Flexible Plastic Packaging Market

Flexible Plastic Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705466 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

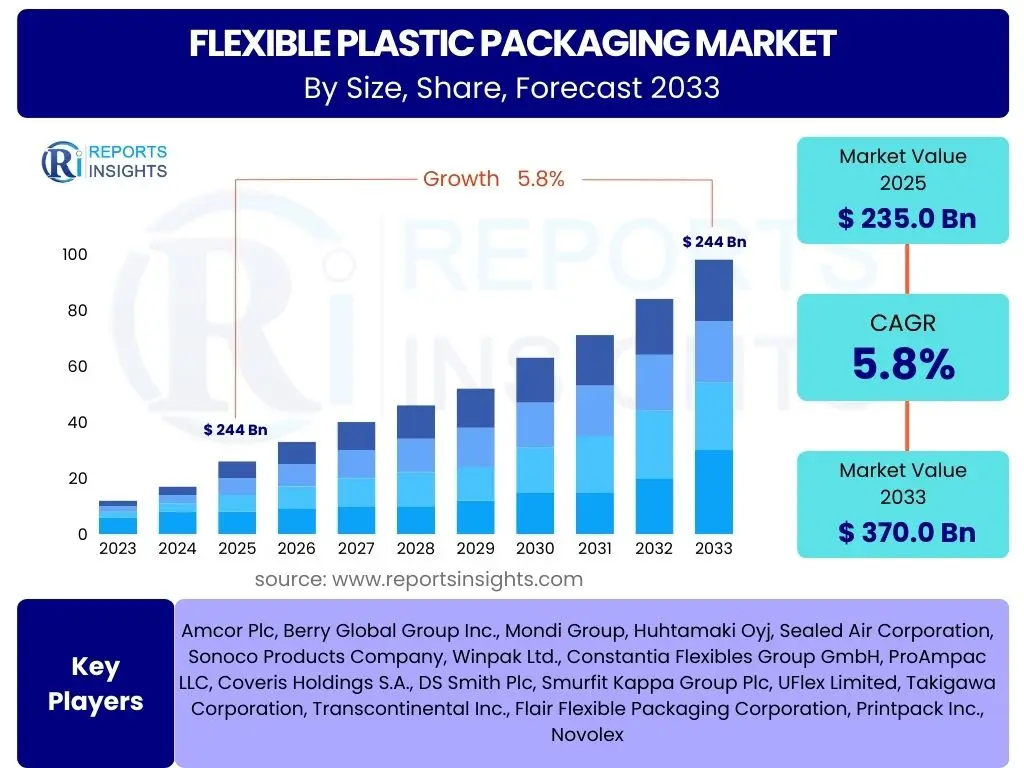

Flexible Plastic Packaging Market Size

According to Reports Insights Consulting Pvt Ltd, The Flexible Plastic Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 235.0 Billion in 2025 and is projected to reach USD 370.0 Billion by the end of the forecast period in 2033.

Key Flexible Plastic Packaging Market Trends & Insights

The flexible plastic packaging market is characterized by dynamic shifts driven by consumer preferences, technological advancements, and a heightened focus on sustainability. Users frequently inquire about the leading trends shaping this industry, particularly concerning eco-friendly solutions, smart packaging innovations, and the impact of e-commerce on packaging design and functionality. A prominent trend involves the development and adoption of mono-material structures, which simplify the recycling process compared to multi-layer composites, directly addressing growing environmental concerns and regulatory pressures for a circular economy.

Another significant insight revolves around the increasing integration of digital printing technologies, enabling greater customization, shorter production runs, and enhanced brand engagement through variable data printing. This trend caters to the demand for personalized products and agile supply chains. Furthermore, the market is witnessing a surge in demand for high-barrier flexible packaging solutions that extend product shelf life, reduce food waste, and maintain product integrity, especially for sensitive food, beverage, and pharmaceutical applications. These innovations are critical for maintaining product quality across extended distribution channels.

The expansion of e-commerce continues to reshape packaging requirements, driving demand for flexible formats that are lightweight, durable, and optimized for shipping efficiency, while also offering an unboxing experience that aligns with brand identity. This has led to innovations in flexible packaging that withstand the rigors of transit and maintain product presentation upon arrival. Consumers are also increasingly seeking convenience features such as easy-open and reclosable options, driving manufacturers to innovate in design and functionality to enhance user experience.

- Shift towards sustainable and recyclable mono-material solutions.

- Increased adoption of digital printing for customization and agility.

- Growing demand for high-barrier films to extend shelf life.

- E-commerce driven demand for lightweight and robust packaging.

- Innovation in convenience features like easy-open and reclosable designs.

AI Impact Analysis on Flexible Plastic Packaging

User inquiries concerning the impact of Artificial Intelligence (AI) on the flexible plastic packaging sector often center around operational efficiency, quality control, design optimization, and supply chain management. AI's influence is increasingly visible in automating and optimizing manufacturing processes, from predictive maintenance of machinery to real-time quality inspection. AI-powered vision systems can detect even minute defects in film production or sealing, significantly reducing waste and improving product consistency. This leads to higher throughput and reduced operational costs for manufacturers.

Furthermore, AI algorithms are being leveraged for demand forecasting and inventory management, enabling packaging manufacturers to align production more closely with market needs, thereby minimizing overproduction and optimizing resource allocation. This precision in forecasting helps in mitigating supply chain disruptions and ensures a more responsive manufacturing environment. In the realm of product design, AI tools are assisting in optimizing material usage, designing for recyclability, and simulating performance under various conditions, leading to more sustainable and functional packaging solutions.

The application of AI extends to enhancing supply chain transparency and traceability. AI-driven analytics can monitor material flows, track shipments, and identify potential bottlenecks or inefficiencies across the value chain, from raw material sourcing to final product delivery. This comprehensive oversight facilitates better decision-making and fosters greater resilience in complex global supply networks. AI also plays a role in analyzing vast datasets of consumer preferences and market trends, providing actionable insights for developing new packaging formats and features that resonate with target audiences.

- Enhanced quality control through AI-powered vision systems.

- Optimized production planning and demand forecasting.

- AI-driven material optimization and sustainable design.

- Improved supply chain visibility and traceability.

- Data-driven insights for new product development.

Key Takeaways Flexible Plastic Packaging Market Size & Forecast

Common user questions regarding the key takeaways from the flexible plastic packaging market size and forecast consistently point to the market's robust growth trajectory and its underlying drivers. A primary takeaway is the significant projected expansion, fueled by increasing demand from diverse end-use industries, particularly food and beverage, pharmaceuticals, and personal care. The inherent benefits of flexible packaging, such as its lightweight nature, cost-effectiveness, and versatility, continue to make it a preferred choice for manufacturers seeking efficient and adaptable packaging solutions globally.

Another crucial insight is the growing emphasis on sustainability, which is not merely a trend but a fundamental shift influencing investment and innovation within the sector. The market's future growth is heavily contingent on the successful development and widespread adoption of recyclable, compostable, and bio-based flexible materials, alongside advancements in recycling infrastructure. This underscores the industry's commitment to addressing environmental concerns while meeting escalating consumer and regulatory demands for eco-friendly products.

Geographically, emerging economies are expected to be major contributors to market growth, driven by increasing disposable incomes, urbanization, and the expansion of organized retail and e-commerce. These regions present substantial opportunities for market players to expand their footprint and introduce innovative flexible packaging solutions. The market's resilience against economic fluctuations and its continuous evolution through technological integration, such as AI and smart packaging, also highlight its long-term potential and strategic importance in the global packaging landscape.

- Market demonstrates significant growth potential through 2033.

- Sustainability and circular economy initiatives are pivotal growth determinants.

- Emerging economies are key drivers of future demand.

- Technological advancements, including AI, are enhancing market efficiency and innovation.

- Versatility and cost-effectiveness remain core competitive advantages.

Flexible Plastic Packaging Market Drivers Analysis

The growth of the flexible plastic packaging market is propelled by a confluence of factors, prominently featuring the escalating global demand for packaged goods across various industries. The food and beverage sector, in particular, relies heavily on flexible packaging for its ability to preserve freshness, extend shelf life, and offer convenient portion sizes, directly addressing evolving consumer lifestyles and preferences for on-the-go consumption. This packaging format's lightweight nature also contributes significantly to reduced transportation costs and carbon footprint, making it an economically attractive option for manufacturers and distributors seeking operational efficiencies and lower logistics overheads.

The rapid expansion of the e-commerce sector has further intensified the demand for flexible packaging. Products sold online require packaging that is durable enough to withstand the rigors of shipping, yet light enough to minimize freight costs. Flexible packaging, with its excellent protective qualities and adaptability to various product shapes, perfectly meets these requirements, enabling safe delivery and enhancing the overall customer experience. This shift in retail channels necessitates packaging solutions that are optimized for individual parcel delivery rather than bulk retail display.

Innovation in material science, particularly the development of advanced barrier films, active packaging, and smart packaging technologies, also acts as a significant driver. These innovations enhance product protection against moisture, oxygen, and light, thereby improving food safety and reducing waste. Furthermore, the cost-effectiveness of flexible plastic packaging compared to rigid alternatives, coupled with its ability to be customized for specific branding and marketing needs, continues to drive its adoption across a broad spectrum of end-use applications, ensuring its sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Food & Beverage Industry | +1.5% | Global, particularly Asia Pacific & Europe | Short to Long-term (2025-2033) |

| Expansion of E-commerce Sector | +1.2% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Cost-Effectiveness & Lightweighting Benefits | +1.0% | Global | Long-term (2025-2033) |

| Technological Advancements in Barrier Films | +0.8% | Global | Mid-term (2027-2033) |

| Rise in Disposable Incomes & Urbanization | +0.7% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Flexible Plastic Packaging Market Restraints Analysis

Despite its widespread utility, the flexible plastic packaging market faces significant restraints, primarily stemming from escalating environmental concerns and stringent regulatory frameworks. The non-biodegradable nature of many conventional plastics and their contribution to plastic pollution in oceans and landfills have led to widespread public disapproval and increased pressure from environmental advocacy groups. This negative perception is compelling consumers and brands alike to seek more sustainable alternatives, thereby challenging the dominance of traditional flexible plastic solutions.

Government initiatives and regulations, such as bans on single-use plastics, extended producer responsibility (EPR) schemes, and mandates for recycled content, pose substantial hurdles for manufacturers. These regulatory shifts necessitate significant investments in research and development for new materials, redesign of existing packaging, and adaptation of manufacturing processes, which can increase operational costs and complexity. Compliance with diverse regional regulations adds a layer of complexity for global players, requiring tailored approaches for different markets and potentially slowing down market expansion in specific geographies.

Competition from alternative packaging materials, including rigid plastics, paper-based packaging, glass, and metal, also acts as a restraint. As sustainability trends push innovation across all packaging formats, some applications may see a shift away from flexible plastics towards materials perceived as more environmentally friendly or easier to recycle. Furthermore, the technical challenges associated with recycling multi-layer flexible packaging, which often consists of different types of plastics bonded together, limit its circularity and contribute to its environmental footprint, thereby restraining its growth in segments prioritizing end-of-life solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Environmental Regulations & Plastic Bans | -1.3% | Europe, North America, parts of Asia Pacific | Short to Mid-term (2025-2030) |

| Negative Public Perception of Plastic Pollution | -1.0% | Global | Long-term (2025-2033) |

| Challenges in Recycling Multi-layer Structures | -0.9% | Global | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.6% | Global | Short-term (2025-2027) |

| Competition from Alternative Packaging Materials | -0.5% | Global | Mid-term (2026-2031) |

Flexible Plastic Packaging Market Opportunities Analysis

Significant opportunities abound in the flexible plastic packaging market, primarily driven by the imperative for sustainable innovation and the expanding landscape of new applications. The development and commercialization of advanced sustainable materials, such as bio-based polymers, compostable films, and high-performance mono-materials designed for easier recycling, represent a major growth avenue. Brands are actively seeking packaging solutions that align with their corporate sustainability goals and consumer demand for eco-friendly products, creating a robust market for innovators in this space. Investments in research and development for these next-generation materials are crucial for tapping into this demand.

The growing demand for flexible packaging in emerging markets, propelled by increasing disposable incomes, urbanization, and the proliferation of organized retail and e-commerce, presents substantial geographical expansion opportunities. Countries in Asia Pacific, Latin America, and the Middle East and Africa are experiencing rapid industrialization and population growth, leading to a burgeoning middle class with greater purchasing power and a demand for packaged consumer goods. Establishing local manufacturing capabilities and tailored product offerings in these regions can unlock considerable market potential.

Furthermore, the integration of smart packaging technologies offers a compelling opportunity for market differentiation and value addition. Features such as QR codes, NFC tags, temperature indicators, and anti-counterfeit measures can enhance product traceability, provide consumers with real-time information, and improve supply chain efficiency. These innovations not only boost brand engagement but also address critical concerns related to product safety and authenticity, particularly in sensitive sectors like pharmaceuticals and premium food items. The continuous evolution of consumer lifestyles and the need for convenience also open doors for creative packaging designs that offer resealability, portion control, and ease of use.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Sustainable Materials | +1.8% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Expansion in Emerging Economies | +1.5% | Asia Pacific, Latin America, MEA | Mid to Long-term (2026-2033) |

| Integration of Smart Packaging Technologies | +1.1% | North America, Europe, parts of Asia Pacific | Mid-term (2027-2032) |

| Technological Advancements in Recycling Infrastructure | +0.9% | Global | Long-term (2028-2033) |

| Increased Demand for Convenience Packaging | +0.7% | Global | Short to Mid-term (2025-2030) |

Flexible Plastic Packaging Market Challenges Impact Analysis

The flexible plastic packaging market faces several complex challenges, with the most pressing being the imperative to establish truly circular economy models and overcome the technical difficulties associated with recycling multi-layer materials. The inherent complexity of separating and processing different plastic layers, often combined with barrier coatings or foils, makes mechanical recycling economically and technically challenging. This limitation hinders the industry's ability to meet ambitious recycling targets and contributes to the perception of flexible plastics as difficult-to-recycle materials, despite ongoing innovations in advanced recycling technologies.

Another significant challenge is managing the volatility of raw material prices, primarily crude oil derivatives. Fluctuations in petrochemical prices directly impact the cost of producing plastic resins, leading to unpredictable manufacturing costs for flexible packaging producers. This unpredictability makes long-term planning and pricing strategies difficult, potentially eroding profit margins and delaying investments in new technologies or sustainable solutions. Supply chain disruptions, often exacerbated by geopolitical events or global health crises, further complicate the procurement of essential raw materials and components, leading to production delays and increased operational risks.

Furthermore, regulatory divergence across different regions and countries poses a compliance challenge for global manufacturers. Varying standards for packaging design, material composition, labeling, and waste management necessitate customized approaches for different markets, increasing operational complexity and costs. Educating consumers and stakeholders about the benefits of flexible packaging, particularly in the context of food waste reduction and resource efficiency, also remains a continuous challenge, requiring coordinated efforts across the industry to counter negative perceptions and foster responsible consumption and disposal practices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Recycling Multi-material Structures | -1.1% | Global | Long-term (2025-2033) |

| Volatility of Raw Material Prices | -0.8% | Global | Short to Mid-term (2025-2028) |

| Regulatory Divergence Across Regions | -0.7% | Global | Long-term (2025-2033) |

| Establishing Robust Circular Economy Infrastructure | -0.6% | Global | Long-term (2025-2033) |

| Public Misconceptions Regarding Plastic Packaging | -0.5% | Global | Long-term (2025-2033) |

Flexible Plastic Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Flexible Plastic Packaging Market, offering valuable insights into its current landscape, key trends, drivers, restraints, opportunities, and challenges. The scope encompasses a detailed examination of market size and growth forecasts, segmented analysis by material, product type, and application, alongside a thorough regional assessment. The report also highlights the competitive environment and profiles key industry players, providing a holistic view for strategic decision-making and investment planning within the global flexible plastic packaging sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 235.0 Billion |

| Market Forecast in 2033 | USD 370.0 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor Plc, Berry Global Group Inc., Mondi Group, Huhtamaki Oyj, Sealed Air Corporation, Sonoco Products Company, Winpak Ltd., Constantia Flexibles Group GmbH, ProAmpac LLC, Coveris Holdings S.A., DS Smith Plc, Smurfit Kappa Group Plc, UFlex Limited, Takigawa Corporation, Transcontinental Inc., Flair Flexible Packaging Corporation, Printpack Inc., Novolex |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The flexible plastic packaging market is extensively segmented based on material type, product type, and application or end-use industry, reflecting the diverse requirements and functionalities of packaging solutions across various sectors. This detailed segmentation provides a granular view of market dynamics, identifying specific growth pockets and areas of innovation. Each segment plays a crucial role in shaping the overall market, driven by unique consumer demands, regulatory landscapes, and technological advancements tailored to specific product categories.

The material segment encompasses various polymers like Polyethylene (PE), Polypropylene (PP), and Polyethylene Terephthalate (PET), each chosen for its specific properties such as barrier, strength, or clarity. The increasing focus on sustainability is leading to significant shifts within this segment, with growing interest in bioplastics and mono-material solutions that enhance recyclability. Product types range from versatile pouches and bags to specialized films and sachets, each designed to meet specific product protection, shelf-life, and consumer convenience needs. The constant innovation in product formats, such as stand-up pouches with spouts, continues to expand market reach.

The application segment highlights the broad utility of flexible plastic packaging across major industries. The food and beverage sector remains the largest consumer, driven by trends in convenience foods, fresh produce packaging, and portion control. Pharmaceutical and healthcare applications demand high-barrier and sterile packaging, while cosmetics and personal care benefit from flexible solutions for tubes, sachets, and refill packs. Industrial and consumer goods sectors also contribute significantly, utilizing flexible packaging for protective and logistical purposes. Understanding these interdependencies across segments is vital for strategic market positioning and product development.

- By Material:

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polyamide (PA)

- Polyvinyl Chloride (PVC)

- Ethylene Vinyl Alcohol (EVOH)

- Bioplastics (e.g., PLA, PHA, PBS)

- Others (e.g., Cellophane, Aluminum Foil laminates)

- By Product Type:

- Pouches (Stand-up Pouches, Spouted Pouches, Flat Pouches)

- Bags (Wicketed Bags, Gusseted Bags, Side-weld Bags)

- Films & Wraps (Stretch Films, Shrink Films, Lidding Films, Barrier Films)

- Sachets

- Labels

- Lids

- By Application/End-Use Industry:

- Food & Beverage (Ready Meals, Snacks, Dairy, Meat, Poultry & Seafood, Bakery, Beverages)

- Pharmaceutical & Healthcare (Blister Packaging, Medical Devices, Over-the-counter Drugs)

- Cosmetics & Personal Care (Shampoos, Lotions, Soaps)

- Industrial (Chemicals, Automotive Parts, Building Materials)

- Consumer Goods (Home Care Products, Pet Food, Sporting Goods)

- Other Applications (Agriculture, Electronics)

Regional Highlights

- North America: Characterized by mature markets and a strong emphasis on sustainable packaging solutions. High adoption of flexible packaging in food and beverage, pharmaceuticals, and e-commerce. Significant investments in advanced recycling technologies and bio-based plastics.

- Europe: Driven by stringent environmental regulations and robust consumer demand for eco-friendly packaging. Leading the way in circular economy initiatives, fostering innovation in mono-materials, and advocating for higher recycling rates. Strong market for premium and convenient flexible packaging formats.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid urbanization, increasing disposable incomes, expanding manufacturing base, and the booming e-commerce sector. China and India are key contributors, with rising demand for packaged food, personal care products, and pharmaceuticals. Investment in new production capacities and technological upgrades is substantial.

- Latin America: Exhibiting steady growth, primarily fueled by the expanding food and beverage industry and rising consumer demand for convenient packaging solutions. Brazil and Mexico are dominant markets, influenced by economic stability and increasing retail penetration.

- Middle East and Africa (MEA): Emerging as a promising market, driven by population growth, diversifying economies, and increasing organized retail. Significant opportunities in the food, personal care, and industrial sectors, with a growing focus on cost-effective and practical packaging solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Flexible Plastic Packaging Market.- Amcor Plc

- Berry Global Group Inc.

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Sonoco Products Company

- Winpak Ltd.

- Constantia Flexibles Group GmbH

- ProAmpac LLC

- Coveris Holdings S.A.

- DS Smith Plc

- Smurfit Kappa Group Plc

- UFlex Limited

- Takigawa Corporation

- Transcontinental Inc.

- Flair Flexible Packaging Corporation

- Printpack Inc.

- Novolex

Frequently Asked Questions

What is flexible plastic packaging?

Flexible plastic packaging refers to packaging made from pliable materials like films, foils, or sheets, designed to protect, preserve, and transport products. Unlike rigid packaging, it can change shape, offering benefits such as lightweighting, reduced material usage, and enhanced convenience for various consumer goods, food, beverage, and pharmaceutical products.

What are the primary benefits of flexible plastic packaging?

The primary benefits include its lightweight nature, which reduces transportation costs and carbon footprint; excellent barrier properties that extend product shelf life and prevent spoilage; cost-effectiveness compared to rigid alternatives; versatility in design and printing for branding; and consumer convenience features like easy opening and reclosability. It also offers efficient use of storage space.

What are the main challenges facing the flexible plastic packaging market?

Key challenges include environmental concerns related to plastic pollution, the technical complexity and cost of recycling multi-layer flexible plastics, volatility in raw material prices, and the increasing stringency of global regulations on plastic use. Overcoming these requires significant investment in sustainable materials and advanced recycling infrastructure.

How is sustainability impacting the flexible plastic packaging industry?

Sustainability is a major driver of innovation, pushing the industry towards developing recyclable and compostable mono-material solutions, increasing recycled content, and investing in advanced recycling technologies. Consumer and regulatory pressures are accelerating this shift, aiming for a more circular economy where packaging materials are reused or recycled efficiently, reducing environmental impact.

Which regions are leading the growth in the flexible plastic packaging market?

The Asia Pacific region, particularly countries like China and India, is projected to lead market growth due to rapid urbanization, increasing disposable incomes, and the expansion of the e-commerce sector. North America and Europe also maintain significant market shares, driven by technological innovation and a strong focus on sustainable packaging solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted