HDPE Microduct Market

HDPE Microduct Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701190 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

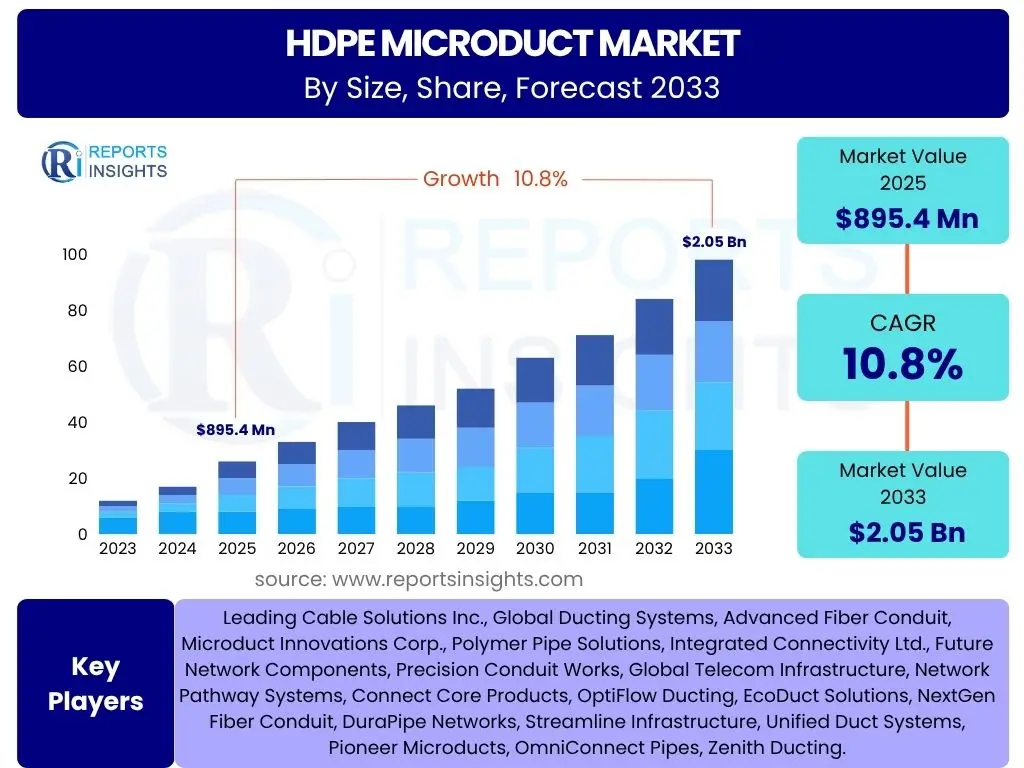

HDPE Microduct Market Size

According to Reports Insights Consulting Pvt Ltd, The HDPE Microduct Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. This robust growth is primarily driven by the escalating global demand for high-speed internet connectivity, particularly propelled by the widespread deployment of 5G networks and Fiber-to-the-Home (FTTH) initiatives. The inherent advantages of HDPE microducts, such as flexibility, ease of installation, and cost-effectiveness for fiber optic cable deployment, position them as critical infrastructure components in the ongoing digital transformation.

The market is estimated at USD 895.4 million in 2025 and is projected to reach USD 2.05 billion by the end of the forecast period in 2033. This significant expansion underscores the vital role of microduct technology in laying the groundwork for future communication networks. Factors such as urban densification, the proliferation of smart city projects, and the increasing reliance on data centers further contribute to this growth trajectory, necessitating efficient and scalable cable infrastructure solutions that HDPE microducts readily provide.

Key HDPE Microduct Market Trends & Insights

Analysis of prevalent user inquiries regarding the HDPE Microduct market reveals a strong interest in the underlying technological shifts and application expansions driving market evolution. Users frequently seek information on how emerging technologies influence microduct adoption, the most impactful deployment scenarios, and geographical disparities in market development. The market is increasingly characterized by innovations aimed at enhancing installation efficiency, improving product durability, and expanding the range of applications beyond traditional telecommunications infrastructure. This includes a growing focus on sustainable manufacturing practices and the development of specialized microduct solutions tailored for specific environmental conditions or demanding industrial applications.

A significant trend highlighted by user questions is the convergence of various digital infrastructure projects, where microducts serve as a foundational element. This includes not only the well-known FTTH and 5G rollouts but also smart city initiatives, intelligent transportation systems, and the expansion of edge computing facilities. There is also a keen interest in the adoption of automated or semi-automated installation techniques, which reduce deployment times and costs, thereby accelerating market penetration. Furthermore, the market is witnessing a shift towards higher fiber count cables within smaller diameter microducts, reflecting the increasing demand for greater bandwidth capacity in confined spaces. This optimization of space and capacity is a key driver for future product development and market strategy.

- Increasing adoption of Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB) deployments globally.

- Rapid expansion of 5G network infrastructure necessitating efficient fiber optic cable pathways.

- Growing demand for robust and flexible conduit solutions in smart city projects and IoT ecosystems.

- Technological advancements in microduct materials and manufacturing processes enhancing durability and installation ease.

- Emphasis on sustainable and environmentally friendly microduct solutions.

AI Impact Analysis on HDPE Microduct

Common user questions related to the impact of Artificial Intelligence (AI) on the HDPE Microduct domain primarily revolve around optimizing network deployment, predictive maintenance, and enhancing operational efficiencies. Users are keen to understand how AI can streamline the complex processes involved in laying extensive fiber optic networks, minimize errors, and forecast potential infrastructure issues before they arise. There is a general expectation that AI will bring about a new era of 'smart infrastructure' management, moving beyond reactive maintenance to proactive, data-driven strategies for network reliability and performance.

The integration of AI algorithms into network planning and management systems is anticipated to revolutionize the deployment and lifecycle management of HDPE microduct networks. AI can analyze vast datasets concerning terrain, existing infrastructure, weather patterns, and population density to recommend optimal routing for microduct installations, thereby reducing material waste and labor costs. Furthermore, AI-powered predictive analytics can monitor the health of deployed microducts and the fiber cables within them, identifying subtle changes that could indicate impending faults due to environmental stress, physical damage, or material degradation. This capability significantly enhances network uptime and reduces the need for costly manual inspections and repairs. The ability of AI to optimize resource allocation, automate certain monitoring tasks, and provide actionable insights is expected to drive greater efficiency and resilience across the entire microduct value chain.

- AI-driven optimization of microduct routing and network planning, minimizing deployment costs and time.

- Predictive maintenance analytics for microduct integrity, enhancing network reliability and reducing downtime.

- Automated monitoring of fiber optic performance within microducts, ensuring proactive issue resolution.

- Improved supply chain and inventory management for microduct components through AI-driven forecasting.

- Enhanced quality control during microduct manufacturing and installation via AI-powered vision systems.

Key Takeaways HDPE Microduct Market Size & Forecast

User inquiries concerning the key takeaways from the HDPE Microduct market size and forecast consistently highlight the market's high growth potential and its foundational role in global digital transformation. There is a clear interest in understanding the primary drivers behind the significant CAGR and how this growth translates into investment opportunities across various geographies. The insights sought often focus on identifying the most lucrative segments and the overarching market forces that will sustain this upward trajectory through the forecast period, emphasizing the long-term viability and strategic importance of microduct technology in modern communication infrastructure.

The primary takeaway is the indispensable nature of HDPE microducts in enabling the rapid and efficient deployment of next-generation communication networks, particularly 5G and FTTH. The substantial projected market size by 2033 signifies sustained investment in digital infrastructure globally. The market's resilience and growth are further bolstered by the increasing data consumption patterns, which necessitate robust and scalable fiber optic backbone networks. Furthermore, the market's trajectory indicates a shift towards more advanced, durable, and easily deployable microduct solutions, emphasizing innovation as a critical component for market leadership and continued expansion.

- Significant and sustained market growth driven by global digital infrastructure investments.

- Essential role of HDPE microducts in enabling widespread 5G and FTTH deployments.

- Increasing demand for robust, flexible, and scalable fiber optic conduit solutions.

- Strong market momentum across diverse applications including telecom, smart cities, and data centers.

- Innovation in materials and installation techniques as key enablers for future market expansion.

HDPE Microduct Market Drivers Analysis

The growth of the HDPE Microduct Market is primarily fueled by a confluence of macroeconomic and technological factors, predominantly the surging global demand for high-speed internet connectivity. The widespread commitment of governments and private entities to establish ubiquitous broadband access, particularly through Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB) initiatives, serves as a fundamental driver. These deployments inherently require robust, flexible, and scalable conduit solutions, for which HDPE microducts are optimally suited due to their ease of installation, protective qualities for delicate fiber optic cables, and cost-efficiency in large-scale rollouts.

Another pivotal driver is the unprecedented global rollout of 5G networks. 5G technology, with its promise of ultra-low latency and high bandwidth, necessitates a vastly denser fiber optic infrastructure compared to previous generations. This densification requires efficient and compact cabling solutions to connect numerous small cells and base stations, making HDPE microducts an ideal choice for last-mile connectivity and backhaul networks. Furthermore, the rapid expansion of data centers and cloud computing infrastructure worldwide contributes significantly, as these facilities require high-capacity fiber interconnections, often utilizing microducts for organized and future-proof cable management within and between facilities. The continuous evolution of smart city projects, integrating IoT devices and advanced communication systems, also generates substantial demand for underground cabling solutions that can be installed with minimal disruption, where microducts offer a distinct advantage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollout | +3.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Increasing Fiber-to-the-Home (FTTH) Deployments | +3.0% | Europe, Asia Pacific, Latin America | 2025-2033 |

| Growth in Data Centers & Cloud Infrastructure | +2.0% | North America, Europe, Asia Pacific | 2025-2030 |

| Smart City & IoT Infrastructure Development | +1.5% | Global, particularly developed economies | 2025-2033 |

HDPE Microduct Market Restraints Analysis

Despite the robust growth prospects, the HDPE Microduct Market faces several restraining factors that could impede its accelerated expansion. A primary restraint is the significant initial investment required for establishing comprehensive microduct networks. While the long-term benefits in terms of ease of maintenance and future-proofing are evident, the upfront capital expenditure for materials, specialized equipment, and skilled labor can be substantial, particularly for smaller service providers or projects in developing regions. This high initial cost can deter immediate adoption, especially where budget constraints are stringent or where traditional, less expensive (though less efficient) conduit solutions are perceived as sufficient.

Another significant restraint involves the complexities associated with regulatory hurdles and obtaining permits for new infrastructure deployments. Laying underground infrastructure often requires navigating a labyrinth of local, regional, and national regulations, including environmental impact assessments, right-of-way agreements, and construction permits. Delays in acquiring these necessary approvals can significantly prolong project timelines and escalate costs, thereby slowing down the pace of microduct adoption. Furthermore, the availability of alternative ducting solutions, such as traditional PVC or concrete conduits, which are often more familiar to installers and cheaper in the short term, presents a competitive challenge. While microducts offer superior long-term advantages for fiber deployment, the entrenched use of conventional methods in some markets acts as a barrier to wider penetration. Lastly, a shortage of highly skilled technicians specifically trained in the installation and maintenance of microduct systems, particularly in emerging markets, can pose a bottleneck, impacting deployment efficiency and quality.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -1.2% | Global, particularly emerging markets | 2025-2030 |

| Regulatory Hurdles & Permitting Delays | -1.0% | Europe, North America, Specific Asian countries | 2025-2033 |

| Competition from Alternative Ducting Solutions | -0.8% | Global, especially mature markets | 2025-2028 |

HDPE Microduct Market Opportunities Analysis

The HDPE Microduct Market is characterized by several significant opportunities that are poised to accelerate its growth trajectory. One of the most prominent opportunities lies in the expansion into rural and underserved areas globally. Governments and telecommunication companies are increasingly focusing on bridging the digital divide by extending high-speed internet access to remote communities. Microduct technology offers an efficient and cost-effective solution for these challenging deployments, as it allows for quicker installation with minimal ground disturbance, making it ideal for rural infrastructure projects where traditional trenching might be impractical or too expensive.

Another compelling opportunity emerges from the ongoing innovation in product development, including specialized microducts designed for niche applications. This includes the creation of microducts with enhanced fire retardancy for indoor applications, improved resistance to extreme temperatures or chemicals for industrial environments, or integrated features like pull ropes or detection wires for easier installation and maintenance. The development of hybrid microduct systems, combining different duct sizes or types within a single jacket, also presents an opportunity for optimized cable management. Furthermore, the increasing integration of IoT devices and smart infrastructure components in various sectors, such as transportation, utilities, and public safety, creates a burgeoning demand for compact and reliable fiber optic pathways. HDPE microducts are perfectly suited to support this proliferation of connected devices, offering a flexible and scalable solution for future smart ecosystems. Lastly, emerging economies, particularly in Southeast Asia, Africa, and parts of Latin America, represent untapped markets with significant potential for growth as they embark on large-scale digital infrastructure upgrades.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Rural & Underserved Areas | +1.8% | Global, particularly emerging and developing regions | 2025-2033 |

| Development of Specialized & Hybrid Microducts | +1.5% | North America, Europe, Asia Pacific | 2025-2030 |

| Integration with IoT & Smart Infrastructure Projects | +1.3% | Global, particularly developed economies | 2025-2033 |

HDPE Microduct Market Challenges Impact Analysis

The HDPE Microduct Market faces a unique set of challenges that require strategic navigation to sustain its rapid growth. One significant challenge pertains to the complexity of ensuring durability and longevity in diverse environmental conditions. While HDPE is known for its resilience, factors such as extreme temperature fluctuations, soil acidity, rodent damage, and unforeseen ground movements can impact the long-term integrity of buried microducts. This necessitates rigorous material testing and installation standards to prevent premature failure, which could lead to costly repairs and network disruptions. Maintaining consistent quality across various manufacturers and ensuring adherence to industry best practices during installation remain critical hurdles to widespread, reliable deployment.

Another notable challenge is the intense competition from traditional cabling methods and alternative conduit materials. While microducts offer distinct advantages for fiber optic deployment, incumbent infrastructure and established installation practices often favor older, more familiar technologies. Overcoming this inertia requires continuous education on the long-term benefits and cost efficiencies of microducts, alongside efforts to standardize installation procedures and equipment. Furthermore, global supply chain disruptions, as experienced in recent years, can significantly impact the availability of raw materials (HDPE resin) and finished products, leading to price volatility and project delays. This underscores the need for robust supply chain management and diversified sourcing strategies. Lastly, the industry grapples with the need for ongoing innovation to meet evolving network demands, such as higher fiber densities and novel deployment scenarios, requiring significant R&D investment and agile product development cycles to stay ahead of technological shifts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Durability & Longevity in Diverse Environments | -0.9% | Global | 2025-2033 |

| Competition from Traditional Cabling Methods | -0.7% | Global, especially mature markets | 2025-2030 |

| Supply Chain Volatility & Raw Material Costs | -0.6% | Global | 2025-2027 |

HDPE Microduct Market - Updated Report Scope

This report offers a comprehensive analysis of the HDPE Microduct Market, providing detailed insights into its current landscape, future growth trajectories, and influential market dynamics. It encompasses an exhaustive examination of market size estimations, historical trends, and future projections across various segments and key geographical regions. The scope meticulously covers the drivers, restraints, opportunities, and challenges shaping the market, alongside a thorough assessment of the competitive environment and the strategic initiatives undertaken by leading market participants to maintain or gain market share. The report aims to furnish stakeholders with actionable intelligence to make informed business decisions and capitalize on emerging market trends and opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 895.4 Million |

| Market Forecast in 2033 | USD 2.05 Billion |

| Growth Rate | 10.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Cable Solutions Inc., Global Ducting Systems, Advanced Fiber Conduit, Microduct Innovations Corp., Polymer Pipe Solutions, Integrated Connectivity Ltd., Future Network Components, Precision Conduit Works, Global Telecom Infrastructure, Network Pathway Systems, Connect Core Products, OptiFlow Ducting, EcoDuct Solutions, NextGen Fiber Conduit, DuraPipe Networks, Streamline Infrastructure, Unified Duct Systems, Pioneer Microducts, OmniConnect Pipes, Zenith Ducting. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The HDPE Microduct market is extensively segmented to provide a granular view of its diverse applications and product types, facilitating a comprehensive understanding of market dynamics. This segmentation aids in identifying key growth areas, pinpointing market opportunities, and analyzing competitive landscapes across various dimensions. The market can be broadly categorized by product type, diameter, application, and end-use industry, each reflecting specific technological requirements and market demands.

Understanding these segments is crucial for stakeholders to tailor their strategies and product offerings. For instance, the distinction between single, multiple, and hybrid microducts reflects varying capacities and deployment methodologies, catering to different network architectures. Diameter segmentation is vital for compatibility with different fiber cable counts and installation techniques. Application-based segmentation highlights the primary sectors driving demand, from massive FTTH rollouts to niche smart grid communications, while end-use industry segmentation provides insight into the diverse sectors leveraging microduct technology beyond traditional telecom, indicating potential for market diversification and expansion into industrial and utility infrastructure.

- By Type:

- Single Microduct: Used for individual fiber optic cable protection and easy expansion.

- Multiple Microduct (Bundled Microducts): Consists of several smaller microducts bundled together within a common outer sheath, ideal for high-density fiber deployments.

- Hybrid Microduct: Combines different types or sizes of ducts within one jacket, offering versatile network solutions.

- Specialized Microducts: Engineered for specific performance needs, such as fire retardancy, UV resistance, or enhanced crush resistance.

- By Diameter:

- 7mm - 12mm: Primarily for last-mile and compact installations.

- 12mm - 18mm: Standard sizes for various fiber deployments.

- 18mm - 24mm: For higher fiber counts and main distribution lines.

- Above 24mm: Used for trunk lines and large-scale infrastructure.

- By Application:

- Fiber-to-the-Home (FTTH): Dominant application driving residential broadband connectivity.

- 5G Network Infrastructure: Critical for connecting 5G small cells and base stations.

- Data Center Interconnect (DCI): Facilitates high-speed data transfer between data centers.

- Enterprise Networks: Supports internal network infrastructure for businesses.

- Smart Grid Communications: For robust and reliable communication in power grids.

- Intelligent Transportation Systems (ITS): Used in traffic management and connected vehicle infrastructure.

- CATV Networks: For cable television and broadband services.

- Other Telecommunication Networks: Includes metro, long-haul, and specialized networks.

- By End-Use Industry:

- Telecommunication & Broadband: Core consumer of microducts for network expansion.

- Utilities (Power, Water): For internal communication and smart metering infrastructure.

- Oil & Gas: For remote monitoring and control systems in harsh environments.

- Transportation (Rail, Road): Supports communication and signaling systems.

- Commercial & Residential: For building internal wiring and multi-dwelling unit connectivity.

- Others (e.g., Mining, Industrial): Niche applications requiring robust and secure fiber pathways.

Regional Highlights

- North America: This region demonstrates strong market growth driven by significant investments in 5G infrastructure deployment and ongoing efforts to expand Fiber-to-the-Home (FTTH) connectivity, particularly in rural and underserved areas. The presence of major telecommunication providers and a robust technological ecosystem contribute to sustained demand for HDPE microducts. The U.S. and Canada are actively upgrading their broadband networks, which fuels the adoption of efficient fiber deployment solutions.

- Europe: Europe is experiencing substantial growth in the HDPE Microduct market, primarily due to ambitious national and EU-led initiatives aimed at achieving ubiquitous gigabit connectivity. Countries like Germany, France, and the UK are heavily investing in FTTH rollouts, alongside modernization of existing telecommunication infrastructures. Regulatory support and the drive for digital transformation across various sectors also contribute significantly to market expansion in this region.

- Asia Pacific (APAC): APAC stands as the largest and fastest-growing market for HDPE Microducts, propelled by massive 5G network rollouts, rapid urbanization, and extensive FTTH deployments, especially in China, India, Japan, and South Korea. The region's dense populations and increasing data consumption necessitate scalable and efficient fiber optic infrastructure, making microducts a preferred choice. Government initiatives to enhance digital connectivity and the proliferation of smart cities are key drivers.

- Latin America: The market in Latin America is witnessing moderate but steady growth, driven by increasing internet penetration rates and government programs aimed at improving digital infrastructure. Countries like Brazil, Mexico, and Argentina are investing in FTTH deployments to meet rising broadband demand. The region presents significant untapped potential as telecommunication networks continue to expand and modernize.

- Middle East and Africa (MEA): The MEA region is emerging as a promising market, driven by substantial infrastructure development projects, including smart city initiatives (e.g., Neom in Saudi Arabia) and efforts to diversify economies away from oil. Investments in fiber optic networks and 5G deployments are on the rise, particularly in countries like UAE, Saudi Arabia, and South Africa, leading to increased demand for HDPE microducts for robust and future-proof connectivity solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the HDPE Microduct Market.- Global Ducting Systems

- Advanced Fiber Conduit Solutions

- Precision Cable Pathways Inc.

- Microduct Innovations Global

- Polymer Pipe Networks Ltd.

- Integrated Connectivity Solutions

- Future Network Components Corp.

- OptiFlow Ducting Systems

- EcoDuct Materials

- NextGen Fiber Conduit

- DuraPipe Networks International

- Streamline Infrastructure Products

- Unified Duct Systems

- Pioneer Microduct Technology

- OmniConnect Pipes

- Zenith Ducting & Solutions

- Continental Ducting Supplies

- Nordic Fiber Pathway Systems

- Asia Pacific Microduct Co.

- African Telecom Ducts

Frequently Asked Questions

What are HDPE microducts primarily used for?

HDPE (High-Density Polyethylene) microducts are primarily used as protective pathways for fiber optic cables in telecommunication networks. They facilitate the blowing, pulling, or pushing of fiber optic cables over long distances, offering flexibility, ease of installation, and protection against environmental factors and physical damage.

What are the main benefits of using HDPE microducts over traditional conduits?

The primary benefits of HDPE microducts include significantly faster and more cost-effective installation (especially for fiber blowing), superior protection for delicate fiber optic cables, future-proofing network infrastructure by allowing for easy upgrades or additional fiber deployments, and reduced environmental impact due to smaller trenching requirements.

How does the 5G rollout impact the demand for HDPE microducts?

The global 5G rollout significantly boosts the demand for HDPE microducts. 5G networks require a much denser fiber optic infrastructure to connect numerous small cells and base stations. Microducts provide an efficient, scalable, and cost-effective solution for deploying the vast amount of fiber needed for 5G backhaul and front-haul networks, ensuring high bandwidth and low latency connectivity.

Which regions are leading the growth in the HDPE Microduct market?

The Asia Pacific (APAC) region, particularly countries like China, India, and South Korea, is leading the growth in the HDPE Microduct market due to extensive 5G deployments, widespread Fiber-to-the-Home (FTTH) initiatives, and rapid urbanization. Europe and North America also show strong growth driven by significant investments in modernizing their broadband infrastructures and expanding fiber access.

What innovations are shaping the future of HDPE microduct technology?

Future innovations in HDPE microduct technology are focusing on developing specialized microducts with enhanced properties (e.g., fire retardancy, improved crush resistance), integration with smart infrastructure (IoT, AI for network planning), and more sustainable manufacturing processes. Efforts are also being made to simplify installation further and increase the density of fibers that can be housed within compact duct systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted