Radiation Detection In Industrial and Scientific Market

Radiation Detection In Industrial and Scientific Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708636 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

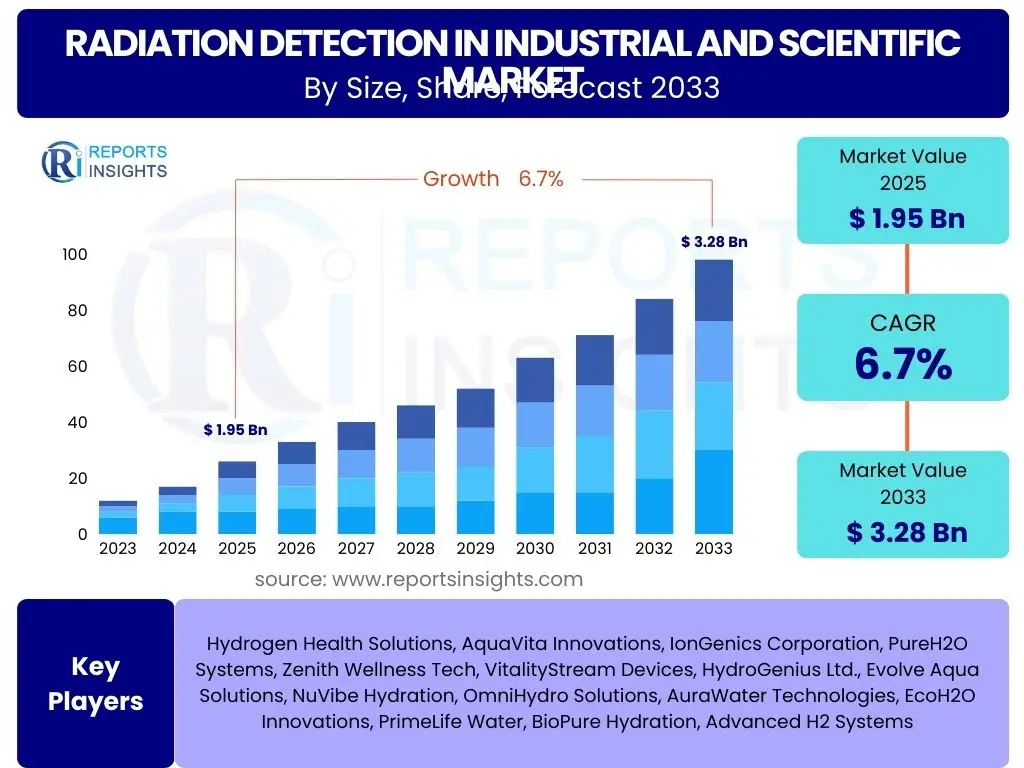

Radiation Detection In Industrial and Scientific Market Size

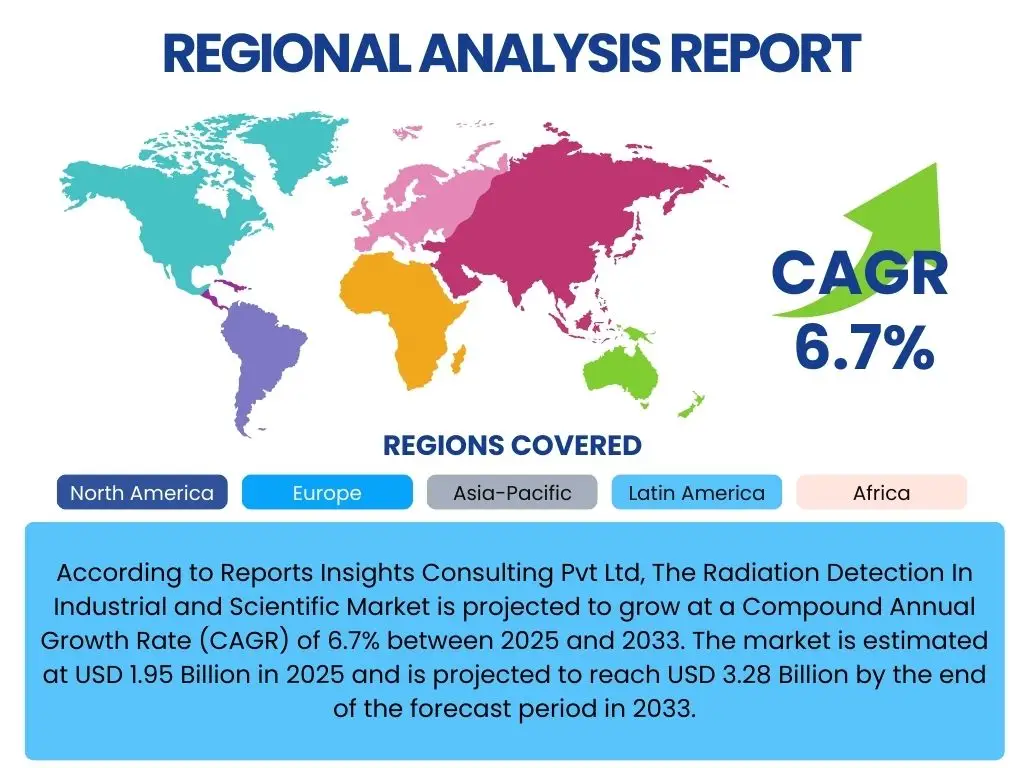

According to Reports Insights Consulting Pvt Ltd, The Radiation Detection In Industrial and Scientific Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 1.95 Billion in 2025 and is projected to reach USD 3.28 Billion by the end of the forecast period in 2033.

Key Radiation Detection In Industrial and Scientific Market Trends & Insights

The radiation detection market, particularly within industrial and scientific applications, is experiencing significant transformation driven by technological advancements and evolving regulatory landscapes. User inquiries frequently highlight the demand for more sensitive, accurate, and miniaturized detection systems, reflecting a broader trend towards enhanced safety and operational efficiency. There is also a keen interest in integrated solutions that offer real-time data and remote monitoring capabilities, moving beyond traditional standalone detectors. Furthermore, the push for sustainable and environmentally conscious practices is influencing the development of detectors that can operate effectively in diverse and challenging conditions, emphasizing robustness and reliability.

Another prominent area of interest among users revolves around the integration of advanced data processing and connectivity features. The market is moving towards intelligent detection systems capable of not only identifying radiation but also analyzing patterns, predicting potential hazards, and seamlessly communicating data to centralized platforms. This shift is particularly evident in nuclear power plants, research facilities, and industrial settings where continuous, precise monitoring is critical. The drive for cost-effective and low-maintenance solutions also underpins many of these trends, as organizations seek to optimize their operational expenditures while maintaining high safety standards.

- Miniaturization and portability of detection devices for versatile applications.

- Increased demand for real-time, high-sensitivity, and high-resolution radiation monitoring.

- Integration of IoT and cloud connectivity for remote data access and management.

- Development of advanced semiconductor detectors offering improved performance.

- Growing adoption of spectroscopic detectors for radionuclide identification.

- Emphasis on multi-purpose detectors capable of identifying various radiation types.

- Customization of solutions for specific industrial and scientific research needs.

AI Impact Analysis on Radiation Detection In Industrial and Scientific

User queries regarding the impact of Artificial Intelligence (AI) on radiation detection reveal a strong expectation for enhanced capabilities, particularly in data analysis, anomaly detection, and predictive maintenance. Stakeholders anticipate AI to revolutionize how vast amounts of sensor data are processed, leading to more accurate and faster identification of radiation sources and patterns that might otherwise be missed by human observation or traditional algorithms. There is significant interest in AI's role in reducing false positives and improving the reliability of alarms, which is crucial in high-stakes environments like nuclear facilities or security checkpoints. Moreover, users are looking for AI to automate complex calibration processes and optimize detector performance over time, extending equipment lifespan and reducing operational costs.

The integration of AI is also viewed as a catalyst for developing next-generation intelligent detectors capable of learning from historical data and adapting to new operational conditions. This adaptability is expected to be particularly beneficial in dynamic research environments or industrial settings where conditions can change rapidly. Concerns often center around the initial investment costs, the need for specialized AI expertise, and ensuring data privacy and security, especially when sensitive information is involved. However, the overarching sentiment is one of optimism, with users envisioning AI as a transformative force that will lead to more autonomous, efficient, and robust radiation detection systems, ultimately enhancing safety and operational intelligence across various sectors.

- Enhanced data analysis for faster and more accurate identification of radiation sources.

- Automated anomaly detection and pattern recognition to reduce false positives.

- Predictive maintenance for detection equipment, improving reliability and lifespan.

- Optimization of sensor calibration and system performance through machine learning algorithms.

- Development of intelligent detection systems capable of adaptive monitoring.

- Integration of AI for real-time risk assessment and decision-making support.

- Improved classification and characterization of radioactive materials.

Key Takeaways Radiation Detection In Industrial and Scientific Market Size & Forecast

Key takeaways from the Radiation Detection in Industrial and Scientific market size and forecast frequently center on the robust growth trajectory and the underlying factors driving this expansion. Users consistently inquire about the primary applications fueling demand, such as nuclear power, healthcare, and industrial safety, and how these sectors contribute to market expansion. The forecast indicates sustained growth, underscoring the increasing global emphasis on safety, environmental monitoring, and advancements in scientific research that necessitate sophisticated radiation detection capabilities. Understanding the long-term potential requires considering the interplay of technological innovation, regulatory mandates, and geopolitical factors impacting energy and security sectors.

Furthermore, the market's resilience and forward momentum are attributed to continuous innovations in detector technology, making devices more sensitive, compact, and capable of real-time analysis. The increasing investment in R&D across various scientific disciplines, coupled with the expansion of nuclear energy programs in certain regions, directly translates into a greater demand for advanced detection solutions. Stakeholders are particularly interested in the segment-wise growth, discerning which technologies and applications are poised for the most significant uptake, thus informing strategic investment and development decisions within the market ecosystem.

- Market projected for consistent growth through 2033, driven by safety and research needs.

- Significant opportunities emerging from advancements in nuclear energy and medical diagnostics.

- Technological innovation, particularly in solid-state and semiconductor detectors, is a primary growth engine.

- Increasing regulatory stringency across industries demanding advanced detection solutions.

- Regional variations in growth, with Asia Pacific exhibiting strong expansion due to industrialization.

- Demand for integrated, smart, and connected detection systems is accelerating market evolution.

Radiation Detection In Industrial and Scientific Market Drivers Analysis

The radiation detection market is significantly propelled by several key drivers, primarily stemming from the increasing global focus on safety, security, and scientific advancement. The expansion of nuclear power generation capacity worldwide, as countries seek cleaner energy sources, inherently drives demand for sophisticated radiation monitoring equipment to ensure operational safety and regulatory compliance. Concurrently, the burgeoning fields of medical diagnostics and therapy, particularly in oncology and imaging, rely heavily on precise radiation measurement, contributing substantially to market growth. Additionally, stringent environmental regulations governing industrial emissions and waste disposal necessitate advanced detectors for real-time environmental monitoring, thereby expanding the market scope.

Beyond energy and healthcare, the persistent threat of nuclear proliferation and terrorism mandates robust homeland security and defense applications, fostering innovation and adoption of advanced detection systems. Research and academic institutions also serve as a crucial driver, constantly pushing the boundaries of material science, high-energy physics, and life sciences, all of which require cutting-edge radiation detection tools. The convergence of these factors creates a strong, sustained demand across various sectors, ensuring the market's continued upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Nuclear Power Generation Capacity | +0.8% | Asia Pacific, Europe, North America | Long-term (2030-2033) |

| Increasing Demand in Medical Diagnostics & Therapy | +0.7% | North America, Europe, China, India | Mid-term (2027-2030) |

| Stringent Safety & Environmental Regulations | +0.6% | Europe, North America, Japan | Short-term (2025-2027) |

| Expansion of Homeland Security & Defense Applications | +0.5% | North America, Europe, Middle East | Mid-term (2027-2030) |

| Advancements in Scientific Research & Development | +0.4% | Global, particularly developed economies | Long-term (2030-2033) |

Radiation Detection In Industrial and Scientific Market Restraints Analysis

Despite the strong growth drivers, the Radiation Detection in Industrial and Scientific market faces several notable restraints that could temper its expansion. One significant challenge is the high initial cost associated with advanced radiation detection equipment, particularly for high-sensitivity and specialized instruments. This cost barrier can limit adoption, especially for smaller research facilities or industrial operations with constrained budgets. Additionally, the complexity of regulatory frameworks and the need for rigorous certification processes can be burdensome, increasing time-to-market for new technologies and potentially stifling innovation due to compliance overheads.

Another crucial restraint is the scarcity of highly skilled personnel required to operate, maintain, and interpret data from sophisticated radiation detection systems. The specialized knowledge demanded for effective deployment and analysis can create workforce shortages, particularly in emerging markets. Furthermore, public perception regarding radiation risks, often influenced by historical events or misinformation, can lead to resistance against the expansion of nuclear-related industries or research, indirectly impacting the demand for detection technologies. These factors collectively present significant hurdles that market participants must address to unlock the full potential of the sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Equipment | -0.7% | Global, particularly developing economies | Mid-term (2027-2030) |

| Complex Regulatory & Certification Processes | -0.6% | Europe, North America | Long-term (2030-2033) |

| Shortage of Skilled Professionals | -0.5% | Global, especially emerging markets | Short-term (2025-2027) |

| Public Perception of Radiation Risks | -0.4% | Europe, North America | Long-term (2030-2033) |

Radiation Detection In Industrial and Scientific Market Opportunities Analysis

The Radiation Detection in Industrial and Scientific market is ripe with opportunities, driven by several key factors that promise to open new avenues for growth and innovation. The increasing investment in research and development across various scientific disciplines, including high-energy physics, astrophysics, and advanced material science, consistently creates demand for novel and highly specialized detection solutions. This drive for scientific discovery necessitates detectors with enhanced sensitivity, energy resolution, and spatial accuracy, pushing technological boundaries and fostering market expansion. Furthermore, the global trend towards environmental sustainability and the need for robust monitoring of radioactive waste and emissions present significant opportunities for advanced environmental radiation detection systems.

Emerging economies, with their rapidly expanding industrial bases and growing awareness of occupational safety and environmental protection, represent substantial untapped markets. As these regions invest in infrastructure and adopt international safety standards, the demand for affordable yet reliable radiation detection equipment is expected to surge. Moreover, the ongoing decommissioning of aging nuclear facilities worldwide presents a unique opportunity for specialized detection technologies and services required for safe dismantling and waste management. The integration of artificial intelligence and machine learning into detection systems for predictive analysis and automated monitoring further exemplifies the innovative opportunities poised to reshape the market landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing R&D Investment in Scientific Fields | +0.9% | North America, Europe, Japan, South Korea | Long-term (2030-2033) |

| Increasing Demand in Emerging Economies | +0.8% | Asia Pacific, Latin America, Middle East | Mid-term (2027-2030) |

| Decommissioning of Nuclear Facilities | +0.7% | Europe, North America, Japan | Long-term (2030-2033) |

| Integration of AI and Machine Learning | +0.6% | Global | Mid-term (2027-2030) |

| Customized Solutions for Specific Applications | +0.5% | Global | Short-term (2025-2027) |

Radiation Detection In Industrial and Scientific Market Challenges Impact Analysis

The Radiation Detection in Industrial and Scientific market, while promising, is not without its significant challenges that could impede growth and adoption. One prominent challenge is the rapid pace of technological obsolescence, where new and more advanced detection methods can quickly render existing equipment less competitive or even outdated. This necessitates continuous investment in R&D and product upgrades, which can strain resources for manufacturers and end-users alike. Additionally, the management of vast amounts of data generated by modern, high-sensitivity detectors presents a complex challenge, requiring robust data processing, storage, and analytical capabilities that may not always be readily available or integrated.

Another critical challenge lies in the supply chain vulnerabilities, particularly concerning specialized components and rare earth elements essential for certain advanced detector technologies. Geopolitical tensions or supply disruptions can significantly impact production timelines and costs. Furthermore, ensuring the accuracy and reliability of detection systems in diverse and often harsh industrial or scientific environments remains a persistent technical hurdle. Calibration, interference from background radiation, and maintaining performance in extreme temperatures or pressures demand continuous innovation and rigorous testing. Addressing these multifaceted challenges is crucial for sustainable market development and widespread adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -0.7% | Global | Mid-term (2027-2030) |

| Data Management and Analysis Complexity | -0.6% | Global | Long-term (2030-2033) |

| Supply Chain Vulnerabilities | -0.5% | Global, particularly Asia Pacific (for raw materials) | Short-term (2025-2027) |

| Ensuring Accuracy in Harsh Environments | -0.4% | Global, specific industrial sectors | Mid-term (2027-2030) |

Radiation Detection In Industrial and Scientific Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Radiation Detection in Industrial and Scientific market, offering a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and geographic regions. The scope encompasses a thorough evaluation of current market dynamics and future projections, leveraging historical data to forecast growth trajectories and identify key strategic imperatives for stakeholders. It aims to deliver actionable insights that enable businesses to navigate the evolving market landscape, capitalize on emerging opportunities, and mitigate potential risks within this critical sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.95 Billion |

| Market Forecast in 2033 | USD 3.28 Billion |

| Growth Rate | 6.7% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Radiation Solutions, Mirion Technologies, Berkeley Nucleonics, LND, AMETEK ORTEC, Canberra Industries, Ludlum Measurements, Thermo Fisher Scientific, Xylem Analytics, Fuji Electric, Hitachi, Siemens Healthineers, General Electric Healthcare, NUVIA, Kromek Group, Rapiscan Systems, Smiths Detection, Arktis Radiation Detectors, Polimaster, RAE Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Radiation Detection in Industrial and Scientific market is comprehensively segmented to provide granular insights into its diverse applications and technological landscapes. This segmentation allows for a detailed understanding of market dynamics within specific product types, end-use industries, and technological approaches, highlighting areas of high growth and specific market needs. The intricate interdependencies between these segments reveal how advancements in one area can significantly influence others, shaping the overall market trajectory.

By dissecting the market into various categories, stakeholders can identify niche opportunities and tailor strategies to address the unique demands of each segment. For instance, the distinction between gas-filled, scintillator, and solid-state detectors underscores varying performance characteristics and suitability for different applications, from high-sensitivity scientific research to robust industrial monitoring. Similarly, differentiating by application areas such as nuclear power, healthcare, and homeland security allows for a precise analysis of demand drivers and regulatory influences specific to each sector. This detailed segmentation is crucial for targeted market entry and product development.

- By Type: Gas-filled Detectors (Geiger-Muller, Proportional, Ionization Chambers), Scintillators (Solid Scintillators, Liquid Scintillators), Solid-state Detectors (Semiconductor Detectors, CdTe, CZT), Others (Neutron Detectors, Hybrid Detectors)

- By Application: Nuclear Power Generation, Healthcare and Medical Diagnostics (Radiology, Nuclear Medicine, Radiation Therapy), Industrial Non-Destructive Testing (NDT), Homeland Security and Defense (Border Security, CBRN Detection), Research and Academic Institutions (High Energy Physics, Material Science, Astrophysics), Environmental Monitoring and Protection, Mining and Geology, Agriculture and Food Processing

- By End-Use Industry: Energy, Manufacturing, Life Sciences, Defense, Environmental Agencies, Academic Research

- By Technology: Passive Detectors, Active Detectors

- By Product: Handheld Devices, Portable Devices, Fixed Systems, Personal Dosimeters

Regional Highlights

- North America: A mature market characterized by significant R&D investments, stringent regulatory frameworks, and high adoption of advanced radiation detection technologies in healthcare, defense, and nuclear energy sectors. The region benefits from a strong presence of key market players and a robust scientific research ecosystem.

- Europe: Driven by strict environmental and safety regulations, particularly in nuclear waste management and decommissioning. Strong demand from medical applications and a focus on advanced research in particle physics and material science contribute to its market share.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid industrialization, increasing energy demands leading to nuclear power expansion, and rising investments in healthcare infrastructure. Countries like China, India, and Japan are at the forefront of this growth, with significant opportunities in both industrial and scientific applications.

- Latin America: An emerging market with growing awareness of industrial safety and environmental protection. Increasing investments in mining, energy, and healthcare infrastructure are expected to drive demand for radiation detection solutions.

- Middle East and Africa (MEA): Marked by substantial investments in nuclear energy programs (e.g., UAE, Saudi Arabia) and heightened focus on homeland security. The region presents nascent but promising growth opportunities as countries enhance their industrial and scientific capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Radiation Detection In Industrial and Scientific Market.- Mirion Technologies

- Thermo Fisher Scientific

- AMETEK ORTEC

- Canberra Industries

- LND

- Ludlum Measurements

- Berkeley Nucleonics Corporation

- Radiation Solutions Inc.

- Xylem Analytics

- Fuji Electric Co., Ltd.

- Hitachi, Ltd.

- Siemens Healthineers AG

- General Electric Healthcare

- NUVIA (Vinci Construction)

- Kromek Group plc

- Rapiscan Systems

- Smiths Detection

- Arktis Radiation Detectors Ltd.

- Polimaster Inc.

- RAE Systems (Honeywell)

Frequently Asked Questions

What is the projected growth rate for the Radiation Detection in Industrial and Scientific Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033, reflecting a robust expansion driven by increasing industrial and scientific demands.

What are the primary drivers of growth in this market?

Key drivers include the expansion of nuclear power generation, increasing demand in medical diagnostics and therapy, stringent safety and environmental regulations, and continuous advancements in scientific research and development.

How is AI impacting radiation detection technologies?

AI is significantly impacting the market by enabling enhanced data analysis, automated anomaly detection, predictive maintenance for equipment, and the development of intelligent, adaptive monitoring systems, leading to more efficient and reliable detection.

Which regions are expected to exhibit the most significant growth?

The Asia Pacific region is anticipated to show the most significant growth due to rapid industrialization, expanding nuclear energy programs, and increasing investments in healthcare infrastructure across countries like China and India.

What are the main challenges faced by the Radiation Detection in Industrial and Scientific Market?

The primary challenges include the high initial cost of advanced equipment, complex regulatory frameworks, the scarcity of skilled professionals, rapid technological obsolescence, and the complexities of data management and analysis.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted