Military Aerospace Engine Market

Military Aerospace Engine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709874 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

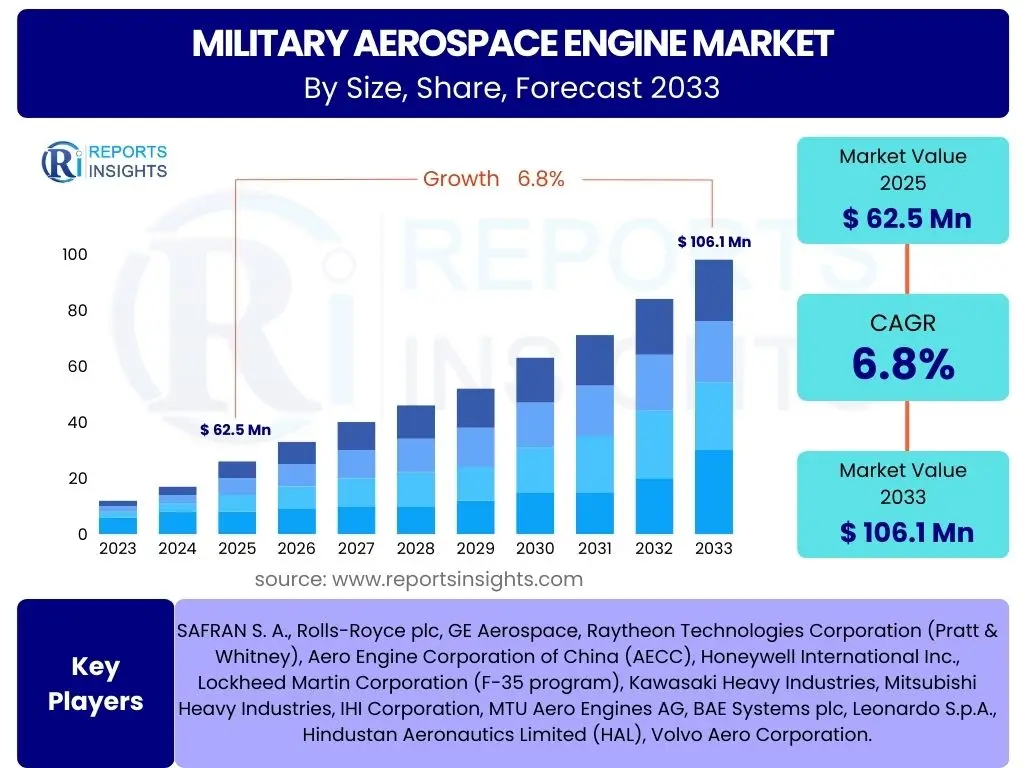

Military Aerospace Engine Market Size

According to Reports Insights Consulting Pvt Ltd, The Military Aerospace Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This robust growth is primarily driven by increasing global defense expenditures, advancements in aerospace technology, and the continuous modernization of military aircraft fleets worldwide. The market's expansion is further fueled by the demand for more fuel-efficient, powerful, and stealth-capable engines for both new platforms and existing aircraft upgrades, alongside the rising adoption of unmanned aerial vehicles (UAVs).

The market is estimated at USD 62.5 billion in 2025 and is projected to reach USD 106.1 billion by the end of the forecast period in 2033. This significant upward trajectory reflects a sustained investment cycle in military aviation capabilities, with a particular focus on next-generation combat aircraft, advanced transport platforms, and rotorcraft. Strategic partnerships between defense contractors and engine manufacturers are also contributing to the development and deployment of innovative propulsion systems, securing long-term market growth.

Key Military Aerospace Engine Market Trends & Insights

Users frequently inquire about the evolving technological landscape and strategic shifts impacting the military aerospace engine sector. Analysis reveals a strong emphasis on engines that offer enhanced performance, reduced fuel consumption, and lower operational costs. There is a growing interest in propulsion systems capable of supporting stealth characteristics, supersonic flight, and extended range, alongside solutions for unmanned and optionally manned aircraft. Furthermore, the integration of advanced materials and manufacturing processes, such as additive manufacturing, is a significant area of focus for improving engine durability and reducing production timelines. The long-term support and maintenance implications of these advanced engines are also a recurring theme.

- Development of adaptive cycle engines for multi-mission capability and improved fuel efficiency across varied flight envelopes.

- Increasing adoption of additive manufacturing (3D printing) for complex engine components, leading to lighter, stronger, and more cost-effective parts.

- Focus on enhancing engine stealth capabilities, including thermal signature reduction and noise suppression for advanced combat aircraft.

- Integration of advanced digital technologies for predictive maintenance, real-time diagnostics, and engine health monitoring systems (EHMS).

- Growing demand for propulsion systems tailored for Unmanned Aerial Vehicles (UAVs) and Unmanned Combat Aerial Vehicles (UCAVs), requiring lightweight and highly reliable engines.

- Emphasis on sustainable aviation fuel (SAF) compatibility and reduced emissions for future military aircraft, aligning with broader environmental initiatives.

- Strategic partnerships and collaborations between engine manufacturers and defense ministries for joint research and development of next-generation propulsion technologies.

- Modernization and upgrade programs for existing military aircraft fleets, driving demand for engine overhauls, component replacements, and performance enhancements.

AI Impact Analysis on Military Aerospace Engine

Common user questions regarding AI's influence on military aerospace engines often revolve around its potential to revolutionize maintenance, performance optimization, and autonomous operations. Users are keen to understand how AI can enhance engine reliability, predict potential failures, and reduce maintenance downtime, thereby lowering through-life costs. There is also significant interest in AI's role in engine design optimization, from material selection to aerodynamic efficiency, and its application in advanced control systems for enhanced flight performance and decision support for pilots.

Expectations are high for AI to contribute to more intelligent and resilient propulsion systems, capable of self-diagnosis and even self-repair in the long term. Concerns often touch upon the security implications of AI-driven systems, the ethical considerations of autonomous decision-making in combat, and the need for robust validation and verification processes. However, the overarching sentiment suggests a strong belief in AI's transformative potential to deliver unparalleled efficiencies and strategic advantages within the military aerospace engine domain.

- Predictive Maintenance: AI algorithms analyze engine data to forecast component failures, optimizing maintenance schedules and reducing unscheduled downtime.

- Engine Performance Optimization: AI-driven control systems fine-tune engine parameters in real-time for improved fuel efficiency, thrust, and overall performance.

- Autonomous Operations: AI enables intelligent decision-making for engine management in autonomous and optionally-manned aircraft, enhancing mission effectiveness.

- Design and Simulation: AI accelerates the design process by optimizing engine architectures, material selection, and aerodynamic profiles through advanced simulations.

- Supply Chain Management: AI improves efficiency in sourcing parts and managing inventory for engine manufacturing and MRO, reducing lead times and costs.

- Security and Resilience: AI is being developed to detect and mitigate cyber threats to engine control systems, ensuring operational integrity.

- Pilot Decision Support: AI provides real-time insights into engine health and performance, assisting pilots in critical decision-making during flight.

Key Takeaways Military Aerospace Engine Market Size & Forecast

Users frequently seek a concise summary of the most critical insights from the military aerospace engine market analysis, particularly concerning its future trajectory and growth drivers. A key takeaway is the consistent upward trend in market valuation, fueled by a global commitment to defense modernization and the development of next-generation aerial platforms. The market is not merely growing in size but also evolving technologically, with a strong emphasis on innovation in propulsion efficiency, stealth, and digital integration. These advancements are crucial for maintaining strategic superiority and adapting to emerging threats.

Another significant insight is the increasing demand for engines that support a wider range of mission profiles, from high-speed combat to long-endurance surveillance, including unmanned capabilities. The forecast highlights substantial opportunities for manufacturers investing in adaptive technologies, sustainable solutions, and robust supply chain resilience. Geopolitical factors and defense budget allocations will continue to be primary determinants of regional market performance, with a sustained focus on upgrading aging fleets and acquiring advanced systems.

- The Military Aerospace Engine Market is poised for significant growth, projected to exceed USD 100 billion by 2033, driven by global defense modernization.

- Technological innovation in engine design, materials, and manufacturing (e.g., adaptive cycle engines, additive manufacturing) is a primary growth catalyst.

- Increasing investment in Unmanned Aerial Vehicles (UAVs) and Unmanned Combat Aerial Vehicles (UCAVs) is creating a distinct demand segment for specialized engines.

- Predictive maintenance and AI integration are transforming engine lifecycle management, enhancing reliability and reducing operational costs.

- Geopolitical landscape and national defense policies heavily influence market dynamics, leading to sustained demand for high-performance propulsion systems.

- Major players are focusing on research and development, strategic partnerships, and mergers & acquisitions to gain a competitive edge and expand product portfolios.

- The trend towards more fuel-efficient, quieter, and lower-emission engines is gaining traction, balancing performance with environmental considerations.

Military Aerospace Engine Market Drivers Analysis

The military aerospace engine market is propelled by a confluence of geopolitical, technological, and economic factors. Escalating global defense expenditures, particularly in response to evolving security threats and regional conflicts, stand as a primary driver. Nations are actively investing in strengthening their air forces through the acquisition of new combat aircraft, transport planes, and helicopters, alongside significant modernization programs for existing fleets. This necessitates the development and procurement of advanced, high-performance engines that can meet stringent operational requirements and provide a strategic advantage.

Technological advancements also play a crucial role, with continuous innovation in engine design, materials science, and digital controls leading to more powerful, fuel-efficient, and stealth-capable propulsion systems. The proliferation of unmanned aerial systems (UAS) across military applications, from surveillance to combat, further drives demand for specialized, lightweight, and reliable engines. Additionally, the long-term support and maintenance requirements for existing military aircraft fleets ensure a steady market for engine overhauls, spare parts, and upgrades, contributing significantly to market stability and growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Global Defense Spending | +1.5% | Global, particularly North America, Asia Pacific | Short to Long Term (2025-2033) |

| Modernization of Aging Aircraft Fleets | +1.2% | Europe, North America, parts of Asia | Medium to Long Term (2026-2033) |

| Technological Advancements in Propulsion Systems | +1.0% | Global (leading R&D nations) | Short to Long Term (2025-2033) |

| Rising Demand for Unmanned Aerial Vehicles (UAVs) | +0.8% | North America, Asia Pacific, Middle East | Short to Medium Term (2025-2030) |

| Geopolitical Tensions and Regional Conflicts | +0.7% | Middle East, Eastern Europe, South China Sea | Short Term (2025-2027) |

| Development of Next-Generation Combat Aircraft | +0.6% | North America, Europe, China | Medium to Long Term (2028-2033) |

| Demand for Enhanced Fuel Efficiency and Performance | +0.5% | Global | Short to Long Term (2025-2033) |

Military Aerospace Engine Market Restraints Analysis

Despite the robust growth prospects, the military aerospace engine market faces several significant restraints that could temper its expansion. High research and development (R&D) costs associated with developing advanced engine technologies represent a considerable barrier to entry and can inflate the final cost of military platforms. The need for specialized materials, complex manufacturing processes, and extensive testing cycles contributes to these elevated costs, making innovative engine development a capital-intensive endeavor.

Stringent regulatory requirements and lengthy certification processes imposed by defense authorities globally also pose a challenge, extending development timelines and increasing program complexities. Furthermore, geopolitical instability, while sometimes acting as a driver for defense spending, can also disrupt international collaborations, supply chains, and export opportunities, thereby impacting market access and sales. Budgetary constraints in certain nations or shifts in defense priorities can lead to program delays or cancellations, directly affecting engine procurement volumes. The reliance on a limited number of highly specialized suppliers for critical components also introduces supply chain vulnerabilities and potential bottlenecks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development Costs | -1.3% | Global | Long Term (2025-2033) |

| Stringent Regulatory & Certification Processes | -1.0% | North America, Europe | Long Term (2025-2033) |

| Long Development & Procurement Cycles | -0.8% | Global | Long Term (2025-2033) |

| Supply Chain Disruptions and Geopolitical Risks | -0.7% | Global (esp. Asia-Pacific, Europe) | Short to Medium Term (2025-2028) |

| Environmental Regulations and Emission Concerns | -0.5% | Europe, North America | Medium to Long Term (2027-2033) |

| Defense Budgetary Constraints in Some Nations | -0.4% | Latin America, parts of Africa | Short to Medium Term (2025-2030) |

Military Aerospace Engine Market Opportunities Analysis

Significant opportunities are emerging within the military aerospace engine market, driven by evolving defense strategies and technological breakthroughs. The development of next-generation fighter jets, bombers, and advanced surveillance platforms presents a substantial market for innovative engine designs that offer enhanced performance, fuel efficiency, and stealth capabilities. These programs often involve multi-billion-dollar investments and long-term production contracts, securing future revenue streams for engine manufacturers. Furthermore, the global trend towards replacing aging military aircraft fleets opens avenues for both new engine sales and extensive upgrade and overhaul services for existing propulsion systems.

The burgeoning market for military unmanned aerial vehicles (UAVs) and unmanned combat aerial vehicles (UCAVs) also represents a lucrative opportunity. These platforms require specialized, lightweight, and highly reliable engines that can operate autonomously for extended durations, differing from traditional manned aircraft propulsion needs. Additionally, advancements in sustainable aviation fuels (SAFs) and hybrid-electric propulsion systems, initially gaining traction in civil aviation, present a long-term opportunity for military applications seeking to reduce carbon footprint and operational costs, aligning with broader environmental and strategic goals.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Aircraft Programs | +1.4% | North America, Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Growing Demand for UAV/UCAV Propulsion Systems | +1.1% | Global (esp. US, China, Israel, Turkey) | Short to Medium Term (2025-2030) |

| Fleet Modernization & Upgrade Programs | +0.9% | Europe, Asia Pacific, North America | Medium Term (2026-2031) |

| Emergence of Adaptive Cycle Engine Technology | +0.8% | North America, Europe | Long Term (2029-2033) |

| International Collaborations & Joint Ventures | +0.6% | Global | Short to Long Term (2025-2033) |

| Expansion in Maintenance, Repair, and Overhaul (MRO) Services | +0.5% | Global | Short to Long Term (2025-2033) |

| Integration of AI and Digital Twins for Engine Optimization | +0.4% | Global | Medium to Long Term (2028-2033) |

Military Aerospace Engine Market Challenges Impact Analysis

The military aerospace engine market, while promising, is not without its significant challenges. One of the foremost issues is the immense technical complexity and the inherently long development cycles associated with designing, testing, and certifying new military engines. These processes can span decades, delaying market entry and requiring sustained, substantial investment before any return is realized. Furthermore, ensuring cybersecurity for increasingly digitized engine control systems is a critical challenge, as vulnerabilities could compromise mission effectiveness or even lead to catastrophic failures. The growing reliance on advanced software and connected systems makes these engines prime targets for sophisticated cyber threats.

Another pressing challenge is the maintenance of a highly skilled workforce, encompassing engineers, technicians, and specialized manufacturing personnel. The advanced nature of aerospace engine technology necessitates continuous training and recruitment to address talent shortages, particularly in niche areas like composite materials, additive manufacturing, and AI integration. Geopolitical instability, while a driver of demand, can also act as a challenge by creating export restrictions, impacting international supply chains, and leading to sudden shifts in defense priorities that might alter or cancel engine programs. Managing the obsolescence of legacy engine components while integrating cutting-edge technologies into existing platforms also presents a significant logistical and technical hurdle for defense forces and manufacturers alike.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexity & Long Development Cycles | -1.1% | Global | Long Term (2025-2033) |

| Ensuring Cybersecurity of Engine Control Systems | -0.9% | Global | Short to Long Term (2025-2033) |

| Talent Shortages and Workforce Development | -0.7% | North America, Europe | Long Term (2025-2033) |

| Supply Chain Vulnerabilities & Raw Material Sourcing | -0.6% | Global | Short to Medium Term (2025-2028) |

| High Maintenance & Operational Costs of Advanced Engines | -0.5% | Global | Short to Long Term (2025-2033) |

| Managing Obsolescence of Legacy Systems | -0.4% | Global | Medium to Long Term (2027-2033) |

| Adapting to Rapid Technological Evolution | -0.3% | Global | Short to Long Term (2025-2033) |

Military Aerospace Engine Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the military aerospace engine sector, providing a robust analysis of its current state and future trajectory. It offers an in-depth exploration of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages extensive data analysis to forecast market trends and project future valuations, offering strategic insights for stakeholders navigating this critical defense industry. It also includes an examination of emerging technologies, such as AI integration and advanced manufacturing, and their impact on engine development and operational efficiency, ensuring a holistic understanding of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 62.5 Billion |

| Market Forecast in 2033 | USD 106.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAFRAN S. A., Rolls-Royce plc, GE Aerospace, Raytheon Technologies Corporation (Pratt & Whitney), Aero Engine Corporation of China (AECC), Honeywell International Inc., Lockheed Martin Corporation (F-35 program), Kawasaki Heavy Industries, Mitsubishi Heavy Industries, IHI Corporation, MTU Aero Engines AG, BAE Systems plc, Leonardo S.p.A., Hindustan Aeronautics Limited (HAL), Volvo Aero Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Military Aerospace Engine Market is extensively segmented to provide granular insights into its diverse components and applications. These segmentations allow for a detailed analysis of specific market niches, technological preferences, and operational requirements. The primary segmentation categories include engine type, aircraft type, crucial components, application (new production versus aftermarket), and the underlying technology employed. Each segment exhibits unique growth drivers and market dynamics, reflecting the varied needs of global defense forces and the capabilities of engine manufacturers.

Understanding these distinct segments is essential for identifying key areas of investment, strategic partnerships, and emerging demand patterns. For instance, the market for turbofan engines used in combat aircraft differs significantly from that for turboshaft engines powering helicopters, both in terms of design complexity and MRO requirements. Similarly, the rapid expansion of unmanned aerial vehicle fleets is creating a specialized segment for smaller, highly efficient engines, distinct from those powering large transport aircraft. This detailed segmentation enables a more targeted and effective market analysis.

- By Type: Turbofan, Turboshaft, Turboprop, Ramjet/Scramjet, Others (e.g., Electric/Hybrid)

- By Aircraft Type: Combat Aircraft (Fighters, Bombers), Transport Aircraft (Cargo, Tankers), Helicopters (Attack, Utility, Transport), Unmanned Aerial Vehicles (UAVs/UCAVs), Trainer Aircraft

- By Component: Compressor, Turbine, Combustor, Nozzle, Afterburner, Accessory Gearbox, Engine Control Systems (FADEC)

- By Application: New Aircraft Production, Aftermarket (Maintenance, Repair, Overhaul (MRO), Upgrades)

- By Technology: Conventional Propulsion, Advanced & Adaptive Propulsion, Electric/Hybrid-Electric Propulsion

Regional Highlights

- North America: Dominates the market due to robust defense budgets, extensive R&D investments, and the presence of major aerospace engine manufacturers in the United States. Significant ongoing programs for next-generation fighters (e.g., F-35), bombers, and advanced UAVs drive consistent demand. The region is a pioneer in adaptive cycle engine technology and AI integration.

- Europe: A strong market driven by fleet modernization efforts, collaboration on multi-national defense projects (e.g., Eurofighter Typhoon, FCAS), and increasing defense spending from nations facing evolving security challenges. Key countries like the UK, France, and Germany are investing heavily in both new acquisitions and MRO services for their air forces.

- Asia Pacific (APAC): Emerging as the fastest-growing region, fueled by rising defense expenditures from countries like China, India, Japan, and South Korea. Geopolitical tensions and territorial disputes in the region are driving an arms race, leading to significant procurement of advanced combat aircraft and UAVs, along with indigenous engine development efforts.

- Middle East and Africa (MEA): Experiences substantial growth due to ongoing regional conflicts and the need for enhanced aerial defense capabilities. Countries like Saudi Arabia, UAE, and Turkey are investing in high-performance military aircraft and UAVs, often through imports and technology transfer agreements.

- Latin America: Represents a smaller but growing market, primarily focused on upgrading existing fleets of transport aircraft and helicopters. Economic stability and evolving security concerns in some nations are gradually leading to increased, albeit selective, defense spending on aerospace assets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Military Aerospace Engine Market.- SAFRAN S. A.

- Rolls-Royce plc

- GE Aerospace

- Raytheon Technologies Corporation (Pratt & Whitney)

- Aero Engine Corporation of China (AECC)

- Honeywell International Inc.

- Lockheed Martin Corporation (F-35 program)

- Kawasaki Heavy Industries

- Mitsubishi Heavy Industries

- IHI Corporation

- MTU Aero Engines AG

- BAE Systems plc

- Leonardo S.p.A.

- Hindustan Aeronautics Limited (HAL)

- Volvo Aero Corporation

- Hanwha Aerospace

- Snecma (a Safran company)

- Motor Sich JSC

- Klimov (United Engine Corporation)

- Saturn (United Engine Corporation)

Frequently Asked Questions

What is the projected growth rate for the Military Aerospace Engine Market?

The Military Aerospace Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 106.1 billion by 2033.

What are the primary drivers of growth in this market?

Key drivers include increased global defense spending, modernization of aging aircraft fleets, technological advancements in propulsion systems, the rising demand for Unmanned Aerial Vehicles (UAVs), and ongoing geopolitical tensions.

How is Artificial Intelligence (AI) impacting military aerospace engines?

AI is significantly impacting military aerospace engines through predictive maintenance, real-time performance optimization, autonomous control systems for UAVs, enhanced design and simulation, and improved supply chain management, ultimately boosting efficiency and reliability.

Which regions are expected to show significant growth?

North America currently dominates, but the Asia Pacific (APAC) region is expected to exhibit the fastest growth due to increasing defense budgets and military modernization efforts by countries like China and India.

What are the main challenges facing the Military Aerospace Engine Market?

Major challenges include high research and development costs, stringent regulatory processes, long development and procurement cycles, cybersecurity threats to advanced systems, and managing supply chain vulnerabilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted