Electronic Component Market

Electronic Component Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703533 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Electronic Component Market Size

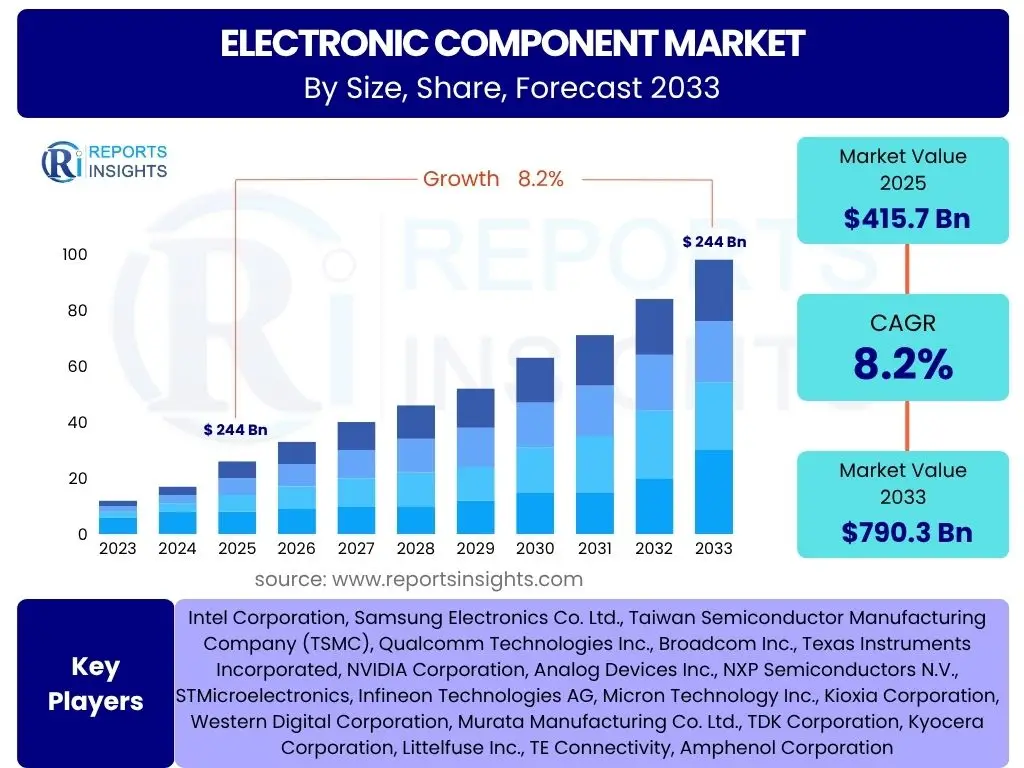

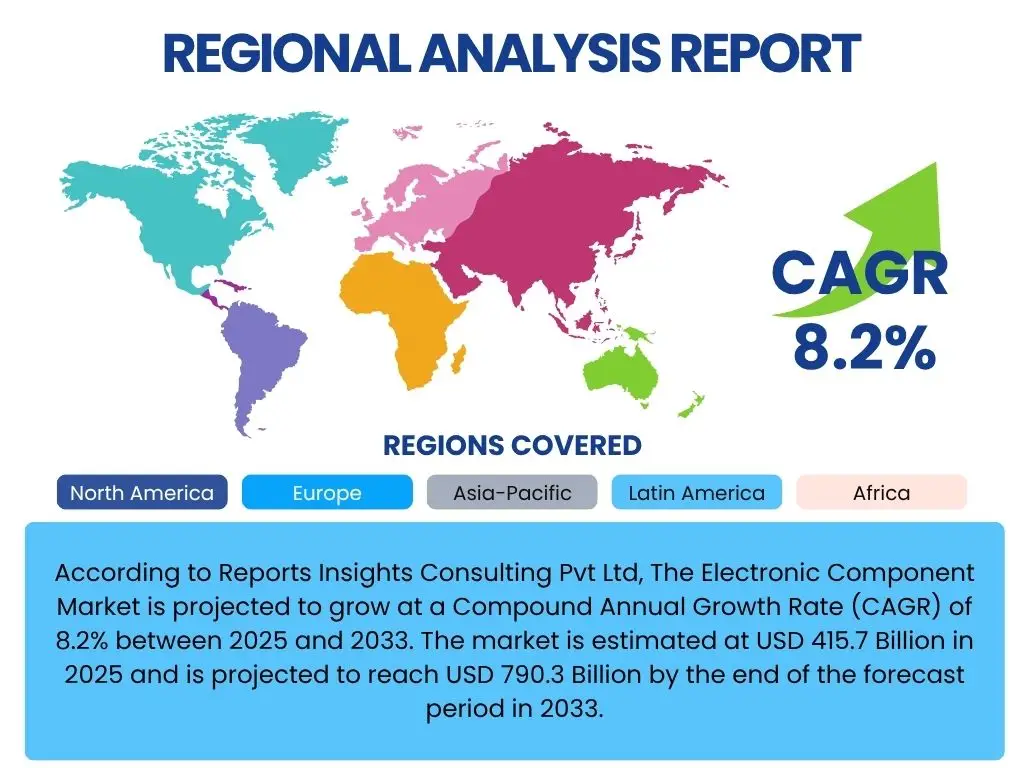

According to Reports Insights Consulting Pvt Ltd, The Electronic Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 415.7 Billion in 2025 and is projected to reach USD 790.3 Billion by the end of the forecast period in 2033.

Key Electronic Component Market Trends & Insights

The electronic component market is undergoing significant transformation, driven by pervasive technological advancements and evolving consumer and industrial demands. A primary trend is the accelerating miniaturization and integration of components, enabling the creation of more compact, powerful, and efficient electronic devices across various sectors. This includes advancements in System-in-Package (SiP) and heterogeneous integration, which are critical for increasing functional density and improving performance within limited footprints.

Another crucial trend is the increasing demand for specialized components tailored for emerging technologies such as Artificial Intelligence, 5G communication, and the Internet of Things (IoT). This drives innovation in high-performance processors, advanced sensors, and low-power connectivity modules. Furthermore, the push towards sustainability and energy efficiency is influencing component design and manufacturing, leading to the development of more eco-friendly materials and power-efficient architectures. Geopolitical considerations and supply chain resilience have also become paramount, leading to efforts to diversify manufacturing bases and strengthen domestic production capabilities.

The automotive industry's rapid transition towards electric vehicles (EVs) and autonomous driving is a significant catalyst for growth in power semiconductors, advanced sensors, and connectivity modules. Similarly, the expansion of cloud computing and data centers fuels demand for high-speed memory, robust processors, and optical components. These multifaceted trends collectively shape the market, emphasizing innovation, reliability, and strategic supply chain management as key determinants of success.

- Miniaturization and higher integration density in component design.

- Increased demand for AI-specific chips, high-performance computing, and edge processing.

- Proliferation of 5G technology driving demand for RF components and baseband processors.

- Rapid growth in IoT devices necessitating advanced sensors and low-power connectivity solutions.

- Electrification and autonomy in the automotive sector boosting demand for power semiconductors and control units.

- Focus on supply chain diversification and regional manufacturing resilience.

- Emphasis on energy-efficient and sustainable component manufacturing processes.

- Advancements in advanced packaging technologies for improved performance and cost-efficiency.

AI Impact Analysis on Electronic Component

Artificial Intelligence (AI) is profoundly reshaping the electronic component landscape, fundamentally altering both demand patterns and manufacturing processes. The escalating need for AI-specific hardware, such as Graphics Processing Units (GPUs), Neural Processing Units (NPUs), and application-specific integrated circuits (ASICs), is a primary driver. These components are designed for parallel processing and efficient execution of AI algorithms, ranging from cloud-based AI training to edge AI inference, thereby demanding higher computational power, lower latency, and greater energy efficiency.

Beyond specialized chips, AI also influences the demand for a broader range of components crucial for AI infrastructure, including high-bandwidth memory (HBM), advanced storage solutions, and high-speed interconnects. The integration of AI into manufacturing processes, such as predictive maintenance for machinery and quality control in fabrication plants, is also enhancing efficiency and reducing waste in component production. This extends to AI-driven design automation tools that accelerate chip design cycles and optimize complex layouts, leading to faster innovation and time-to-market for new components.

Furthermore, the proliferation of AI in various end-use applications, from smart consumer electronics and autonomous vehicles to industrial automation and healthcare, creates new markets for integrated AI modules and intelligent sensors. This pushes manufacturers to develop more sophisticated and interconnected components capable of on-device AI processing. Consequently, the impact of AI is not limited to specific component types but rather permeates the entire ecosystem, driving a paradigm shift towards intelligent and highly optimized electronic hardware.

- Spike in demand for high-performance AI processors (GPUs, NPUs, ASICs).

- Increased requirement for high-bandwidth memory (HBM) and low-latency storage.

- Integration of AI in chip design and verification processes, accelerating development cycles.

- Enhanced manufacturing efficiency through AI-powered predictive maintenance and quality control.

- Development of edge AI components enabling on-device intelligence and reduced reliance on cloud.

- Creation of new markets for AI-enabled sensors and integrated modules in various applications.

- Focus on energy-efficient AI hardware to support sustainable AI deployment.

Key Takeaways Electronic Component Market Size & Forecast

The Electronic Component Market is poised for substantial and sustained growth over the forecast period, reflecting its foundational role in the rapidly advancing digital economy. The projected Compound Annual Growth Rate (CAGR) of 8.2% from 2025 to 2033 indicates a robust expansion, driven by the pervasive integration of electronics into nearly every aspect of modern life. This growth is underpinned by the increasing adoption of transformative technologies across diverse industries, leading to consistent demand for more sophisticated, efficient, and interconnected components.

The market's expansion from an estimated USD 415.7 Billion in 2025 to USD 790.3 Billion by 2033 highlights the continuous innovation and investment in the sector. Key drivers include the accelerated deployment of 5G infrastructure, the widespread adoption of Internet of Things (IoT) devices, the rapid evolution of artificial intelligence and machine learning capabilities, and the significant shift towards electric and autonomous vehicles. These factors collectively stimulate demand for a wide array of electronic components, from advanced semiconductors and passive components to intricate electromechanical devices and optoelectronics.

Furthermore, global geopolitical dynamics and the emphasis on supply chain resilience are influencing regional manufacturing strategies, potentially leading to diversified production hubs and increased domestic investments. The imperative for energy efficiency and sustainable practices is also shaping product development, driving innovation towards greener and more resource-efficient components. Overall, the market's trajectory underscores its critical importance as an enabler of technological progress and a core pillar of industrial and consumer innovation globally.

- Significant market expansion with a projected CAGR of 8.2% from 2025 to 2033.

- Market valuation is expected to nearly double, reaching USD 790.3 Billion by 2033.

- Growth driven by pervasive digitalization, 5G deployment, IoT expansion, and AI integration.

- Automotive industry's transition to EVs and autonomous driving is a major growth catalyst.

- Emphasis on supply chain stability and localized manufacturing influencing market dynamics.

- Continuous innovation in component design and materials is essential for sustaining growth.

- Increasing demand for energy-efficient and high-performance components across all sectors.

Electronic Component Market Drivers Analysis

The electronic component market is propelled by a confluence of powerful technological and industrial forces that are fundamentally reshaping global demand. A primary driver is the accelerating pace of digital transformation across all sectors, leading to a pervasive need for electronic devices and systems. This includes the expansion of cloud computing infrastructure, necessitating high-performance processors and memory, as well as the proliferation of smart cities and smart homes, which rely on an intricate network of interconnected sensors and controllers.

Another significant driver is the rapid global deployment of 5G networks, which demands a new generation of high-frequency, high-efficiency radio frequency (RF) components, baseband processors, and optical communication modules. Concurrently, the burgeoning Internet of Things (IoT) ecosystem, encompassing everything from industrial IoT to consumer wearables, fuels demand for low-power, compact, and highly integrated components such as microcontrollers, sensors, and wireless connectivity chips. The automotive sector's dramatic shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is creating an unprecedented need for power semiconductors, advanced sensors, and sophisticated electronic control units (ECUs), becoming a critical growth engine for the market.

Furthermore, advancements in Artificial Intelligence (AI) and Machine Learning (ML) are driving specialized demand for high-performance computing components, including GPUs, NPUs, and custom ASICs, which are essential for processing complex algorithms. The increasing consumer adoption of sophisticated smart devices, wearables, and augmented/virtual reality (AR/VR) technologies also significantly contributes to the demand for advanced electronic components. These integrated drivers collectively create a robust and expanding market for electronic components, fostering continuous innovation and investment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Digital Transformation & Cloud Computing Expansion | +2.1% | North America, Europe, Asia Pacific | 2025-2033 |

| Rapid 5G Network Deployment & IoT Proliferation | +1.8% | Asia Pacific (China, South Korea), North America, Europe | 2025-2030 |

| Electrification and Autonomy in the Automotive Industry | +1.7% | Europe (Germany), Asia Pacific (China, Japan), North America | 2025-2033 |

| Growing Adoption of AI and Machine Learning Technologies | +1.5% | North America, Asia Pacific (China), Europe | 2026-2033 |

| Increasing Demand for Smart Consumer Electronics | +1.1% | Asia Pacific (China, India), North America, Europe | 2025-2033 |

Electronic Component Market Restraints Analysis

Despite robust growth prospects, the electronic component market faces several significant restraints that could impede its trajectory. A primary concern is the inherent volatility and complexity of global supply chains. Geopolitical tensions, trade disputes, and unexpected events such as natural disasters or pandemics can lead to severe disruptions in the availability of raw materials, manufacturing capacity, and logistics. This susceptibility to external shocks can result in component shortages, price volatility, and extended lead times, directly impacting production cycles and market stability for end-product manufacturers.

Another considerable restraint is the substantial capital investment and high research and development (R&D) costs associated with advancing component technologies. The semiconductor industry, in particular, requires billions of dollars for new fabrication plants (fabs) and continuous innovation to keep pace with Moore's Law and evolving market demands. This high barrier to entry and the need for constant reinvestment can limit the number of new players and put financial strain on existing ones, especially during economic downturns or periods of reduced demand.

Furthermore, the market is subject to intense global competition and pricing pressures, particularly in commodity component segments. This competition, coupled with rapid technological obsolescence, means manufacturers must constantly innovate while simultaneously managing cost efficiencies. Economic slowdowns and fluctuating consumer spending patterns also pose a threat, as they can directly reduce demand for electronic devices across various sectors, leading to inventory build-ups and revenue declines for component suppliers. Navigating these multifaceted restraints requires strategic foresight, robust risk management, and continuous adaptation to market dynamics.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions & Geopolitical Tensions | -1.5% | Global, particularly Asia Pacific (China, Taiwan), North America, Europe | Short-to-Medium Term (2025-2028) |

| High Capital Investment & R&D Costs | -0.9% | Global, particularly advanced manufacturing regions | Long Term (2025-2033) |

| Intense Global Competition & Pricing Pressures | -0.8% | Global | Ongoing (2025-2033) |

| Economic Downturns and Fluctuating Consumer Spending | -0.7% | Global, especially major consumer markets | Intermittent (2025-2033) |

| Technological Obsolescence & Rapid Innovation Cycles | -0.6% | Global | Ongoing (2025-2033) |

Electronic Component Market Opportunities Analysis

The electronic component market presents numerous strategic opportunities for growth and innovation, driven by evolving technological paradigms and expanding market needs. A significant opportunity lies in the burgeoning adoption of advanced packaging technologies, such as 3D stacking, chiplets, and fan-out wafer-level packaging. These innovations enable higher integration density, improved performance, and reduced power consumption, addressing the increasing demand for compact and powerful devices across AI, HPC, and edge computing applications. Companies investing in these areas can gain a significant competitive edge.

Emerging economies and underserved regions offer substantial untapped market potential. As digitalization efforts intensify in parts of Latin America, Africa, and Southeast Asia, the demand for basic to advanced electronic components for infrastructure development, consumer electronics, and industrial automation is expected to surge. Localized manufacturing and distribution strategies, coupled with products tailored to regional needs, can unlock significant market share in these growing areas.

Furthermore, the increasing focus on sustainability and energy efficiency across industries creates opportunities for components that facilitate greener electronics. This includes the development of power-efficient semiconductors, eco-friendly materials, and components designed for circular economy principles, such as recyclability and extended lifespan. Manufacturers that can demonstrate a commitment to environmental responsibility through their product offerings and manufacturing processes will likely resonate with environmentally conscious consumers and increasingly stringent regulatory requirements, paving the way for differentiated market positions and new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Packaging Technologies | +1.3% | Global, particularly Asia Pacific (Taiwan, South Korea), North America | 2025-2033 |

| Expansion into Emerging Markets & Developing Economies | +1.1% | Asia Pacific (India, Southeast Asia), Latin America, MEA | 2026-2033 |

| Growing Demand for Sustainable & Energy-Efficient Components | +0.9% | Europe, North America, parts of Asia Pacific (Japan) | 2025-2033 |

| Niche Applications in Healthcare, Aerospace, and Defense | +0.8% | North America, Europe, parts of Asia Pacific | 2025-2033 |

Electronic Component Market Challenges Impact Analysis

The electronic component market faces several significant challenges that require strategic navigation for sustained growth and profitability. One major challenge is the inherent complexity and high cost associated with R&D and manufacturing processes. Producing cutting-edge components, especially semiconductors, demands multi-billion-dollar investments in advanced fabrication plants (fabs) and sophisticated equipment, coupled with continuous expenditure on research to develop smaller, faster, and more energy-efficient designs. This financial burden can be prohibitive for smaller players and impacts the profitability margins of even large corporations.

Another critical challenge is the rapid pace of technological obsolescence. In a market driven by relentless innovation, components can become outdated quickly, leading to shorter product lifecycles and the need for manufacturers to constantly update their product portfolios. This requires significant resources for redesign, retooling, and market introduction, making it difficult to recoup investments fully before the next generation of technology emerges. This challenge is compounded by the intense global competition, which often leads to price erosion and tighter profit margins across various component categories.

Furthermore, managing intricate global supply chains remains a formidable challenge. The electronic component industry relies on a complex web of international suppliers for raw materials, sub-components, and manufacturing services. Geopolitical instability, trade protectionism, and unexpected events like pandemics or natural disasters can severely disrupt these chains, leading to shortages, increased costs, and production delays. Ensuring supply chain resilience and diversification has become a strategic imperative, yet it introduces its own set of complexities and costs, requiring significant foresight and adaptability from market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Manufacturing Costs | -1.2% | Global | Ongoing (2025-2033) |

| Rapid Technological Obsolescence | -1.0% | Global | Ongoing (2025-2033) |

| Supply Chain Vulnerability & Geopolitical Risks | -0.8% | Global, particularly Asia Pacific | Short to Medium Term (2025-2028) |

| Skilled Labor Shortages | -0.7% | North America, Europe, parts of Asia Pacific | Long Term (2025-2033) |

| Intellectual Property (IP) Theft and Cybersecurity Threats | -0.5% | Global, particularly emerging manufacturing hubs | Ongoing (2025-2033) |

Electronic Component Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Electronic Component Market, covering historical data, current market dynamics, and future projections. It examines key trends, drivers, restraints, opportunities, and challenges influencing market growth from 2019 to 2033, with a detailed forecast extending to 2033. The report segments the market by component type, application, and end-use industry across major global regions, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 415.7 Billion |

| Market Forecast in 2033 | USD 790.3 Billion |

| Growth Rate | 8.2% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Samsung Electronics Co. Ltd., Taiwan Semiconductor Manufacturing Company (TSMC), Qualcomm Technologies Inc., Broadcom Inc., Texas Instruments Incorporated, NVIDIA Corporation, Analog Devices Inc., NXP Semiconductors N.V., STMicroelectronics, Infineon Technologies AG, Micron Technology Inc., Kioxia Corporation, Western Digital Corporation, Murata Manufacturing Co. Ltd., TDK Corporation, Kyocera Corporation, Littelfuse Inc., TE Connectivity, Amphenol Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The electronic component market is highly diverse, segmented across various dimensions to reflect the complexity of its offerings and applications. These segmentations are crucial for understanding the nuanced dynamics of demand and supply across the industry. Components are broadly categorized into Active Components, which include semiconductors (integrated circuits, microprocessors, memory chips) and optoelectronics; Passive Components, such as resistors, capacitors, and inductors, which are essential for circuit functionality; and Electromechanical Components, encompassing connectors, switches, and relays, vital for system interconnection and control. This categorization helps to delineate market shares and growth trajectories for different core technologies.

Further segmentation by application highlights the key industries driving demand. Consumer electronics remains a foundational segment, driven by smartphones, laptops, and home appliances. The automotive sector is experiencing explosive growth due to the proliferation of electric vehicles, autonomous driving systems, and in-car infotainment. Industrial applications, telecommunications infrastructure, healthcare devices, and aerospace and defense also represent significant and growing segments, each with unique requirements for component performance, reliability, and certifications. This granular view allows for a detailed analysis of market opportunities and challenges specific to each sector.

The end-use industry segmentation provides a deeper insight into how electronic components are ultimately consumed, from computing and data storage centers requiring high-performance components to communications networks, industrial automation systems, and medical devices. This comprehensive segmentation framework assists stakeholders in identifying high-growth areas, understanding competitive landscapes, and formulating targeted business strategies. The interplay between component types and their diverse applications and end-uses defines the intricate structure and future direction of the electronic component market.

- By Component Type:

- Active Components (Semiconductors, Optoelectronics, Displays)

- Passive Components (Resistors, Capacitors, Inductors)

- Electromechanical Components (Connectors, Switches, Relays)

- Other Components

- By Application:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunication

- Healthcare

- Aerospace & Defense

- Others

- By End-Use Industry:

- Computing & Data Storage

- Communications

- Industrial Automation

- Automotive & Transportation

- Consumer Appliances

- Medical Devices

- Energy & Utilities

Regional Highlights

- Asia Pacific (APAC): Dominates the global market due to its robust manufacturing base, encompassing major producers like China, South Korea, Taiwan, and Japan. The region benefits from high consumer electronics production, rapid adoption of 5G and IoT technologies, and significant investments in automotive electronics. China is a key growth engine due to its vast manufacturing capabilities and burgeoning domestic demand, while South Korea and Taiwan lead in advanced semiconductor fabrication.

- North America: A leader in research and development, particularly for high-end semiconductors, AI-specific chips, and advanced computing components. The region exhibits strong demand from the automotive, aerospace, defense, and data center industries. Investments in domestic manufacturing capabilities and a focus on cutting-edge technologies drive innovation and market value.

- Europe: Characterized by a strong automotive sector, driving demand for power semiconductors, sensors, and microcontrollers for electric and autonomous vehicles. Europe also has significant industrial automation and healthcare electronics markets, contributing to stable demand for specialized components. Germany, France, and the UK are key contributors to regional market growth.

- Latin America: An emerging market with growing demand driven by increasing industrialization, infrastructure development, and rising disposable incomes fueling consumer electronics adoption. Brazil and Mexico are notable markets, attracting investment in electronics manufacturing and assembly, particularly in the automotive and telecommunications sectors.

- Middle East and Africa (MEA): Shows promising growth potential, spurred by government initiatives for economic diversification, investment in smart city projects, and expanding telecommunications infrastructure. The region is increasingly focusing on local assembly and manufacturing capabilities, though it remains a net importer of many advanced components.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electronic Component Market.- Intel Corporation

- Samsung Electronics Co. Ltd.

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Qualcomm Technologies Inc.

- Broadcom Inc.

- Texas Instruments Incorporated

- NVIDIA Corporation

- Analog Devices Inc.

- NXP Semiconductors N.V.

- STMicroelectronics

- Infineon Technologies AG

- Micron Technology Inc.

- Kioxia Corporation

- Western Digital Corporation

- Murata Manufacturing Co. Ltd.

- TDK Corporation

- Kyocera Corporation

- Littelfuse Inc.

- TE Connectivity

- Amphenol Corporation

Frequently Asked Questions

Analyze common user questions about the Electronic Component market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Electronic Component Market?

The Electronic Component Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033, driven by pervasive digitalization and technological advancements.

Which key factors are driving the demand for electronic components?

Key drivers include the global rollout of 5G, rapid expansion of IoT devices, increasing adoption of Artificial Intelligence, growth in the electric and autonomous vehicle sectors, and overall digital transformation across industries.

How is AI impacting the electronic component market?

AI is significantly impacting the market by increasing demand for specialized high-performance processors (GPUs, NPUs), high-bandwidth memory, and advanced sensors, while also enhancing manufacturing processes through automation and design optimization.

What are the major challenges faced by the Electronic Component Market?

The market faces challenges such as high R&D and manufacturing costs, rapid technological obsolescence, vulnerabilities in global supply chains, intense competition, and skilled labor shortages.

Which region holds the largest share in the Electronic Component Market?

Asia Pacific (APAC) currently holds the largest market share, driven by its robust manufacturing ecosystem, significant consumer electronics production, and rapid technology adoption in countries like China, South Korea, and Taiwan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted