Fluorine Refrigerant Market

Fluorine Refrigerant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700381 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

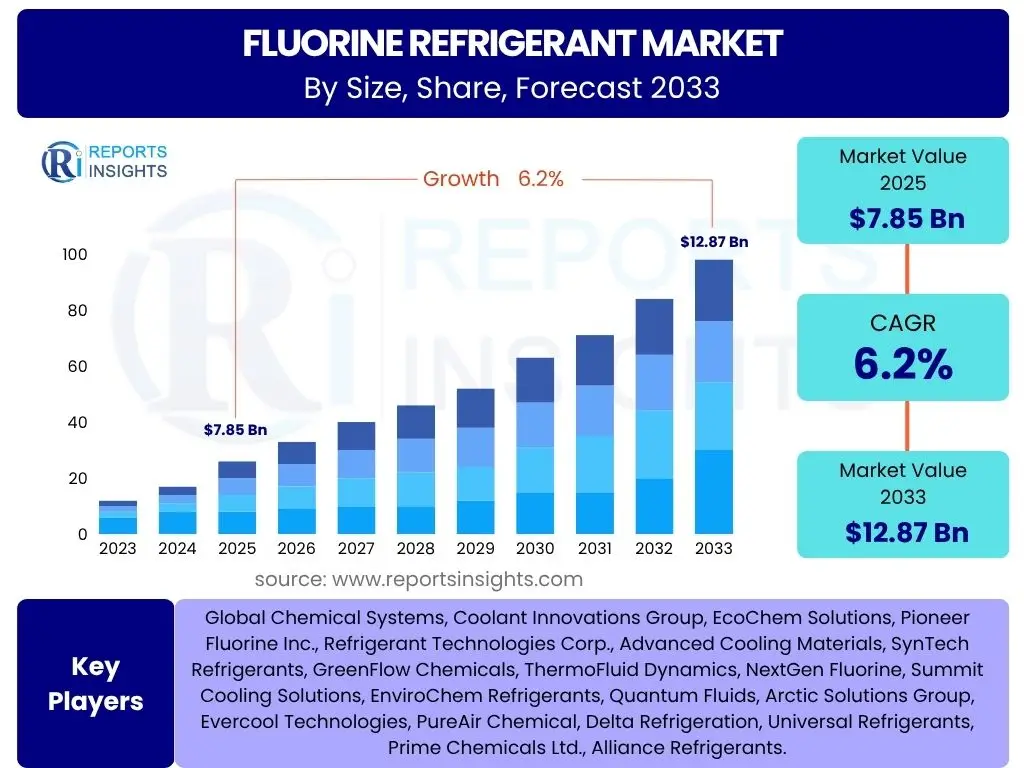

Fluorine Refrigerant Market Size

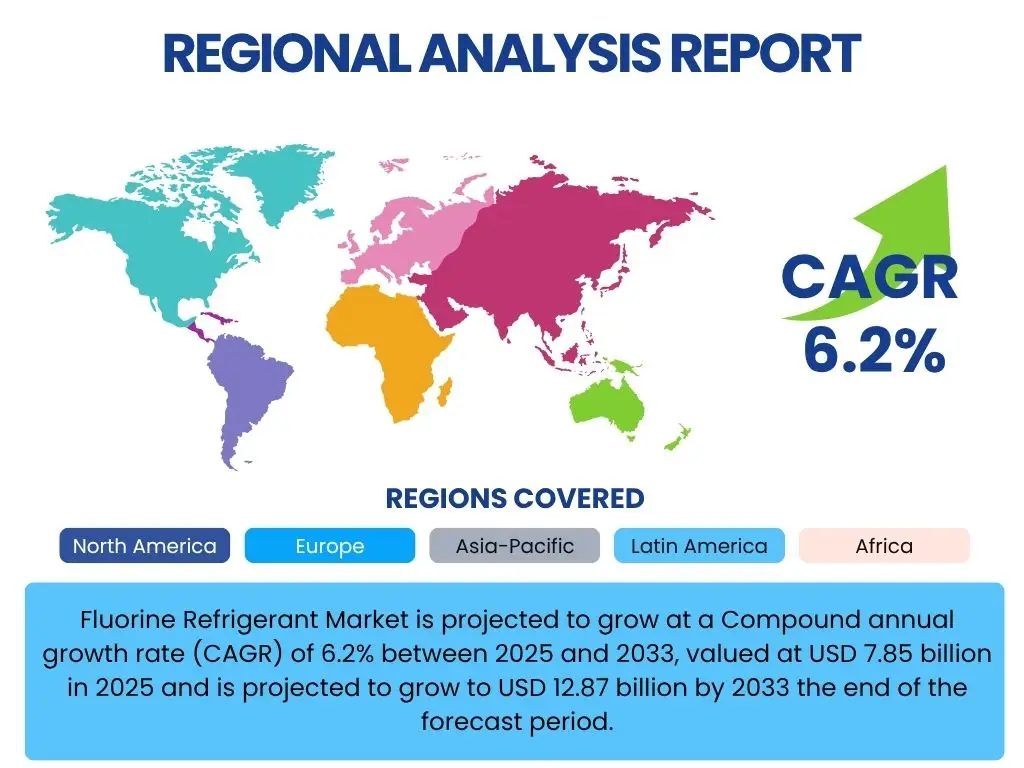

Fluorine Refrigerant Market is projected to grow at a Compound annual growth rate (CAGR) of 6.2% between 2025 and 2033, valued at USD 7.85 billion in 2025 and is projected to grow to USD 12.87 billion by 2033 the end of the forecast period.

Key Fluorine Refrigerant Market Trends & Insights

The fluorine refrigerant market is currently undergoing a transformative period driven by a complex interplay of environmental regulations, technological advancements, and shifting industry demands. Key trends indicate a significant push towards refrigerants with lower Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP), influenced by international agreements and national legislations. Innovations in refrigerant blends and recovery technologies are becoming increasingly important, alongside a growing emphasis on energy efficiency across HVAC-R systems. The market is also witnessing an expansion of natural refrigerant alternatives, although fluorine-based solutions, particularly HFOs, continue to play a crucial role due to their performance characteristics and safety profiles in specific applications. Urbanization and the burgeoning cold chain logistics sector, particularly in developing economies, are further propelling demand for efficient cooling solutions, shaping the market's trajectory towards sustainable yet effective refrigerant options.

- Transition to low-GWP and non-ODP refrigerants.

- Increasing adoption of Hydrofluoroolefins (HFOs) as alternatives.

- Rising demand for energy-efficient refrigeration and air conditioning systems.

- Growth in cold chain logistics, especially in emerging markets.

- Intensified research and development in new refrigerant technologies.

- Stricter environmental regulations driving innovation and market shifts.

- Growing focus on refrigerant recovery and recycling initiatives.

AI Impact Analysis on Fluorine Refrigerant

Artificial Intelligence (AI) is set to significantly impact the fluorine refrigerant market by optimizing various stages of the value chain, from production and distribution to end-use and maintenance. In manufacturing, AI-driven predictive analytics can enhance production efficiency, reduce waste, and improve quality control for refrigerant gases. For logistics and supply chain management, AI algorithms can optimize inventory levels, forecast demand more accurately, and streamline distribution networks, thereby reducing costs and improving responsiveness. In end-use applications, AI integration into HVAC-R systems enables smarter climate control, predictive maintenance, and energy consumption optimization, extending equipment lifespan and improving efficiency. Furthermore, AI can accelerate research and development efforts for novel refrigerant compounds, simulating molecular interactions and predicting performance characteristics, leading to faster innovation in low-GWP alternatives. The ability of AI to analyze vast datasets related to environmental impact and regulatory compliance will also be critical in guiding strategic decisions and ensuring adherence to evolving global standards within the fluorine refrigerant industry.

- Optimization of refrigerant manufacturing processes through predictive analytics.

- Enhanced supply chain efficiency and demand forecasting using AI algorithms.

- Development of smart HVAC-R systems for energy optimization and predictive maintenance.

- Accelerated R&D for novel, environmentally friendly refrigerant formulations.

- Improved leak detection and refrigerant management systems through AI monitoring.

- Data-driven insights for regulatory compliance and environmental impact assessment.

Key Takeaways Fluorine Refrigerant Market Size & Forecast

- The global fluorine refrigerant market is poised for steady growth, driven by expanding HVAC-R industries.

- Demand is primarily propelled by urbanization, industrial expansion, and cold chain development.

- Regulatory pressures are accelerating the shift towards low-GWP and more sustainable refrigerants.

- HFOs are emerging as a key growth segment, replacing older generation refrigerants.

- Challenges include the high cost of new alternatives and complexities in their widespread adoption.

- Opportunities lie in continued R&D for next-generation compounds and retrofit solutions.

- The Asia Pacific region is expected to lead market expansion due to robust economic growth and infrastructure development.

- AI integration will significantly enhance operational efficiencies and accelerate innovation across the market.

Fluorine Refrigerant Market Drivers Analysis

The fluorine refrigerant market is significantly propelled by several robust drivers that underscore the necessity and growth of cooling technologies across various sectors. The burgeoning global demand for air conditioning and refrigeration systems, fueled by rising temperatures, increasing disposable incomes, and rapid urbanization, forms the foundational driver. Industrial expansion, particularly in sectors requiring precise temperature control like food and beverage, pharmaceuticals, and chemicals, further bolsters this demand. Additionally, the continuous growth of the cold chain logistics network, essential for preserving perishable goods and medicines, directly translates into higher consumption of refrigerants. While regulatory shifts favor environmentally friendlier alternatives, the continued innovation in fluorine-based refrigerants, such as HFOs, that meet these new standards ensures their relevance and adoption, driving market expansion by offering efficient and compliant solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for HVAC-R Systems | +1.8% | Global, particularly Asia Pacific and Middle East & Africa | Long-term (2025-2033) |

| Expansion of Cold Chain Logistics | +1.5% | Emerging economies, e-commerce dependent regions | Medium to Long-term (2025-2033) |

| Urbanization and Infrastructure Development | +1.3% | China, India, Southeast Asia, Latin America | Long-term (2025-2033) |

| Technological Advancements in Refrigerant Blends | +0.9% | Developed markets (North America, Europe, Japan) | Medium-term (2025-2029) |

| Increased Adoption of Heat Pump Technology | +0.7% | Europe, North America, East Asia | Medium to Long-term (2025-2033) |

| Demand for Energy-Efficient Cooling Solutions | +0.6% | Global, driven by rising energy costs and sustainability goals | Long-term (2025-2033) |

Fluorine Refrigerant Market Restraints Analysis

Despite significant demand, the fluorine refrigerant market faces substantial restraints, primarily stemming from stringent environmental regulations aimed at mitigating climate change. International protocols and national legislations continuously push for the phase-down or outright ban of high Global Warming Potential (GWP) fluorinated gases, impacting the traditional market for HFCs. The relatively higher cost of new generation, lower-GWP refrigerants, such as HFOs, compared to conventional options presents a significant economic barrier to widespread adoption, particularly for small and medium-sized enterprises. Furthermore, the complexities associated with retrofitting existing equipment to accommodate new refrigerants, coupled with the need for specialized training for technicians, can slow down market transition. Concerns regarding the safety and flammability of certain next-generation refrigerants, along with the potential for illegal trade of phased-out substances, further complicate the market landscape and impede seamless growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations (e.g., F-gas Regulation, Kigali Amendment) | -1.5% | Europe, North America, developed Asia-Pacific nations | Long-term (2025-2033) |

| High Cost of New Generation Low-GWP Refrigerants | -1.2% | Global, particularly developing and cost-sensitive markets | Medium-term (2025-2029) |

| Technical Challenges in Retrofitting Existing Systems | -0.8% | Regions with large installed base of older equipment | Medium-term (2025-2029) |

| Availability and Perception of Natural Refrigerant Alternatives | -0.7% | Europe, North America, industrial sectors | Long-term (2025-2033) |

| Illegal Trade and Supply Chain Irregularities | -0.4% | Global, impacting market stability and legitimate supply | Ongoing (2025-2033) |

Fluorine Refrigerant Market Opportunities Analysis

Significant opportunities exist within the fluorine refrigerant market, primarily driven by the ongoing shift towards more sustainable and efficient cooling solutions. The continuous investment in research and development for low-GWP (Global Warming Potential) and ultra-low-GWP refrigerants, especially Hydrofluoroolefins (HFOs) and their blends, presents a substantial growth avenue as industries seek compliant alternatives to phased-out substances. The burgeoning demand for cold chain infrastructure in developing economies, coupled with expanding food retail and pharmaceutical sectors globally, offers vast untapped potential for refrigeration system installations and refrigerant supply. Furthermore, the extensive installed base of existing HVAC-R equipment worldwide creates a robust retrofit market, where older systems can be upgraded with newer, environmentally friendly fluorine refrigerants, providing a cost-effective path to compliance for many businesses. The growing integration of smart technologies and IoT in cooling systems also opens doors for enhanced refrigerant management and efficiency, presenting additional value creation opportunities for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensive R&D in Low-GWP & Ultra-Low-GWP Refrigerants (e.g., HFOs) | +1.6% | Developed markets, leading chemical manufacturers globally | Long-term (2025-2033) |

| Growing Demand for Cold Chain in Developing Economies | +1.4% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Retrofit Market for Existing HVAC-R Systems | +1.0% | Europe, North America, countries with legacy equipment | Medium-term (2025-2029) |

| Integration of Smart Technology and IoT in Cooling Systems | +0.8% | Global, primarily commercial and industrial applications | Medium to Long-term (2025-2033) |

| Expansion of the Pharmaceutical and Healthcare Cold Chain | +0.7% | Global, particularly post-pandemic healthcare infrastructure build-out | Long-term (2025-2033) |

Fluorine Refrigerant Market Challenges Impact Analysis

The fluorine refrigerant market faces several critical challenges that necessitate strategic adaptation and continuous innovation. The most prominent challenge is the phasedown and eventual phase-out of high-GWP HFCs under international accords and regional regulations, compelling industries to transition to newer, often more expensive, and technically complex alternatives. This transition is further complicated by the technical difficulties associated with integrating these new refrigerants into existing infrastructure, which may require significant system modifications or complete overhauls. Supply chain disruptions, exacerbated by geopolitical events and raw material volatility, pose another significant hurdle, affecting production and distribution stability. Additionally, the fluorine refrigerant industry must contend with the growing advocacy and adoption of natural refrigerants, which, despite their specific application limitations, present a viable alternative that could incrementally erode the market share of fluorinated compounds. Ensuring proper handling, recovery, and recycling of these substances also remains a significant logistical and environmental challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Phasedown of High-GWP HFCs | -1.3% | Global, with varying timelines per region/country | Long-term (2025-2033) |

| Technical Complexities of New Refrigerants (e.g., flammability, toxicity) | -1.0% | Global, impacting system design and safety protocols | Medium to Long-term (2025-2033) |

| Supply Chain Disruptions and Raw Material Volatility | -0.9% | Global, affecting manufacturing and distribution | Short to Medium-term (2025-2027) |

| Competition from Natural Refrigerants (Ammonia, CO2, Hydrocarbons) | -0.7% | Europe, North America, specific industrial applications | Long-term (2025-2033) |

| Skilled Labor Shortage for Installation and Maintenance of New Systems | -0.5% | Global, impacting transition speed and efficiency | Long-term (2025-2033) |

Fluorine Refrigerant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global fluorine refrigerant market, offering critical insights into its current landscape and future growth trajectory. It covers historical performance, current market dynamics, and detailed forecasts, segmenting the market by various criteria to provide a granular view. The report elucidates key market trends, identifies major drivers and restraints, highlights emerging opportunities, and addresses significant challenges impacting the industry. It also includes a detailed competitive landscape analysis profiling key market players and their strategies, alongside regional market assessments, to empower stakeholders with actionable intelligence for strategic decision-making. The scope encompasses the evolution of refrigerant types, their applications across diverse end-use industries, and the profound influence of global environmental regulations and technological advancements on market development.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.85 billion |

| Market Forecast in 2033 | USD 12.87 billion |

| Growth Rate | 6.2% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Global Chemical Systems, Coolant Innovations Group, EcoChem Solutions, Pioneer Fluorine Inc., Refrigerant Technologies Corp., Advanced Cooling Materials, SynTech Refrigerants, GreenFlow Chemicals, ThermoFluid Dynamics, NextGen Fluorine, Summit Cooling Solutions, EnviroChem Refrigerants, Quantum Fluids, Arctic Solutions Group, Evercool Technologies, PureAir Chemical, Delta Refrigeration, Universal Refrigerants, Prime Chemicals Ltd., Alliance Refrigerants. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The fluorine refrigerant market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to the overall market dynamics. This multi-faceted segmentation allows for a granular analysis of various refrigerant types, their specific applications across different sectors, and their utilization within numerous end-use industries. Such a detailed breakdown aids in identifying key growth pockets, understanding regional preferences, and forecasting demand shifts based on technological advancements, regulatory changes, and evolving consumer and industrial needs. The segmentation highlights the market's complexity, driven by the continuous innovation in refrigerant chemistry and the specific requirements of varied cooling and heating systems globally.

- By Type: The market is analyzed across different categories of fluorinated refrigerants, reflecting their chemical composition and environmental impact.

- Hydrochlorofluorocarbons (HCFCs): Legacy refrigerants undergoing phase-out due to ODP.

- Hydrofluorocarbons (HFCs): Widely used, but facing phasedown due to high GWP.

- Hydrofluoroolefins (HFOs): New generation, low-GWP alternatives driving market innovation.

- Others: Includes various blends and emerging fluorinated compounds.

- By Application: This segment examines where fluorine refrigerants are predominantly used, showcasing their diverse utility in cooling and heating systems.

- Commercial Refrigeration: Encompasses systems in supermarkets, hypermarkets, and food service outlets.

- Industrial Refrigeration: Includes applications in chemical processing plants, large-scale cold storage facilities, and food processing units.

- Stationary Air Conditioning: Covers residential AC units, commercial building AC systems, and large chillers.

- Mobile Air Conditioning: Primarily relates to automotive air conditioning and refrigerated transport.

- Heat Pumps: Focuses on their use in modern heating and cooling solutions for buildings.

- Chillers: Large-scale cooling units used in commercial and industrial settings.

- Refrigerated Transport: Specialized systems for maintaining temperature during transit of perishable goods.

- By End-Use Industry: This segmentation explores the sectors that are primary consumers of fluorine refrigerants, reflecting their critical role in various economic activities.

- Food & Beverage: Essential for preservation, processing, and storage.

- Chemical: Used in various chemical reactions and process cooling.

- Pharmaceutical & Healthcare: Critical for drug preservation, vaccine storage, and laboratory cooling.

- Retail: For display cases and cold storage in retail environments.

- Automotive: For vehicle air conditioning systems.

- Building & Construction: For HVAC systems in residential, commercial, and industrial buildings.

- Data Centers: Crucial for cooling server infrastructure.

- Logistics & Shipping: For refrigerated containers and transport vehicles.

- Others: Diverse applications including medical equipment and electronics manufacturing.

Regional Highlights

The global fluorine refrigerant market exhibits significant regional variations, each driven by unique regulatory environments, economic development trajectories, and industrial demands. Understanding these regional dynamics is crucial for comprehensive market analysis and strategic planning.- Asia Pacific (APAC): This region is anticipated to be the fastest-growing and largest market for fluorine refrigerants due to rapid industrialization, burgeoning population growth, and increasing disposable incomes leading to higher adoption of air conditioning and refrigeration systems. Countries like China, India, and Southeast Asian nations are witnessing massive infrastructure development, expansion of cold chain logistics, and a surge in the food and beverage and pharmaceutical sectors, all contributing to robust demand. The region also presents opportunities for the adoption of newer, compliant refrigerants as it modernizes its cooling infrastructure.

- Europe: Characterized by stringent environmental regulations such as the F-gas Regulation, Europe is at the forefront of the transition towards low-GWP and natural refrigerants. While this poses challenges for traditional fluorine refrigerants, it drives innovation and adoption of HFOs and their blends. The region's focus on energy efficiency, sustainability, and circular economy principles is shaping market trends, with a strong emphasis on refrigerant recovery and recycling. Germany, France, and the UK are key markets, investing heavily in compliant cooling solutions and heat pump technologies.

- North America: This region demonstrates a steady demand, driven by well-established HVAC-R industries and increasing awareness regarding energy efficiency. Regulations, particularly the American Innovation and Manufacturing (AIM) Act, are accelerating the phasedown of HFCs and promoting the adoption of next-generation fluorine refrigerants. The US and Canada are significant consumers across commercial, industrial, and automotive sectors, with ongoing efforts to upgrade existing cooling infrastructure to more sustainable options. Innovation in refrigerant technologies and smart cooling solutions is a key regional highlight.

- Latin America: The market in Latin America is experiencing growth due to economic expansion, increasing urbanization, and the development of modern retail and cold chain infrastructure. Countries like Brazil, Mexico, and Argentina are witnessing rising demand for commercial refrigeration and air conditioning. While regulatory frameworks are still evolving, there is a gradual shift towards more environmentally friendly refrigerants, influenced by global trends and increasing environmental consciousness. The region offers opportunities for both new installations and retrofitting projects.

- Middle East and Africa (MEA): This region is characterized by high demand for air conditioning systems due to extreme climatic conditions, coupled with significant investments in infrastructure development, tourism, and food security initiatives. Rapid urbanization and the expansion of modern retail and logistics networks, particularly in the GCC countries and South Africa, are driving the need for efficient cooling and refrigeration. While the adoption of newer refrigerant technologies is emerging, the market still faces challenges related to infrastructure development and the cost-effectiveness of new solutions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Fluorine Refrigerant Market. Some of the leading players profiled in the report include -:- Global Chemical Systems

- Coolant Innovations Group

- EcoChem Solutions

- Pioneer Fluorine Inc.

- Refrigerant Technologies Corp.

- Advanced Cooling Materials

- SynTech Refrigerants

- GreenFlow Chemicals

- ThermoFluid Dynamics

- NextGen Fluorine

- Summit Cooling Solutions

- EnviroChem Refrigerants

- Quantum Fluids

- Arctic Solutions Group

- Evercool Technologies

- PureAir Chemical

- Delta Refrigeration

- Universal Refrigerants

- Prime Chemicals Ltd.

- Alliance Refrigerants

Frequently Asked Questions:

What are fluorine refrigerants?

Fluorine refrigerants are chemical compounds containing fluorine that are primarily used as refrigerants in air conditioning and refrigeration systems. These compounds include hydrochlorofluorocarbons (HCFCs), hydrofluorocarbons (HFCs), and hydrofluoroolefins (HFOs). They are valued for their thermodynamic properties that enable efficient heat transfer, making them suitable for cooling applications across various industries.

Why are fluorine refrigerants being phased out or phased down?

Certain fluorine refrigerants, particularly HCFCs and HFCs, are being phased out or phased down due to their significant environmental impact. HCFCs contribute to ozone depletion, while HFCs are potent greenhouse gases with high Global Warming Potential (GWP), contributing to climate change. International agreements like the Montreal Protocol and its Kigali Amendment, alongside regional regulations such as the European F-gas Regulation, mandate their reduction or elimination to protect the ozone layer and mitigate global warming.

What are the key alternatives to traditional fluorine refrigerants?

The key alternatives to traditional high-GWP fluorine refrigerants fall into two main categories: new-generation fluorinated refrigerants and natural refrigerants. New-generation fluorinated alternatives include Hydrofluoroolefins (HFOs) and their blends, which offer significantly lower GWP while maintaining desirable thermodynamic properties. Natural refrigerants comprise substances like ammonia (R-717), carbon dioxide (R-744), and hydrocarbons (e.g., propane R-290, isobutane R-600a), which have very low or zero GWP and ODP, but often come with specific application constraints regarding flammability, toxicity, or operating pressures.

How big is the market for fluorine refrigerants currently, and what is its projected growth?

The global fluorine refrigerant market was valued at approximately USD 7.85 billion in 2025. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% from 2025 to 2033, reaching an estimated market size of USD 12.87 billion by the end of the forecast period. This growth is driven by increasing demand for cooling solutions across various sectors and the ongoing transition to newer, environmentally compliant refrigerants.

What is the future outlook for the fluorine refrigerant market?

The future outlook for the fluorine refrigerant market is characterized by continued innovation and a strong emphasis on sustainability. The market will see an accelerating shift towards low-GWP HFOs and their blends, driven by global environmental regulations and technological advancements. While natural refrigerants will gain traction in specific applications, fluorine refrigerants will remain crucial for many sectors due to their performance, safety, and energy efficiency. The market will also be influenced by the expansion of cold chain logistics, urbanization, and the integration of smart technologies for optimized refrigerant management and system efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted