Powder Metallurgy Component Market

Powder Metallurgy Component Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702957 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

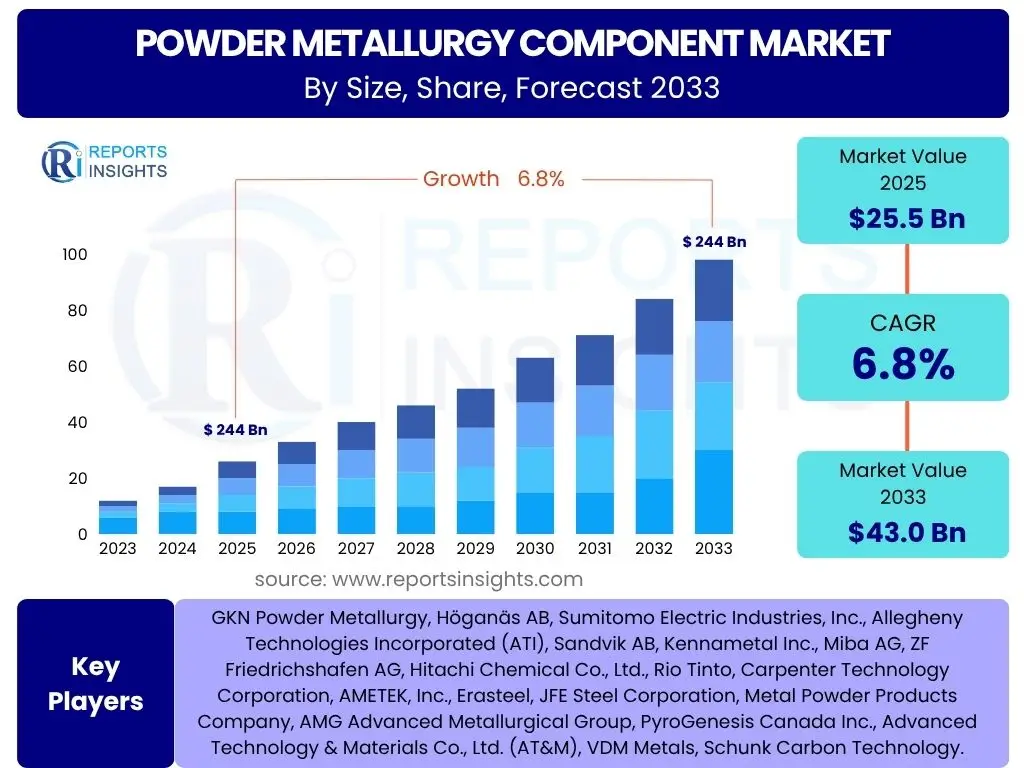

Powder Metallurgy Component Market Size

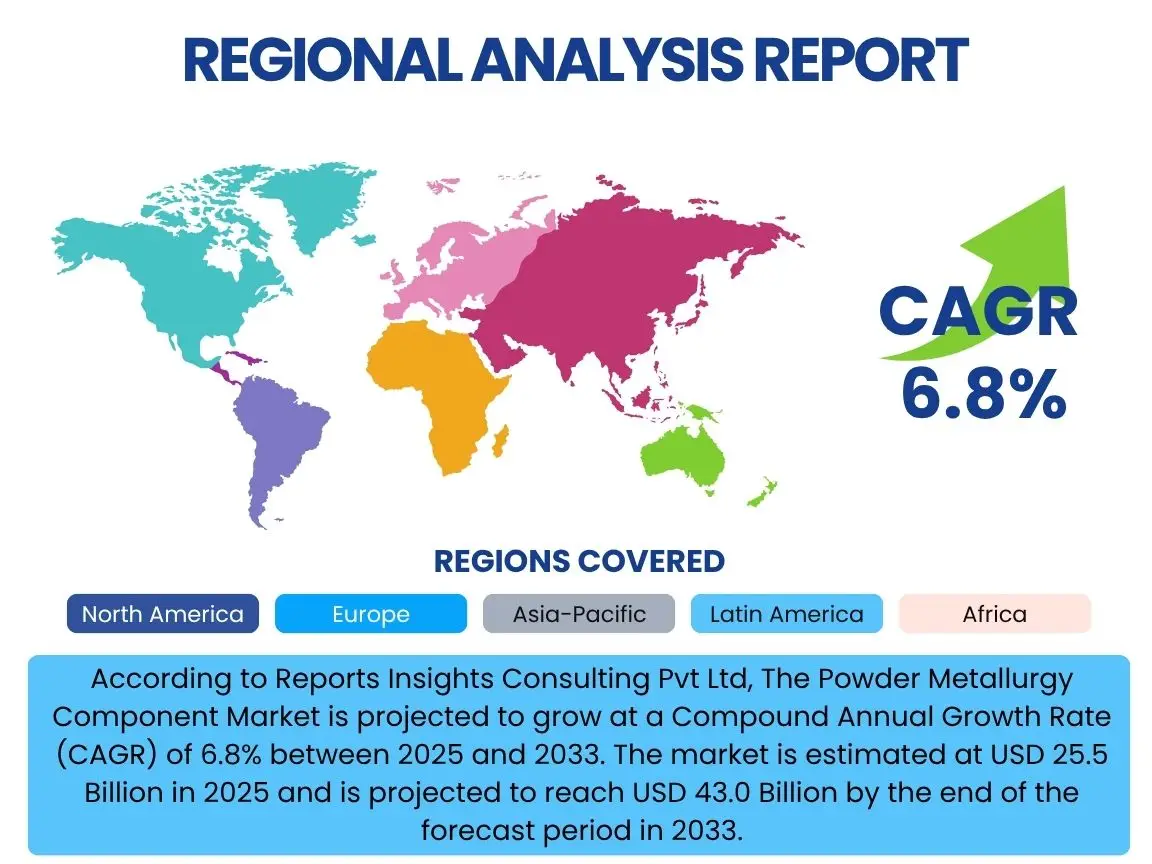

According to Reports Insights Consulting Pvt Ltd, The Powder Metallurgy Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 43.0 Billion by the end of the forecast period in 2033.

Key Powder Metallurgy Component Market Trends & Insights

The Powder Metallurgy Component market is currently experiencing dynamic shifts driven by advancements in material science, manufacturing processes, and increasing demand from key end-use industries. User inquiries frequently highlight a strong interest in understanding how lightweighting trends in the automotive sector, the expansion of electric vehicles (EVs), and the integration of advanced manufacturing techniques are shaping the market landscape. There is also significant curiosity regarding the adoption of new alloys and composite materials, which offer superior performance characteristics for specialized applications.

Furthermore, the market is witnessing a notable trend towards higher precision and complexity in component design, facilitated by innovations in Metal Injection Molding (MIM) and additive manufacturing (3D printing) processes. These technologies enable the production of intricate geometries with enhanced material properties, opening new avenues for application in medical, aerospace, and consumer electronics sectors. The drive for cost-efficiency and sustainability is also influencing material selection and process optimization, pushing manufacturers to explore more resource-efficient production methods and recyclable materials.

Another prominent insight from market analysis indicates a growing focus on automation and digitalization within powder metallurgy facilities. This includes the implementation of smart manufacturing principles, real-time quality control, and data analytics to optimize production yields and reduce defects. Such trends are critical for maintaining competitiveness and meeting the evolving performance demands of high-growth industries, ultimately contributing to the market's robust expansion.

- Growing demand for lightweight and high-performance components in automotive, aerospace, and medical sectors.

- Increasing adoption of Metal Injection Molding (MIM) and additive manufacturing (3D printing) for complex geometries.

- Development of new alloys and composite materials with enhanced properties.

- Emphasis on energy efficiency and sustainable manufacturing practices.

- Integration of automation, digitalization, and Industry 4.0 principles in production processes.

AI Impact Analysis on Powder Metallurgy Component

Common user questions related to the impact of Artificial Intelligence (AI) on the Powder Metallurgy Component sector revolve around its potential to revolutionize various stages of the manufacturing process, from material design to final product quality control. Users are keen to understand how AI can optimize powder formulations, predict material behavior during sintering, and enhance the overall efficiency and reliability of production lines. The overarching theme is the aspiration for a more intelligent, autonomous, and error-free manufacturing environment facilitated by AI-driven insights and automation.

AI's influence extends significantly to predictive maintenance and anomaly detection within powder metallurgy operations. By analyzing sensor data from machinery, AI algorithms can foresee equipment failures, schedule maintenance proactively, and minimize downtime, thereby improving operational continuity and reducing costs. Furthermore, AI is seen as a crucial tool for quality assurance, enabling real-time monitoring and analysis of component characteristics to identify and rectify defects much earlier in the production cycle, leading to higher product consistency and reduced waste.

The application of AI in the design and simulation phases is also a key area of interest. Generative design techniques, powered by AI, can explore a vast array of component designs, optimizing for specific performance criteria such as strength-to-weight ratio or thermal conductivity. This accelerated design cycle, coupled with AI-enhanced process parameter optimization, allows manufacturers to innovate faster, bring new products to market more quickly, and produce components with unprecedented precision and complexity.

- Optimization of powder formulation and material selection using AI algorithms.

- Predictive maintenance and anomaly detection for powder metallurgy equipment.

- Enhanced quality control through real-time defect detection and process monitoring.

- Accelerated component design and simulation via AI-driven generative design.

- Improved process parameter optimization for sintering and other manufacturing steps.

Key Takeaways Powder Metallurgy Component Market Size & Forecast

Analysis of common user questions concerning the Powder Metallurgy Component market size and forecast reveals a strong interest in the underlying drivers of growth, particularly within the automotive and industrial sectors. Users frequently inquire about the impact of electric vehicle adoption on PM demand and the ongoing shift towards lightweighting in transportation. The market is poised for significant expansion, driven by continuous technological advancements in materials and processes that enhance component performance and cost-effectiveness, making PM an increasingly attractive manufacturing solution across diverse applications.

A significant takeaway is the pivotal role of regional manufacturing hubs, especially in Asia Pacific, which are expected to contribute substantially to market expansion due to burgeoning industrialization and vehicle production. The forecast highlights a sustained demand for high-precision, intricate components, which powder metallurgy is uniquely positioned to deliver, especially through advanced techniques like Metal Injection Molding (MIM) and additive manufacturing. These capabilities allow for the creation of components that are difficult or impossible to produce with traditional methods, thus securing PM's future growth trajectory.

The market's resilience is also a key insight, demonstrating its ability to adapt to evolving industry standards and embrace innovation. Despite potential challenges such as raw material price volatility or initial investment costs, the long-term benefits of PM—including material efficiency, reduced machining, and complex part integration—underscore its value proposition. This positions the Powder Metallurgy Component market for consistent and robust growth through the forecast period, underpinned by its strategic importance in modern manufacturing paradigms.

- Robust growth projected, primarily driven by automotive and industrial sector demand.

- Technological advancements in PM processes and materials are key enablers.

- Asia Pacific is anticipated to remain a dominant and rapidly growing market.

- Increasing adoption of advanced PM techniques like MIM and 3D printing for complex components.

- Emphasis on lightweighting and performance optimization sustains market expansion.

Powder Metallurgy Component Market Drivers Analysis

The global Powder Metallurgy Component market is significantly propelled by the increasing demand for high-performance, lightweight, and complex components across various end-use industries. A primary driver is the automotive sector's continuous pursuit of improved fuel efficiency and reduced emissions, which necessitates the use of lighter and stronger materials. Powder metallurgy offers a cost-effective solution for producing intricate shapes with minimal material waste, making it an ideal choice for engine, transmission, and structural components in both traditional and electric vehicles.

Furthermore, the rapid advancements in material science and process technologies within powder metallurgy are expanding its applicability and market reach. Innovations in alloy development, such as new ferrous and non-ferrous compositions, allow for enhanced mechanical properties, including higher strength, better wear resistance, and improved corrosion resistance. These material breakthroughs, coupled with refined manufacturing processes like Metal Injection Molding (MIM) and additive manufacturing, enable the production of components with tighter tolerances and superior finishes, meeting the stringent requirements of high-tech applications in aerospace, medical, and electronics sectors.

The economic benefits associated with powder metallurgy also serve as a crucial driver. PM processes inherently reduce material waste through near-net-shape manufacturing, minimizing the need for extensive post-processing and machining. This efficiency translates into lower production costs, especially for high-volume manufacturing, making PM an attractive alternative to conventional machining or forging processes. The ability to integrate multiple functions into a single component further enhances its cost-effectiveness and design flexibility, accelerating its adoption across diverse industrial applications globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Lightweight Automotive Components | +1.5% | North America, Europe, Asia Pacific (China, India) | Short to Mid-term (2025-2030) |

| Technological Advancements in PM Materials and Processes | +1.2% | Global | Mid to Long-term (2027-2033) |

| Increasing Adoption in Industrial and Electrical Applications | +0.8% | Asia Pacific, Europe | Short to Mid-term (2025-2029) |

| Benefits of Near-Net-Shape Manufacturing & Cost Efficiency | +1.0% | Global | Short to Mid-term (2025-2031) |

| Expansion of Electric Vehicle (EV) Production | +1.3% | China, Europe, North America | Mid to Long-term (2028-2033) |

Powder Metallurgy Component Market Restraints Analysis

Despite its significant advantages, the Powder Metallurgy Component market faces certain restraints that could temper its growth trajectory. One notable challenge is the relatively high initial capital investment required for PM equipment, including presses, furnaces, and tooling. This can be a barrier for smaller manufacturers or those in developing regions looking to adopt PM technologies, limiting market penetration in certain segments. The complex nature of process control and the need for specialized expertise also add to the operational costs and can deter wider adoption compared to more conventional manufacturing methods.

Another significant restraint involves the material properties of some powder metallurgy components, particularly concerning their ductility and toughness. While advancements have been made in developing new alloys and processes to improve these characteristics, some PM parts may still exhibit lower ductility compared to conventionally forged or machined components. This limitation can restrict their use in highly dynamic or impact-sensitive applications where maximum toughness is paramount, pushing industries in those sectors towards alternative manufacturing solutions. Overcoming this perception and enhancing material properties remains a continuous R&D focus.

Furthermore, the volatility of raw material prices, especially for metal powders such as iron, copper, and specialized alloys, poses a continuous challenge for manufacturers in the powder metallurgy industry. Fluctuations in commodity markets can directly impact production costs and profit margins, making long-term planning and pricing strategies more complex. This economic uncertainty can sometimes lead to reduced investment in new technologies or expansion, thereby acting as a brake on overall market growth and stability, particularly for companies operating on tight margins.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Equipment Costs | -0.7% | Developing Regions, Small & Medium Enterprises (SMEs) | Mid-term (2026-2030) |

| Limited Ductility and Toughness of Certain PM Parts | -0.5% | Global (Specific High-Stress Applications) | Long-term (2028-2033) |

| Raw Material Price Volatility | -0.4% | Global | Short to Mid-term (2025-2029) |

| Competition from Alternative Manufacturing Processes | -0.6% | Global | Mid-term (2026-2031) |

Powder Metallurgy Component Market Opportunities Analysis

The Powder Metallurgy Component market is presented with significant growth opportunities stemming from the rapid expansion of the electric vehicle (EV) sector. EVs require a new array of components, including soft magnetic materials for motors, specialized gears for powertrains, and complex structural parts, all of which can be efficiently produced using PM techniques. The demand for lightweight and energy-efficient solutions in EVs aligns perfectly with PM's inherent advantages, offering a substantial avenue for market expansion as automotive manufacturers increasingly shift towards electrification globally.

Another compelling opportunity lies in the growing demand from the medical and dental industries. Powder metallurgy, particularly Metal Injection Molding (MIM), is highly suitable for producing intricate, high-precision components for surgical instruments, implants, and dental prosthetics. The ability to work with biocompatible materials like titanium and stainless steel, combined with the capacity for miniaturization and complex designs, positions PM as a vital manufacturing process for these critical applications. As healthcare technologies advance and the global population ages, the demand for such specialized components is expected to surge.

Furthermore, the increasing integration of additive manufacturing (3D printing) technologies within the broader powder metallurgy landscape opens new frontiers for innovation and application. While traditional PM is geared for mass production, 3D printing with metal powders allows for rapid prototyping, customized low-volume production, and the creation of highly complex geometries that are impossible with conventional methods. This convergence provides manufacturers with unparalleled design freedom and the ability to produce on-demand parts for aerospace, defense, and advanced industrial sectors, effectively broadening the market's addressable scope and driving technological evolution.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Electric Vehicle (EV) Sector | +1.8% | Global (China, Europe, North America) | Mid to Long-term (2027-2033) |

| Expansion into Medical and Dental Applications | +1.0% | North America, Europe, Japan | Mid-term (2026-2030) |

| Integration with Additive Manufacturing (3D Printing) | +1.2% | Global | Long-term (2028-2033) |

| Increasing Focus on Sustainable Manufacturing | +0.7% | Europe, North America | Short to Mid-term (2025-2029) |

Powder Metallurgy Component Market Challenges Impact Analysis

The Powder Metallurgy Component market faces several operational and strategic challenges that can impede its optimal growth. One significant challenge is the inherent complexity associated with process control in PM manufacturing. Achieving consistent component density, mechanical properties, and dimensional accuracy requires precise control over numerous parameters, including powder characteristics, pressing pressure, sintering temperature, and atmosphere. Any deviation can lead to defects or inconsistent product quality, necessitating advanced monitoring systems and highly skilled personnel, which adds to operational complexity and costs.

Another pressing challenge is the need for continuous research and development to address the perceived limitations of PM components, particularly regarding their ductility and fatigue strength compared to wrought materials. While significant progress has been made, certain high-stress or critical applications still favor alternative manufacturing methods due to these concerns. Overcoming this perception and demonstrating superior performance in new material combinations and process refinements is crucial for expanding PM's market share in highly demanding sectors such as aerospace and defense, where failure tolerance is extremely low.

Furthermore, the industry is grappling with the challenge of a skilled labor shortage. Operating sophisticated powder metallurgy equipment and optimizing complex processes demand specialized knowledge in material science, metallurgy, and advanced manufacturing techniques. The lack of adequately trained technicians and engineers can lead to inefficiencies, increased production errors, and a slower adoption rate of new technologies. Addressing this talent gap through training programs and educational initiatives is vital for sustaining innovation and ensuring the long-term growth and competitiveness of the powder metallurgy industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Process Control and Quality Assurance | -0.6% | Global | Short to Mid-term (2025-2029) |

| Perceived Material Limitations (Ductility, Fatigue Strength) | -0.5% | Global (High-Performance Applications) | Mid to Long-term (2027-2033) |

| Skilled Labor Shortage | -0.4% | North America, Europe | Short to Mid-term (2025-2030) |

| Intense Competition and Pricing Pressures | -0.3% | Asia Pacific | Short-term (2025-2027) |

Powder Metallurgy Component Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Powder Metallurgy Component market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscapes. It covers the historical performance, current market status, and future projections, aiming to equip stakeholders with actionable intelligence for strategic decision-making. The scope encompasses various material types, manufacturing processes, and diverse application sectors, highlighting growth opportunities and critical challenges.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 43.0 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GKN Powder Metallurgy, Höganäs AB, Sumitomo Electric Industries, Inc., Allegheny Technologies Incorporated (ATI), Sandvik AB, Kennametal Inc., Miba AG, ZF Friedrichshafen AG, Hitachi Chemical Co., Ltd., Rio Tinto, Carpenter Technology Corporation, AMETEK, Inc., Erasteel, JFE Steel Corporation, Metal Powder Products Company, AMG Advanced Metallurgical Group, PyroGenesis Canada Inc., Advanced Technology & Materials Co., Ltd. (AT&M), VDM Metals, Schunk Carbon Technology. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Powder Metallurgy Component market is extensively segmented based on material type, manufacturing process, and application, reflecting the diverse and specialized nature of its end-use industries. This granular segmentation allows for a precise understanding of market dynamics within each category, revealing specific growth drivers, technological preferences, and regional adoption patterns. Analyzing these segments is critical for identifying niche opportunities and developing targeted strategies to meet the varying demands of sectors such as automotive, industrial, and medical.

The material type segmentation highlights the predominant use of ferrous metals (iron, steel, stainless steel) due to their cost-effectiveness and versatile mechanical properties, while non-ferrous and refractory metals gain traction in high-performance applications. Process segmentation underscores the increasing sophistication of PM technologies, with Metal Injection Molding (MIM) and additive manufacturing (3D printing) emerging as key growth areas for complex, high-precision components, complementing traditional press and sinter methods. These advanced processes enable the production of geometries and material combinations previously unattainable.

Furthermore, the application-based segmentation demonstrates the widespread utility of powder metallurgy components across a multitude of industries. The automotive sector remains the largest consumer, driven by trends toward lightweighting and electrification. However, significant growth is also observed in industrial machinery, electrical and electronics, and particularly the medical and aerospace sectors, where the demand for specialized, high-reliability components is robust. This broad application spectrum underscores the adaptability and increasing importance of powder metallurgy in modern manufacturing.

- By Material Type:

- Ferrous: Iron, Steel, Stainless Steel

- Non-Ferrous: Aluminum, Copper, Titanium, Nickel, Cobalt

- Refractory Metals: Tungsten, Molybdenum, Tantalum

- Precious Metals

- By Process:

- Conventional Press and Sinter

- Metal Injection Molding (MIM)

- Hot Isostatic Pressing (HIP)

- Additive Manufacturing (3D Printing)

- Powder Forging

- Spray Forming

- By Application:

- Automotive: Engine Components, Transmission Components, Chassis Components, Structural Components

- Industrial: Gears, Bearings, Filters, Tooling, Electrical Components

- Electrical & Electronics: Magnets, Heat Sinks, Connectors

- Medical & Dental: Implants, Surgical Instruments, Dental Brackets

- Aerospace & Defense: Turbine Components, Structural Parts, Munitions

- Consumer Goods: Sports Equipment, Appliances

- Oil & Gas

Regional Highlights

The global Powder Metallurgy Component market exhibits significant regional variations in terms of production capabilities, market demand, and technological adoption. Asia Pacific consistently leads the market, primarily driven by the robust growth of its manufacturing sectors, particularly in automotive, industrial machinery, and consumer electronics. Countries like China, India, and Japan are major contributors, benefiting from large-scale industrialization, increasing disposable incomes, and a strong emphasis on domestic production. The region's expanding electric vehicle market also acts as a substantial growth catalyst for advanced PM components.

Europe represents a mature yet highly innovative market for powder metallurgy components, with Germany, France, and the UK at the forefront. The region is characterized by its strong automotive industry, a significant presence of precision engineering, and early adoption of advanced manufacturing technologies. European manufacturers are heavily investing in R&D for sustainable PM practices and high-performance alloys, catering to stringent environmental regulations and the demand for high-quality, durable components across industrial and aerospace applications. The focus here is often on higher value-added, specialized parts.

North America, particularly the United States, is another key region in the powder metallurgy market, driven by its advanced automotive sector, thriving aerospace and defense industries, and a growing medical device market. The region benefits from substantial investments in R&D, a strong focus on additive manufacturing integration, and the presence of numerous key players and research institutions. The demand for lightweight materials in transportation and complex components in medical implants provides significant growth opportunities, supported by a favorable regulatory environment and a strong manufacturing base.

- Asia Pacific: Dominant market share due to burgeoning automotive production, rapid industrialization, and increasing demand for consumer electronics in countries like China, India, and Japan. Significant growth from EV manufacturing.

- Europe: Mature market with strong focus on high-performance applications, precision engineering, and sustainable manufacturing, especially in Germany, France, and the UK. Automotive and industrial sectors are key drivers.

- North America: Significant market driven by aerospace, defense, automotive, and medical industries. High adoption of advanced PM processes and strong R&D investments.

- Latin America & Middle East and Africa (MEA): Emerging markets with growing industrial bases and increasing automotive production, offering future growth potential as manufacturing capabilities expand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Powder Metallurgy Component Market.- GKN Powder Metallurgy

- Höganäs AB

- Sumitomo Electric Industries, Inc.

- Allegheny Technologies Incorporated (ATI)

- Sandvik AB

- Kennametal Inc.

- Miba AG

- ZF Friedrichshafen AG

- Hitachi Chemical Co., Ltd.

- Rio Tinto

- Carpenter Technology Corporation

- AMETEK, Inc.

- Erasteel

- JFE Steel Corporation

- Metal Powder Products Company

- AMG Advanced Metallurgical Group

- PyroGenesis Canada Inc.

- Advanced Technology & Materials Co., Ltd. (AT&M)

- VDM Metals

- Schunk Carbon Technology

Frequently Asked Questions

Analyze common user questions about the Powder Metallurgy Component market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is powder metallurgy and how does it differ from traditional manufacturing?

Powder metallurgy (PM) is a manufacturing process that forms components from metal powders. It differs from traditional methods like machining or forging by enabling the creation of complex shapes with minimal material waste, often reducing the need for secondary machining operations and allowing for unique material combinations.

What are the primary applications of powder metallurgy components?

Powder metallurgy components are extensively used in the automotive industry for engine, transmission, and chassis parts. Other major applications include industrial machinery, electrical and electronics, medical devices, and aerospace and defense for high-performance and lightweight parts.

What key trends are shaping the Powder Metallurgy Component market?

Key trends include the growing demand for lightweight components, increasing adoption in electric vehicles (EVs), advancements in Metal Injection Molding (MIM) and additive manufacturing (3D printing), and the development of new high-performance alloys and composite materials.

How does powder metallurgy contribute to sustainability?

Powder metallurgy is inherently a sustainable manufacturing process due to its near-net-shape capabilities, which significantly reduce material waste. It also enables the use of recycled materials and can be more energy-efficient than traditional methods for certain parts, contributing to a lower carbon footprint.

What are the main challenges facing the Powder Metallurgy Component market?

Key challenges include the high initial capital investment for equipment, the complexity of process control, perceived limitations in ductility for some PM parts compared to wrought materials, and the ongoing challenge of raw material price volatility.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted