Rail Equipment Market

Rail Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700939 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

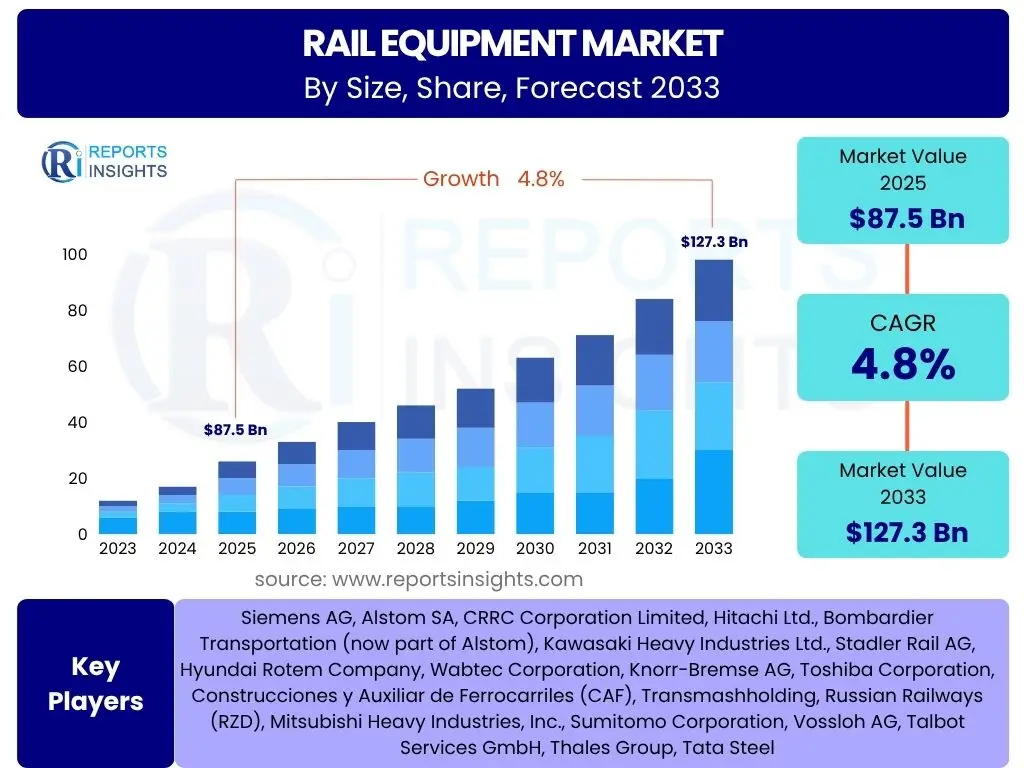

Rail Equipment Market Size

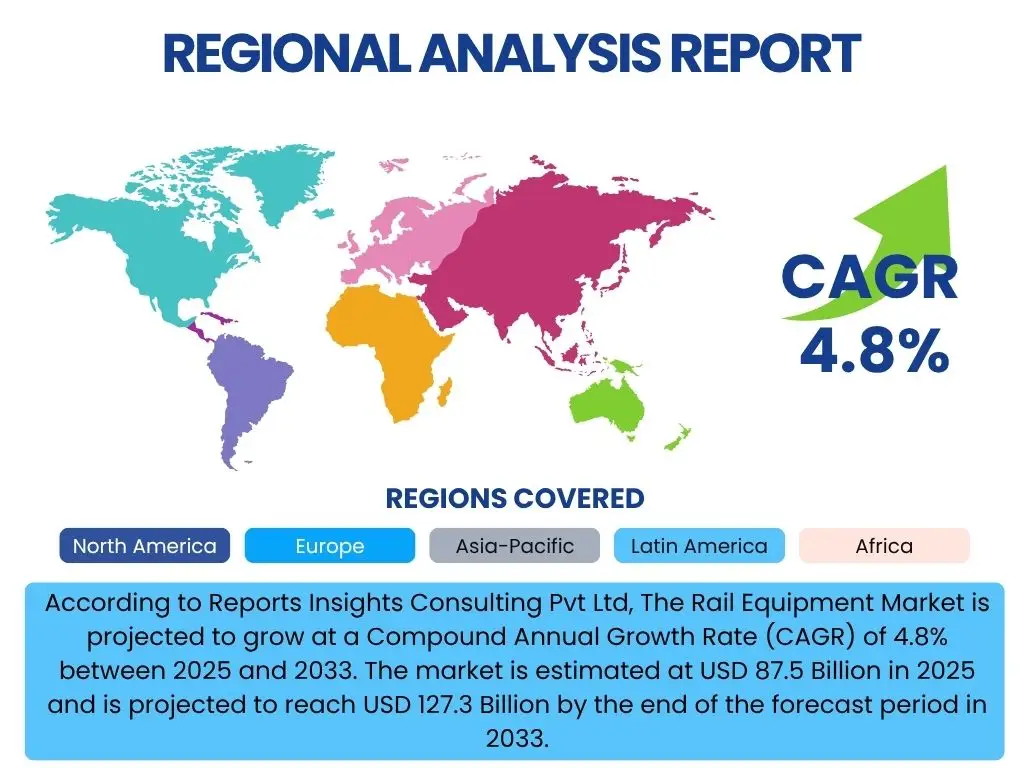

According to Reports Insights Consulting Pvt Ltd, The Rail Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 87.5 Billion in 2025 and is projected to reach USD 127.3 Billion by the end of the forecast period in 2033.

Key Rail Equipment Market Trends & Insights

The global rail equipment market is witnessing transformative trends driven by a confluence of technological advancements, evolving urban landscapes, and a heightened focus on sustainability. Users frequently inquire about the impact of digitalization, the push for eco-friendly solutions, and the expansion of high-speed rail networks. These inquiries underscore a collective interest in understanding how the industry is adapting to modern demands for efficiency, connectivity, and environmental responsibility.

Digitalization, encompassing the Internet of Things (IoT), big data analytics, and advanced connectivity solutions, is revolutionizing operational efficiency and maintenance practices across the rail sector. This trend enables predictive maintenance, real-time monitoring of assets, and optimized traffic management, leading to significant cost savings and improved safety. Concurrently, the imperative for sustainable transport solutions is accelerating the adoption of electric and hybrid locomotives, lightweight materials, and energy-efficient designs, aligning with global decarbonization goals.

Furthermore, the continuous expansion of high-speed rail networks, particularly in Asia Pacific and Europe, represents a major growth driver, addressing increasing passenger demand for faster and more comfortable intercity travel. Urbanization continues to fuel investment in metro, tram, and light rail systems, necessitating modern rolling stock and advanced signaling solutions to manage dense populations. Modernization of existing freight rail infrastructure to support growing trade volumes and improve logistics efficiency also stands out as a critical trend shaping market dynamics.

- Digitalization and implementation of smart rail technologies for enhanced operational efficiency.

- Increasing focus on sustainability, leading to adoption of electric and hydrogen-powered trains and eco-friendly materials.

- Expansion of high-speed rail networks globally to meet rising passenger demand and reduce travel times.

- Modernization of aging rail infrastructure and rolling stock in developed economies.

- Growth in urban rail transit systems, including metros, trams, and light rail, due to rapid urbanization.

- Development of advanced signaling and communication systems for improved safety and capacity.

AI Impact Analysis on Rail Equipment

Users frequently express curiosity about the transformative potential of Artificial Intelligence (AI) within the rail equipment sector, specifically querying its applications in operational efficiency, safety, and maintenance. Common themes include how AI can reduce costs, prevent failures, and enhance decision-making in complex railway environments. The general expectation is that AI will be a core enabler of the next generation of intelligent and autonomous rail systems, addressing longstanding industry challenges.

AI's impact on rail equipment is profound, primarily through enabling sophisticated predictive maintenance capabilities. By analyzing vast datasets from sensors on trains and infrastructure, AI algorithms can predict equipment failures before they occur, allowing for proactive repairs and significantly reducing downtime and maintenance costs. This shifts the industry from reactive repairs to a more efficient, preventative approach, ensuring higher asset utilization and operational reliability across the network.

Beyond maintenance, AI is crucial for optimizing traffic management and enhancing safety systems. AI-powered solutions can analyze real-time traffic data, optimize train scheduling, and dynamically adjust routes to prevent congestion and improve energy efficiency. In terms of safety, AI contributes through advanced object detection, anomaly detection in track conditions, and autonomous train operation pilot programs, aiming to minimize human error and enhance overall network security. The integration of AI also facilitates data-driven decision-making, providing operators with actionable insights for network planning, resource allocation, and service optimization, thereby contributing to a more resilient and responsive rail ecosystem.

- Predictive maintenance and fault detection, leading to reduced downtime and operational costs.

- Optimization of train scheduling and traffic management for increased efficiency and energy savings.

- Enhanced safety systems through AI-powered anomaly detection and obstacle recognition.

- Development of autonomous or semi-autonomous train operation capabilities.

- Data-driven insights for improved network planning, resource allocation, and operational decision-making.

- Automated inspection of tracks and rolling stock for early identification of defects.

Key Takeaways Rail Equipment Market Size & Forecast

Common user questions regarding the rail equipment market size and forecast often revolve around identifying the primary growth drivers, the influence of technological advancements, and the most promising regional markets. There is also significant interest in understanding how global sustainability targets and infrastructure spending policies will shape the industry's trajectory. These inquiries highlight a need for clarity on the foundational elements propelling market expansion and where future investments are likely to yield the highest returns.

A key takeaway from the market size and forecast analysis is the consistent growth trajectory of the rail equipment sector, primarily propelled by increasing government investments in public transport infrastructure and the global push for sustainable transportation solutions. Urbanization continues to be a major catalyst, driving demand for modern metro and light rail systems in rapidly expanding cities worldwide. Furthermore, the imperative to modernize aging railway networks in developed economies, coupled with ambitious new high-speed rail projects in emerging markets, ensures sustained demand for a wide range of rail equipment, from rolling stock to advanced signaling systems.

Technological innovation, particularly in digitalization and automation, is emerging as a critical competitive differentiator and a significant growth enabler, allowing for more efficient, safer, and environmentally friendly rail operations. The market's resilience is also underscored by the diversification of demand across passenger and freight segments, each driven by distinct yet complementary factors such as population growth, e-commerce expansion, and global trade volumes. While regional dynamics vary, the overall outlook remains positive, with Asia Pacific poised to lead growth, followed by substantial opportunities in Europe and North America through infrastructure upgrades and decarbonization efforts.

- Sustained market growth driven by global infrastructure development and urbanization.

- Significant investment in high-speed rail projects and urban transit systems is a primary growth engine.

- Technological advancements, including digitalization and AI, are critical for efficiency and market competitiveness.

- Demand for eco-friendly and energy-efficient rail solutions is accelerating market adoption.

- Asia Pacific continues to be the dominant and fastest-growing region, fueled by rapid expansion and modernization.

Rail Equipment Market Drivers Analysis

The rail equipment market is significantly influenced by a multitude of interconnected drivers, each contributing to its expansion and evolution. Governments globally are increasingly recognizing the importance of efficient and sustainable transportation networks, leading to substantial public and private investments in railway infrastructure. This surge in investment is directly correlated with the demand for new rolling stock, signaling systems, and maintenance equipment, driving the market forward.

Rapid urbanization and population growth, particularly in developing economies, are creating an urgent need for robust public transit solutions. This demographic shift necessitates the development and expansion of metro, tram, and light rail systems, thereby increasing the demand for urban rail equipment. Concurrently, the growing emphasis on environmental sustainability and the need to reduce carbon emissions are prompting a shift from road and air transport to rail, which is inherently more energy-efficient and less polluting. This environmental imperative is accelerating the adoption of electric and low-emission rail technologies.

Furthermore, the global increase in trade volumes and the expansion of e-commerce are driving the modernization and expansion of freight rail networks. Efficient freight rail is crucial for supply chain resilience and cost-effective movement of goods, leading to investments in advanced freight wagons, locomotives, and digital logistics solutions. Technological advancements, including smart rail systems, automation, and predictive maintenance capabilities, also serve as significant drivers, enhancing operational efficiency, safety, and capacity, thereby making rail a more attractive and viable transport option.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Government Initiatives & Infrastructure Investment | +1.5% - +2.0% | Global, particularly APAC (China, India), Europe, North America | 2025-2033 (Long-term) |

| Urbanization & Demand for Public Transit | +1.0% - +1.5% | Global, with high impact in emerging economies | 2025-2033 (Long-term) |

| Focus on Sustainable & Green Transportation | +0.8% - +1.2% | Europe, North America, followed by APAC | 2025-2033 (Long-term) |

| Growth in Freight Transportation & E-commerce | +0.7% - +1.0% | North America, APAC (China, India), Europe | 2025-2033 (Long-term) |

Rail Equipment Market Restraints Analysis

Despite robust growth drivers, the rail equipment market faces several significant restraints that can impede its expansion. One of the primary barriers is the exceptionally high initial capital expenditure required for large-scale railway projects. Building or modernizing rail infrastructure, including tracks, signaling systems, and rolling stock, demands substantial financial commitment, which can be a deterrent, especially for developing nations or private investors.

Another considerable restraint is the extended project gestation period often associated with railway development. From feasibility studies and land acquisition to construction and testing, these projects can span several years, if not decades. Such lengthy timelines tie up capital for extended periods and expose projects to economic uncertainties, political shifts, and changes in public policy, increasing overall risk and potentially delaying market adoption of new equipment.

Furthermore, stringent regulatory frameworks and complex approval processes pose significant challenges. Railway operations are subject to rigorous safety standards, environmental regulations, and technical specifications that vary by region and country. Navigating these diverse and often evolving regulatory landscapes can add significant costs, time, and complexity to project development and equipment deployment. Competition from other modes of transport, such as road and air, particularly for passenger travel over shorter distances and high-value freight, also acts as a restraint, limiting the market share of rail in certain segments. Additionally, geopolitical instability and supply chain disruptions can impact the availability and cost of raw materials and components, further constraining market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.2% - -1.8% | Global, higher impact in developing regions | 2025-2033 (Long-term) |

| Long Project Gestation Periods | -0.8% - -1.3% | Global, across all major projects | 2025-2033 (Long-term) |

| Complex Regulatory & Approval Processes | -0.7% - -1.1% | Europe, North America, emerging economies | 2025-2033 (Long-term) |

| Competition from Other Transport Modes | -0.5% - -0.9% | Global, particularly for intercity passenger and specific freight | 2025-2033 (Long-term) |

Rail Equipment Market Opportunities Analysis

The rail equipment market is replete with opportunities for growth and innovation, particularly as global priorities shift towards sustainability and smart infrastructure. One significant area of opportunity lies in the widespread need for modernization of aging railway infrastructure across developed nations. Many existing networks require significant upgrades to improve safety, increase capacity, and integrate new technologies, creating substantial demand for modern signaling systems, track components, and refurbished rolling stock.

The development and deployment of smart railway systems, leveraging technologies such as IoT, AI, and big data analytics, present another lucrative opportunity. These systems can enable predictive maintenance, autonomous operations, real-time diagnostics, and enhanced security, transforming traditional rail operations into highly efficient and intelligent networks. Investment in digital solutions and cybersecurity for rail infrastructure and equipment will be paramount for securing these advancements.

Furthermore, the expansion into emerging markets, particularly in Africa, Latin America, and parts of Asia that are undergoing rapid industrialization and urbanization, offers vast untapped potential. These regions require foundational rail networks for both passenger and freight transport, presenting opportunities for new installations and complete system deployments. Public-private partnerships (PPPs) are increasingly facilitating these large-scale projects, allowing governments to leverage private sector expertise and funding, thereby mitigating the financial burden and accelerating project execution. The growing emphasis on multimodal transport solutions, integrating rail with other forms of logistics, also opens new avenues for specialized equipment and interconnected systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Modernization of Aging Infrastructure | +1.0% - +1.5% | Europe, North America, Japan | 2025-2033 (Mid to Long-term) |

| Development of Smart Railway Systems & Digitalization | +0.9% - +1.3% | Global, with strong adoption in developed markets | 2025-2033 (Long-term) |

| Expansion into Emerging Markets | +0.8% - +1.2% | Africa, Latin America, Southeast Asia | 2025-2033 (Long-term) |

| Public-Private Partnerships (PPPs) | +0.6% - +1.0% | Global, particularly for large-scale projects | 2025-2033 (Long-term) |

Rail Equipment Market Challenges Impact Analysis

The rail equipment market, while exhibiting robust growth, is not without its significant challenges that can impede progress and profitability. One pervasive challenge is the increasing threat of cybersecurity attacks. As rail systems become more digitized and interconnected, they become vulnerable to cyber threats that can disrupt operations, compromise sensitive data, and even endanger passenger safety. Protecting critical infrastructure from sophisticated cyberattacks requires continuous investment in advanced security solutions and expertise, adding to operational costs.

Another notable challenge is the persistent shortage of skilled labor across various segments of the rail industry, from engineers and technicians to maintenance personnel. The highly specialized nature of rail equipment development, manufacturing, and maintenance demands a workforce with specific expertise. An aging workforce and a lack of new talent entering the sector can lead to project delays, increased operational costs, and a hindrance to the adoption of new technologies.

Economic volatility, including inflation, currency fluctuations, and recessions, presents a substantial challenge. Large-scale rail projects often involve long planning and execution phases, making them susceptible to economic downturns that can lead to budget cuts, project postponements, or cancellations. Such economic uncertainties affect investment decisions and market stability. Additionally, environmental regulations, public opposition to new rail projects due to land acquisition or noise concerns, and unforeseen cost overruns further complicate project delivery and can significantly impact the financial viability of new rail ventures and the demand for associated equipment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats | -0.9% - -1.3% | Global, particularly in technologically advanced regions | 2025-2033 (Ongoing) |

| Skilled Labor Shortage | -0.7% - -1.1% | Europe, North America, Japan | 2025-2033 (Long-term) |

| Economic Volatility & Funding Constraints | -0.6% - -1.0% | Global, sensitive to macroeconomic conditions | 2025-2033 (Variable) |

| Environmental Regulations & Public Opposition | -0.5% - -0.8% | Europe, North America, densely populated APAC regions | 2025-2033 (Ongoing) |

Rail Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global rail equipment market, offering detailed insights into market size, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. The report segments the market by product type, application, end-user, and technology, providing a granular view of market dynamics across various categories. It also includes an extensive regional analysis, covering major geographical markets and their respective contributions to the overall market landscape. The study profiles key industry players, offering a competitive analysis to understand the market's structure and strategic developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 87.5 Billion |

| Market Forecast in 2033 | USD 127.3 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Alstom SA, CRRC Corporation Limited, Hitachi Ltd., Bombardier Transportation (now part of Alstom), Kawasaki Heavy Industries Ltd., Stadler Rail AG, Hyundai Rotem Company, Wabtec Corporation, Knorr-Bremse AG, Toshiba Corporation, Construcciones y Auxiliar de Ferrocarriles (CAF), Transmashholding, Russian Railways (RZD), Mitsubishi Heavy Industries, Inc., Sumitomo Corporation, Vossloh AG, Talbot Services GmbH, Thales Group, Tata Steel |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The rail equipment market is intricately segmented to provide a comprehensive understanding of its diverse components and their respective growth trajectories. These segmentations allow for a detailed analysis of specific product types, applications, end-users, and technologies, enabling stakeholders to identify niche opportunities and tailor strategies effectively. The "By Product Type" segment highlights the distinction between rolling stock, which includes all types of trains and wagons, and infrastructure, covering the fixed assets like tracks and signaling systems, along with services vital for maintenance and modernization. This breakdown is crucial for understanding where capital is primarily allocated within the rail ecosystem.

The "By Application" segmentation distinguishes between passenger and freight transport, recognizing the unique demands and equipment specifications for each. Passenger transport further divides into urban, intercity, and high-speed rail, reflecting varying needs from daily commuting to long-distance travel. Freight transport, on the other hand, considers different cargo types like bulk, containerized, and specialized goods, influencing wagon design and locomotive power. This distinction is fundamental for manufacturers and service providers targeting specific operational requirements and cargo volumes.

Furthermore, the market is segmented "By End-User" into public and private operators, acknowledging the different ownership and operational models prevalent globally. Public entities often drive large infrastructure projects, while private operators might focus on niche freight services or specific routes. The "By Technology" segment classifies the market based on conventional rail, high-speed rail, and light rail/metro, highlighting the technological advancements and investment priorities in different rail system types. Each segment is critical for market participants to identify their core competencies and align with global and regional market demands effectively.

- By Product Type:

- Rolling Stock: Locomotives (Diesel, Electric, Hybrid), Passenger Coaches (High-Speed, Intercity, Commuter), Freight Wagons (Open, Closed, Flat, Tank), Metros/Subways, Tramways & Light Rail Vehicles

- Infrastructure: Tracks, Bridges & Tunnels, Signaling Systems (CBTC, ERTMS, PTC), Electrification Systems (Catenary, Third Rail), Stations & Depots

- Services: Maintenance, Repair & Overhaul (MRO), Modernization & Refurbishment, Consulting & Engineering

- By Application:

- Passenger Transport (Urban, Intercity, High-Speed)

- Freight Transport (Bulk, Containerized, Special Cargo)

- By End-User:

- Public Operators

- Private Operators

- By Technology:

- Conventional Rail

- High-Speed Rail

- Light Rail & Metro

Regional Highlights

The global rail equipment market exhibits significant regional variations, each driven by unique economic, infrastructural, and regulatory factors. Asia Pacific (APAC) stands out as the largest and fastest-growing region, primarily fueled by massive infrastructure investments in countries like China, India, and Japan. China continues to dominate high-speed rail expansion and urban metro development, while India is rapidly modernizing its vast network and developing new corridors. Southeast Asian nations are also witnessing increased investment in rail to support burgeoning populations and economic growth, making APAC a critical hub for both manufacturing and demand for all types of rail equipment.

Europe represents a mature yet highly innovative market, characterized by extensive high-speed networks, a strong focus on decarbonization, and cross-border connectivity initiatives. Countries such as Germany, France, and the UK are investing heavily in upgrading existing lines, electrifying routes, and integrating advanced digital signaling systems like ERTMS. The region is a leader in sustainable rail solutions, including hydrogen-powered trains and lightweight materials, driven by stringent environmental regulations and public demand for greener transport. This focus ensures continuous demand for sophisticated and energy-efficient rail equipment.

North America is primarily driven by the modernization of its freight rail network, which is critical for the movement of goods across the continent. While passenger rail, particularly high-speed, has seen slower adoption compared to Europe or APAC, there is increasing investment in improving commuter rail systems and regional passenger services. The focus on enhancing rail safety, efficiency, and incorporating digital technologies like Positive Train Control (PTC) systems significantly impacts equipment demand. The region also sees a push for infrastructure revitalization and replacement of aging rolling stock.

Latin America's rail equipment market is characterized by ongoing infrastructure development, particularly for commodity transport and urban mobility projects in major cities. Countries like Brazil, Mexico, and Argentina are investing in new lines and upgrading existing ones to support economic growth and address urbanization challenges. While the pace of development can be influenced by economic stability, the long-term potential for rail expansion remains substantial. The Middle East and Africa (MEA) region is emerging as a significant market, with ambitious new rail projects aimed at diversifying economies, improving regional connectivity, and supporting mega-events. Countries in the Gulf Cooperation Council (GCC) are investing in extensive passenger and freight networks, requiring advanced and often customized rail equipment. African nations are also gradually investing in rail infrastructure to connect key economic centers and facilitate trade, though these projects often face funding and logistical challenges.

- Asia Pacific (APAC): Dominant market, driven by extensive high-speed rail development (China, Japan), urban metro expansion (India, Southeast Asia), and robust manufacturing capabilities.

- Europe: Mature market with continuous investment in high-speed rail upgrades, decarbonization efforts, and advanced signaling systems; strong focus on R&D and sustainable solutions.

- North America: Focus on freight rail modernization, intermodal transport, and revitalization of passenger rail infrastructure, with increasing adoption of digital technologies.

- Latin America: Growing market driven by infrastructure development for commodity exports and increasing demand for urban rail solutions in major cities.

- Middle East and Africa (MEA): Emerging market with significant planned investments in new rail networks for economic diversification and regional connectivity.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Rail Equipment Market.- Siemens AG

- Alstom SA

- CRRC Corporation Limited

- Hitachi Ltd.

- Kawasaki Heavy Industries Ltd.

- Stadler Rail AG

- Hyundai Rotem Company

- Wabtec Corporation

- Knorr-Bremse AG

- Toshiba Corporation

- Construcciones y Auxiliar de Ferrocarriles (CAF)

- Transmashholding

- Mitsubishi Heavy Industries, Inc.

- Sumitomo Corporation

- Vossloh AG

- Talbot Services GmbH

- Thales Group

- Tata Steel

Frequently Asked Questions

What is the projected growth of the rail equipment market?

The rail equipment market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated value of USD 127.3 Billion by 2033 from USD 87.5 Billion in 2025. This growth is primarily driven by global infrastructure investments and the increasing demand for sustainable transportation solutions.

What are the primary drivers for the rail equipment market?

Key drivers include substantial government and private investments in railway infrastructure, rapid urbanization leading to increased demand for public transit, and a global shift towards sustainable and green transportation. Additionally, the growth in freight transportation, boosted by e-commerce, and continuous technological advancements further propel market expansion.

How is AI transforming the rail equipment industry?

Artificial Intelligence is significantly transforming the rail equipment industry by enabling advanced predictive maintenance, optimizing train scheduling and traffic management, and enhancing safety systems through real-time anomaly detection. AI also facilitates the development of autonomous operations and provides data-driven insights for improved operational efficiency and decision-making across the rail network.

Which regions are expected to show significant growth in the rail equipment market?

Asia Pacific is expected to demonstrate the most significant growth, driven by extensive high-speed rail and urban metro developments in countries like China and India. Europe will continue its strong growth through modernization and decarbonization initiatives, while North America focuses on freight rail and passenger rail infrastructure upgrades. Emerging markets in Latin America and MEA also offer substantial growth potential with new project developments.

What are the key challenges faced by the rail equipment market?

Major challenges include the high initial capital expenditure for projects, long project gestation periods, and complex regulatory frameworks that vary by region. Additionally, cybersecurity threats to increasingly digitized systems, a persistent shortage of skilled labor, and susceptibility to economic volatility present significant hurdles to market growth and stability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted