Cast Component for Wind Turbine Market

Cast Component for Wind Turbine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708066 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Cast Component for Wind Turbine Market Size

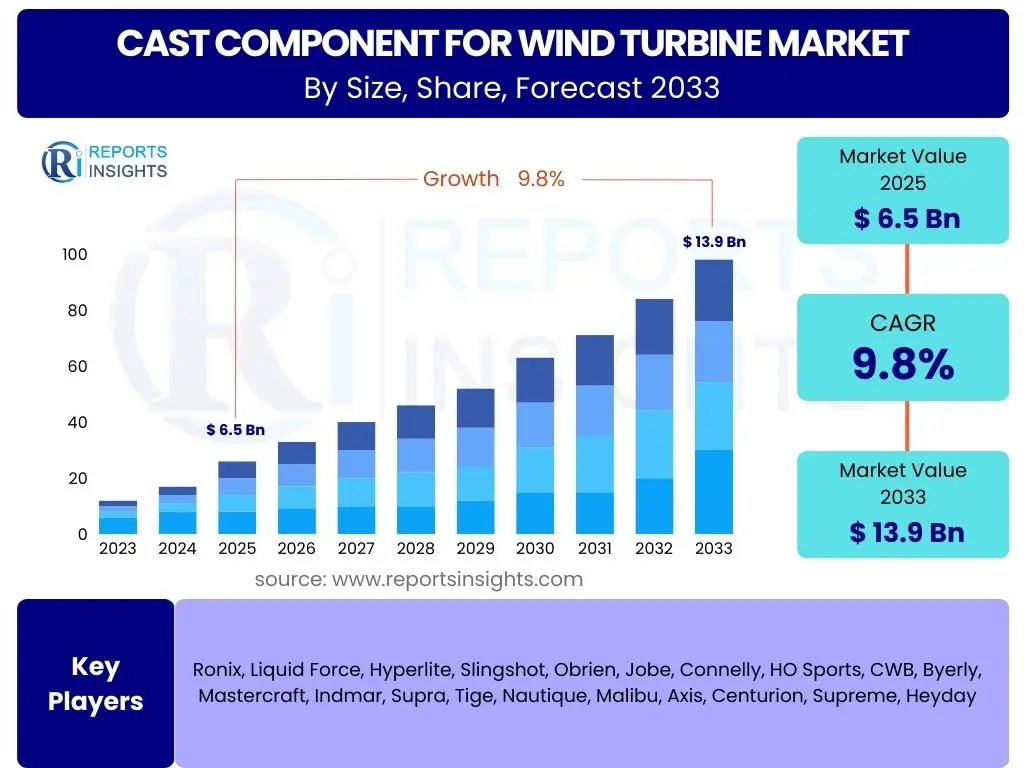

According to Reports Insights Consulting Pvt Ltd, The Cast Component for Wind Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 6.5 Billion in 2025 and is projected to reach USD 13.9 Billion by the end of the forecast period in 2033.

The consistent expansion of the global renewable energy sector, particularly wind power, serves as a fundamental driver for this market growth. As nations worldwide commit to decarbonization targets and invest heavily in sustainable infrastructure, the demand for robust and efficient wind turbine components, predominantly cast parts, continues its upward trajectory. These components are critical for the structural integrity and operational longevity of wind turbines, directly influencing their performance and reliability across diverse environmental conditions.

Technological advancements in casting processes, material science, and turbine design are also significant contributors to the market's projected growth. Manufacturers are continuously innovating to produce lighter, stronger, and more durable cast components capable of withstanding extreme stresses and operating in harsher environments, such as offshore wind farms. This focus on performance enhancement and cost-effectiveness through improved manufacturing techniques is expected to bolster market expansion over the forecast period.

Key Cast Component for Wind Turbine Market Trends & Insights

The market for cast components in wind turbines is undergoing significant transformation, driven by a confluence of technological advancements, evolving energy policies, and growing environmental concerns. Common inquiries from industry stakeholders often center on material innovations, the impact of turbine scaling, and the increasing emphasis on supply chain resilience. There is a clear trend towards optimizing component design for enhanced durability and performance, while simultaneously exploring sustainable manufacturing processes to reduce the carbon footprint associated with production.

Furthermore, the shift towards larger, more powerful wind turbines, especially in the offshore segment, is mandating the development of immensely complex and precise cast components. This trend necessitates closer collaboration between foundries, material scientists, and turbine original equipment manufacturers (OEMs) to ensure components can withstand increased mechanical loads and environmental stresses. Automation and digitalization within casting operations are also emerging as key trends to improve efficiency, reduce lead times, and enhance product quality.

- Upscaling of Wind Turbine Size: Development of larger, more powerful turbines, particularly for offshore applications, requiring bigger and more complex cast components.

- Advanced Material Development: Adoption of higher-strength, lighter, and more durable alloys and composite materials for improved component performance and longevity.

- Additive Manufacturing Integration: Exploration and gradual integration of additive manufacturing (3D printing) for prototyping, complex part production, and repair of cast components.

- Digitalization and Industry 4.0: Increased use of smart manufacturing, IoT, and data analytics for process optimization, predictive maintenance, and supply chain management in casting operations.

- Sustainability and Circular Economy: Growing emphasis on eco-friendly casting processes, material recycling, and reduction of waste throughout the component lifecycle.

- Supply Chain Localization and Diversification: Efforts to reduce reliance on single-source suppliers and to establish regional manufacturing hubs to enhance resilience and reduce geopolitical risks.

AI Impact Analysis on Cast Component for Wind Turbine

Artificial Intelligence (AI) is poised to revolutionize various aspects of the cast component for wind turbine market, addressing user concerns around efficiency, quality control, and predictive maintenance. Stakeholders are keen to understand how AI can optimize casting processes, reduce defects, and accelerate design iterations. The application of AI algorithms allows for advanced simulation and modeling, enabling foundries to predict material behaviors under specific casting conditions, thereby minimizing trial-and-error and speeding up product development cycles. This directly contributes to higher production yields and reduced waste, aligning with sustainability goals.

Beyond the manufacturing floor, AI significantly impacts the operational phase of wind turbines. Predictive maintenance, powered by AI-driven analytics, can monitor the real-time performance of cast components, identifying potential failures before they occur. This capability drastically reduces downtime, extends component lifespan, and lowers maintenance costs, offering substantial economic benefits to wind farm operators. Furthermore, AI can aid in supply chain optimization, from demand forecasting for raw materials to logistics planning for component delivery, enhancing overall market efficiency and responsiveness.

- Optimized Casting Processes: AI algorithms analyze data from casting simulations and real-world production to fine-tune parameters, reducing defects and improving material utilization.

- Predictive Maintenance: AI-powered sensors and analytics monitor component health in real-time, predicting potential failures and enabling proactive maintenance, reducing downtime.

- Accelerated Design and R&D: Machine learning models aid in rapid prototyping and material selection, shortening the design cycle for new and improved cast components.

- Enhanced Quality Control: AI vision systems and data analysis detect microscopic flaws in cast parts more accurately and consistently than traditional methods, ensuring higher quality standards.

- Supply Chain Optimization: AI tools forecast demand, manage inventory, and optimize logistics for raw materials and finished cast components, improving efficiency and reducing costs.

- Robotics and Automation: AI integration with robotics in casting and finishing processes enhances precision, speeds up production, and improves worker safety.

Key Takeaways Cast Component for Wind Turbine Market Size & Forecast

The robust growth projected for the Cast Component for Wind Turbine Market underscores the critical role of wind energy in the global energy transition. User inquiries consistently highlight the market's resilience, driven by ambitious renewable energy targets and continuous innovation in turbine technology. A primary takeaway is the significant expansion expected across both onshore and offshore wind segments, demanding increasingly sophisticated and large-scale cast parts to support more powerful and efficient turbines. This growth trajectory offers substantial opportunities for manufacturers capable of meeting evolving technical specifications and production volumes.

Another crucial insight is the increasing emphasis on the durability, reliability, and sustainability of cast components. As wind farms operate for longer durations in more challenging environments, the quality and longevity of every component become paramount. This drives investment in advanced materials, improved casting techniques, and stringent quality control measures, which will define competitive advantage. Furthermore, the market's future will be heavily influenced by geopolitical factors, supply chain dynamics, and the ability of the industry to adopt and integrate advanced manufacturing technologies like AI and automation to enhance efficiency and reduce costs.

- Significant Market Expansion: The market is poised for substantial growth, nearly doubling in value by 2033, driven by global wind energy expansion.

- Strategic Importance of Components: Cast components are foundational to turbine performance and longevity, directly impacting the efficiency and reliability of wind energy projects.

- Innovation-Driven Growth: Continuous advancements in material science, casting technologies, and turbine design are critical for meeting future market demands.

- Offshore Wind Dominance: The escalating development of offshore wind farms will be a primary growth catalyst, requiring specialized, high-performance cast parts.

- Sustainability Imperative: Environmental considerations and the drive for circular economy principles are influencing manufacturing processes and material choices within the sector.

Cast Component for Wind Turbine Market Drivers Analysis

The global shift towards renewable energy sources is the paramount driver for the cast component for wind turbine market. Governments worldwide are implementing supportive policies, subsidies, and ambitious targets to increase renewable energy generation, with wind power at the forefront. This policy-driven acceleration directly translates into a higher demand for wind turbine installations, consequently boosting the need for essential cast components. As nations strive to reduce carbon emissions and achieve energy independence, the wind energy sector benefits from sustained investment and regulatory backing, creating a stable and growing market for its supply chain.

Furthermore, the decreasing Levelized Cost of Electricity (LCOE) for wind power has made it increasingly competitive with traditional fossil fuel-based generation. This economic viability encourages greater adoption of wind energy projects, attracting more private and public investment. Technological advancements leading to more efficient and larger turbines, coupled with optimized manufacturing processes for cast components, contribute to this cost reduction, making wind power a more attractive and accessible energy solution globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Renewable Energy Targets & Policies | +3.0% | Europe, North America, APAC (China, India) | Short to Long-term (2025-2033) |

| Decreasing Levelized Cost of Electricity (LCOE) for Wind Power | +2.5% | Global | Mid to Long-term (2026-2033) |

| Technological Advancements in Turbine Design & Capacity | +2.0% | Europe, APAC (China), North America | Short to Mid-term (2025-2030) |

| Growth in Offshore Wind Energy Projects | +1.5% | Europe, APAC (China, Taiwan), North America (USA) | Mid to Long-term (2026-2033) |

Cast Component for Wind Turbine Market Restraints Analysis

Despite the robust growth, the cast component for wind turbine market faces several significant restraints, notably the volatility of raw material prices and the complexities of global supply chains. Fluctuations in the cost of metals like iron and steel, which are primary inputs for cast components, directly impact manufacturing costs and profit margins. This unpredictability can lead to budget overruns for wind farm developers and create financial instability for component manufacturers. Geopolitical events, trade policies, and disruptions in global mining and processing industries can exacerbate these price variations, posing a continuous challenge to market stability.

Another key restraint is the high capital expenditure required for establishing and upgrading advanced casting facilities. The production of large, high-precision cast components for modern wind turbines demands significant investment in specialized machinery, tooling, and skilled labor. This high barrier to entry can limit competition and innovation, particularly for smaller enterprises. Additionally, stringent quality and certification standards for critical components, while necessary for safety and performance, can add to manufacturing complexity and cost, potentially slowing down market entry for new players or new product lines.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility (Iron, Steel) | -1.8% | Global | Short to Mid-term (2025-2030) |

| Supply Chain Disruptions and Logistics Challenges | -1.5% | Global | Short-term (2025-2027) |

| High Capital Investment for Advanced Foundry Technologies | -1.2% | Global | Long-term (2025-2033) |

| Stringent Quality Standards and Certification Processes | -0.8% | Europe, North America | Short to Mid-term (2025-2030) |

Cast Component for Wind Turbine Market Opportunities Analysis

The increasing global investment in offshore wind energy presents a significant opportunity for the cast component market. Offshore turbines are generally larger and require more robust and specialized cast components to withstand harsh marine environments and increased operational loads. This segment demands innovative material solutions and advanced manufacturing techniques, creating a premium market for high-performance cast parts. As more countries develop their offshore wind capabilities, the demand for these specialized components is expected to surge, offering substantial growth avenues for manufacturers capable of meeting these stringent requirements.

Another prominent opportunity lies in the development and adoption of advanced materials and manufacturing processes, including digital casting and additive manufacturing. These innovations can lead to lighter, stronger, and more cost-effective components, improving turbine efficiency and reducing overall project costs. Furthermore, the growing focus on the circular economy and sustainability within the wind industry creates opportunities for manufacturers to develop eco-friendly casting processes, utilize recycled materials, and design components for easier end-of-life recycling. This not only aligns with environmental goals but also provides a competitive edge in a market increasingly prioritizing sustainability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Offshore Wind Energy Projects | +2.2% | Europe, APAC (China, Vietnam), North America | Mid to Long-term (2026-2033) |

| Development of Advanced Materials and Casting Technologies | +1.8% | Global | Short to Mid-term (2025-2030) |

| Emerging Markets and Developing Economies | +1.5% | APAC (India, Southeast Asia), Latin America, MEA | Mid to Long-term (2026-2033) |

| Focus on Component Lifetime Extension and Predictive Maintenance | +1.0% | Global | Short to Long-term (2025-2033) |

Cast Component for Wind Turbine Market Challenges Impact Analysis

The cast component for wind turbine market faces a significant challenge in managing the complex and often fragmented global supply chain. The production of large, specialized castings requires raw materials from various sources, extensive manufacturing processes, and intricate logistics for transportation. Any disruption, whether from geopolitical tensions, natural disasters, or trade disputes, can cause significant delays and cost escalations. This vulnerability necessitates greater diversification and localization of supply chains, which itself presents logistical and investment challenges for component manufacturers and turbine OEMs seeking to maintain efficiency and reliability.

Another critical challenge stems from the intense competitive landscape and the continuous pressure to reduce costs while simultaneously improving performance. Wind turbine manufacturers consistently seek more cost-effective solutions for components without compromising on quality or durability. This places immense pressure on cast component suppliers to innovate in manufacturing processes, optimize material usage, and achieve economies of scale. Balancing these demands, particularly when faced with high raw material costs and stringent quality requirements, remains a persistent obstacle for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Global Supply Chain Management | -1.7% | Global | Short to Mid-term (2025-2030) |

| Intense Price Competition and Cost Reduction Pressures | -1.4% | Global | Short to Long-term (2025-2033) |

| Skilled Labor Shortages in Advanced Casting | -1.0% | Europe, North America, APAC (Japan) | Mid to Long-term (2026-2033) |

| Integration of New Technologies and Digitalization | -0.9% | Global | Mid-term (2026-2031) |

Cast Component for Wind Turbine Market - Updated Report Scope

This comprehensive market report provides a detailed analysis of the global cast component for wind turbine market, offering in-depth insights into its size, growth drivers, restraints, opportunities, and challenges. The scope extends to a meticulous segmentation analysis by component type, material, turbine application, and geographical region, alongside a competitive landscape assessment of key market players. It aims to furnish stakeholders with actionable intelligence to navigate market dynamics and identify strategic growth avenues within the evolving wind energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 13.9 Billion |

| Growth Rate | 9.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., General Electric Company, Enercon GmbH, Nordex SE, Goldwind Science & Technology Co., Ltd., Ming Yang Smart Energy Group Limited, Suzlon Energy Ltd., TPI Composites Inc., ArcelorMittal, DHI Group, GL Garrad Hassan, SGS SA, Casting Technology Co. Ltd., Sinoma Wind Power Blade Co. Ltd., XEMC Windpower Co., Ltd., ZF Friedrichshafen AG, NGC Gear Group, Vacon Oy, thyssenkrupp AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cast Component for Wind Turbine Market is meticulously segmented to provide a granular understanding of its diverse facets, reflecting the varied requirements of wind energy projects. These segmentations are critical for identifying specific market niches, understanding demand patterns across different component types and materials, and assessing the influence of turbine application and capacity on component design and manufacturing. This structured analysis enables stakeholders to tailor strategies for product development, market entry, and supply chain optimization, ensuring relevance and competitiveness in a rapidly evolving industry landscape.

- By Component Type: Includes critical parts such as nacelle components (gearbox housing, main shaft, main bearing housing), hub components, yaw system components, blade root connectors, and tower base sections, each vital for turbine functionality.

- By Material: Categorized into ductile iron (nodular cast iron), gray iron (grey cast iron), steel alloys (cast steel), and specialty alloys, reflecting the material science advancements and performance requirements.

- By Turbine Application: Differentiated between onshore wind turbines and offshore wind turbines, acknowledging the distinct design and durability demands of each environment.

- By Capacity: Segmented by turbine power output, including less than 3 MW, 3 MW to 5 MW, and above 5 MW, indicative of the scaling trends and engineering complexities involved.

Regional Highlights

- North America: A significant market driven by renewable energy mandates, growing investments in wind farms, and advancements in turbine technology, particularly in the United States and Canada.

- Europe: A mature market with strong government support for wind energy, extensive offshore wind development, and a robust manufacturing base for cast components, led by Germany, UK, and Denmark.

- Asia Pacific (APAC): The fastest-growing region, dominated by China's massive wind power expansion, along with increasing installations in India, Japan, and Australia, driven by energy demand and clean energy policies.

- Latin America: An emerging market with strong growth potential, particularly in countries like Brazil and Mexico, benefiting from favorable wind resources and government initiatives.

- Middle East and Africa (MEA): A nascent but growing market, with increasing interest in renewable energy projects to diversify energy portfolios, leading to gradual investment in wind power infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cast Component for Wind Turbine Market.- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy S.A.

- General Electric Company

- Enercon GmbH

- Nordex SE

- Goldwind Science & Technology Co., Ltd.

- Ming Yang Smart Energy Group Limited

- Suzlon Energy Ltd.

- TPI Composites Inc.

- ArcelorMittal

- DHI Group

- GL Garrad Hassan

- SGS SA

- Casting Technology Co. Ltd.

- Sinoma Wind Power Blade Co. Ltd.

- XEMC Windpower Co., Ltd.

- ZF Friedrichshafen AG

- NGC Gear Group

- Vacon Oy

- thyssenkrupp AG

Frequently Asked Questions

What is the projected growth rate for the Cast Component for Wind Turbine Market?

The Cast Component for Wind Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033, reaching USD 13.9 Billion by 2033.

Which factors are primarily driving the growth of this market?

The market growth is primarily driven by global renewable energy targets and policies, the decreasing Levelized Cost of Electricity (LCOE) for wind power, and continuous technological advancements in turbine design and capacity.

How is AI impacting the cast component sector for wind turbines?

AI is significantly impacting the sector by optimizing casting processes, enabling predictive maintenance, accelerating design and R&D, enhancing quality control, and improving supply chain efficiency.

What are the key challenges faced by manufacturers in this market?

Key challenges include raw material price volatility, complex global supply chain management, intense price competition, and the high capital investment required for advanced foundry technologies.

Which region is expected to lead market growth for cast components in wind turbines?

The Asia Pacific (APAC) region is expected to lead market growth, driven by extensive wind power expansion in countries like China and India, coupled with increasing energy demand and clean energy policies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted