Microduct Market

Microduct Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704557 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

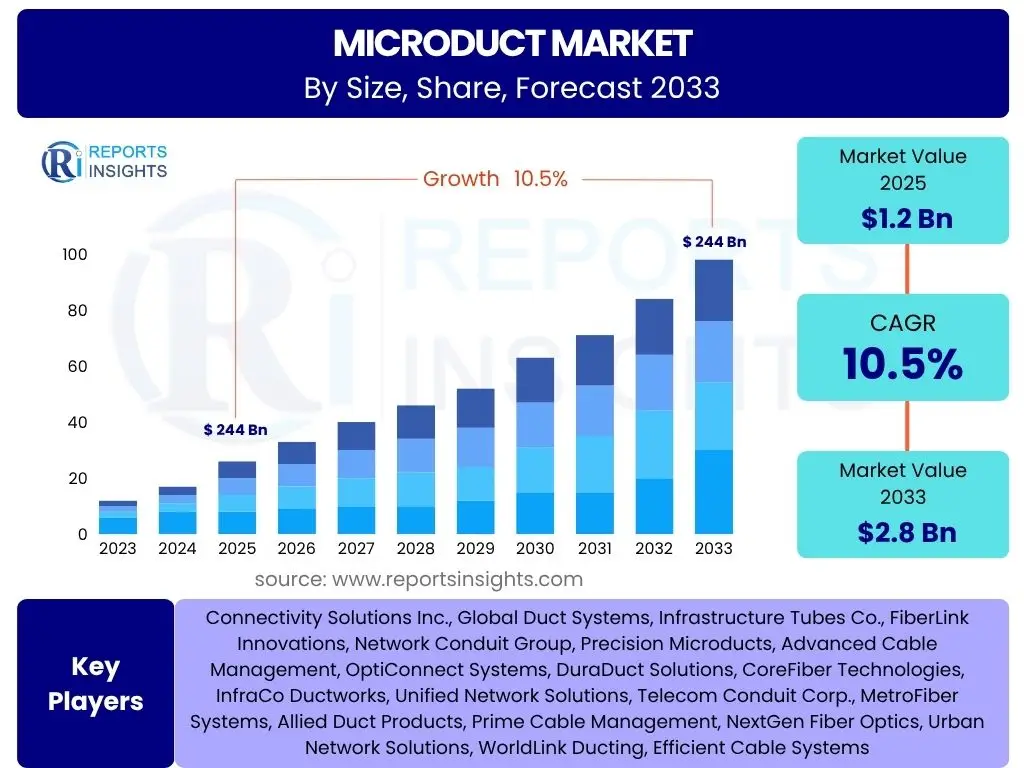

Microduct Market Size

According to Reports Insights Consulting Pvt Ltd, The Microduct Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating global demand for high-speed internet connectivity, the aggressive rollout of 5G infrastructure, and the expansion of fiber optic networks deeper into residential and commercial areas. The inherent advantages of microduct systems, such as their flexibility, cost-effectiveness, and ease of installation for future upgrades, are significant contributors to their increasing adoption across diverse regions.

Key Microduct Market Trends & Insights

User inquiries frequently highlight the dynamic shifts within the Microduct market, focusing on technological advancements, evolving application areas, and sustainability considerations. Common questions include the impact of urbanization on network density, the integration of smart city initiatives, and the drive towards more environmentally friendly materials and installation methods. Furthermore, there is a strong interest in understanding how microducts facilitate the rapid deployment of next-generation communication networks and enhance the scalability of existing infrastructure. The market is witnessing a convergence of demand for high performance, ease of deployment, and long-term cost efficiency.

- Miniaturization and Higher Density: A growing trend towards smaller diameter microducts that allow for higher fiber count within existing conduits, optimizing space and reducing civil works.

- Sustainable Materials and Practices: Increasing adoption of eco-friendly and recyclable materials, along with installation methods that minimize environmental impact and energy consumption.

- 5G and Edge Computing Integration: Microducts are becoming essential for deploying fiber backhaul to 5G small cells and edge data centers, facilitating ultra-low latency and high bandwidth.

- Pre-bundled Microduct Solutions: Manufacturers are offering pre-installed fiber within microducts, simplifying installation and reducing on-site labor requirements.

- Smart City Infrastructure Development: Integral role in connecting various smart city components, including IoT sensors, surveillance cameras, and intelligent traffic systems, demanding reliable and scalable fiber networks.

AI Impact Analysis on Microduct

User queries regarding artificial intelligence in the Microduct domain often revolve around optimizing network planning, predicting maintenance needs, and streamlining installation processes. There is keen interest in how AI can enhance efficiency, reduce operational costs, and improve the overall reliability of fiber optic deployments utilizing microduct systems. Users are also exploring AI's role in data analysis from network performance, predictive analytics for infrastructure longevity, and automated decision-making for capacity management. The integration of AI is expected to lead to more intelligent and resilient fiber networks, where microducts serve as the fundamental physical backbone.

- Optimized Network Planning: AI algorithms can analyze geographic data, population density, and existing infrastructure to optimize microduct routing and placement, minimizing deployment costs and time.

- Predictive Maintenance: AI can monitor network performance and predict potential faults or degradation in microduct-housed fiber, enabling proactive maintenance and reducing downtime.

- Automated Quality Control: AI-powered vision systems can inspect microduct integrity during manufacturing and installation, ensuring higher quality standards and reducing errors.

- Resource Allocation and Logistics: AI can optimize the logistics of microduct delivery and the allocation of installation teams, improving project efficiency and reducing waste.

- Enhanced Security and Monitoring: AI can integrate with network monitoring systems to detect anomalies or unauthorized access to fiber infrastructure, improving the security of microduct-protected cables.

Key Takeaways Microduct Market Size & Forecast

Common user questions regarding key takeaways from the Microduct market size and forecast focus on identifying the most lucrative growth segments, understanding the primary drivers propelling market expansion, and assessing the long-term investment potential. There is a strong emphasis on understanding how the projected growth translates into opportunities for different stakeholders, from manufacturers to service providers and network operators. Users are keen to identify regions poised for significant growth and the specific applications that will drive the highest demand. The overall sentiment points towards a market characterized by sustained expansion, driven by foundational shifts in global communication infrastructure needs.

- Significant Market Expansion: The market is poised for substantial growth, driven by an insatiable demand for bandwidth and expanding digital infrastructure.

- Fiber Optic Deployment Catalyst: Microducts are critical enablers for the widespread and efficient deployment of fiber optic networks globally, including FTTH and 5G backhaul.

- Cost-Efficiency and Scalability: Their ability to reduce installation costs, simplify future upgrades, and provide high scalability makes them a preferred choice for network planners.

- Regional Growth Disparities: While global growth is strong, specific regions like Asia Pacific and North America are expected to lead in adoption due to aggressive infrastructure investments.

- Innovation in Materials and Design: Ongoing innovation in microduct materials and designs will further enhance performance, durability, and ease of installation, sustaining market momentum.

Microduct Market Drivers Analysis

The Microduct market is experiencing robust growth driven by several interconnected factors primarily centered around the global expansion of digital infrastructure. The increasing demand for high-speed internet connectivity, fueled by data-intensive applications and the proliferation of connected devices, necessitates extensive fiber optic deployment, for which microducts offer an efficient and scalable solution. Furthermore, the global push towards 5G network rollout, which relies heavily on dense fiber backhaul, significantly contributes to market acceleration. Urbanization trends and smart city initiatives also create a strong demand for reliable and flexible communication infrastructure, with microducts playing a pivotal role in these complex networks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| 5G Network Expansion | +2.5% | Global, particularly North America, APAC (China, South Korea), Europe | Short to Medium-Term (2025-2030) |

| Fiber-to-the-Home/Building (FTTH/B) Deployment | +2.0% | Europe, North America, APAC (India, Southeast Asia), Latin America | Medium to Long-Term (2025-2033) |

| Growth in Data Centers & Cloud Infrastructure | +1.5% | Global, with high concentration in key economic hubs (USA, Ireland, Singapore) | Medium to Long-Term (2025-2033) |

| Smart City Initiatives & IoT Proliferation | +1.0% | Major urban centers globally, particularly in developed and rapidly developing economies | Medium to Long-Term (2026-2033) |

| Government Initiatives & Digital Inclusion Programs | +1.0% | Rural areas and underserved regions globally, notable in EU, India, US | Medium to Long-Term (2025-2033) |

Microduct Market Restraints Analysis

Despite significant growth drivers, the Microduct market faces certain restraints that could temper its expansion. High initial investment costs associated with new fiber optic infrastructure, including the purchase and installation of microduct systems, can be a deterrent for smaller service providers or projects with limited budgets. Regulatory hurdles and the complexity of obtaining permits for underground installations in densely populated urban areas can also slow down deployment timelines and increase project costs. Furthermore, the inherent competition from alternative wireless technologies, while not entirely substitutable, can impact the perceived urgency or necessity of extensive wired infrastructure. Lastly, the requirement for specialized installation equipment and skilled labor presents a bottleneck in some regions, limiting the pace of adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Capital Expenditure | -1.2% | Developing Economies, Greenfield Projects | Short to Medium-Term (2025-2030) |

| Complex Regulatory Frameworks & Permitting | -0.8% | Densely Populated Urban Areas (Europe, North America) | Medium-Term (2025-2030) |

| Competition from Wireless Technologies (e.g., Fixed Wireless Access) | -0.5% | Rural Areas, Areas with existing strong wireless infrastructure | Medium to Long-Term (2026-2033) |

| Shortage of Skilled Installation Labor | -0.3% | Global, particularly pronounced in rapidly expanding markets | Medium-Term (2025-2030) |

Microduct Market Opportunities Analysis

The Microduct market is poised to capitalize on several significant opportunities driven by evolving technological landscapes and global infrastructure priorities. The widespread initiatives for rural broadband expansion across various countries present a substantial untapped market, where microducts offer an efficient solution for bringing fiber connectivity to remote areas. The growing emphasis on green infrastructure and sustainable development also provides an opportunity for manufacturers to innovate with eco-friendly materials and methods, aligning with global environmental goals. Furthermore, the emergence of new applications in industrial settings, smart grid deployment, and the increasing demand for future-proof, scalable network solutions underscore promising avenues for market growth. Specialized microduct designs for harsh environments or specific niche applications can also unlock new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rural Broadband & Digital Divide Initiatives | +1.8% | Global, particularly North America, Europe, parts of APAC, Latin America | Medium to Long-Term (2025-2033) |

| Green Infrastructure & Sustainable Development Goals | +1.5% | Europe, North America, environmentally conscious regions globally | Medium to Long-Term (2026-2033) |

| Emerging Market Penetration (Africa, Latin America) | +1.0% | Sub-Saharan Africa, South America, parts of Southeast Asia | Long-Term (2027-2033) |

| Specialty & Niche Applications (e.g., industrial, smart grid) | +0.7% | Developed industrial economies, energy sectors | Medium to Long-Term (2025-2033) |

Microduct Market Challenges Impact Analysis

The Microduct market, while expanding, navigates distinct challenges that require strategic responses from industry players. Volatility in raw material costs, particularly for polymers like HDPE, can impact manufacturing expenses and subsequently influence product pricing and profit margins. The inherent complexity of installation, especially in brownfield projects or congested urban environments, demands specialized techniques and can lead to higher labor costs and potential project delays. Environmental concerns, such as the disposal of plastic materials and the impact of trenching on local ecosystems, necessitate the adoption of more sustainable practices and materials. Furthermore, potential supply chain disruptions, stemming from geopolitical events or global crises, can affect the availability and timely delivery of microduct products, posing significant operational hurdles for network deployment projects.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.9% | Global, impacts all manufacturing regions | Short to Medium-Term (2025-2028) |

| Installation Complexity & Associated Labor Costs | -0.7% | Densely Populated Areas, Brownfield Projects | Medium-Term (2025-2030) |

| Environmental Regulations & Sustainability Pressure | -0.5% | Europe, North America, environmentally conscious countries | Medium to Long-Term (2026-2033) |

| Supply Chain Disruptions | -0.4% | Global, particularly areas reliant on specific manufacturing hubs | Short-Term (2025-2027) |

Microduct Market - Updated Report Scope

This report provides an in-depth analysis of the global Microduct Market, offering a comprehensive understanding of its current dynamics, historical performance, and future growth projections. It delineates market size estimations, identifies key market trends, analyzes the impact of drivers, restraints, opportunities, and challenges, and provides a detailed segmentation analysis. The report also highlights regional dynamics and profiles leading market players, offering a holistic view for strategic decision-making. The scope covers the market from a technological, application, and geographical perspective, providing actionable insights for stakeholders across the value chain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.8 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Connectivity Solutions Inc., Global Duct Systems, Infrastructure Tubes Co., FiberLink Innovations, Network Conduit Group, Precision Microducts, Advanced Cable Management, OptiConnect Systems, DuraDuct Solutions, CoreFiber Technologies, InfraCo Ductworks, Unified Network Solutions, Telecom Conduit Corp., MetroFiber Systems, Allied Duct Products, Prime Cable Management, NextGen Fiber Optics, Urban Network Solutions, WorldLink Ducting, Efficient Cable Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Microduct market is segmented to provide a detailed understanding of its diverse components and their respective contributions to overall market growth. This comprehensive segmentation allows for a granular analysis of market dynamics, identifying high-growth areas, and tailoring strategies to specific industry needs. The segmentation covers various dimensions, including the type of microduct, the materials used in their manufacturing, their specific diameter sizes, the diverse applications they serve, and the end-use industries that predominantly adopt these solutions. Each segment reflects unique demand drivers and market characteristics, providing a holistic view of the market landscape.

- By Type:

- Single Microduct: Individual tubes for single fiber installation.

- Multiple Microduct: Several microducts bundled together within a larger outer sheath.

- Bundle Microduct: Compact bundles of smaller microducts, designed for higher density deployments.

- By Material:

- High-Density Polyethylene (HDPE): Dominant material due to its flexibility, durability, and cost-effectiveness.

- Polyvinyl Chloride (PVC): Used for specific applications where its properties are advantageous.

- Others: Includes materials like polypropylene and specialized composites for niche requirements.

- By Diameter:

- Micro (up to 7mm): Suited for high-density, small-footprint installations.

- Small (7-12mm): Common for last-mile and premise connectivity.

- Medium (12-20mm): Versatile for various network extensions.

- Large (>20mm): Used for backbone infrastructure and high-capacity routes.

- By Application:

- Fiber-to-the-Home (FTTH): Primary application for residential broadband.

- 5G Backhaul: Critical for connecting 5G small cells and towers to core networks.

- Data Centers & Enterprise Connectivity: For high-speed internal and external fiber links.

- Smart City Infrastructure: Integrating various urban services with fiber optics.

- Industrial & Commercial Applications: For robust and scalable industrial communication networks.

- Rural Broadband: Extending high-speed internet to underserved areas.

- By End-Use Industry:

- Telecommunications: Largest segment, driven by network expansion and upgrades.

- Utilities (Power, Water): For smart grid applications and infrastructure monitoring.

- Transportation: For traffic management systems, railways, and airport connectivity.

- Commercial & Residential: For new builds and retrofits requiring advanced connectivity.

- Others: Including healthcare, education, and defense sectors.

Regional Highlights

- North America: Exhibits strong growth driven by aggressive 5G deployments, continued FTTH expansion, and significant investments in data center infrastructure. The United States and Canada are leading the adoption of advanced microduct solutions, focusing on efficiency and future-proofing.

- Europe: Characterized by robust FTTH rollout initiatives as countries strive to meet digital agenda targets. Governments and private entities are investing heavily in broadband infrastructure, with a particular emphasis on sustainable and efficient deployment methods, favoring microduct solutions.

- Asia Pacific (APAC): Represents the largest and fastest-growing market due to massive telecommunications infrastructure development, particularly in countries like China, India, Japan, and South Korea. Rapid urbanization, smart city projects, and the sheer scale of population requiring connectivity are key drivers.

- Latin America: Experiencing increasing adoption of microducts as countries focus on bridging the digital divide and improving internet penetration. Brazil, Mexico, and Argentina are key markets, with rising investments in fiber optic networks and rural broadband initiatives.

- Middle East and Africa (MEA): Shows significant potential for growth, primarily driven by expanding telecom networks, smart city mega-projects (e.g., in UAE, Saudi Arabia), and increasing digital transformation efforts across the region. Demand for reliable and scalable fiber infrastructure is accelerating.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Microduct Market.- Connectivity Solutions Inc.

- Global Duct Systems

- Infrastructure Tubes Co.

- FiberLink Innovations

- Network Conduit Group

- Precision Microducts

- Advanced Cable Management

- OptiConnect Systems

- DuraDuct Solutions

- CoreFiber Technologies

- InfraCo Ductworks

- Unified Network Solutions

- Telecom Conduit Corp.

- MetroFiber Systems

- Allied Duct Products

- Prime Cable Management

- NextGen Fiber Optics

- Urban Network Solutions

- WorldLink Ducting

- Efficient Cable Systems

Frequently Asked Questions

Analyze common user questions about the Microduct market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Microduct and how is it used in fiber optic networks?

A microduct is a small-diameter, flexible tube, typically made of high-density polyethylene (HDPE), designed to protect and facilitate the installation of fiber optic cables. It is primarily used to create pathways for blowing or pulling optical fibers, especially micro-cables, into existing or new conduit systems, enabling efficient network expansion and upgrades.

What are the primary benefits of using Microducts for fiber deployment?

Microducts offer several key benefits, including cost-effectiveness by reducing the need for extensive civil works, flexibility for future network upgrades or expansions by allowing new fibers to be blown into empty ducts, and enhanced cable protection against environmental factors and physical damage, leading to increased network reliability.

How do Microducts support 5G network expansion and smart city initiatives?

Microducts are crucial for 5G backhaul by providing the necessary fiber connectivity to small cells and distributed antenna systems due to their small footprint and ease of deployment in dense urban areas. For smart cities, they facilitate the widespread, flexible, and scalable fiber infrastructure required to connect IoT sensors, surveillance, and other intelligent urban systems.

What are the different types of Microducts available in the market?

Microducts come in various types, including single microducts for individual fiber installations, multiple microducts (several tubes within one outer sheath) for high-density deployments, and pre-installed fiber-in-duct solutions. They also vary by material (e.g., HDPE, PVC) and internal surface treatment (e.g., ribbed, smooth) to optimize blowing distances.

What is the typical lifespan of a Microduct system and its environmental impact?

A well-installed microduct system can have a lifespan of 20-30 years, matching the longevity of the fiber optic cables it protects, assuming proper material selection and installation. Environmentally, manufacturers are increasingly using recyclable materials and promoting trenchless installation methods to reduce carbon footprint and minimize ecological disruption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted