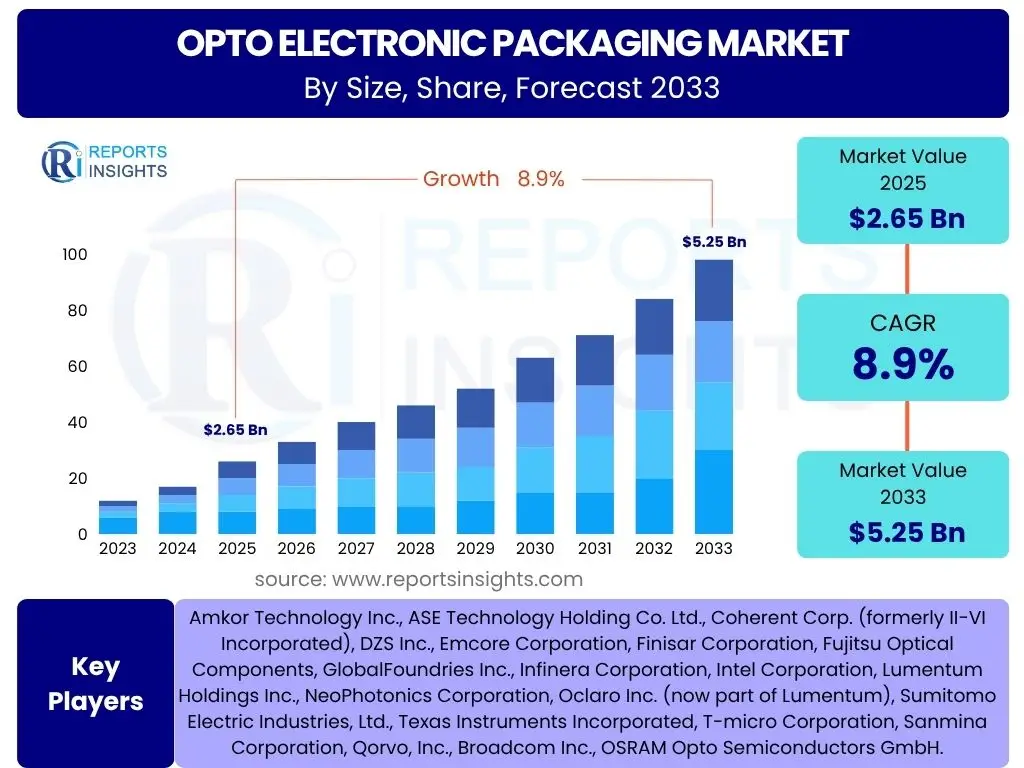

According to Reports Insights Consulting Pvt Ltd, The Opto Electronic Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. This robust growth is primarily driven by the escalating demand for high-speed data communication technologies, the widespread adoption of advanced sensing solutions across various industries, and continuous innovations in miniaturization and integration techniques within the optoelectronics sector. The market's expansion reflects the critical role opto-electronic components play in next-generation communication networks, consumer electronics, and automotive systems.

The market is estimated at USD 2.65 Billion in 2025 and is projected to reach USD 5.25 Billion by the end of the forecast period in 2033. This significant increase underscores the expanding applications of opto-electronic devices, ranging from fiber optic communications and data centers to advanced driver-assistance systems (ADAS) and medical imaging. The intricate requirements for robust protection, efficient heat dissipation, and precise optical alignment of these delicate components necessitate sophisticated packaging solutions, fueling market growth across diverse end-use industries globally.

Key Opto Electronic Packaging Market Trends & Insights

The Opto Electronic Packaging market is currently experiencing dynamic shifts, driven by technological advancements and evolving application demands. Common user inquiries often revolve around the push for increased integration, the development of new materials for enhanced performance, and the critical need for effective thermal management solutions in high-power optical devices. There is also significant interest in how packaging innovations are enabling smaller form factors and higher bandwidth capabilities, essential for emerging technologies like 5G, Artificial Intelligence (AI), and the Internet of Things (IoT).

Users are keen to understand the shift towards more cost-effective and scalable packaging processes, alongside the challenges associated with achieving hermeticity and reliability for sensitive opto-electronic components. The integration of photonics with electronics, often referred to as 'photonic integration,' is another area of intense focus, highlighting the industry's move towards higher levels of functional density and performance. These trends collectively shape the landscape of opto-electronic packaging, influencing research and development efforts and investment strategies across the value chain.

- Miniaturization and High-Density Integration: The continuous demand for smaller, lighter, and more powerful devices drives the need for ultra-compact packaging solutions and advanced integration techniques like 3D stacking and chip-on-board (COB) assembly.

- Advanced Thermal Management: High-power opto-electronic devices generate significant heat, making efficient thermal dissipation a critical packaging requirement, leading to the development of novel heat sinks, thermal interface materials, and advanced cooling designs.

- Silicon Photonics Integration: The convergence of optics and electronics on a single silicon chip is a transformative trend, reducing manufacturing costs, increasing bandwidth, and enabling new applications by leveraging existing semiconductor fabrication infrastructure.

- Heterogeneous Integration: Packaging solutions that allow for the seamless integration of disparate materials and components, such as different semiconductor types (e.g., III-V materials with silicon), are becoming vital for complex optical modules.

- Enhanced Reliability and Hermeticity: As opto-electronic devices are deployed in harsher environments (e.g., automotive, industrial), there is an increasing emphasis on packaging solutions that offer superior protection against moisture, dust, and mechanical stress, ensuring long-term performance.

- Development of Advanced Packaging Materials: Research into new materials with superior electrical, thermal, and mechanical properties, including low-loss polymers, advanced ceramics, and composite materials, is crucial for optimizing package performance.

- Automated Assembly and Testing: The shift towards highly automated manufacturing processes for packaging, including automated optical alignment and in-situ testing, improves yield, reduces costs, and enhances consistency in high-volume production.

AI Impact Analysis on Opto Electronic Packaging

User queries regarding the impact of AI on Opto Electronic Packaging frequently explore how artificial intelligence can optimize design processes, enhance manufacturing efficiency, and improve quality control. There is a strong interest in AI's potential to accelerate the development cycle of complex packaging solutions, from conceptual design to final validation. Users often seek examples of predictive maintenance applications in packaging equipment or how AI can aid in the discovery of new materials or assembly techniques.

The general expectation is that AI will streamline various stages of the packaging workflow, leading to more robust, cost-effective, and performance-optimized products. Concerns often include the data requirements for effective AI implementation, the need for skilled personnel to manage AI-driven systems, and the initial investment costs associated with adopting AI technologies. Overall, the consensus among users is that AI holds significant promise for revolutionizing opto-electronic packaging, making it more intelligent and efficient.

- Design Optimization: AI algorithms can rapidly analyze vast datasets to optimize package designs for thermal performance, optical alignment, and mechanical stability, significantly reducing design iteration cycles and time-to-market.

- Predictive Maintenance: AI-powered analytics can monitor manufacturing equipment in real-time, predict potential failures, and schedule preventative maintenance, thereby minimizing downtime and improving overall equipment effectiveness (OEE) in packaging lines.

- Automated Quality Control and Inspection: Machine vision systems integrated with AI can perform highly accurate and rapid defect detection in packaged components, surpassing human capabilities in consistency and speed, leading to higher yield rates.

- Process Optimization and Control: AI can analyze manufacturing parameters (e.g., temperature, pressure, bonding force) to dynamically adjust processes, ensuring optimal conditions for precise packaging operations like die bonding, wire bonding, and sealing.

- Materials Discovery and Characterization: AI-driven simulations and data analysis can accelerate the identification and characterization of novel materials with desirable properties for packaging, such as enhanced thermal conductivity or improved optical transparency.

- Supply Chain Management: AI can optimize logistics, inventory management, and demand forecasting for packaging components and materials, leading to more resilient and efficient supply chains.

Key Takeaways Opto Electronic Packaging Market Size & Forecast

Common user questions regarding the key takeaways from the Opto Electronic Packaging market size and forecast often center on understanding the primary drivers of growth, identifying the most lucrative application areas, and assessing the long-term sustainability of market expansion. Users are keen to know which technological advancements are most impactful and how geopolitical and economic factors might influence future market trajectories. The core interest lies in discerning actionable insights that can inform strategic planning and investment decisions within this rapidly evolving sector.

The insights reveal a market characterized by sustained growth, propelled by the insatiable demand for high-speed data across various industries and the increasing integration of optical components into everyday technologies. The continuous drive towards miniaturization, improved performance, and enhanced reliability remains paramount, creating a fertile ground for innovation in packaging solutions. Furthermore, the market's resilience is underpinned by its critical role in foundational technologies such as 5G, AI, cloud computing, and advanced automotive systems, positioning it for robust expansion throughout the forecast period.

- Strong Growth Trajectory: The market is poised for significant expansion, driven by increasing data traffic and the proliferation of optical technologies in diverse applications.

- Technology-Driven Expansion: Innovations in silicon photonics, heterogeneous integration, and advanced thermal management are pivotal in overcoming current packaging limitations and opening new market avenues.

- Critical Enabler for Emerging Tech: Opto-electronic packaging is fundamental to the realization and scalability of 5G infrastructure, AI hardware, autonomous vehicles, and high-performance computing.

- Demand from Diverse Industries: Key growth sectors include telecommunications, data centers, consumer electronics, automotive, and healthcare, each presenting unique packaging requirements and opportunities.

- Focus on Reliability and Performance: As devices become more complex and operate in challenging environments, the emphasis on robust, hermetic, and high-performance packaging solutions will intensify.

Opto Electronic Packaging Market Drivers Analysis

The Opto Electronic Packaging market is significantly influenced by a confluence of powerful drivers stemming from global technological advancements and increasing data consumption. The ever-growing demand for higher bandwidth and faster data transmission speeds across various sectors, coupled with the miniaturization trend in electronic devices, necessitates innovative and highly efficient packaging solutions for optical components. These drivers collectively create a robust environment for market expansion, pushing the boundaries of current packaging technologies.

Furthermore, the rapid proliferation of smart devices, the build-out of 5G infrastructure, and the expansion of data centers are putting unprecedented pressure on opto-electronic components to perform reliably under demanding conditions. This demand translates directly into a need for sophisticated packaging that can protect sensitive components, manage heat effectively, and ensure precise optical alignment. The automotive industry's pivot towards autonomous driving and advanced sensing also significantly contributes to the market's growth, as opto-electronic components like LiDAR and advanced lighting systems become integral.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth in Data Traffic and Cloud Computing | +1.5% | Global, particularly North America, APAC (China, India) | Long-term (2025-2033) |

| Expansion of 5G Infrastructure and Next-Gen Telecom Networks | +1.2% | Global, especially APAC (South Korea, China), North America, Europe | Mid-term (2025-2030) |

| Increasing Adoption of Opto-electronic Devices in Automotive (LiDAR, ADAS, Lighting) | +1.0% | Europe, North America, APAC (Japan, Germany, USA) | Long-term (2025-2033) |

| Miniaturization and Integration Trends in Consumer Electronics | +0.8% | Global, especially APAC (China, South Korea), North America | Short-term to Mid-term (2025-2028) |

| Growing Demand for Advanced Sensing Technologies in Healthcare and Industrial IoT | +0.7% | North America, Europe, APAC (Japan, USA, Germany) | Mid-term (2025-2030) |

Opto Electronic Packaging Market Restraints Analysis

Despite the robust growth trajectory, the Opto Electronic Packaging market faces several significant restraints that could potentially impede its full potential. One primary challenge lies in the inherent complexity and precision required for advanced packaging techniques. This often translates into higher manufacturing costs and lower yields, particularly for high-performance and highly integrated optical modules, making them less accessible for cost-sensitive applications.

Furthermore, the specialized nature of materials and equipment, coupled with a highly skilled workforce requirement, can create bottlenecks in production and innovation. Supply chain vulnerabilities, often exacerbated by geopolitical tensions or global events, also pose a considerable risk, leading to material shortages and increased lead times. These factors necessitate continuous innovation in cost-effective manufacturing processes and diversified supply chains to mitigate their impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital-Intensive Equipment | -1.0% | Global, particularly emerging economies | Long-term (2025-2033) |

| Technical Complexity and Yield Challenges for Advanced Packaging | -0.8% | Global | Mid-term (2025-2030) |

| Lack of Standardization Across Different Opto-electronic Devices | -0.7% | Global | Short-term to Mid-term (2025-2028) |

| Supply Chain Vulnerabilities and Geopolitical Dependencies | -0.6% | Global, especially reliant regions (e.g., East Asia) | Short-term (2025-2027) |

| Limited Availability of Specialized Materials and Skilled Workforce | -0.5% | Global, particularly developing regions | Mid-term (2025-2030) |

Opto Electronic Packaging Market Opportunities Analysis

The Opto Electronic Packaging market presents numerous growth opportunities, primarily driven by the advent of new technologies and the expansion into untapped application areas. The increasing investment in quantum computing and advanced AI hardware, which heavily rely on sophisticated optical interconnects, opens up a significant niche for specialized packaging solutions. Furthermore, the ongoing research and development in novel packaging materials and manufacturing techniques offer pathways to overcome existing limitations and achieve higher performance and cost efficiency.

The global shift towards smart cities, smart homes, and the broader Internet of Things (IoT) ecosystem creates a vast landscape for integrated optical sensors and communication modules, each requiring tailored packaging. Collaborations between research institutions, material suppliers, and device manufacturers can accelerate innovation and foster the development of next-generation packaging technologies. These emerging avenues represent substantial potential for market players to diversify their portfolios and capture new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Quantum Computing and AI Hardware | +1.5% | North America, Europe, APAC (Japan, China) | Long-term (2028-2033) |

| Expansion into New Application Verticals (e.g., AR/VR, Space, Biomedical) | +1.3% | Global | Mid-term (2026-2030) |

| Advancements in Heterogeneous Integration and Silicon Photonics | +1.1% | Global, particularly research hubs (e.g., USA, Europe, Japan) | Long-term (2025-2033) |

| Development of Novel Materials and Fabrication Techniques | +0.9% | Global | Mid-term (2025-2030) |

| Increasing Investments in Smart City and IoT Infrastructure | +0.8% | APAC (China, India), Europe, North America | Mid-term (2025-2030) |

Opto Electronic Packaging Market Challenges Impact Analysis

The Opto Electronic Packaging market faces formidable challenges that demand continuous innovation and strategic adaptation. Achieving extremely high precision in optical alignment, particularly for multi-component modules, remains a complex and costly endeavor. This challenge is compounded by the need to manage significant heat dissipation in increasingly powerful and compact opto-electronic devices, which can compromise long-term reliability if not adequately addressed through advanced thermal solutions.

Furthermore, maintaining the long-term reliability and hermeticity of packaged components, especially in harsh operating environments, presents ongoing engineering hurdles. The inherent trade-offs between performance, cost, and manufacturability also pose a significant dilemma for market players. These challenges necessitate collaborative efforts across the supply chain, from material science to manufacturing process optimization, to ensure the sustained growth and technical advancement of the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-High Precision Optical Alignment | -1.2% | Global | Long-term (2025-2033) |

| Effective Thermal Management for High-Power Devices | -1.0% | Global | Mid-term (2025-2030) |

| Ensuring Long-term Reliability and Hermeticity in Harsh Environments | -0.9% | Global | Long-term (2025-2033) |

| Balancing Performance, Cost, and Manufacturability | -0.8% | Global | Mid-term (2025-2030) |

| Integration of Dissimilar Materials and Components | -0.7% | Global | Short-term to Mid-term (2025-2028) |

Opto Electronic Packaging Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Opto Electronic Packaging Market, offering valuable insights into its current state, historical performance, and future projections. The scope encompasses detailed market sizing, growth rate analysis, identification of key market drivers, restraints, opportunities, and challenges influencing the industry landscape. It delves into the impact of emerging technologies like AI and offers a meticulous segmentation analysis across various types, materials, applications, and regional landscapes. The report also highlights the profiles of leading market players, providing a holistic view for stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.65 Billion |

| Market Forecast in 2033 | USD 5.25 Billion |

| Growth Rate | 8.9% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amkor Technology Inc., ASE Technology Holding Co. Ltd., Coherent Corp. (formerly II-VI Incorporated), DZS Inc., Emcore Corporation, Finisar Corporation, Fujitsu Optical Components, GlobalFoundries Inc., Infinera Corporation, Intel Corporation, Lumentum Holdings Inc., NeoPhotonics Corporation, Oclaro Inc. (now part of Lumentum), Sumitomo Electric Industries, Ltd., Texas Instruments Incorporated, T-micro Corporation, Sanmina Corporation, Qorvo, Inc., Broadcom Inc., OSRAM Opto Semiconductors GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Opto Electronic Packaging market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation encompasses various classifications based on packaging type, materials used, application areas, and end-use industries, reflecting the multifaceted nature of opto-electronic components and their varied requirements. Analyzing these segments helps in identifying specific growth pockets, technological preferences, and demand patterns across different verticals.

Each segment is influenced by unique drivers and faces distinct challenges, from the stringent reliability demands in aerospace and defense to the cost-effectiveness imperative in consumer electronics. Understanding these nuances is crucial for market participants to tailor their product offerings, R&D investments, and market entry strategies. The detailed breakdown reveals how technological advancements are shaping each sub-segment, fostering innovation that addresses specific industry needs and expands the overall market's reach into new and emerging applications.

- By Type: Hermetic Packaging, Non-Hermetic Packaging

- By Material: Ceramic, Plastic, Glass, Metal, Others (e.g., Silicon)

- By Packaging Type: Chip-on-board (COB), Surface Mount Device (SMD), Transistor Outline (TO), Fiber Optic (FO) Connectors/Modules, System-in-Package (SiP), Wafer-Level Packaging (WLP), Others

- By Application: Telecommunications, Data Communications (Data Centers, Cloud), Consumer Electronics (Smartphones, Wearables, Displays), Automotive (LiDAR, ADAS, In-cabin Sensing, Lighting), Healthcare & Medical (Imaging, Diagnostics, Surgical), Industrial (Sensors, Automation, Lighting), Aerospace & Defense, Others (e.g., Scientific Instruments, Energy)

Regional Highlights

The global Opto Electronic Packaging market exhibits distinct regional dynamics driven by varying levels of technological adoption, manufacturing capabilities, and end-use industry concentration. Asia Pacific, particularly China, Japan, South Korea, and Taiwan, dominates the market due to its robust electronics manufacturing base, significant investments in 5G infrastructure, and burgeoning consumer electronics and automotive industries. This region is a major hub for both production and consumption of opto-electronic devices, fostering rapid advancements in packaging technologies.

North America and Europe are significant players, characterized by strong R&D capabilities, a high concentration of data centers, and leading automotive and aerospace industries. These regions focus on high-performance and specialized packaging solutions, particularly for advanced communication networks, AI hardware, and autonomous vehicle technologies. Latin America, the Middle East, and Africa are emerging markets, showing gradual growth driven by increasing internet penetration, developing infrastructure, and rising demand for consumer electronics, presenting future opportunities for market expansion.

- Asia Pacific (APAC): Expected to hold the largest market share due to its prominent position as a manufacturing hub for electronics and semiconductors, coupled with extensive investments in 5G deployment, data centers, and electric vehicles in countries like China, Japan, South Korea, and Taiwan.

- North America: A significant market driven by technological innovation, the presence of major data center operators, strong adoption of cloud computing, and advancements in autonomous vehicle technology and defense applications.

- Europe: A key region for automotive electronics, industrial automation, and advanced communication networks, with notable contributions from countries like Germany, France, and the UK focusing on high-reliability and specialized packaging solutions.

- Latin America: An emerging market with growing demand for internet services and consumer electronics, leading to increasing adoption of opto-electronic components, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Witnessing growth spurred by ongoing digital transformation initiatives, increasing investments in telecommunications infrastructure, and rising adoption of smart technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Opto Electronic Packaging Market.- Amkor Technology Inc.

- ASE Technology Holding Co. Ltd.

- Coherent Corp. (formerly II-VI Incorporated)

- DZS Inc.

- Emcore Corporation

- Finisar Corporation

- Fujitsu Optical Components

- GlobalFoundries Inc.

- Infinera Corporation

- Intel Corporation

- Lumentum Holdings Inc.

- NeoPhotonics Corporation

- Oclaro Inc. (now part of Lumentum)

- Sumitomo Electric Industries, Ltd.

- Texas Instruments Incorporated

- T-micro Corporation

- Sanmina Corporation

- Qorvo, Inc.

- Broadcom Inc.

- OSRAM Opto Semiconductors GmbH

Frequently Asked Questions

What is opto-electronic packaging?

Opto-electronic packaging refers to the intricate process of enclosing and protecting sensitive opto-electronic components, such as lasers, detectors, and optical fibers, to ensure their reliable operation, thermal management, and precise optical alignment for optimal performance in various applications.

Why is advanced packaging crucial for optoelectronics?

Advanced packaging is crucial because it provides mechanical protection, enables efficient heat dissipation, maintains precise optical alignment, ensures hermetic sealing against environmental factors, and facilitates electrical and optical interconnects, all of which are essential for the high performance, reliability, and longevity of opto-electronic devices.

Which industries are driving the opto-electronic packaging market?

The primary industries driving the opto-electronic packaging market include telecommunications (5G, fiber optics), data communications (data centers, cloud computing), consumer electronics (smartphones, wearables), automotive (LiDAR, ADAS), and healthcare (medical imaging, diagnostics).

What are the latest innovations in materials for opto-electronic packaging?

Recent innovations in materials for opto-electronic packaging include the development of advanced ceramics with improved thermal conductivity, low-loss polymers for optical waveguides, glass-based interposers for high-density integration, and specialized epoxies and solders for enhanced reliability and hermeticity.

How does miniaturization impact opto-electronic packaging?

Miniaturization profoundly impacts opto-electronic packaging by demanding smaller form factors, higher integration density (e.g., 3D stacking, SiP), and more efficient thermal management within reduced volumes, driving innovations in wafer-level packaging and chip-on-board technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted