Power Generation Equipment Market

Power Generation Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700193 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

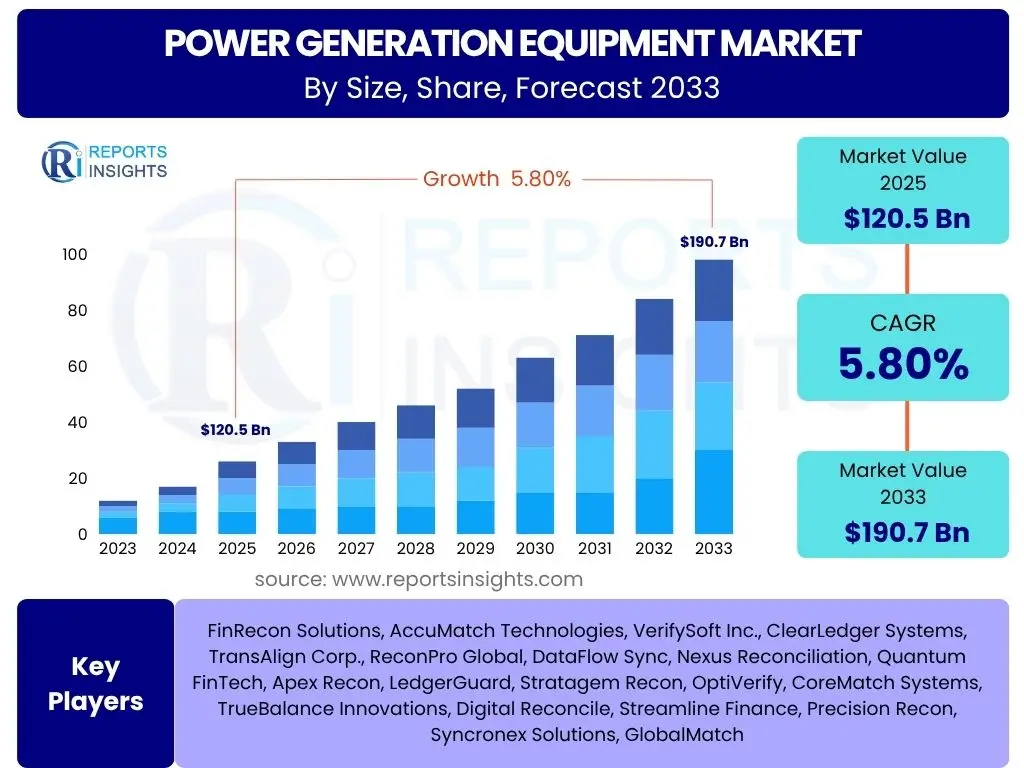

Power Generation Equipment Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 120.5 Billion in 2025 and is projected to grow to USD 190.7 Billion by 2033 the end of the forecast period.

Key Power Generation Equipment Market Trends & Insights

The power generation equipment market is undergoing a significant transformation driven by global energy transitions and technological advancements. Key trends include a strong emphasis on renewable energy integration, the modernization of existing grid infrastructure, and the widespread adoption of smart technologies to enhance efficiency and reliability. Decarbonization initiatives are pushing for cleaner energy sources, impacting the demand for traditional fossil fuel-based equipment while accelerating the uptake of wind, solar, and hydro power solutions. Additionally, the increasing focus on distributed power generation is decentralizing energy production, leading to growth in smaller, modular equipment. This dynamic landscape necessitates continuous innovation and adaptation across the entire power generation value chain.

- Shift towards renewable energy sources (solar, wind, hydro)

- Modernization and digitalization of grid infrastructure

- Integration of smart technologies for operational efficiency

- Focus on decarbonization and emission reduction

- Growth in distributed power generation systems

- Advancements in energy storage solutions complementing generation

- Increased investment in hydrogen-based power solutions

AI Impact Analysis on Power Generation Equipment

Artificial intelligence (AI) is set to revolutionize the power generation equipment market by enhancing operational efficiency, predictive maintenance, and grid management capabilities. AI algorithms can analyze vast amounts of data from sensors embedded in power generation assets to predict equipment failures, optimize performance, and reduce downtime, leading to significant cost savings and improved reliability. Furthermore, AI contributes to smarter grid operations by optimizing energy distribution, integrating variable renewable sources more seamlessly, and managing demand response. Its application extends to advanced analytics for resource planning, enabling better forecasting and strategic investment decisions for future power infrastructure. The increasing sophistication of AI models will drive the development of more autonomous and efficient power systems.

- Enhanced predictive maintenance and fault detection in equipment

- Optimization of power plant performance and efficiency

- Intelligent grid management and load balancing

- Improved forecasting for renewable energy output

- Automated control systems for power generation processes

- Data-driven decision-making for asset management and investment

Key Takeaways Power Generation Equipment Market Size & Forecast

- The global Power Generation Equipment Market is set for robust growth, projected to expand at a CAGR of 5.8% from 2025 to 2033.

- The market is estimated to reach USD 120.5 Billion in 2025, reflecting significant current investment.

- By 2033, the market size is forecasted to reach USD 190.7 Billion, indicating substantial long-term expansion opportunities.

- Growth is primarily fueled by increasing global electricity demand and the accelerating transition to renewable energy sources.

- Technological advancements in smart grids and energy storage systems are key contributors to market expansion.

- Emerging economies in Asia Pacific and Latin America are expected to be major growth drivers due to industrialization and urbanization.

Power Generation Equipment Market Drivers Analysis

The power generation equipment market is propelled by a confluence of macroeconomic and technological factors. A primary driver is the burgeoning global demand for electricity, stemming from rapid urbanization, industrial growth, and the increasing digitalization of economies worldwide. This escalating demand necessitates significant investments in new power generation capacity and the upgrade of existing infrastructure. Simultaneously, global commitments to decarbonization and the urgent need to address climate change are accelerating the adoption of renewable energy technologies. Governments and corporations are setting ambitious targets for clean energy, driving demand for specialized equipment like wind turbines, solar panels, and hydro generators. Furthermore, aging power infrastructure in developed nations requires modernization and replacement, creating a steady demand for advanced, efficient power generation components.

Technological advancements also play a pivotal role, fostering the development of more efficient, reliable, and cost-effective power generation equipment. Innovations in smart grid technologies, energy storage solutions, and predictive maintenance capabilities enhance the overall performance and economic viability of power systems. Policy support, including incentives, subsidies, and favorable regulations for renewable energy projects, further stimulates market growth. The increasing focus on energy security, driven by geopolitical considerations, also encourages diversification of energy sources and investment in domestic power generation capabilities. These interwoven factors collectively create a strong impetus for the expansion and evolution of the power generation equipment market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Electricity Demand Growth | +0.8% | Asia Pacific, Africa, Latin America | Ongoing |

| Transition to Renewable Energy Sources | +1.0% | Europe, North America, China, India | Long-term |

| Aging Infrastructure Modernization | +0.6% | North America, Western Europe, Japan | Mid-term to Long-term |

| Government Policies and Incentives for Clean Energy | +0.7% | Global, particularly EU, US, India, China | Ongoing, Policy-dependent |

| Technological Advancements in Efficiency and Storage | +0.5% | Developed Economies, R&D Hubs | Ongoing |

| Growing Industrialization and Urbanization | +0.7% | Emerging Economies (China, India, Southeast Asia) | Ongoing |

| Energy Security Concerns and Diversification | +0.4% | Europe, Middle East, Asia | Short-term to Mid-term |

Power Generation Equipment Market Restraints Analysis

Despite robust growth prospects, the power generation equipment market faces several significant restraints that could impede its expansion. One primary challenge is the high upfront capital expenditure required for power generation projects, especially for large-scale power plants and renewable energy installations. This substantial investment cost can deter potential investors and lead to delays in project execution, particularly in regions with limited access to financing or unfavorable economic conditions. Regulatory hurdles and complex permitting processes also present a considerable restraint, often causing prolonged lead times for project development and increasing overall costs. Environmental regulations, while necessary, can sometimes lead to stringent requirements that are difficult and expensive for equipment manufacturers and project developers to meet.

Furthermore, volatility in raw material prices, such as steel, copper, and rare earth minerals, directly impacts the manufacturing costs of power generation equipment, potentially leading to increased product prices and reduced profit margins. Grid integration challenges, particularly for intermittent renewable energy sources like solar and wind, pose another technical restraint. Existing grid infrastructure may not be adequately equipped to handle large-scale influxes of variable renewable energy, requiring costly upgrades and smart grid solutions. Geopolitical instability and trade disputes can also disrupt supply chains and hinder international collaborations, affecting market access and equipment availability. These multifaceted restraints demand strategic planning and innovative solutions from market participants to mitigate their adverse effects on growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Projects | -0.7% | Global, particularly Emerging Markets | Ongoing |

| Complex Regulatory and Permitting Processes | -0.5% | Europe, North America, India | Ongoing |

| Fluctuations in Raw Material Prices | -0.4% | Global, Supply Chain Dependent | Short-term to Mid-term |

| Grid Integration Challenges for Renewables | -0.6% | Developing Grids, High Renewable Penetration Areas | Mid-term |

| Public Opposition to Certain Power Projects (e.g., Nuclear, Hydro) | -0.3% | Developed Nations, Environmentally Sensitive Areas | Long-term |

| Shortage of Skilled Workforce | -0.2% | Global, Specialized Fields | Ongoing |

| Intermittency of Renewable Energy Sources | -0.5% | High Renewable Energy Deployment Regions | Ongoing |

Power Generation Equipment Market Opportunities Analysis

The power generation equipment market is rife with significant opportunities, primarily driven by the global energy transition and technological innovation. The aggressive push towards decarbonization and climate goals presents a vast opening for manufacturers of renewable energy equipment, including advanced wind turbines, high-efficiency solar photovoltaic systems, and innovative hydro power solutions. Developing economies, undergoing rapid industrialization and urbanization, represent a substantial untapped market for establishing new power generation capacity, encompassing both conventional and renewable technologies. These regions often lack sufficient existing infrastructure, necessitating comprehensive investments in power plants and associated equipment.

Further opportunities arise from the increasing demand for energy storage solutions, which are crucial for integrating intermittent renewable sources into the grid and enhancing grid stability. This drives demand for related equipment like battery storage systems and advanced control technologies. The modernization of aging grid infrastructure in developed nations, along with the development of smart grids, creates demand for digitalized and interconnected power generation equipment capable of advanced monitoring and control. Furthermore, emerging technologies such as green hydrogen production for power generation, carbon capture, utilization, and storage (CCUS) solutions, and small modular reactors (SMRs) for nuclear power offer long-term growth avenues. Manufacturers who invest in research and development to address these evolving needs are poised to capture substantial market share and drive future innovations within the sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Investment in Renewable Energy Projects | +1.2% | Global, particularly Asia Pacific, Europe | Long-term |

| Expansion into Emerging Markets for New Capacity | +0.9% | Africa, Southeast Asia, Latin America | Mid-term to Long-term |

| Growing Demand for Energy Storage Systems | +0.8% | North America, Europe, China | Ongoing |

| Advancements in Smart Grid and Digitalization Solutions | +0.6% | Developed Economies, Urban Centers | Mid-term |

| Development of Green Hydrogen Economy | +0.5% | Europe, Australia, Middle East | Long-term |

| Decentralization and Distributed Power Generation | +0.7% | Residential, Commercial Sectors Globally | Ongoing |

| Retrofit and Upgrade of Existing Conventional Plants | +0.4% | Developed Nations with Mature Grids | Mid-term |

Power Generation Equipment Market Challenges Impact Analysis

The power generation equipment market faces several critical challenges that can hinder its growth trajectory. One significant hurdle is the intermittent nature of key renewable energy sources like solar and wind, which necessitates advanced grid management and substantial energy storage solutions. This intermittency makes grid balancing complex and requires significant investment in supporting infrastructure, posing a challenge for widespread adoption. Another major challenge is the intense price competition, particularly in the renewable energy equipment sector, driven by a large number of manufacturers and continuous technological advancements. This fierce competition can compress profit margins for companies and lead to market consolidation.

Furthermore, evolving environmental regulations and standards, while driving cleaner energy, also impose complex compliance requirements and can lead to increased operational costs for equipment manufacturers. Supply chain disruptions, exacerbated by geopolitical tensions, trade protectionism, and global events, present a recurring challenge, affecting the availability and cost of critical components and raw materials. Additionally, the transition from conventional fossil fuel-based power generation to renewables creates stranded asset risks for existing infrastructure, leading to resistance from traditional energy players. Addressing these challenges requires significant technological innovation, flexible policy frameworks, and robust global cooperation to ensure a stable and sustainable power generation landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intermittency of Renewable Energy Sources | -0.8% | Regions with High Renewable Penetration | Ongoing |

| Intense Price Competition and Margin Pressure | -0.7% | Global, especially Solar PV and Wind Markets | Ongoing |

| Evolving Regulatory Landscape and Compliance Costs | -0.5% | Developed Economies, Strict Environmental Regions | Ongoing |

| Supply Chain Disruptions and Raw Material Volatility | -0.6% | Global, Geopolitically Sensitive Regions | Short-term to Mid-term |

| Integration Complexity with Existing Infrastructure | -0.4% | Mature Grids in Developed Countries | Mid-term |

| Policy Uncertainty and Lack of Long-Term Clarity | -0.3% | Markets Dependent on Government Support | Short-term |

| Cybersecurity Threats to Digitalized Power Systems | -0.2% | Global, All Digitalized Assets | Ongoing |

Power Generation Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Power Generation Equipment Market, covering historical data, current trends, and future projections. It offers a detailed examination of market dynamics, including key drivers, restraints, opportunities, and challenges influencing industry growth. The report segments the market extensively by various parameters, providing granular insights into specific equipment types, applications, and regional landscapes. Furthermore, it profiles leading market players, offering competitive intelligence and strategic recommendations for stakeholders navigating this evolving sector. This report is an essential resource for businesses, investors, and policymakers seeking to understand and capitalize on the opportunities within the global power generation equipment landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 120.5 Billion |

| Market Forecast in 2033 | USD 190.7 Billion |

| Growth Rate | 5.8% CAGR from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Energy, General Electric, Mitsubishi Heavy Industries, ABB, Schneider Electric, Vestas Wind Systems, Gamesa, Goldwind, Hitachi, Toshiba, Fuji Electric, Doosan Enerbility, MAN Energy Solutions, Wärtsilä, Caterpillar, Cummins, Bharat Heavy Electricals Limited, Rolls-Royce, Shanghai Electric, CRRC Zhuzhou Electric Locomotive |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Generation Equipment Market is comprehensively segmented to provide granular insights into its diverse components and applications. Understanding these segments is crucial for identifying specific growth areas, market dynamics, and competitive landscapes. The market is primarily categorized by equipment type, encompassing a wide array of machinery essential for electricity generation, transmission, and distribution. Further segmentation by fuel source highlights the ongoing transition from traditional fossil fuels to a growing portfolio of renewable energy options, reflecting global sustainability goals. Application and end-use sectors illustrate how these equipment types are deployed across various industries and consumer environments, from large-scale utility operations to localized industrial and residential power solutions. Finally, segmentation by technology differentiates between conventional and non-conventional power generation methods, emphasizing the shift towards greener and more efficient energy production systems.

- By Equipment Type: This segment includes the core machinery used in power generation. Turbines, a critical component, are further broken down into Steam Turbines (used in thermal power plants), Gas Turbines (for combined cycle and peaker plants), Hydro Turbines (for hydroelectric facilities), and Wind Turbines (for wind farms). Generators convert mechanical energy into electrical energy, encompassing Synchronous Generators (widely used) and Asynchronous Generators. Boilers are essential for steam production in thermal power plants, categorized by their fuel source (Coal-fired, Gas-fired, Biomass-fired). Transformers are vital for voltage regulation and transmission, including Power Transformers (for long-distance transmission) and Distribution Transformers (for local distribution). Switchgear components manage and protect electrical circuits across various voltage levels (High Voltage, Medium Voltage, Low Voltage). Other equipment includes Heat Exchangers, Pumps, and Motors that support overall plant operations.

- By Fuel Source: This segmentation highlights the energy input used to generate power. Fossil Fuels remain significant, including Coal, Natural Gas, and Oil, though their share is declining. Renewables represent the fastest-growing segment, comprising Hydro (large and small-scale), Solar (photovoltaic and concentrated solar power), Wind (onshore and offshore), Geothermal (harnessing earth's heat), and Biomass (organic matter). Nuclear power continues to play a role, utilizing nuclear fission. Other emerging sources like Fuel Cells and Waste-to-Energy technologies are also gaining traction.

- By Application: This categorizes where the power generation equipment is utilized. The Utility segment covers large, centralized power plants and associated grid infrastructure designed for widespread electricity distribution. Industrial applications include Captive Power generation (where industries produce their own power) and Co-generation (combined heat and power systems). The Commercial & Residential segment focuses on localized power solutions, such as Distributed Generation and Rooftop Solar installations for buildings and homes.

- By End-Use Sector: This specifies the ultimate consumers of the generated power. The Power & Energy sector encompasses the entire electricity supply chain. Industrial Manufacturing includes heavy industries that require substantial power for operations. The Residential & Commercial sectors cover power consumption in homes, offices, retail spaces, and public buildings. Transportation also increasingly relies on generated power for electric vehicles and public transit systems.

- By Technology: This segment differentiates between established and modern power generation methods. Conventional technologies include Thermal (coal, gas, oil), large-scale Hydro, and Nuclear power plants. Non-Conventional technologies represent renewable energy sources such as Solar PV, Wind Onshore, Wind Offshore,Geothermal, and Biomass, which are characterized by their sustainability and reduced environmental impact.

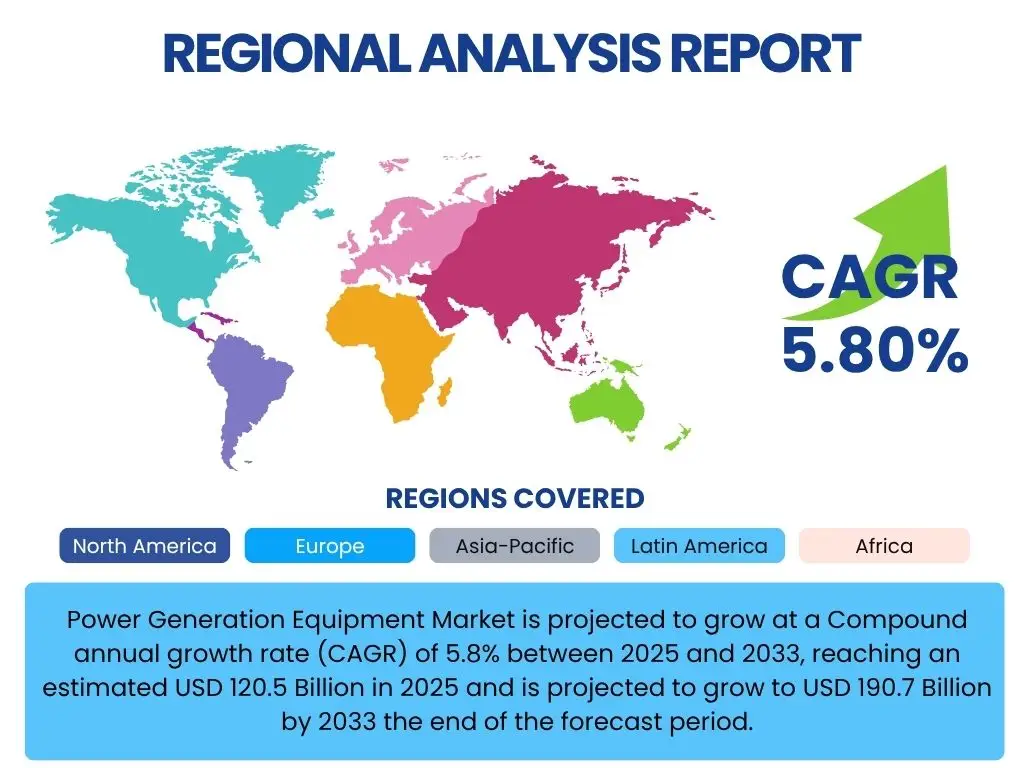

Regional Highlights

The power generation equipment market exhibits distinct growth patterns and driving forces across key geographical regions, each contributing uniquely to the global landscape. Understanding these regional dynamics is crucial for strategic market engagement and investment decisions.

- Asia Pacific (APAC): This region stands as the dominant and fastest-growing market for power generation equipment, primarily driven by rapid industrialization, urbanization, and burgeoning population growth, particularly in China and India. These countries are making massive investments in both conventional and renewable power infrastructure to meet soaring electricity demand. Government initiatives supporting renewable energy deployment, coupled with expanding manufacturing capabilities and the availability of affordable labor, make APAC a critical hub for new installations and equipment production. Countries like Vietnam, Indonesia, and Australia are also significant contributors, focusing on balancing energy security with decarbonization goals.

- North America: The market in North America is characterized by significant investments in grid modernization, replacement of aging infrastructure, and a strong push towards renewable energy integration. The United States, in particular, is witnessing substantial growth in solar and wind power, supported by federal incentives and state-level renewable portfolio standards. There's also a growing focus on energy storage solutions and advanced grid technologies to enhance reliability and resilience. Canada continues to leverage its vast hydroelectric potential while also expanding wind and solar capacities. The region's mature industrial base and robust research and development ecosystem drive innovation in high-efficiency and digitally integrated power generation equipment.

- Europe: Europe is at the forefront of the global energy transition, exhibiting a strong commitment to decarbonization and a rapid expansion of renewable energy sources, especially wind and solar. Countries like Germany, the UK, France, and Spain are leading in terms of installed renewable capacity and supportive policy frameworks. The region's market is driven by ambitious climate targets, the phase-out of coal-fired power plants, and significant investments in offshore wind technology. The focus is also on improving grid interconnectivity, developing green hydrogen infrastructure, and adopting smart grid solutions to manage increased renewable penetration effectively. Eastern European countries are also investing in upgrading their grid infrastructure and diversifying their energy mix.

- Latin America: This region presents a significant growth opportunity, fueled by increasing electricity demand, expanding industrial sectors, and rich renewable energy resources, especially hydro, solar, and wind. Brazil, Mexico, and Chile are key markets, attracting foreign investments in large-scale renewable projects. The need to expand access to electricity in remote areas and reduce reliance on fossil fuel imports further drives the demand for distributed generation and renewable energy equipment. Policy support for renewable auctions and energy independence initiatives are key factors shaping the market here.

- Middle East and Africa (MEA): The MEA region is characterized by diverse market dynamics. The Middle East, traditionally reliant on fossil fuels, is increasingly diversifying its energy mix with massive investments in solar and, to a lesser extent, wind power, driven by sustainability goals and economic diversification strategies in countries like Saudi Arabia and the UAE. Africa, on the other hand, faces a significant energy deficit and is focusing on expanding electrification rates through a mix of large-scale power projects and decentralized renewable solutions. The abundant solar and wind resources, coupled with the need for reliable power, make Africa a promising long-term market for various power generation equipment, especially off-grid and mini-grid solutions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Power Generation Equipment Market. Some of the leading players profiled in the report include -:- Siemens Energy

- General Electric

- Mitsubishi Heavy Industries

- ABB

- Schneider Electric

- Vestas Wind Systems

- Gamesa

- Goldwind

- Hitachi

- Toshiba

- Fuji Electric

- Doosan Enerbility

- MAN Energy Solutions

- Wärtsilä

- Caterpillar

- Cummins

- Bharat Heavy Electricals Limited

- Rolls-Royce

- Shanghai Electric

- CRRC Zhuzhou Electric Locomotive

Frequently Asked Questions:

What is the projected growth rate of the Power Generation Equipment Market?

The Power Generation Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by increasing global electricity demand and the accelerating shift towards renewable energy sources.

What are the primary drivers for the Power Generation Equipment Market?

Key drivers include the escalating global demand for electricity due to urbanization and industrialization, the worldwide transition to renewable energy sources, the modernization of aging power infrastructure, and supportive government policies and incentives for clean energy initiatives.

How does AI impact the Power Generation Equipment Market?

AI significantly impacts the market by enabling advanced predictive maintenance, optimizing power plant performance, facilitating intelligent grid management for better load balancing, and improving forecasting accuracy for renewable energy output, leading to enhanced efficiency and reliability.

Which regions are expected to be key contributors to market growth?

Asia Pacific is expected to be the leading and fastest-growing region due to rapid industrialization and urbanization. North America and Europe will also be significant contributors, driven by grid modernization efforts and aggressive renewable energy targets.

What are the main challenges faced by the Power Generation Equipment Market?

Major challenges include the intermittency of renewable energy sources, intense price competition among manufacturers, complex and evolving regulatory landscapes, and potential supply chain disruptions affecting raw material availability and costs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted