R134A Refrigerant Market

R134A Refrigerant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701026 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

R134A Refrigerant Market Size

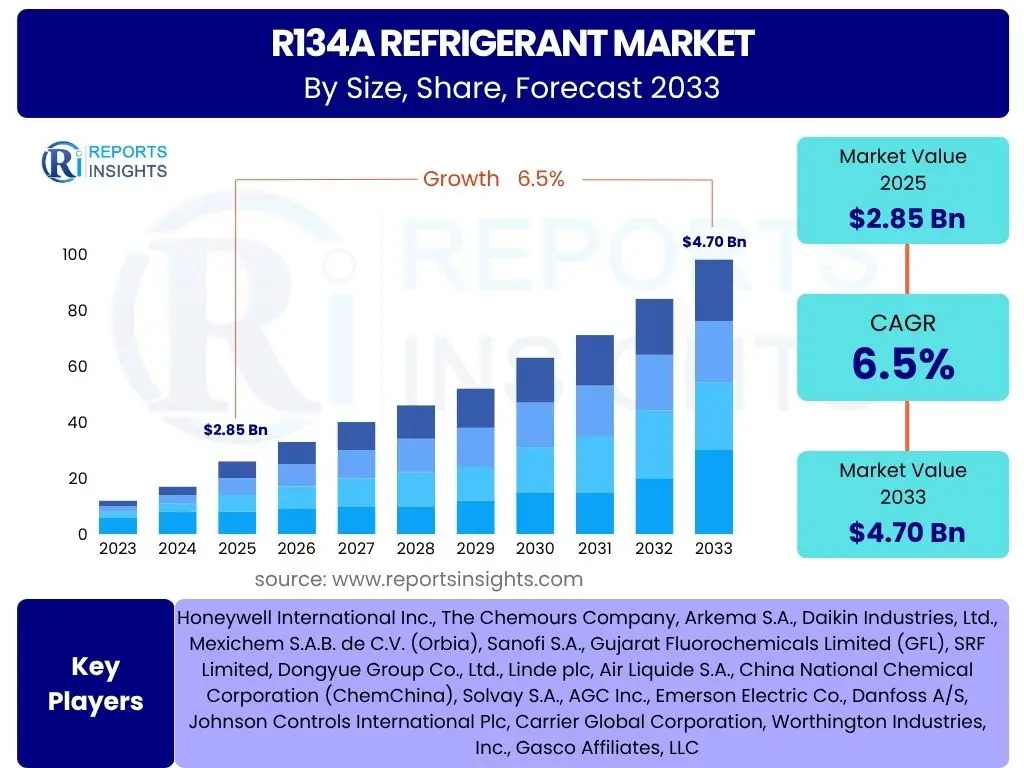

According to Reports Insights Consulting Pvt Ltd, The R134A Refrigerant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 4.70 Billion by the end of the forecast period in 2033.

Key R134A Refrigerant Market Trends & Insights

The R134A refrigerant market is currently navigating a complex landscape shaped by evolving environmental regulations and sustained demand from key application sectors. Common user questions often revolve around the impact of the global phase-down of hydrofluorocarbons (HFCs) under international agreements like the Kigali Amendment, and how this affects the production, supply, and future use of R134a. Despite the overarching trend towards low-Global Warming Potential (GWP) alternatives, R134a continues to hold significant market share due to its vast installed base in existing refrigeration and air conditioning systems worldwide, particularly in the automotive and domestic refrigeration sectors. Market insights suggest a bifurcated scenario: a gradual decline in new installations in developed regions adhering to strict HFC reduction targets, contrasted by persistent demand in developing economies and a robust aftermarket for servicing existing equipment.

Furthermore, the market is witnessing a strategic shift towards circular economy principles, with an increasing emphasis on the reclamation, recycling, and reuse of R134a to minimize environmental impact and manage supply. This trend is driven by both regulatory mandates and economic incentives, as it provides a more sustainable approach to managing refrigerants already in circulation. Innovations in leak detection technologies and refrigerant management systems are also gaining traction, aiming to reduce fugitive emissions from existing R134a systems. Stakeholders are keenly observing the pace of transition to alternatives such as HFO-1234yf in automotive air conditioning and natural refrigerants in commercial refrigeration, which will ultimately dictate the long-term trajectory of R134a, especially in new equipment.

- Persistent demand from existing automotive and domestic refrigeration systems.

- Increasing focus on R134a reclamation, recycling, and reuse.

- Gradual phase-down of HFCs under global environmental regulations.

- Development and adoption of advanced leak detection and refrigerant management solutions.

- Emergence of regional disparities in R134a consumption and transition rates.

AI Impact Analysis on R134A Refrigerant

Common user questions regarding the impact of Artificial Intelligence (AI) on the R134A refrigerant market often center on how AI can optimize system performance, enhance maintenance practices, and improve the efficiency of refrigerant management. While AI does not directly alter the chemical properties of R134a, its influence is profound in the operational aspects of systems utilizing this refrigerant. AI-powered algorithms are increasingly being deployed in smart HVAC systems and automotive air conditioning units to predict maintenance needs, optimize cooling cycles, and detect potential refrigerant leaks more efficiently than traditional methods. This predictive capability helps in minimizing refrigerant loss, thereby extending the operational life of systems and reducing the environmental footprint associated with R134a emissions. The insights derived from AI analysis can lead to more precise charging of systems, reduced energy consumption, and proactive servicing, all contributing to the sustainable use of R134a.

Moreover, AI plays a crucial role in optimizing the supply chain and logistics of R134a, from production and distribution to recycling and reclamation. Through advanced analytics and machine learning, AI can forecast demand, manage inventory, and streamline transportation, ensuring efficient supply and reducing wastage. This is particularly relevant in the context of HFC phase-down, where managing the remaining supply of R134a for servicing existing equipment becomes critical. Furthermore, AI can aid in the development of new refrigerant blends by rapidly analyzing molecular structures and their thermodynamic properties, potentially leading to novel solutions that are more environmentally friendly or offer superior performance, although direct replacements for R134a are often non-HFC alternatives. The integration of AI tools within the refrigerant industry signals a move towards more intelligent, resource-efficient, and environmentally conscious practices.

- Optimization of refrigerant charging and system performance through AI-driven controls.

- Enhanced predictive maintenance for HVAC and automotive AC systems, reducing R134a leaks.

- Streamlined supply chain and inventory management for R134a reclamation and distribution.

Key Takeaways R134A Refrigerant Market Size & Forecast

Analysis of common user questions about the R134A refrigerant market size and forecast reveals a primary concern regarding its future viability amidst stringent environmental regulations. Despite the ongoing global phase-down of HFCs, the market for R134a is projected to exhibit a moderate Compound Annual Growth Rate (CAGR) through 2033, largely sustained by its substantial installed base in various applications, particularly automotive air conditioning and domestic refrigeration. This paradoxical growth, even under regulatory pressure, underscores the immense challenge and cost associated with retrofitting or replacing millions of existing systems. Therefore, a significant portion of the future market will be driven by servicing and maintaining this legacy equipment, along with continued demand from developing economies where the transition to low-GWP alternatives is slower.

Another crucial takeaway is the increasing importance of circular economy practices within the R134a market. As new production is curtailed in many regions, the emphasis shifts heavily towards reclamation, recycling, and effective waste management of R134a. This not only mitigates environmental impact but also creates a valuable secondary supply stream crucial for the aftermarket. Stakeholders must strategically adapt to these evolving market dynamics, focusing on efficient recovery technologies, robust supply chain management for recycled refrigerants, and compliance with varying regional regulatory frameworks. The forecast suggests that while the overall trajectory points towards a long-term decline for R134a in new installations, its market presence for servicing and in specific emerging applications will remain significant for the foreseeable future, representing a critical transitional phase in the refrigerant industry.

- The R134A market, while facing phase-down, shows continued growth driven by the servicing of vast existing installations.

- Regulatory mandates are accelerating the shift towards reclamation and recycling, creating a secondary market.

- Emerging economies will play a crucial role in sustaining demand due to slower adoption of alternatives.

- Strategic focus on leak prevention and efficient refrigerant management is paramount for environmental compliance.

R134A Refrigerant Market Drivers Analysis

The R134A refrigerant market is primarily driven by the expansive installed base of systems across various sectors that continue to rely on this chemical. The automotive industry, in particular, represents a significant driver, with millions of vehicles globally still utilizing R134a in their air conditioning systems. While newer car models are transitioning to HFO-1234yf, the aftermarket demand for servicing and repairing older vehicles ensures a consistent need for R134a. Similarly, a substantial proportion of domestic refrigerators, commercial refrigeration units, and chillers globally were manufactured to operate with R134a, thereby sustaining its demand for maintenance, repairs, and refills. The sheer scale of this existing infrastructure underpins the market's continued vitality despite regulatory headwinds.

Furthermore, the growth in population, urbanization, and disposable incomes in developing regions contributes significantly to the market. As these economies expand, there is a rising demand for refrigeration and air conditioning solutions, often incorporating R134a due to its cost-effectiveness, established supply chain, and proven performance compared to some nascent alternatives. The pharmaceutical and food and beverage industries, with their stringent requirements for cold chain logistics, also represent stable demand segments for R134a, particularly in applications where reliable and well-understood refrigeration is paramount. These factors collectively counterbalance the pressures from regulatory phase-downs in developed nations, maintaining the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Large Installed Base of R134a Systems | +2.5% | Global, especially North America, Europe, APAC | Short-term to Mid-term (2025-2030) |

| Growing Automotive Aftermarket Demand | +1.8% | Global, particularly North America, Europe, China, India | Mid-term (2025-2033) |

| Increasing Demand for Refrigeration in Emerging Economies | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2028-2033) |

| Essential Use in Cold Chain Logistics (Pharma, F&B) | +0.7% | Global | Ongoing |

R134A Refrigerant Market Restraints Analysis

The primary restraint on the R134A refrigerant market stems from increasingly stringent environmental regulations targeting high-Global Warming Potential (GWP) refrigerants. International agreements, notably the Kigali Amendment to the Montreal Protocol, mandate a phasedown of HFCs like R134a, compelling countries to reduce their production and consumption. Region-specific regulations, such as the European Union's F-gas Regulation, impose strict quotas and bans on new equipment containing high-GWP refrigerants, significantly curbing the adoption of R134a in new installations. These regulatory pressures are forcing manufacturers to invest in and transition towards alternative refrigerants with lower GWP, diminishing the long-term prospects for R134a in many developed markets. The uncertainty created by future regulatory landscapes also discourages new investments in R134a production capabilities.

Furthermore, the availability and increasing adoption of viable low-GWP alternatives, such as HFO-1234yf for automotive air conditioning and natural refrigerants (e.g., CO2, ammonia, hydrocarbons) for commercial and industrial refrigeration, pose a significant competitive restraint. While these alternatives often require system redesigns or specialized components, their long-term environmental benefits and regulatory compliance make them increasingly attractive for new equipment. The higher initial cost of transitioning existing R134a systems to alternatives, or the complete replacement of equipment, also acts as a financial barrier for some end-users, yet it still signifies a shift away from R134a. This combination of regulatory pressure and viable alternatives effectively limits the growth potential of R134a in new applications and accelerates its decline in established markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations and HFC Phase-down (Kigali Amendment, F-gas) | -3.0% | Global, particularly Europe, North America | Ongoing to Long-term (2025-2033) |

| Growing Adoption of Low-GWP Alternatives (HFOs, Naturals) | -2.2% | Global, especially developed markets | Mid-term to Long-term (2027-2033) |

| High Cost of Transitioning from R134a Systems | -1.0% | Global | Mid-term (2025-2030) |

R134A Refrigerant Market Opportunities Analysis

Despite the prevailing narrative of phase-down, significant opportunities exist within the R134A refrigerant market, primarily centered around the extensive installed base of equipment. The large number of existing automotive, domestic, and commercial refrigeration systems designed for R134a presents a robust retrofit and servicing market. As new production is curtailed in certain regions, the demand for recycled and reclaimed R134a is set to increase substantially. This creates a lucrative opportunity for companies involved in refrigerant recovery, purification, and redistribution, adhering to circular economy principles. Innovations in recycling technologies and establishment of efficient collection networks can unlock significant value, ensuring a sustainable supply for the aftermarket without contributing to new HFC emissions. This trend supports both environmental goals and economic viability for stakeholders.

Furthermore, opportunities are emerging in the development of "drop-in" or "near drop-in" alternative blends that are compatible with existing R134a systems, requiring minimal or no modifications. While not a permanent solution, these interim refrigerants could extend the useful life of existing equipment, providing a smoother transition period for end-users and equipment owners. Additionally, the increasing focus on energy efficiency in refrigeration and air conditioning systems, driven by both cost savings and environmental concerns, opens avenues for R134a system optimization services. This involves fine-tuning existing R134a equipment for improved performance and reduced refrigerant charge, thereby maximizing the efficiency of the remaining R134a stock. Lastly, emerging economies, which are less constrained by immediate phase-down mandates and have burgeoning demand for new refrigeration, offer a continued albeit time-limited market for R134a in new installations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in R134a Recycling and Reclamation Services | +1.5% | Global | Mid-term to Long-term (2025-2033) |

| Expansion of Aftermarket Servicing for Existing R134a Systems | +1.2% | Global, particularly North America, Europe, APAC | Short-term to Mid-term (2025-2030) |

| Development of R134a Compatible Blends for Retrofit Applications | +0.8% | Global | Mid-term (2027-2032) |

| Increasing Demand for R134a in Emerging Markets | +0.5% | Asia Pacific, Latin America, Middle East & Africa | Short-term to Mid-term (2025-2030) |

R134A Refrigerant Market Challenges Impact Analysis

The R134A refrigerant market faces significant challenges primarily driven by the intricate and ever-evolving regulatory landscape. Navigating the varying HFC phase-down schedules and specific regulations across different countries and regions poses a substantial hurdle for manufacturers and distributors. Compliance requires continuous monitoring, significant investment in R&D for alternative technologies, and often, a complete overhaul of production processes and supply chains. The risk of non-compliance can lead to hefty fines, reputational damage, and loss of market access. Moreover, the long-term uncertainty surrounding the availability and cost of virgin R134a, coupled with the increasing emphasis on lower-GWP alternatives, complicates strategic planning and investment decisions for market participants, leading to a hesitant market environment.

Another critical challenge is the illegal trade and counterfeiting of refrigerants. As R134a production is curtailed in regulated markets, illicit channels can emerge, supplying substandard or counterfeit products. These products not only pose safety risks and damage equipment but also undermine legitimate businesses and environmental efforts by circumventing regulations. Furthermore, the technological shift required to transition from R134a systems to those operating on new generation refrigerants presents considerable technical and economic challenges. This includes the need for new equipment designs, specialized training for technicians, and the high cost of retrofitting existing infrastructure, all of which can slow down the adoption of sustainable alternatives and create friction within the market. Managing these multifaceted challenges while balancing continued demand for existing equipment and the push for environmental responsibility is a complex task for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Evolving and Varied Global Regulations | -1.5% | Global | Ongoing to Long-term (2025-2033) |

| Illegal Trade and Counterfeiting of Refrigerants | -1.0% | Global, particularly emerging economies with weaker enforcement | Ongoing |

| High Cost and Complexity of Technological Transition | -0.8% | Global | Mid-term (2025-2030) |

| Competition from Next-Generation Low-GWP Refrigerants | -0.7% | Global | Ongoing to Long-term (2025-2033) |

R134A Refrigerant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the R134A Refrigerant market, covering market dynamics, segmentation, regional insights, and competitive landscape. It offers a detailed forecast, highlighting key trends, drivers, restraints, opportunities, and challenges impacting market growth from 2025 to 2033. The report is designed to assist stakeholders in understanding the market's trajectory amidst evolving environmental regulations and technological advancements, providing actionable insights for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 4.70 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., The Chemours Company, Arkema S.A., Daikin Industries, Ltd., Mexichem S.A.B. de C.V. (Orbia), Sanofi S.A., Gujarat Fluorochemicals Limited (GFL), SRF Limited, Dongyue Group Co., Ltd., Linde plc, Air Liquide S.A., China National Chemical Corporation (ChemChina), Solvay S.A., AGC Inc., Emerson Electric Co., Danfoss A/S, Johnson Controls International Plc, Carrier Global Corporation, Worthington Industries, Inc., Gasco Affiliates, LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The R134A refrigerant market is extensively segmented to provide a granular view of its diverse applications and supply dynamics, enabling a precise understanding of its current usage and future trajectory. The primary segmentation by application highlights the dominant role of automotive air conditioning and domestic refrigeration, which collectively account for a significant portion of R134a consumption due to their widespread adoption globally. Commercial refrigeration, industrial refrigeration, and chillers also represent substantial segments, catering to diverse cooling needs across various industries. Understanding these application segments is crucial as the phase-down impacts and availability of alternatives vary considerably across them, influencing adoption rates and regional demand patterns.

Further segmentation by type of R134a, namely virgin versus recycled/reclaimed, is increasingly vital given the global regulatory push towards circular economy principles and HFC phase-down. The growing emphasis on managing existing refrigerants responsibly means the recycled and reclaimed R134a segment is projected to gain significant prominence, especially in developed markets where new production of virgin R134a is being curtailed. Additionally, analyzing the market by end-use industry, such as automotive, HVAC, food and beverage, and pharmaceuticals, provides insights into specific industry demands, regulatory compliance challenges, and the pace of transition to alternatives. These detailed segmentations allow for a comprehensive assessment of market opportunities and challenges, supporting targeted strategic interventions.

- By Application:

- Automotive Air Conditioning (Mobile AC)

- Domestic Refrigeration

- Commercial Refrigeration

- Industrial Refrigeration

- Chillers

- Aerosols and Propellants

- Medical and Pharmaceutical (e.g., Metered Dose Inhalers)

- Others (e.g., Foam Blowing, Fire Suppression)

- By Type/Form:

- Virgin R134A

- Recycled/Reclaimed R134A

- By End-Use Industry:

- Automotive

- HVAC (Heating, Ventilation, Air Conditioning)

- Food and Beverage

- Pharmaceuticals

- Chemical Industry

- Retail

- Manufacturing

- Other Industrial Sectors

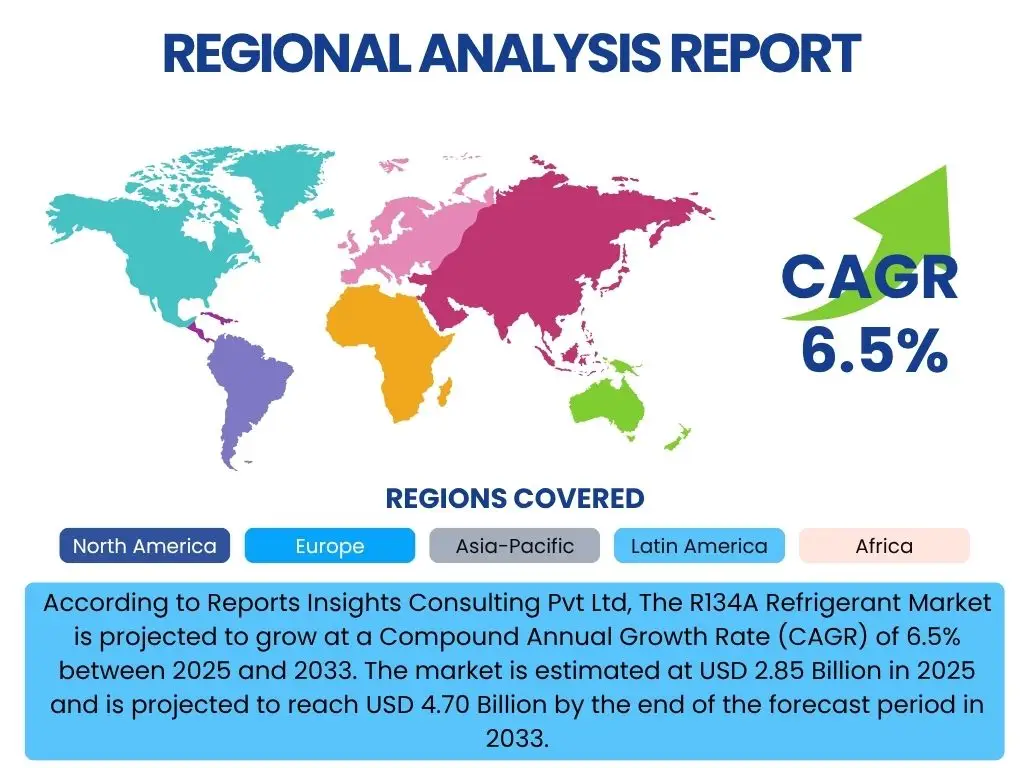

Regional Highlights

- North America: This region represents a mature market for R134a, characterized by stringent environmental regulations, particularly the U.S. EPA's HFC phase-down rules and state-level initiatives. While new equipment largely shifts to alternatives, the extensive installed base of automotive and residential HVAC systems sustains a robust aftermarket for R134a, primarily through recycling and reclamation. The region is a leader in refrigerant management and recycling technologies.

- Europe: Europe is at the forefront of the HFC phase-down through its ambitious F-gas Regulation, which has significantly restricted the use of R134a in new equipment. This has accelerated the transition to low-GWP alternatives and natural refrigerants. The market for R134a here is predominantly driven by servicing existing systems and is heavily reliant on reclaimed and recycled material to comply with regulations.

- Asia Pacific (APAC): APAC is projected to be a key growth driver for the R134a market, especially in developing economies like China, India, and Southeast Asian countries. Rapid urbanization, increasing disposable incomes, and growing demand for refrigeration and air conditioning systems contribute to this. While some countries are adopting HFC phase-down measures, the pace is generally slower than in developed regions, leading to continued new installations and significant aftermarket demand.

- Latin America: This region presents a mixed landscape. Countries like Brazil and Mexico, with significant automotive manufacturing and growing middle classes, exhibit strong demand for R134a in both new and existing applications. Regulatory frameworks are evolving, generally following the global trend towards HFC reduction, but often with longer transition periods, maintaining R134a's relevance for the foreseeable future.

- Middle East and Africa (MEA): The MEA region is experiencing rapid infrastructure development and population growth, leading to increased demand for cooling solutions across residential, commercial, and industrial sectors. R134a continues to be a prevalent choice due to its proven performance and established supply chain. However, regulatory adoption related to HFC phase-down is gaining momentum, indicating a gradual shift in the long term, though current demand remains robust.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the R134A Refrigerant Market.- Honeywell International Inc.

- The Chemours Company

- Arkema S.A.

- Daikin Industries, Ltd.

- Mexichem S.A.B. de C.V. (Orbia)

- Sanofi S.A.

- Gujarat Fluorochemicals Limited (GFL)

- SRF Limited

- Dongyue Group Co., Ltd.

- Linde plc

- Air Liquide S.A.

- China National Chemical Corporation (ChemChina)

- Solvay S.A.

- AGC Inc.

- Emerson Electric Co.

- Danfoss A/S

- Johnson Controls International Plc

- Carrier Global Corporation

- Worthington Industries, Inc.

- Gasco Affiliates, LLC

Frequently Asked Questions

Analyze common user questions about the R134A Refrigerant market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is R134a Refrigerant and its primary applications?

R134a, or 1,1,1,2-tetrafluoroethane, is a hydrofluorocarbon (HFC) refrigerant widely used in automotive air conditioning, domestic refrigerators, commercial chillers, and certain aerosol propellants. It is known for its excellent thermodynamic properties and non-flammability.

Why is R134a being phased out globally?

R134a is being phased out due to its high Global Warming Potential (GWP), which contributes significantly to climate change. International agreements like the Kigali Amendment to the Montreal Protocol mandate a global reduction in HFC production and consumption to mitigate their environmental impact.

What are the main alternatives to R134a?

The primary alternatives to R134a include hydrofluoroolefins (HFOs) like HFO-1234yf for automotive AC, and natural refrigerants such as CO2 (carbon dioxide), ammonia (R717), and hydrocarbons (e.g., propane R290, isobutane R600a) for various refrigeration and HVAC applications, all having significantly lower GWP.

How do regulations impact the future market outlook for R134a?

Regulations, particularly in developed regions (e.g., EU F-gas Regulation, U.S. EPA rules), are steadily reducing the supply and increasing the cost of virgin R134a. This shifts the market focus towards reclaimed and recycled R134a for existing equipment servicing, while new installations increasingly adopt low-GWP alternatives.

What role does recycling and reclamation play in the R134a market?

Recycling and reclamation are becoming crucial for the R134a market, ensuring a sustainable supply for the vast installed base of equipment that still relies on it. These practices reduce environmental emissions, support circular economy goals, and help manage the phase-down by extending the lifecycle of existing refrigerants.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted