Power Distribution Cable Market

Power Distribution Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705838 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

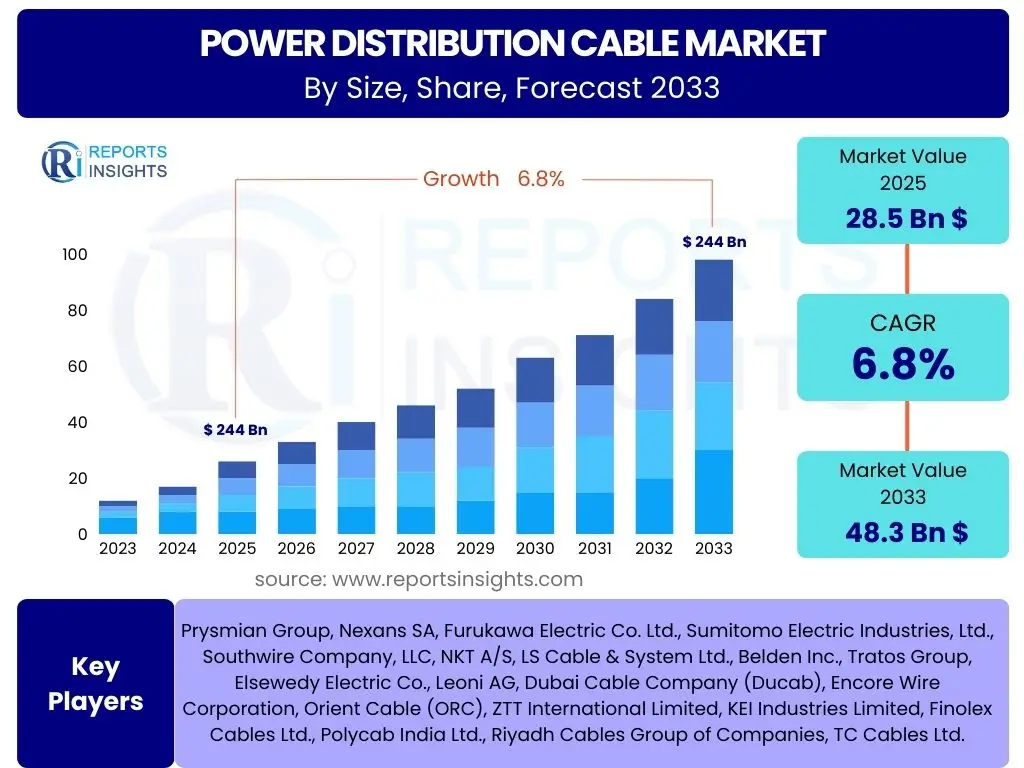

Power Distribution Cable Market Size

According to Reports Insights Consulting Pvt Ltd, The Power Distribution Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at 28.5 Billion USD in 2025 and is projected to reach 48.3 Billion USD by the end of the forecast period in 2033.

Key Power Distribution Cable Market Trends & Insights

The Power Distribution Cable Market is undergoing significant transformation driven by global megatrends and technological advancements. A primary trend is the accelerating transition towards renewable energy sources, such as solar and wind power, which necessitates extensive infrastructure for grid integration and power transmission over long distances. This shift is spurring demand for specialized cables capable of handling varying loads and environmental conditions. Furthermore, rapid urbanization and industrialization, particularly in emerging economies, are fueling massive investments in new power grids and the expansion of existing ones to meet escalating energy demands.

Another crucial insight revolves around the modernization and digitalization of grid infrastructure, often termed as smart grid initiatives. These initiatives aim to enhance grid reliability, efficiency, and resilience through advanced monitoring, control, and automation technologies. The deployment of smart grids requires sophisticated power distribution cables that can support bidirectional power flow and integrate with digital communication networks. Additionally, the growing adoption of electric vehicles (EVs) is creating a new surge in demand for robust charging infrastructure, impacting the design and deployment of local power distribution networks. Material innovations, including lighter, more durable, and environmentally friendly insulation materials, are also shaping the market by improving cable performance and reducing their environmental footprint.

- Accelerated integration of renewable energy sources into national grids.

- Rapid urbanization and industrial expansion driving infrastructure development.

- Increased investment in smart grid technologies and grid modernization.

- Rising adoption of electric vehicles (EVs) and corresponding charging infrastructure build-out.

- Development of advanced cable materials and insulation technologies for enhanced performance.

- Growing preference for underground and submarine cabling for aesthetic and resilience reasons.

AI Impact Analysis on Power Distribution Cable

Artificial Intelligence (AI) is poised to profoundly impact the Power Distribution Cable market, primarily through the optimization and predictive capabilities it offers for grid management. Users frequently inquire about AI's role in enhancing grid reliability, reducing downtime, and improving the overall efficiency of power distribution networks. AI algorithms can analyze vast amounts of data from sensors embedded within smart grids, including cable performance metrics, environmental conditions, and real-time load demands. This analytical capability enables predictive maintenance, allowing utilities to identify potential cable failures before they occur, thus minimizing outages and extending asset lifespan.

Furthermore, AI-driven solutions are crucial for optimizing power flow and managing distributed energy resources, such as rooftop solar panels and battery storage systems, which are increasingly connected to the distribution network. By accurately forecasting demand and supply fluctuations, AI can ensure more efficient utilization of existing cable infrastructure and inform decisions on where new cable deployments are most critical. The technology also plays a role in cybersecurity for smart grids, protecting vital infrastructure from digital threats. While the direct manufacturing of cables may not be AI-intensive, the operational context in which these cables function, and their lifecycle management, will be significantly enhanced by AI, leading to more intelligent and resilient power distribution systems globally.

- Predictive maintenance for cables, minimizing faults and extending operational life.

- Optimized power flow and load management within smart grids.

- Enhanced grid resilience through real-time anomaly detection and rapid response.

- Improved demand forecasting and integration of distributed energy resources.

- Cybersecurity enhancements for protecting digitalized grid infrastructure.

- Automated monitoring and inspection of cable networks.

Key Takeaways Power Distribution Cable Market Size & Forecast

The Power Distribution Cable Market is characterized by robust growth projections, reflecting a fundamental shift in global energy infrastructure and consumption patterns. A key takeaway is the sustained demand for diverse cable types driven by both emerging and developed economies. Developing regions, propelled by rapid urbanization, industrialization, and electrification initiatives, represent significant growth engines, necessitating extensive investments in new power grid installations. Concurrently, developed nations are focusing on modernizing aging infrastructure, integrating renewable energy, and enhancing grid resilience, which also fuels demand for advanced and specialized distribution cables.

Another critical insight is that the market's expansion is intrinsically linked to global decarbonization efforts and the proliferation of smart grid technologies. The transition away from fossil fuels towards cleaner energy sources demands a resilient and efficient network to transmit electricity, where power distribution cables form the backbone. The forecast indicates that innovation in materials science, manufacturing processes, and grid management will be pivotal in shaping the market's trajectory, addressing challenges related to efficiency, sustainability, and operational longevity. Stakeholders must therefore prioritize strategic investments in research and development to capitalize on these evolving market dynamics and maintain competitive advantage.

- Strong growth trajectory driven by global electrification and energy transition.

- Significant demand from both new infrastructure development and grid modernization.

- Renewable energy integration and smart grid initiatives are primary growth catalysts.

- Emphasis on enhanced cable performance, durability, and environmental sustainability.

- Emerging economies present substantial opportunities for market expansion.

Power Distribution Cable Market Drivers Analysis

The Power Distribution Cable Market is propelled by several potent drivers, fundamentally linked to global energy demand and infrastructure development. The increasing demand for reliable electricity, coupled with rapid urbanization and industrialization, especially in developing economies, necessitates continuous expansion and upgrading of power grids. Furthermore, the global shift towards renewable energy sources like solar and wind power requires extensive new cabling infrastructure to connect these generation sites to distribution networks, often over long distances. The modernization of aging power infrastructure in developed countries, aimed at improving grid efficiency and resilience, also contributes significantly to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Renewable Energy Integration | +1.8% | Global, particularly Europe, Asia Pacific, North America | 2025-2033 (Long-term) |

| Urbanization and Industrialization | +1.5% | Asia Pacific (China, India), Africa, Latin America | 2025-2033 (Mid to Long-term) |

| Smart Grid Initiatives & Grid Modernization | +1.2% | North America, Europe, select Asia Pacific countries | 2025-2033 (Mid to Long-term) |

| Aging Infrastructure Replacement | +1.0% | North America, Europe, Japan | 2025-2033 (Consistent) |

| Electric Vehicle (EV) Charging Infrastructure | +0.8% | Global, especially Europe, China, North America | 2025-2033 (Accelerating) |

Power Distribution Cable Market Restraints Analysis

Despite robust growth prospects, the Power Distribution Cable Market faces several significant restraints that could impede its expansion. High initial investment costs associated with new cable deployment, particularly for underground and submarine installations, pose a financial barrier for utilities and developers. Fluctuating prices of raw materials, such as copper and aluminum, introduce volatility into manufacturing costs and can impact project viability and profitability. Additionally, stringent environmental regulations regarding cable disposal and the use of certain materials present compliance challenges and can increase operational complexities. Slow and complex project approval processes in various regions also delay infrastructure development, acting as a decelerating factor for market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -0.9% | Global | 2025-2033 (Persistent) |

| Volatile Raw Material Prices | -0.7% | Global (All regions) | 2025-2033 (Fluctuating) |

| Environmental Regulations & Disposal Challenges | -0.6% | Europe, North America, parts of Asia Pacific | 2025-2033 (Increasingly stringent) |

| Complex Permitting and Regulatory Hurdles | -0.5% | Global, specific impact by country | 2025-2033 (Ongoing) |

Power Distribution Cable Market Opportunities Analysis

The Power Distribution Cable Market is abundant with opportunities stemming from evolving energy landscapes and technological advancements. The burgeoning offshore wind power sector, requiring specialized submarine cables for energy transmission, represents a significant growth avenue. The global push for smart cities and microgrid development offers demand for integrated and resilient distribution cable networks capable of supporting localized energy systems. Furthermore, the increasing adoption of High-Voltage Direct Current (HVDC) transmission technology, which requires high-performance cables for long-distance bulk power transfer with minimal losses, creates a niche for advanced cable solutions. Innovations in cable design, such as superconducting cables and those with enhanced fire resistance, also present new market segments and competitive advantages.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Offshore Wind Farm Development | +1.1% | Europe, North America, Asia Pacific (China, Japan) | 2025-2033 (Significant) |

| Smart City & Microgrid Expansion | +0.9% | Global (Urban centers) | 2025-2033 (Growing) |

| HVDC Cable Technology Adoption | +0.8% | Global (Long-distance transmission projects) | 2025-2033 (Emerging) |

| Development of Specialized & Advanced Cables | +0.7% | Global (R&D focused regions) | 2025-2033 (Continuous) |

Power Distribution Cable Market Challenges Impact Analysis

The Power Distribution Cable Market confronts several challenges that demand strategic responses from industry players. Cybersecurity threats to interconnected smart grid infrastructure pose a risk to operational integrity and data security, necessitating robust protective measures in cable systems and network protocols. The complexities arising from diverse and often conflicting regulatory frameworks across different countries and regions can complicate international market entry and standardized product development. Moreover, a persistent shortage of skilled labor for cable installation, maintenance, and smart grid management presents an operational bottleneck. Lastly, the increasing frequency and intensity of extreme weather conditions globally threaten the physical resilience of overhead and even underground cable infrastructure, requiring more robust and resilient designs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Smart Grids | -0.8% | Global (especially developed regions) | 2025-2033 (Increasing) |

| Complex Regulatory & Policy Environment | -0.7% | Global (diverse country-specific impacts) | 2025-2033 (Ongoing) |

| Shortage of Skilled Workforce | -0.6% | North America, Europe, parts of Asia Pacific | 2025-2033 (Persistent) |

| Impact of Extreme Weather Conditions | -0.5% | Global (regions prone to natural disasters) | 2025-2033 (Growing) |

Power Distribution Cable Market - Updated Report Scope

This report provides a comprehensive analysis of the Power Distribution Cable market, offering detailed insights into its size, growth trends, key drivers, restraints, opportunities, and challenges. It segments the market by various types, applications, and end-use industries, providing a granular view of market dynamics across different regions. The scope encompasses historical data analysis from 2019 to 2023, coupled with robust forecasts extending to 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 28.5 Billion USD |

| Market Forecast in 2033 | 48.3 Billion USD |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Prysmian Group, Nexans SA, Furukawa Electric Co. Ltd., Sumitomo Electric Industries, Ltd., Southwire Company, LLC, NKT A/S, LS Cable & System Ltd., Belden Inc., Tratos Group, Elsewedy Electric Co., Leoni AG, Dubai Cable Company (Ducab), Encore Wire Corporation, Orient Cable (ORC), ZTT International Limited, KEI Industries Limited, Finolex Cables Ltd., Polycab India Ltd., Riyadh Cables Group of Companies, TC Cables Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Power Distribution Cable market is extensively segmented to reflect the diverse applications and technical specifications demanded by various sectors. These segmentations allow for a granular understanding of market dynamics, identifying specific growth pockets and technological preferences. The market is primarily bifurcated by voltage level, encompassing High Voltage (HV), Medium Voltage (MV), and Low Voltage (LV) cables, each catering to distinct transmission and distribution needs. Insulation type also forms a critical segmentation, with XLPE and PVC being predominant, alongside PILC and EPR, reflecting advancements in material science for improved performance and environmental considerations.

Further segmentation by end-use application highlights the varied demand from sectors such as utilities, industrial, commercial, and residential, along with specialized requirements from renewable energy projects and transportation infrastructure like electric vehicles and railways. The installation type distinguishes between overhead, underground, and submarine cables, each presenting unique engineering challenges and environmental impacts. This comprehensive segmentation provides a detailed map of the market, allowing stakeholders to pinpoint opportunities and tailor their strategies to specific industry and geographical needs, ensuring optimal resource allocation and market penetration.

- By Voltage Level: High Voltage (HV), Medium Voltage (MV), Low Voltage (LV)

- By Insulation Type: XLPE (Cross-linked Polyethylene), PVC (Polyvinyl Chloride), PILC (Paper Insulated Lead Covered), EPR (Ethylene Propylene Rubber), Other Insulation Types

- By End-Use Application: Utilities, Industrial, Commercial, Residential, Renewable Energy (Solar Farms, Wind Farms), Transportation (Railways, Electric Vehicles)

- By Installation Type: Overhead Cables, Underground Cables, Submarine Cables

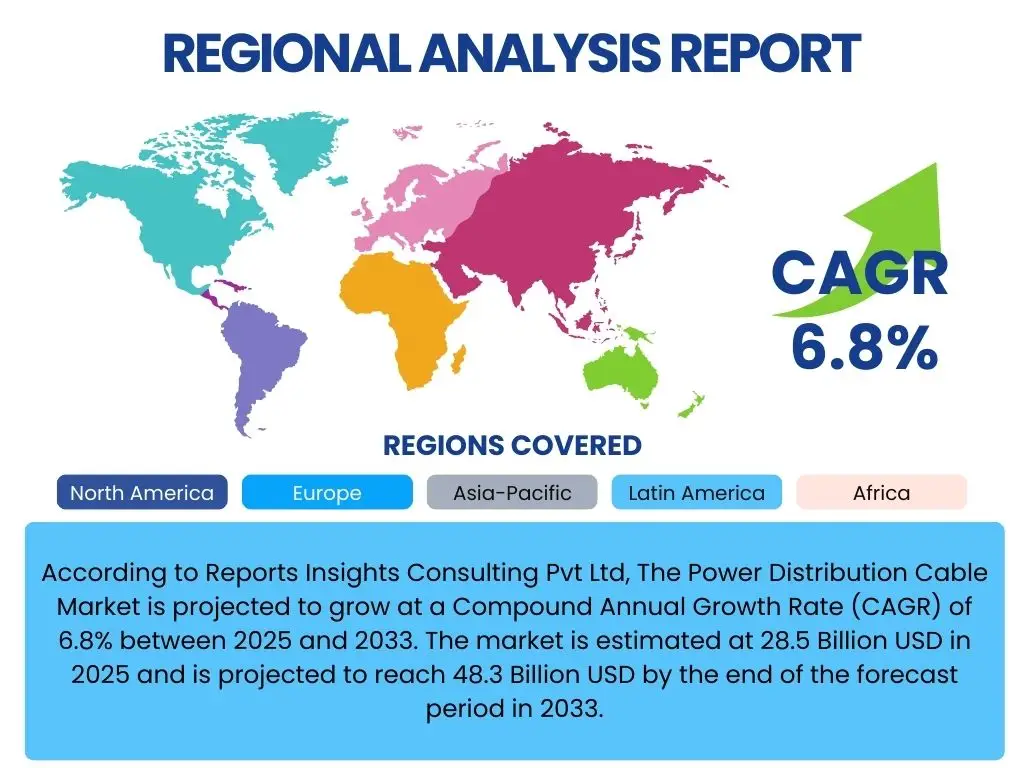

Regional Highlights

The Power Distribution Cable Market exhibits varied dynamics across key geographical regions, driven by distinct regulatory landscapes, economic development, and infrastructure priorities. North America and Europe are characterized by significant investments in grid modernization, replacement of aging infrastructure, and the integration of renewable energy sources. These regions are also witnessing increased adoption of smart grid technologies, driving demand for advanced and high-performance cables designed for efficiency and resilience. The emphasis on sustainability and reducing carbon footprints further fuels the demand for environmentally friendly cable solutions.

Asia Pacific is projected to be the fastest-growing market, primarily due to rapid urbanization, industrialization, and massive government investments in new power infrastructure projects, particularly in countries like China and India. The expanding population and growing energy demand necessitate extensive new grid installations and upgrades. Latin America and the Middle East & Africa (MEA) are also experiencing growth, albeit at a different pace, driven by electrification initiatives, infrastructure development, and increasing industrial activities. The MEA region, in particular, benefits from investments in smart cities and renewable energy projects, contributing to sustained demand for power distribution cables across their developing economies.

- North America: Strong focus on grid modernization, smart grid deployment, and aging infrastructure replacement; significant investments in renewable energy integration.

- Europe: Leading the transition to renewable energy; extensive grid reinforcement projects; high emphasis on environmental regulations and sustainable cable solutions.

- Asia Pacific (APAC): Dominant growth region due to rapid urbanization, industrialization, and large-scale infrastructure development; high energy demand from emerging economies like China and India.

- Latin America: Growing demand driven by electrification projects, industrial expansion, and investments in renewable energy infrastructure.

- Middle East and Africa (MEA): Increasing investments in smart cities, renewable energy projects, and general infrastructure development to support economic diversification.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Power Distribution Cable Market.- Prysmian Group

- Nexans SA

- Furukawa Electric Co. Ltd.

- Sumitomo Electric Industries, Ltd.

- Southwire Company, LLC

- NKT A/S

- LS Cable & System Ltd.

- Belden Inc.

- Tratos Group

- Elsewedy Electric Co.

- Leoni AG

- Dubai Cable Company (Ducab)

- Encore Wire Corporation

- Orient Cable (ORC)

- ZTT International Limited

- KEI Industries Limited

- Finolex Cables Ltd.

- Polycab India Ltd.

- Riyadh Cables Group of Companies

- TC Cables Ltd.

Frequently Asked Questions

Analyze common user questions about the Power Distribution Cable market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Power Distribution Cable Market?

The Power Distribution Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated 48.3 Billion USD by 2033.

Which key factors are driving the Power Distribution Cable Market?

Key drivers include the global push for renewable energy integration, rapid urbanization and industrialization, significant investments in smart grid initiatives and grid modernization, replacement of aging infrastructure, and the expansion of electric vehicle charging networks.

How is AI impacting the Power Distribution Cable sector?

AI primarily impacts the sector by enabling predictive maintenance for cables, optimizing power flow in smart grids, enhancing grid resilience through anomaly detection, improving demand forecasting, and bolstering cybersecurity measures for critical infrastructure.

What are the primary regional growth opportunities for power distribution cables?

Asia Pacific is expected to exhibit the fastest growth due to extensive infrastructure development, while North America and Europe focus on smart grid modernization and renewable energy integration. Latin America and MEA are driven by electrification and industrial expansion.

What types of cables are most prevalent in power distribution?

Power distribution cables are segmented by voltage level (HV, MV, LV), insulation type (XLPE, PVC, PILC), end-use application (utilities, industrial, residential, renewable energy), and installation type (overhead, underground, submarine).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted