RF Power Semiconductor Market

RF Power Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702985 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

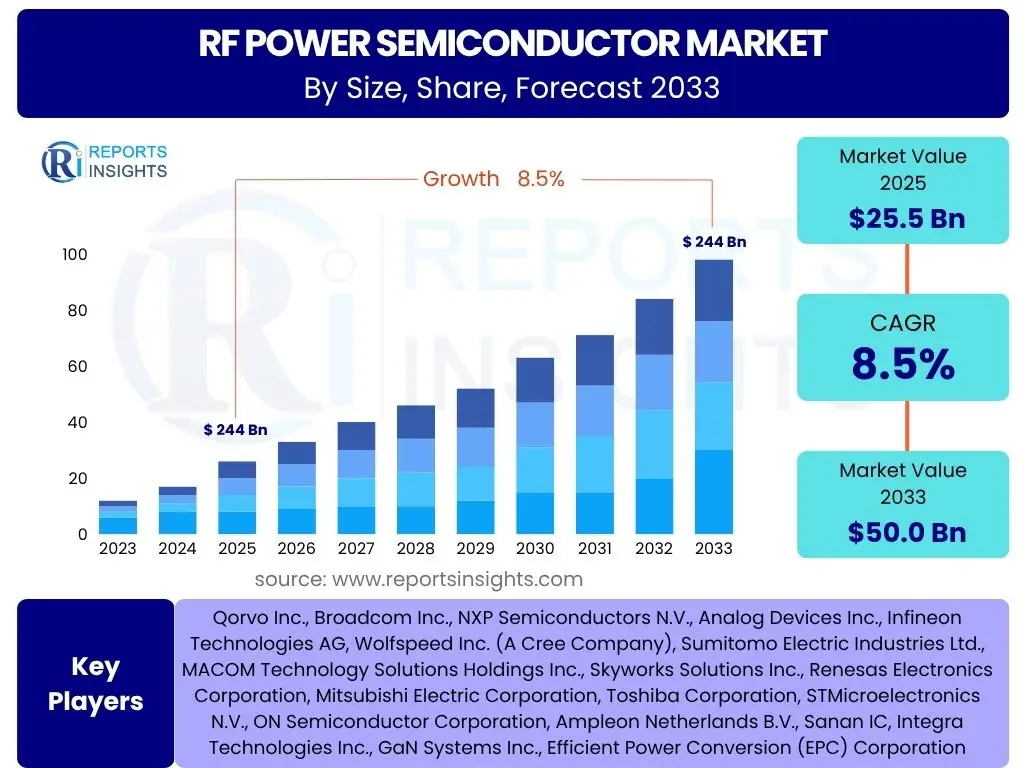

RF Power Semiconductor Market Size

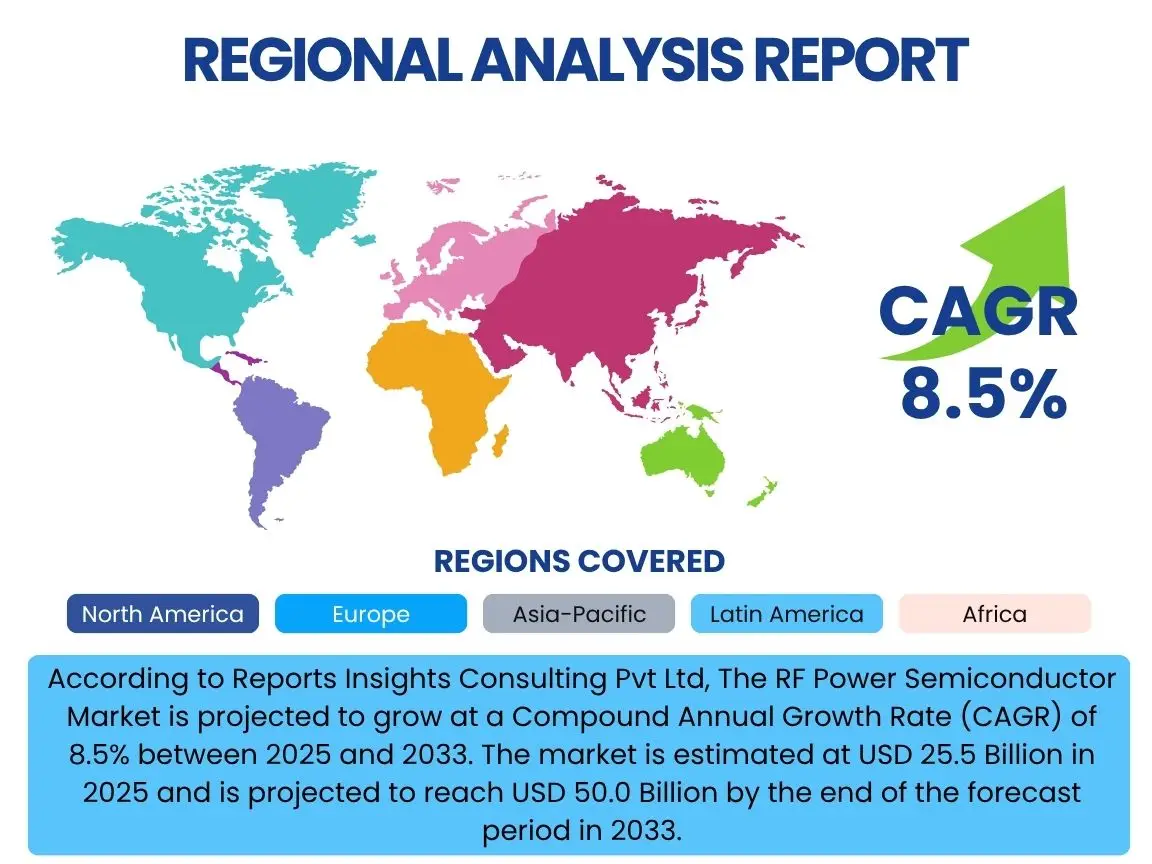

According to Reports Insights Consulting Pvt Ltd, The RF Power Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 50.0 Billion by the end of the forecast period in 2033.

Key RF Power Semiconductor Market Trends & Insights

User queries regarding the RF Power Semiconductor market frequently revolve around its dynamic evolution, driven by advancements in wireless communication and emerging technologies. A primary area of interest concerns the rapid deployment of 5G networks globally, which necessitates higher frequency and power capabilities from RF components. Another significant trend attracting attention is the increasing adoption of wide-bandgap (WBG) materials, particularly Gallium Nitride (GaN) and Silicon Carbide (SiC), due to their superior performance characteristics compared to traditional Silicon LDMOS, especially in high-frequency and high-power applications. The convergence of these material advancements with diverse application requirements is reshaping the market landscape.

Beyond network infrastructure, key insights highlight the growing integration of RF power semiconductors into new sectors, including advanced automotive radar systems, satellite communications, and industrial heating. There is a discernible shift towards more integrated and compact modules that offer enhanced power efficiency and reduced form factors, addressing the demand for smaller, lighter, and more capable electronic devices. Furthermore, the market is experiencing an emphasis on energy efficiency and thermal management solutions, critical for sustainable operation and extending device longevity, particularly as power densities increase. The ongoing research and development in these areas are indicative of a market poised for continuous innovation.

- Rapid global deployment of 5G and future 6G communication networks, driving demand for higher frequency and power components.

- Increasing adoption of Gallium Nitride (GaN) and Silicon Carbide (SiC) based RF power semiconductors due to their superior efficiency, power density, and thermal performance at higher frequencies.

- Growth in automotive radar and ADAS systems, requiring robust and precise RF power solutions for autonomous driving applications.

- Expansion of satellite communication and aerospace and defense sectors, boosting demand for high-reliability and high-power RF components.

- Development of advanced packaging technologies and integrated modules for enhanced power efficiency and reduced component size.

- Rising focus on energy efficiency and thermal management in RF power amplifier designs to meet environmental regulations and improve system reliability.

- Emergence of new industrial applications such as plasma generators, medical imaging, and RF heating, diversifying market opportunities.

AI Impact Analysis on RF Power Semiconductor

User inquiries about AI's impact on RF power semiconductors primarily focus on how artificial intelligence can optimize design processes, enhance operational efficiency, and potentially influence demand for these components. There is keen interest in AI's role in accelerating the development of new materials and device architectures, enabling more complex simulations and predictive modeling. Users are keen to understand if AI can reduce the time-to-market for novel RF solutions and improve the precision of their performance characteristics. Concerns often include the computational resources required and the integration challenges of AI tools into existing design workflows, alongside the potential for AI-driven optimization to lead to more efficient, yet potentially less volume-intensive, RF designs.

The application of AI in RF power semiconductor manufacturing and testing is also a significant area of user exploration, with expectations that AI can improve yield rates, identify defects more rapidly, and optimize production parameters. Beyond design and manufacturing, AI is anticipated to influence the demand for RF power semiconductors by enabling more sophisticated wireless communication systems, edge computing devices, and advanced IoT applications that rely heavily on optimized RF front-ends. The ability of AI to manage and optimize complex RF environments, such as those found in smart cities or industrial IoT, suggests a future where AI-driven decision-making directly impacts the performance requirements and subsequent demand for high-performance RF power semiconductors, pushing the boundaries of current capabilities and fostering continuous innovation in the sector.

- Accelerated design and optimization of RF power semiconductor devices through AI-driven simulation and modeling.

- Enhanced manufacturing processes and yield improvement using AI for predictive maintenance and quality control in wafer fabrication.

- Optimization of RF system performance and energy efficiency in applications through AI-powered adaptive algorithms.

- Facilitation of complex RF signal processing and intelligent network management in 5G/6G infrastructure, increasing demand for capable RF front-ends.

- Development of AI-enabled test and measurement equipment for precise characterization and verification of RF power components.

Key Takeaways RF Power Semiconductor Market Size & Forecast

The analysis of common user questions regarding the RF Power Semiconductor market size and forecast reveals a strong interest in understanding the core growth drivers and the future trajectory of this critical industry. Users frequently seek clarity on which applications will contribute most significantly to market expansion, emphasizing the role of telecommunications, particularly 5G, and emerging high-growth sectors like automotive and aerospace. Another key area of inquiry focuses on the technological shifts, specifically the transition towards wide-bandgap materials like GaN and SiC, and their expected impact on market value and competitive dynamics. The inherent volatility of global supply chains and geopolitical factors also feature prominently in user concerns, as these elements could influence market stability and accessibility of components.

A significant takeaway is the anticipated robust growth, underscored by continuous innovation in device materials and design, which is enabling higher performance and efficiency. The market's resilience is driven by the fundamental need for advanced RF capabilities across an expanding array of applications, from consumer devices to highly specialized defense systems. Furthermore, the forecast indicates a strategic shift in manufacturing and supply chain resilience, with increasing regionalization efforts aimed at mitigating risks. Overall, the market is poised for substantial expansion, characterized by technological evolution and diversification into new, high-value application areas, while navigating a complex global economic and political landscape to achieve its projected growth.

- The market is on a robust growth trajectory, primarily fueled by the accelerating global deployment of 5G and next-generation wireless communication networks.

- Wide-bandgap materials, notably GaN and SiC, are pivotal in driving innovation and market share, displacing traditional silicon in high-performance applications.

- Diversification of applications beyond traditional telecom, including automotive radar, aerospace and defense, and industrial heating, represents significant growth avenues.

- Increased focus on energy efficiency and miniaturization is a critical design imperative, impacting product development and market competitiveness.

- Asia Pacific is projected to remain the dominant region, driven by extensive telecommunications infrastructure development and strong manufacturing capabilities.

RF Power Semiconductor Market Drivers Analysis

The RF power semiconductor market is fundamentally driven by the relentless expansion of wireless communication technologies and the increasing demand for high-performance, energy-efficient electronic systems. The global rollout of 5G networks, followed by advancements towards 6G, creates an immense need for advanced RF components capable of operating at higher frequencies and power levels with enhanced efficiency. This technological push extends beyond mobile connectivity to encompass a broader ecosystem of interconnected devices, driving innovation in material science and device architectures. The imperative for faster data rates, lower latency, and greater network capacity acts as a primary catalyst for market growth.

Furthermore, the diversification of RF power semiconductor applications into new and rapidly evolving sectors significantly contributes to market expansion. The automotive industry, with its growing focus on autonomous driving and advanced driver-assistance systems (ADAS), requires robust RF solutions for radar, V2X communication, and in-cabin sensing. Similarly, the aerospace and defense sectors are continuously investing in sophisticated radar, electronic warfare, and satellite communication systems, all of which rely heavily on high-power and high-frequency RF semiconductors. This expanding utility across diverse, high-growth industries ensures a sustained demand for innovative RF power solutions, propelling the market forward.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| 5G Network Deployment & Evolution | +2.5% | Global, particularly Asia Pacific, North America, Europe | Short to Mid-term (2025-2030) |

| Increasing Adoption of Wide-Bandgap Materials (GaN, SiC) | +1.8% | Global, key manufacturing hubs (e.g., USA, Japan, Europe) | Mid to Long-term (2026-2033) |

| Growth in Automotive Radar & ADAS Systems | +1.5% | Europe, North America, China, Japan | Mid-term (2025-2031) |

| Expansion of Aerospace & Defense Applications | +1.2% | North America, Europe, Middle East | Long-term (2027-2033) |

RF Power Semiconductor Market Restraints Analysis

Despite robust growth prospects, the RF power semiconductor market faces several inherent restraints that could temper its expansion. One significant challenge is the high cost associated with research and development (R&D) and manufacturing of advanced RF power devices, especially those based on wide-bandgap materials like GaN and SiC. The specialized fabrication processes, stringent quality control measures, and high material costs contribute to higher unit prices, potentially limiting adoption in cost-sensitive applications. Furthermore, the complexity of designing high-frequency, high-power, and highly efficient RF circuits often necessitates extensive prototyping and testing, adding to the overall development expenditure and time-to-market.

Another major restraint involves the intricacies and potential disruptions within the global supply chain for raw materials and specialized components. The manufacturing of RF power semiconductors relies on a limited number of specialized suppliers for epitaxial wafers, substrates, and specific packaging materials. Geopolitical tensions, trade disputes, and unforeseen events such as pandemics can lead to significant supply chain bottlenecks, impacting production volumes and increasing lead times for essential components. These vulnerabilities can disrupt the market's stability, escalate costs, and delay the deployment of RF-dependent technologies, thereby posing a significant challenge to consistent market growth and accessibility for manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Manufacturing Costs | -1.0% | Global, particularly emerging economies | Short to Mid-term (2025-2029) |

| Supply Chain Disruptions and Geopolitical Tensions | -0.8% | Global, particularly impacting regions dependent on key material sources | Short-term (2025-2027) |

| Technological Complexity and Design Challenges | -0.5% | Global, impacting smaller enterprises | Mid-term (2026-2030) |

RF Power Semiconductor Market Opportunities Analysis

The RF power semiconductor market is presented with substantial opportunities arising from technological advancements and the proliferation of new application areas. The continuous evolution of wireless communication standards, including the ongoing deployment of 5G and the foundational research into 6G, creates a persistent demand for higher frequency, more efficient, and more compact RF power solutions. This pushes manufacturers to innovate in areas such as millimeter-wave (mmWave) technology and beamforming, unlocking new performance capabilities for network infrastructure, fixed wireless access, and advanced consumer devices. The expanding need for ubiquitous, high-speed connectivity worldwide fuels continuous investment and development within this segment.

Beyond traditional telecommunications, significant opportunities lie in the diversification of RF power semiconductor applications across various industries. The burgeoning market for electric vehicles and autonomous driving systems offers a vast potential for RF power devices in advanced radar, lidar, and vehicle-to-everything (V2X) communication modules. Similarly, the aerospace and defense sector's increasing demand for sophisticated radar systems, electronic warfare countermeasures, and satellite communication infrastructure provides a high-value segment for specialized, robust RF components. Furthermore, emerging industrial applications, such as advanced RF heating, plasma generation for manufacturing, and medical diagnostics, represent new frontiers for market penetration, driven by the unique advantages of RF power semiconductors in these niche yet growing sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of mmWave and Higher Frequency Technologies for 5G/6G | +1.8% | Global, particularly North America, Asia Pacific | Mid to Long-term (2026-2033) |

| Expansion into New Industrial and Automotive Applications | +1.5% | Europe, North America, China | Mid-term (2025-2031) |

| Growing Demand for Satellite Communications and Space Applications | +1.0% | North America, Europe, Middle East | Long-term (2027-2033) |

RF Power Semiconductor Market Challenges Impact Analysis

The RF power semiconductor market faces significant challenges, particularly concerning the rapid pace of technological obsolescence and the need for continuous innovation. As new wireless standards emerge and applications demand higher frequencies and power levels, existing technologies and manufacturing processes can quickly become outdated. This necessitates substantial and ongoing investments in research and development to keep pace with evolving requirements, placing considerable financial strain on companies. Furthermore, the design of RF power semiconductors operating at extremely high frequencies (e.g., millimeter-wave) requires overcoming complex physics and material science hurdles, pushing the limits of current capabilities in thermal management, efficiency, and signal integrity. The ability to manage and mitigate these technical complexities is crucial for market participants to remain competitive and deliver next-generation solutions, as failure to adapt can lead to rapid market share erosion.

Another prominent challenge is the intense competition within the market, driven by a blend of established players and agile startups. This competitive landscape puts constant pressure on pricing and necessitates differentiation through performance, efficiency, and specialized applications. Companies must continually demonstrate superior product attributes and cost-effectiveness to secure market positioning. Additionally, the market is vulnerable to global economic downturns and fluctuations in capital expenditure by telecommunication providers and other major end-users. Such economic instability can lead to delays in infrastructure deployment or reduced investments in new product development, directly impacting demand for RF power semiconductors. Navigating these economic uncertainties while maintaining a strong innovation pipeline is critical for sustained growth in this dynamic sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Innovation | -0.7% | Global | Ongoing |

| Intense Competition and Pricing Pressures | -0.6% | Global | Ongoing |

| Economic Volatility and Investment Cycles of End-Users | -0.4% | Global, particularly sensitive markets | Short to Mid-term (2025-2028) |

RF Power Semiconductor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global RF Power Semiconductor market, offering critical insights into its current dynamics, historical performance from 2019 to 2023, and a detailed forecast extending to 2033. The scope encompasses a thorough examination of market size, growth rates, key trends, and the impact of various drivers, restraints, opportunities, and challenges shaping the industry. It further segments the market by material type, frequency band, application, power output, and end-use, providing a granular view of market opportunities across diverse verticals and geographies. The report's objective is to equip stakeholders with actionable intelligence for strategic decision-making and competitive positioning within the evolving RF power semiconductor landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 50.0 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Qorvo Inc., Broadcom Inc., NXP Semiconductors N.V., Analog Devices Inc., Infineon Technologies AG, Wolfspeed Inc. (A Cree Company), Sumitomo Electric Industries Ltd., MACOM Technology Solutions Holdings Inc., Skyworks Solutions Inc., Renesas Electronics Corporation, Mitsubishi Electric Corporation, Toshiba Corporation, STMicroelectronics N.V., ON Semiconductor Corporation, Ampleon Netherlands B.V., Sanan IC, Integra Technologies Inc., GaN Systems Inc., Efficient Power Conversion (EPC) Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The RF power semiconductor market is extensively segmented to provide a granular understanding of its diverse applications and technological underpinnings. This segmentation categorizes the market based on several crucial parameters including the type of material used, the operating frequency range, the specific application areas, and the power output capabilities of the devices. Each segment reflects unique performance requirements, technological maturity, and market demand drivers, offering a detailed perspective on where current and future growth opportunities reside. Understanding these distinct segments is vital for stakeholders to tailor their product development strategies and market penetration efforts effectively.

- By Material:

- Gallium Nitride (GaN)

- LDMOS (Laterally Diffused Metal Oxide Semiconductor)

- Silicon Carbide (SiC)

- Gallium Arsenide (GaAs)

- Others (e.g., Silicon Germanium)

- By Frequency:

- Sub-6 GHz

- C-band (4-8 GHz)

- X-band (8-12 GHz)

- Ku-band (12-18 GHz)

- Ka-band (26.5-40 GHz)

- Millimeter Wave (mmWave) (Above 24 GHz)

- By Application:

- Telecommunications (Base Stations, Small Cells, Backhaul, Repeater, Active Antenna Systems)

- Aerospace & Defense (Radar, Electronic Warfare, Satellite Communication, Avionics)

- Automotive (Radar, Infotainment, V2X Communication, Autonomous Driving Sensors)

- Industrial (Plasma Generators, RF Heating, Welding, Lighting)

- Medical (MRI, Diathermy, Imaging)

- Consumer Electronics (Wi-Fi, IoT Devices, Drones)

- Others (e.g., Test & Measurement, Scientific Research)

- By Power Output:

- Low Power (Below 10W)

- Medium Power (10W-100W)

- High Power (Above 100W)

Regional Highlights

- North America: A significant market driven by early and extensive 5G network deployments, strong investment in aerospace and defense technologies, and a growing automotive industry pushing for advanced radar systems. The region benefits from robust R&D capabilities and a strong presence of key market players.

- Europe: Characterized by substantial investments in automotive electronics, particularly for ADAS and autonomous driving, as well as a mature telecommunications market upgrading to 5G. Strong industrial applications and increasing defense spending also contribute to regional demand for RF power semiconductors.

- Asia Pacific (APAC): Expected to be the largest and fastest-growing market due to massive investments in telecommunications infrastructure, especially 5G and future 6G networks, in countries like China, India, Japan, and South Korea. Rapid expansion of consumer electronics manufacturing and automotive production further fuels growth.

- Latin America: An emerging market with increasing adoption of 5G technologies and expanding telecommunication infrastructure. While smaller in scale compared to developed regions, it presents significant growth opportunities as digital transformation accelerates.

- Middle East and Africa (MEA): Growth is primarily driven by ongoing investments in telecommunication network upgrades, including 5G rollout, and increasing demand from defense sectors. Smart city initiatives and developing industrial sectors also contribute to the market's expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the RF Power Semiconductor Market.- Qorvo Inc.

- Broadcom Inc.

- NXP Semiconductors N.V.

- Analog Devices Inc.

- Infineon Technologies AG

- Wolfspeed Inc. (A Cree Company)

- Sumitomo Electric Industries Ltd.

- MACOM Technology Solutions Holdings Inc.

- Skyworks Solutions Inc.

- Renesas Electronics Corporation

- Mitsubishi Electric Corporation

- Toshiba Corporation

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Ampleon Netherlands B.V.

- Sanan IC

- Integra Technologies Inc.

- GaN Systems Inc.

- Efficient Power Conversion (EPC) Corporation

Frequently Asked Questions

What is an RF Power Semiconductor?

An RF (Radio Frequency) power semiconductor is an electronic device designed to generate or amplify high-frequency signals, typically in the range of kilohertz to terahertz, with significant power output. These semiconductors are crucial components in various wireless communication systems, radar systems, and industrial applications where efficient conversion and amplification of RF energy are required.

What are the primary applications of RF Power Semiconductors?

RF power semiconductors find extensive applications across diverse sectors. Key applications include telecommunications infrastructure (e.g., 5G base stations, small cells), aerospace and defense (e.g., radar, electronic warfare, satellite communications), automotive (e.g., advanced driver-assistance systems, in-cabin radar), industrial heating and plasma generation, and medical equipment (e.g., MRI machines, medical imaging).

What materials are commonly used in RF Power Semiconductors?

The most common materials used for RF power semiconductors are LDMOS (Laterally Diffused Metal Oxide Semiconductor) for lower frequencies, and increasingly, wide-bandgap materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) for higher frequency, higher power, and more efficient applications. Gallium Arsenide (GaAs) is also utilized for specific high-frequency and low-noise applications, particularly in front-end modules.

How does 5G deployment influence the RF Power Semiconductor market?

The widespread deployment of 5G networks significantly drives the RF power semiconductor market. 5G requires higher frequencies, wider bandwidths, and greater power efficiency compared to previous generations, necessitating advanced RF power amplifiers, particularly those based on GaN technology. This demand stems from the need for more base stations, massive MIMO antennas, and beamforming capabilities.

What is the future outlook for the RF Power Semiconductor market?

The future outlook for the RF power semiconductor market is highly positive, driven by the ongoing evolution of wireless communication technologies (including 6G research), increasing adoption of autonomous vehicles, advancements in satellite communications, and the expansion of industrial and medical applications. Continuous innovation in wide-bandgap materials and integrated module designs will further enhance device performance and unlock new market opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted