PE Plastic Packaging Market

PE Plastic Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705300 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

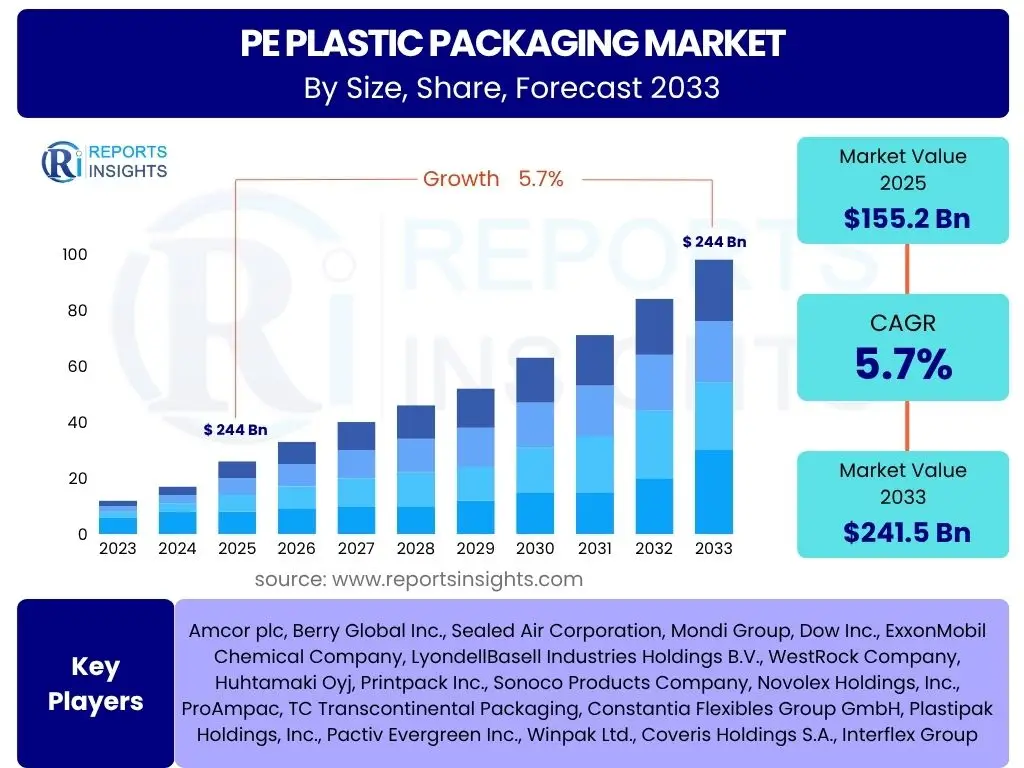

PE Plastic Packaging Market Size

According to Reports Insights Consulting Pvt Ltd, The PE Plastic Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2025 and 2033. The market is estimated at USD 155.2 Billion in 2025 and is projected to reach USD 241.5 Billion by the end of the forecast period in 2033.

Key PE Plastic Packaging Market Trends & Insights

The PE Plastic Packaging market is undergoing significant transformation, driven by a confluence of evolving consumer demands, stringent environmental regulations, and technological advancements. A primary trend is the accelerating shift towards sustainable packaging solutions, with an increasing focus on recyclability, the incorporation of Post-Consumer Recycled (PCR) content, and the development of monomaterial PE structures to simplify recycling processes. This push for circularity is largely influenced by growing consumer awareness regarding plastic pollution and governmental initiatives promoting a circular economy.

Furthermore, the market is witnessing a notable emphasis on light-weighting strategies aimed at reducing material usage and transportation costs, thereby improving the overall environmental footprint of packaging. The expansion of e-commerce continues to be a crucial growth driver, necessitating robust, flexible, and often custom-sized PE packaging solutions for safe product delivery. Innovations in barrier properties and material science are also shaping the market, enabling PE to protect sensitive products more effectively, extend shelf life, and potentially replace multi-material laminates with more recyclable PE-based alternatives.

- Increased adoption of sustainable and recyclable PE packaging solutions.

- Rising demand for Post-Consumer Recycled (PCR) content in PE formulations.

- Significant focus on light-weighting to reduce material consumption and carbon footprint.

- Growth in e-commerce necessitating durable and flexible packaging solutions.

- Advancements in barrier technologies for extended product shelf life and reduced food waste.

- Development of monomaterial PE packaging to enhance recyclability and circularity.

- Integration of smart packaging features for enhanced consumer engagement and supply chain traceability.

AI Impact Analysis on PE Plastic Packaging

Artificial Intelligence (AI) is increasingly poised to revolutionize the PE Plastic Packaging industry by optimizing various stages of the value chain, from design and production to waste management and recycling. Users frequently inquire about how AI can enhance operational efficiency, reduce material waste, and improve the environmental performance of packaging. AI algorithms can analyze vast datasets to predict material behavior, optimize manufacturing parameters for reduced energy consumption, and identify defects with greater precision than traditional methods, leading to higher quality products and reduced scrap rates. This predictive capability extends to maintenance, allowing for proactive intervention and minimized downtime.

Beyond manufacturing, AI holds immense potential in the post-consumer phase. It can significantly enhance the efficiency and accuracy of sorting plastic waste at recycling facilities through advanced vision systems and robotic automation, enabling higher purity levels of recycled PE. Furthermore, AI can aid in the design of packaging that is inherently more recyclable by simulating material interactions and end-of-life scenarios. The application of AI in supply chain management also promises improved logistics, demand forecasting, and inventory optimization, further reducing waste and operational costs throughout the entire packaging lifecycle.

- Optimized manufacturing processes: AI-driven systems improve production line efficiency, reduce energy consumption, and minimize material waste through real-time process control.

- Predictive maintenance: AI algorithms analyze equipment data to forecast potential failures, enabling proactive maintenance and reducing costly downtime.

- Enhanced quality control: AI-powered vision systems detect defects with high precision, ensuring consistent product quality and reducing non-conforming batches.

- Improved recycling sorting: AI and robotics significantly increase the accuracy and speed of sorting PE waste at Material Recovery Facilities (MRFs), leading to higher-quality recycled content.

- Supply chain optimization: AI enables advanced demand forecasting, inventory management, and logistics planning, reducing transport costs and carbon emissions.

- Sustainable design acceleration: AI tools assist in designing packaging for recyclability and reduced material usage by simulating performance and environmental impact.

- Waste reduction: AI contributes to minimizing waste across the entire packaging lifecycle, from production to end-of-life management, by identifying inefficiencies.

Key Takeaways PE Plastic Packaging Market Size & Forecast

The PE Plastic Packaging market is set for robust growth over the forecast period, driven by its unparalleled versatility, cost-effectiveness, and critical role in protecting goods across diverse industries. The market's expansion is intrinsically linked to rising global consumer demand for packaged goods, particularly within the food and beverage, pharmaceutical, personal care, and industrial sectors. Despite increasing environmental scrutiny, PE continues to innovate, demonstrating resilience through advancements in sustainability and circular economy initiatives.

A significant takeaway is the dual emphasis on meeting immediate market demands while proactively addressing long-term environmental responsibilities. Manufacturers are investing heavily in research and development to produce more recyclable, lighter, and resource-efficient PE solutions, including those incorporating a higher percentage of recycled content. The forecast indicates that regional disparities in growth will persist, with emerging economies contributing significantly to overall market expansion, while developed markets focus on regulatory compliance and the transition to sustainable alternatives.

- The PE plastic packaging market is projected for substantial growth, driven by continued demand from essential end-use industries.

- Innovation in sustainable PE solutions, including enhanced recyclability and increased use of PCR content, is critical for future growth.

- The cost-effectiveness and versatile properties of PE continue to ensure its dominant position in the global packaging landscape.

- E-commerce expansion and urbanization are key demand drivers, particularly for flexible PE packaging formats.

- Regulatory pressures and consumer preferences are compelling manufacturers to adopt more circular economy principles.

- Emerging economies in Asia Pacific and Latin America are anticipated to exhibit the highest growth rates due to industrialization and rising disposable incomes.

- Strategic collaborations across the value chain, from raw material suppliers to recyclers, are essential for advancing PE packaging sustainability goals.

PE Plastic Packaging Market Drivers Analysis

The PE plastic packaging market is propelled by a multitude of factors, chief among them the continuous expansion of the food and beverage industry, which relies heavily on PE for its protective qualities, flexibility, and cost-efficiency. Population growth and increasing urbanization globally contribute to higher consumption of packaged goods, directly stimulating demand for PE packaging solutions. The burgeoning e-commerce sector further amplifies this demand, requiring resilient and lightweight packaging to ensure safe delivery of products across vast logistical networks. Additionally, the inherent properties of PE, such as its excellent moisture barrier, chemical resistance, and ease of processing, make it a preferred choice for a wide array of applications, maintaining its competitive edge over alternative materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Food & Beverage Sector | +1.8% | Global, particularly Asia Pacific, North America | Long-term (2025-2033) |

| Expansion of E-commerce Industry | +1.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Global Population & Urbanization | +1.2% | Global, particularly emerging economies | Long-term (2025-2033) |

| Cost-effectiveness and Versatility of PE | +0.9% | Global | Long-term (2025-2033) |

| Advancements in Packaging Technology | +0.7% | Global, particularly developed regions | Medium-term (2025-2029) |

PE Plastic Packaging Market Restraints Analysis

Despite its widespread utility, the PE plastic packaging market faces significant restraints, primarily stemming from escalating environmental concerns over plastic pollution and the resulting stringent regulatory frameworks worldwide. Governments and international bodies are increasingly implementing bans on single-use plastics and mandating higher recycling targets, which directly impacts the production and consumption of virgin PE. Public perception, often fueled by media coverage of plastic waste in oceans and landfills, contributes to a negative sentiment towards plastic packaging, pushing consumers towards perceived eco-friendlier alternatives.

Furthermore, the volatility of raw material prices, specifically crude oil and natural gas, which are primary feedstocks for PE production, introduces economic instability and impacts profit margins for manufacturers. Competition from alternative packaging materials such as paper, glass, metals, and bioplastics, which are gaining traction due to their perceived sustainability advantages, also poses a significant challenge. These factors necessitate continuous innovation within the PE packaging sector to develop more sustainable and economically viable solutions to mitigate these restraints.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations & Bans on Single-Use Plastics | -1.5% | Europe, North America, parts of Asia | Long-term (2025-2033) |

| Negative Public Perception of Plastic Pollution | -1.0% | Global, particularly developed regions | Long-term (2025-2033) |

| Volatility in Raw Material Prices (Crude Oil) | -0.8% | Global | Short to Medium-term (2025-2029) |

| Competition from Alternative Packaging Materials | -0.7% | Global | Long-term (2025-2033) |

| Insufficient Recycling Infrastructure in Some Regions | -0.5% | Global, particularly developing nations | Long-term (2025-2033) |

PE Plastic Packaging Market Opportunities Analysis

Significant opportunities are emerging for the PE plastic packaging market, primarily driven by the escalating demand for sustainable packaging solutions. The focus on enhancing recyclability and the integration of Post-Consumer Recycled (PCR) content in new PE products presents a substantial growth avenue, aligning with circular economy objectives. Innovations in material science are leading to the development of bio-based PE and advanced light-weighting technologies, which not only reduce environmental impact but also offer economic benefits through lower material and transportation costs. These advancements allow manufacturers to meet evolving consumer preferences and regulatory requirements for greener packaging.

Furthermore, the untapped potential in emerging economies, characterized by rapidly growing populations, increasing disposable incomes, and developing retail infrastructure, offers vast market expansion opportunities. As these regions industrialize and modernize, the demand for packaged goods, and consequently PE packaging, is expected to surge. The ongoing research and development into advanced barrier solutions for PE films also open up new applications, particularly in the food and pharmaceutical sectors, by extending shelf life and reducing waste. These strategic shifts towards sustainability and market penetration in high-growth regions are poised to unlock substantial value for the PE plastic packaging industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable and Recyclable Packaging | +2.0% | Global, particularly Europe, North America | Long-term (2025-2033) |

| Technological Advancements in Recycling and PCR Integration | +1.7% | Global | Medium to Long-term (2025-2033) |

| Expansion into Emerging Markets (Asia Pacific, Latin America) | +1.4% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Innovation in Light-weighting and Barrier Properties | +1.0% | Global | Medium-term (2025-2029) |

| Development of Bio-based and Biodegradable PE Variants | +0.8% | Global, particularly Europe | Long-term (2027-2033) |

PE Plastic Packaging Market Challenges Impact Analysis

The PE plastic packaging market faces several significant challenges that necessitate strategic adaptation and continuous innovation. One of the most prominent challenges is the deeply ingrained negative public perception of plastics, which often leads to calls for complete bans and a widespread shift away from plastic materials, regardless of their specific type or recyclability. This public sentiment, coupled with growing environmental activism, exerts considerable pressure on manufacturers and brands to drastically alter their packaging strategies and invest heavily in alternatives or enhanced circularity solutions. The sheer scale and complexity of establishing a truly circular economy for plastics, which includes robust collection, sorting, and reprocessing infrastructure globally, remains a daunting task, particularly in regions with limited waste management capabilities.

Furthermore, the technical complexities associated with recycling multi-layer PE packaging, which often incorporates different polymers or additives to achieve specific barrier properties, pose a significant hurdle. These complex structures are difficult and costly to separate and reprocess into high-quality recyclates, limiting the adoption of circular practices. The transition costs involved in shifting from established conventional PE production methods to more sustainable alternatives, such as bio-based or high-recycled content PE, can be substantial for manufacturers, impacting profitability and requiring significant capital investment in new technologies and infrastructure. Addressing these challenges requires collaborative efforts across the entire value chain, from material science innovation to policy support and consumer education, to foster a more sustainable future for PE packaging.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Public Perception and Brand Scrutiny | -1.3% | Global, particularly developed economies | Long-term (2025-2033) |

| Establishing Robust Global Recycling Infrastructure | -1.0% | Global, particularly developing nations | Long-term (2025-2033) |

| Technological Barriers in Recycling Multi-Layer PE Packaging | -0.9% | Global | Long-term (2025-2033) |

| High Costs Associated with Transition to Circular Models | -0.7% | Global | Medium-term (2025-2029) |

| Maintaining Performance with High PCR Content | -0.6% | Global | Medium-term (2025-2029) |

PE Plastic Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the PE Plastic Packaging market, examining its current size, historical performance, and future growth trajectory. It offers detailed insights into the key market trends, drivers, restraints, opportunities, and challenges shaping the industry. The report encompasses a thorough segmentation analysis by various factors such as type, application, and end-use industry, alongside a robust regional assessment to highlight growth hotspots and competitive landscapes across major geographies. Furthermore, it includes an impact analysis of Artificial Intelligence on the market and profiles leading companies, providing a holistic view for strategic decision-making and market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 155.2 Billion |

| Market Forecast in 2033 | USD 241.5 Billion |

| Growth Rate | 5.7% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Inc., Sealed Air Corporation, Mondi Group, Dow Inc., ExxonMobil Chemical Company, LyondellBasell Industries Holdings B.V., WestRock Company, Huhtamaki Oyj, Printpack Inc., Sonoco Products Company, Novolex Holdings, Inc., ProAmpac, TC Transcontinental Packaging, Constantia Flexibles Group GmbH, Plastipak Holdings, Inc., Pactiv Evergreen Inc., Winpak Ltd., Coveris Holdings S.A., Interflex Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PE plastic packaging market is extensively segmented to provide granular insights into its diverse applications and material types, allowing for a detailed understanding of market dynamics and growth opportunities. Segmentation by type differentiates between High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), and Linear Low-Density Polyethylene (LLDPE), each possessing unique properties that dictate their suitability for specific packaging needs. HDPE is known for its rigidity and strength, often used in bottles and containers, while LDPE and LLDPE are favored for their flexibility in films, bags, and pouches.

Further segmentation by application categorizes the market into various packaging formats, including films (such as food packaging films, stretch films, and shrink films), bottles and containers, and flexible packaging such as bags and pouches. The end-use industry segmentation provides a comprehensive view of consumption patterns across critical sectors like Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Industrial Packaging, and Household Goods. This multi-layered segmentation is crucial for identifying key growth drivers, understanding competitive landscapes, and formulating targeted strategies within the dynamic PE plastic packaging ecosystem.

- By Type:

- HDPE (High-Density Polyethylene): Utilized for rigid packaging like bottles, drums, and crates due to its high strength-to-density ratio.

- LDPE (Low-Density Polyethylene): Primarily used in flexible packaging such as films, bags, and liners, valued for its flexibility and clarity.

- LLDPE (Linear Low-Density Polyethylene): Offers superior tensile strength and puncture resistance, making it ideal for stretch films, agricultural films, and heavy-duty bags.

- By Application:

- Films: Encompasses a broad range including food packaging films, industrial stretch films, and agricultural films.

- Bottles and Containers: Widely used for beverages, detergents, and personal care products.

- Bags and Pouches: Includes shopping bags, stand-up pouches, and heavy-duty sacks.

- Other Flexible Packaging: Specialized flexible solutions for various product categories.

- Other Rigid Packaging: Covers non-bottle/container rigid PE applications.

- By End-Use Industry:

- Food & Beverages: Dominant segment, driven by demand for food wraps, milk bottles, and flexible food pouches.

- Pharmaceuticals: Used for protective packaging of medicines and healthcare products due to inertness and barrier properties.

- Personal Care & Cosmetics: Common in bottles and tubes for shampoos, lotions, and creams.

- Industrial Packaging: Includes heavy-duty bags, protective films, and container linings for industrial products.

- Household Goods: Applications in packaging for cleaning products, toys, and various household items.

- Others: Includes packaging for automotive, electronics, and agricultural products.

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East & Africa (MEA)

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing market, driven by rapid industrialization, increasing urbanization, and a burgeoning consumer base in countries like China, India, and Southeast Asian nations. The region's expanding e-commerce sector and growing demand for packaged food and personal care products significantly contribute to market expansion.

- North America: A mature market characterized by technological advancements and a strong focus on sustainable packaging solutions. Demand is influenced by robust food & beverage and pharmaceutical industries, alongside a growing emphasis on incorporating recycled content and developing lighter packaging designs.

- Europe: Marked by stringent environmental regulations and a strong commitment to the circular economy. This region is a leader in developing innovative recycling technologies and promoting the use of Post-Consumer Recycled (PCR) content. Growth is primarily driven by the food industry and a push for more sustainable and recyclable PE solutions.

- Latin America: Showing steady growth, fueled by increasing disposable incomes, population growth, and the expansion of modern retail formats. Brazil and Mexico are key markets, with rising demand for flexible packaging and consumer goods.

- Middle East & Africa (MEA): Emerging markets with significant growth potential, particularly in the GCC countries due to infrastructure development and rising consumption levels. The region is witnessing investments in packaging capabilities to serve local and regional demands, though challenges related to recycling infrastructure remain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PE Plastic Packaging Market.- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Dow Inc.

- ExxonMobil Chemical Company

- LyondellBasell Industries Holdings B.V.

- WestRock Company

- Huhtamaki Oyj

- Printpack Inc.

- Sonoco Products Company

- Novolex Holdings, Inc.

- ProAmpac

- TC Transcontinental Packaging

- Constantia Flexibles Group GmbH

- Plastipak Holdings, Inc.

- Pactiv Evergreen Inc.

- Winpak Ltd.

- Coveris Holdings S.A.

- Interflex Group

Frequently Asked Questions

What is the current market size and projected growth rate of the PE Plastic Packaging Market?

The PE Plastic Packaging Market is estimated at USD 155.2 Billion in 2025 and is projected to reach USD 241.5 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 5.7% during the forecast period.

What are the primary drivers contributing to the growth of the PE Plastic Packaging Market?

Key drivers include the expanding food and beverage industry, rapid growth of e-commerce, increasing global population and urbanization, and the inherent cost-effectiveness and versatility of PE as a packaging material.

How do environmental concerns and regulations impact the PE Plastic Packaging Market?

Stringent environmental regulations, bans on single-use plastics, and negative public perception exert significant pressure, compelling the market to focus on sustainability, recyclability, and the incorporation of Post-Consumer Recycled (PCR) content to mitigate these challenges.

What are the key opportunities for innovation and growth in the PE Plastic Packaging Market?

Major opportunities lie in the increasing demand for sustainable and recyclable packaging solutions, technological advancements in recycling and PCR integration, expansion into high-growth emerging markets, and continuous innovation in light-weighting and barrier properties.

Which regions are expected to lead the growth in the PE Plastic Packaging Market?

The Asia Pacific region is anticipated to be the fastest-growing market due to rapid industrialization and urbanization, while North America and Europe will continue to drive innovation in sustainable packaging solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted