Consumer Electronic Sensor Market

Consumer Electronic Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703140 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Consumer Electronic Sensor Market Size

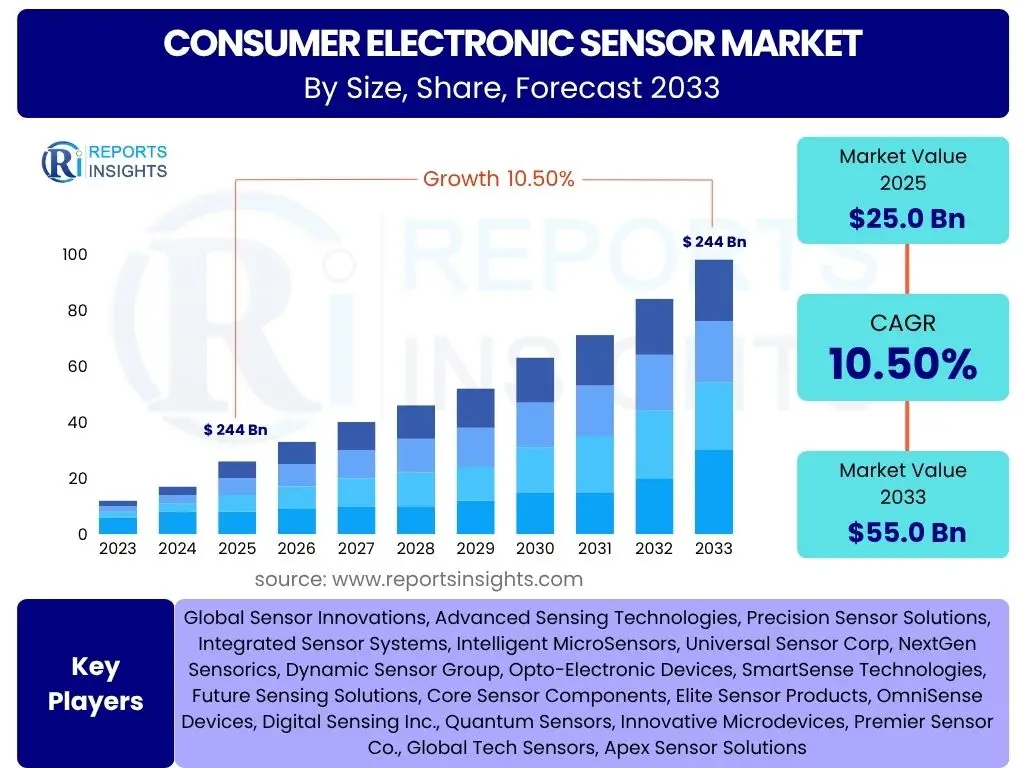

According to Reports Insights Consulting Pvt Ltd, The Consumer Electronic Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 25.0 billion in 2025 and is projected to reach USD 55.0 billion by the end of the forecast period in 2033.

Key Consumer Electronic Sensor Market Trends & Insights

The Consumer Electronic Sensor market is currently experiencing significant transformations driven by an increasing demand for enhanced user experience, advanced functionalities, and seamless connectivity across a myriad of devices. Key trends revolve around the miniaturization of sensors, enabling their integration into smaller, more versatile form factors like smartwatches, hearables, and compact IoT devices. This miniaturization is critical for maintaining the sleek designs and portability expected by consumers, while simultaneously expanding the range of data points that can be captured and processed in real-time.

Another prominent trend is the pervasive integration of multi-sensor modules, where several types of sensors are combined into a single, compact package. This allows for more comprehensive data collection and sophisticated contextual awareness, such as combining accelerometers, gyroscopes, and magnetometers for precise motion tracking or integrating ambient light, proximity, and temperature sensors for optimized smart home environments. The drive towards energy efficiency is also paramount, with sensor manufacturers continuously innovating to reduce power consumption, thereby extending battery life in portable consumer electronics and aligning with broader sustainability goals.

Furthermore, the market is witnessing a surge in demand for biometric and health-monitoring sensors, fueled by growing health consciousness and the proliferation of fitness trackers and medical wearables. These sensors, including heart rate monitors, SpO2 sensors, and even advanced chemical sensors, are transforming personal health management by providing actionable insights directly to consumers. The advent of 5G technology is also playing a pivotal role, enabling faster data transmission and processing, which in turn unlocks new possibilities for real-time sensor applications, cloud-based analytics, and augmented/virtual reality experiences.

- Miniaturization and compact form factors for ubiquitous integration.

- Integration of multi-sensor arrays for enhanced contextual awareness.

- Development of ultra-low power consumption sensors for extended battery life.

- Increased demand for biometric and health-monitoring sensors in wearables.

- Leveraging 5G connectivity for real-time data processing and new applications.

AI Impact Analysis on Consumer Electronic Sensor

The integration of Artificial Intelligence (AI) is fundamentally reshaping the capabilities and applications of consumer electronic sensors, moving them beyond mere data collection to intelligent data interpretation and predictive analytics. Consumers are increasingly seeking devices that can understand their environment and behavior, and AI enables sensors to process vast amounts of raw data from multiple sources, identify patterns, and provide personalized insights. For example, in smart home devices, AI-powered sensors can learn user routines to optimize energy consumption or enhance security by distinguishing between normal and anomalous activities.

AI algorithms are being deployed both at the edge (on-device processing) and in the cloud, allowing for more efficient and faster decision-making. Edge AI reduces latency and enhances privacy by processing sensitive data locally, which is crucial for applications requiring immediate responses like autonomous navigation in robotics or real-time health monitoring. This also lessens reliance on constant cloud connectivity, making devices more robust and independent. Furthermore, AI contributes significantly to noise reduction and data accuracy in sensors, filtering out irrelevant signals and improving the reliability of sensor outputs, which is vital for critical applications such as fall detection in elderly care wearables.

The impact of AI extends to enabling adaptive and self-calibrating sensors, where AI models can learn from environmental changes and continuously optimize sensor performance without manual intervention. This adaptability is particularly valuable in dynamic consumer environments where conditions can vary widely. While AI offers immense potential for enhancing sensor intelligence and creating more intuitive consumer experiences, concerns around data privacy, algorithmic bias, and the computational power required for complex AI models remain key considerations for developers and consumers alike. Addressing these concerns will be critical for widespread adoption and trust in AI-enhanced sensor technologies.

- Enables intelligent data processing and predictive analytics at the edge and cloud.

- Improves sensor accuracy, noise reduction, and data interpretation.

- Facilitates personalized user experiences and adaptive device functionalities.

- Supports real-time decision-making in applications like health monitoring and smart automation.

- Drives the development of self-calibrating and context-aware sensor systems.

Key Takeaways Consumer Electronic Sensor Market Size & Forecast

The Consumer Electronic Sensor market is poised for robust expansion, driven primarily by the relentless innovation in smart devices and the increasing integration of Internet of Things (IoT) technologies into daily life. A significant takeaway is the market's resilience and adaptability, as manufacturers continuously refine sensor technologies to meet evolving consumer demands for more intelligent, interconnected, and miniature devices. This growth is not merely volumetric but also qualitative, reflecting a shift towards more sophisticated, multi-functional, and AI-enabled sensor solutions that provide deeper insights and automation.

Another crucial insight is the diversified application landscape, moving beyond traditional smartphones to encompass a broad spectrum of wearables, smart home devices, automotive infotainment systems, and emerging augmented/virtual reality platforms. This diversification ensures a broad revenue base and mitigates risks associated with over-reliance on a single product category. The Asia Pacific region, particularly China and India, will continue to be a powerhouse for growth, propelled by large manufacturing bases, rapid urbanization, and increasing disposable incomes leading to higher adoption rates of consumer electronics.

Finally, the market forecast underscores the imperative for continuous research and development, particularly in areas like power efficiency, advanced material science for sensor fabrication, and secure data handling. Companies that can effectively balance innovation with cost-effectiveness and address privacy concerns will be best positioned to capture market share. The symbiotic relationship between hardware advancements in sensors and software innovations in AI and data analytics will be critical for unlocking the full potential of this market, enabling a future where devices are truly intuitive and responsive to human needs.

- Significant growth driven by IoT, smart devices, and evolving consumer demands.

- Diversification of applications beyond smartphones into wearables, smart homes, and AR/VR.

- Asia Pacific region identified as a primary growth engine due to manufacturing and adoption rates.

- Emphasis on R&D for power efficiency, advanced materials, and data security.

- AI integration is a core driver for enhanced sensor intelligence and personalized experiences.

Consumer Electronic Sensor Market Drivers Analysis

The pervasive proliferation of smart devices across various consumer segments stands as a primary catalyst for the Consumer Electronic Sensor market's expansion. Smartphones, smartwatches, fitness trackers, and smart home appliances are increasingly integrating a multitude of sensors to offer enhanced functionalities, user convenience, and data-driven insights. This ongoing trend of device adoption, coupled with consumer expectations for more sophisticated features, directly fuels the demand for a diverse range of high-performance sensors, from accelerometers for motion tracking to environmental sensors for air quality monitoring.

The rapid expansion of the Internet of Things (IoT) ecosystem is another significant driver. As more everyday objects become interconnected and capable of data exchange, the need for embedded sensors that can collect relevant information about their environment and status grows exponentially. This includes sensors in smart appliances that can monitor their performance, sensors in wearable devices that track health metrics, and sensors in smart city infrastructures that manage resources. The ability of these sensors to facilitate seamless communication and automation within the IoT framework is indispensable for realizing the vision of a truly smart and connected world.

Furthermore, the increasing global health consciousness and the aging population have created a surging demand for health and wellness monitoring devices. Wearable health trackers equipped with advanced biometric sensors, such as heart rate, blood oxygen, and even ECG sensors, are becoming mainstream consumer products. These devices empower individuals to proactively manage their health, track fitness goals, and even provide early alerts for potential health issues, thereby creating a substantial market segment for specialized medical and wellness-focused electronic sensors. The continuous innovation in these areas is expected to sustain significant growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Smart Devices (Smartphones, Wearables) | +3.2% | Global, particularly Asia Pacific & North America | Short to Mid-term (2025-2029) |

| Expansion of the Internet of Things (IoT) Ecosystem | +2.8% | Global, with strong growth in emerging markets | Mid to Long-term (2027-2033) |

| Increasing Demand for Health & Wellness Monitoring Devices | +2.5% | North America, Europe, East Asia | Short to Mid-term (2025-2030) |

| Advancements in Augmented Reality (AR) and Virtual Reality (VR) | +1.5% | North America, Europe, Japan | Mid to Long-term (2028-2033) |

| Rising Adoption of Home Automation and Smart Home Technologies | +1.0% | North America, Europe, China | Short to Mid-term (2025-2029) |

Consumer Electronic Sensor Market Restraints Analysis

One significant restraint impacting the Consumer Electronic Sensor market is the escalating cost of research and development (R&D) and manufacturing. Developing cutting-edge sensor technologies that meet stringent performance, miniaturization, and power consumption requirements involves substantial investments in materials science, semiconductor fabrication, and precision engineering. These high R&D expenditures, coupled with the capital-intensive nature of setting up and maintaining advanced manufacturing facilities, can inflate the final cost of sensors, potentially hindering their widespread adoption, especially in price-sensitive consumer electronics segments.

Another major challenge stems from supply chain disruptions and geopolitical uncertainties. The global sensor manufacturing industry relies on complex, interconnected supply chains that span multiple countries for raw materials, components, and specialized manufacturing processes. Events such as natural disasters, pandemics, trade disputes, or political instabilities can severely disrupt these chains, leading to raw material shortages, production delays, and increased component costs. Such disruptions can cause unpredictable fluctuations in sensor availability and pricing, impacting the production schedules and profitability of consumer electronics manufacturers.

Furthermore, concerns regarding data privacy and security pose a notable restraint. Consumer electronic sensors, particularly those in wearables and smart home devices, collect vast amounts of personal and sensitive data, including biometric information, location data, and behavioral patterns. Growing consumer awareness and stringent regulatory frameworks, such as GDPR and CCPA, necessitate robust data protection measures. Manufacturers face the challenge of implementing secure data encryption, ensuring transparent data usage policies, and preventing unauthorized access, as data breaches can severely erode consumer trust and lead to significant financial penalties, thereby dampening market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Manufacturing Costs | -1.8% | Global | Mid-term (2026-2031) |

| Supply Chain Disruptions and Geopolitical Instabilities | -1.5% | Global, especially APAC (manufacturing hub) | Short to Mid-term (2025-2029) |

| Data Privacy and Security Concerns | -1.2% | North America, Europe | Long-term (2028-2033) |

| Intense Competition and Price Pressure | -0.9% | Global, particularly emerging markets | Short to Mid-term (2025-2029) |

| Standardization Challenges and Interoperability Issues | -0.7% | Global | Mid-term (2027-2032) |

Consumer Electronic Sensor Market Opportunities Analysis

The burgeoning field of Augmented Reality (AR) and Virtual Reality (VR) presents a significant untapped opportunity for the Consumer Electronic Sensor market. AR/VR headsets and devices require highly precise and low-latency sensors, including accelerometers, gyroscopes, magnetometers, and specialized proximity and eye-tracking sensors, to enable immersive experiences and intuitive human-computer interaction. As these technologies mature and become more accessible to mainstream consumers, the demand for sophisticated sensors capable of real-time spatial awareness, gesture recognition, and physiological feedback will surge, creating new avenues for innovation and market expansion beyond current applications.

Another compelling opportunity lies in the continuous innovation within the smart home ecosystem, particularly with the integration of advanced environmental and security sensors. Beyond basic temperature and light sensing, there is growing potential for chemical sensors to detect air quality and pollutants, acoustic sensors for sound event recognition (e.g., breaking glass, smoke alarms), and sophisticated radar-based sensors for presence detection and fall monitoring in elderly care. These specialized sensors, often enhanced with AI for intelligent automation, can significantly enhance comfort, safety, and energy efficiency, driving a new wave of smart home device adoption.

The expansion of the automotive electronics segment, particularly for in-cabin sensing, offers a substantial growth opportunity. While ADAS (Advanced Driver-Assistance Systems) has traditionally been a major driver for automotive sensors, the focus is now shifting to consumer-centric applications within the vehicle cabin. This includes driver monitoring systems (DMS) utilizing cameras and biometric sensors to detect fatigue or distraction, as well as passenger comfort and entertainment systems incorporating gesture control sensors, haptic feedback sensors, and advanced climate control sensors. As vehicles evolve into personalized and intelligent environments, the integration of consumer-grade sensors for enhanced user experience and safety will become increasingly critical.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in AR/VR Devices | +2.0% | North America, Europe, East Asia (South Korea, Japan) | Mid to Long-term (2028-2033) |

| Advancements in Smart Home Automation and Environmental Monitoring | +1.8% | North America, Europe, China | Short to Mid-term (2025-2030) |

| Growth in Automotive In-Cabin Sensing and Infotainment Systems | +1.5% | Europe, North America, Japan, China | Mid-term (2026-2031) |

| Development of Next-Generation Wearables and Hearables | +1.3% | Global | Short to Mid-term (2025-2029) |

| Integration in Sports, Fitness, and Professional Training Devices | +0.8% | North America, Europe | Short to Mid-term (2025-2029) |

Consumer Electronic Sensor Market Challenges Impact Analysis

The complexity of integrating multiple sensor types into a single consumer electronic device, while maintaining optimal performance and managing power consumption, presents a significant technical challenge. As devices become more compact and feature-rich, designers face hurdles in space constraints, electromagnetic interference between sensors, and ensuring seamless data fusion from disparate sensor inputs. This integration complexity often leads to extended development cycles and increased engineering costs, potentially delaying product launches and impacting competitiveness in a fast-paced market.

Achieving a balance between high performance and cost-effectiveness remains a persistent challenge for sensor manufacturers. Consumers expect advanced functionalities and high accuracy from their electronic devices, but also demand competitive pricing. Innovating sophisticated sensors that deliver superior performance while being mass-producible at a low unit cost requires advanced manufacturing processes, economies of scale, and efficient material utilization. The inability to strike this balance can limit market penetration, especially in emerging economies where price sensitivity is higher, or in mass-market consumer devices where margins are tight.

Another critical challenge is ensuring robust data security and privacy in an increasingly interconnected environment. Consumer electronic sensors collect vast amounts of personal and sensitive data, making them attractive targets for cyberattacks and unauthorized access. Protecting this data from breaches and misuse is paramount to maintaining consumer trust and complying with evolving global data protection regulations. Implementing end-to-end encryption, secure data storage, and transparent data handling policies adds layers of complexity and cost to sensor design and deployment, but is essential for mitigating reputation damage and legal repercussions in the event of a security compromise.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Sensor Integration and Data Fusion | -1.6% | Global | Short to Mid-term (2025-2029) |

| Balancing Performance with Cost-Effectiveness | -1.3% | Global, particularly emerging markets | Mid-term (2026-2031) |

| Ensuring Robust Data Security and Privacy | -1.1% | North America, Europe | Long-term (2028-2033) |

| High Power Consumption in Advanced Sensors | -0.8% | Global | Short to Mid-term (2025-2029) |

| Rapid Technological Obsolescence | -0.6% | Global | Short-term (2025-2027) |

Consumer Electronic Sensor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Consumer Electronic Sensor market, covering market size, growth trends, key drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis by sensor type, application, and region, along with competitive landscape assessment of major market players. The report aims to furnish stakeholders with actionable insights to navigate the market dynamics and make informed strategic decisions for the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.0 Billion |

| Market Forecast in 2033 | USD 55.0 Billion |

| Growth Rate | 10.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Sensor Innovations, Advanced Sensing Technologies, Precision Sensor Solutions, Integrated Sensor Systems, Intelligent MicroSensors, Universal Sensor Corp, NextGen Sensorics, Dynamic Sensor Group, Opto-Electronic Devices, SmartSense Technologies, Future Sensing Solutions, Core Sensor Components, Elite Sensor Products, OmniSense Devices, Digital Sensing Inc., Quantum Sensors, Innovative Microdevices, Premier Sensor Co., Global Tech Sensors, Apex Sensor Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Consumer Electronic Sensor market is extensively segmented to provide a granular view of its diverse components and their respective growth trajectories. The primary segmentation includes analysis by Sensor Type, Application, and End-Use Industry, each offering unique insights into market dynamics. This detailed breakdown helps in understanding which specific sensor technologies are gaining traction, which consumer electronic categories are driving demand, and where the most significant opportunities lie for market participants across different industrial applications.

Segmentation by Sensor Type categorizes the market based on the physical phenomena they detect, such as motion, light, pressure, or biometric signals. This includes accelerometers, gyroscopes, magnetometers for motion sensing; image sensors, ambient light sensors, and proximity sensors for optical applications; and specialized sensors for temperature, humidity, and various chemical elements. The Application segmentation delves into the specific end-use products where these sensors are integrated, ranging from ubiquitous smartphones and tablets to the rapidly expanding wearable devices, smart home ecosystems, and emerging AR/VR platforms, highlighting the varied deployment scenarios.

Finally, the End-Use Industry segmentation provides an overview of the broader sectors that utilize consumer electronic sensors, encompassing the core Consumer Electronics sector, the increasingly sensor-laden Automotive industry (for in-cabin applications), the burgeoning Healthcare sector for personal wellness and monitoring, and the Sports & Fitness industry. This multi-faceted segmentation ensures a comprehensive understanding of market penetration, growth drivers within each category, and the interdependencies between sensor technology advancements and consumer product innovation, aiding in strategic planning and resource allocation for market stakeholders.

- By Sensor Type: Motion Sensors, Environmental Sensors, Optical Sensors, Biometric Sensors, Acoustic Sensors, Position Sensors, Chemical Sensors, Others.

- By Application: Smartphones & Tablets, Wearable Devices, Smart Home Devices, Gaming & Entertainment Devices, Automotive Electronics, Healthcare Devices, Augmented Reality (AR) & Virtual Reality (VR) Devices, Others.

- By End-Use Industry: Consumer Electronics, Automotive, Healthcare, Sports & Fitness, Others.

Regional Highlights

- North America: This region is characterized by early adoption of advanced consumer electronic devices and a strong emphasis on health and wellness technologies. High disposable incomes and significant R&D investments in IoT, AR/VR, and smart home solutions contribute to its substantial market share. The United States leads in innovation and consumer spending on high-end gadgets.

- Europe: Europe exhibits a robust market driven by increasing demand for smart home automation, connected vehicles, and stringent data privacy regulations fostering secure sensor integration. Countries like Germany and the UK are key players, with a focus on sophisticated sensor applications for energy efficiency and security.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by its massive consumer base, rapid urbanization, and a thriving manufacturing ecosystem. China, India, Japan, and South Korea are at the forefront of consumer electronics production and adoption. The region benefits from increasing disposable incomes and government initiatives promoting digitalization and smart city development.

- Latin America: This region shows promising growth, primarily due to increasing smartphone penetration and the nascent adoption of smart home devices. Brazil and Mexico are emerging markets with a growing middle class and expanding access to consumer electronics, driving demand for affordable yet functional sensor technologies.

- Middle East & Africa (MEA): The MEA market is gradually expanding, driven by infrastructure development, smart city initiatives in the GCC countries, and increasing internet connectivity. While smaller in market size compared to other regions, it offers significant untapped potential for basic and mid-range consumer electronic sensorapplications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Consumer Electronic Sensor Market.- Global Sensor Innovations

- Advanced Sensing Technologies

- Precision Sensor Solutions

- Integrated Sensor Systems

- Intelligent MicroSensors

- Universal Sensor Corp

- NextGen Sensorics

- Dynamic Sensor Group

- Opto-Electronic Devices

- SmartSense Technologies

- Future Sensing Solutions

- Core Sensor Components

- Elite Sensor Products

- OmniSense Devices

- Digital Sensing Inc.

- Quantum Sensors

- Innovative Microdevices

- Premier Sensor Co.

- Global Tech Sensors

- Apex Sensor Solutions

Frequently Asked Questions

What is the projected growth rate for the Consumer Electronic Sensor Market?

The Consumer Electronic Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, indicating robust expansion driven by increasing adoption of smart devices and IoT.

Which key trends are shaping the Consumer Electronic Sensor Market?

Key trends include miniaturization for compact integration, multi-sensor fusion, focus on ultra-low power consumption, AI-driven intelligent sensing, and the growing demand for biometric and health monitoring applications.

How does AI impact the Consumer Electronic Sensor Market?

AI integration enables intelligent data processing, predictive analytics, enhanced sensor accuracy, and personalized user experiences, transforming sensors into more adaptive and responsive components within consumer electronics.

What are the main applications of consumer electronic sensors?

Consumer electronic sensors are predominantly used in smartphones, wearables, smart home devices, gaming and entertainment systems, automotive electronics (in-cabin sensing), healthcare devices, and emerging Augmented Reality (AR) & Virtual Reality (VR) technologies.

Which regions are key contributors to the Consumer Electronic Sensor Market?

North America and Europe are significant markets due to technological adoption and R&D. Asia Pacific, particularly China and India, is expected to be the fastest-growing region owing to its large consumer base and strong manufacturing capabilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted