Polyvinyl Chloride Market

Polyvinyl Chloride Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700113 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

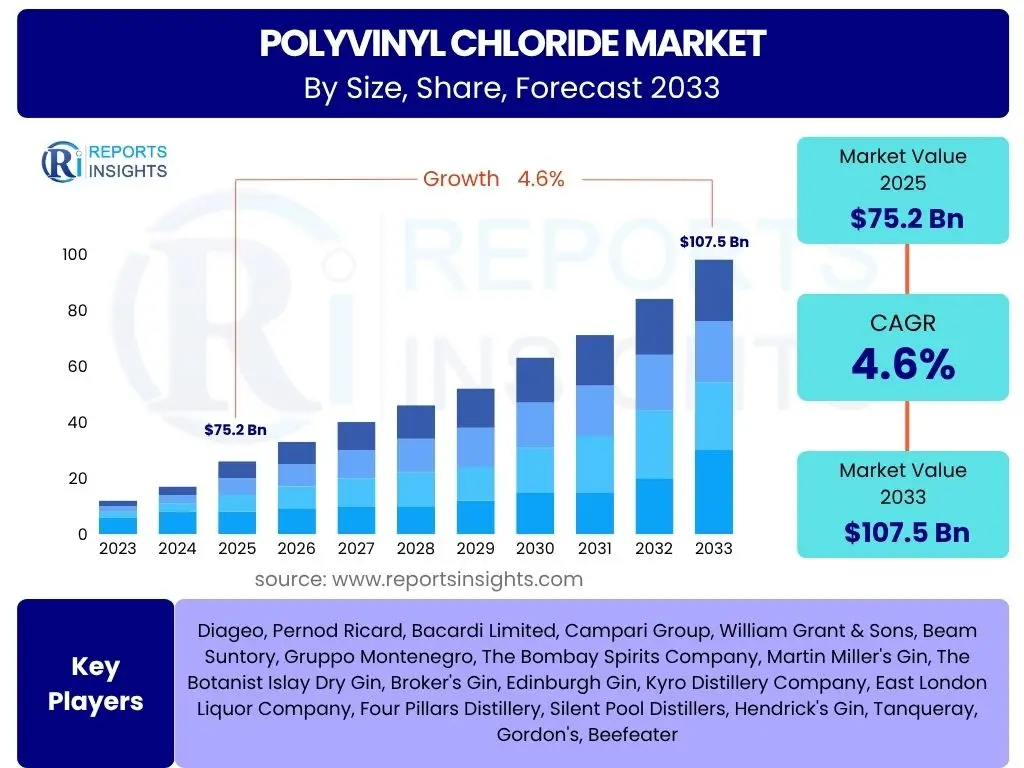

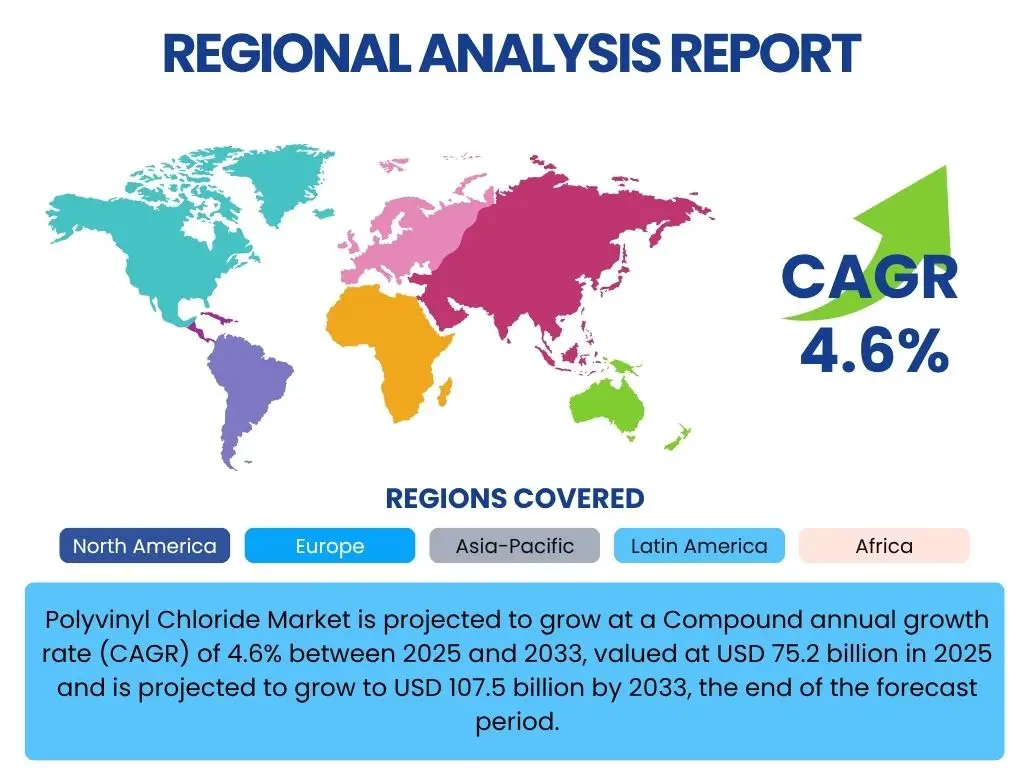

Polyvinyl Chloride Market is projected to grow at a Compound annual growth rate (CAGR) of 4.6% between 2025 and 2033, current valued at USD 75.2 billion in 2025 and is projected to grow to USD 107.5 billion by 2033, the end of the forecast period.

Key Polyvinyl Chloride Market Trends & Insights

The Polyvinyl Chloride (PVC) market is experiencing dynamic shifts driven by evolving industry demands and technological advancements. Key trends include a significant push towards sustainable PVC solutions, driven by environmental regulations and consumer preferences. Concurrently, the robust growth in the construction and infrastructure sectors globally continues to be a primary demand driver for PVC products like pipes, fittings, and window profiles. Innovations in PVC compounding and manufacturing processes are enabling the creation of more durable, flexible, and high-performance materials, expanding its application across diverse industries. Furthermore, the increasing adoption of smart city initiatives and renewable energy projects is creating new avenues for specialized PVC formulations.

- Increasing demand for sustainable and recycled PVC.

- Robust growth in construction and infrastructure development.

- Technological advancements in PVC compounding for enhanced performance.

- Rising adoption of PVC in niche and specialized applications.

- Shift towards digitalization in manufacturing and supply chain management.

AI Impact Analysis on Polyvinyl Chloride

Artificial Intelligence (AI) is set to significantly transform various facets of the Polyvinyl Chloride (PVC) market, from raw material sourcing to end-product distribution. AI-driven predictive analytics can optimize supply chain logistics, forecasting demand fluctuations more accurately and mitigating risks associated with volatile raw material prices. In manufacturing, AI applications can enhance process efficiency, enable predictive maintenance for machinery, and improve quality control through real-time data analysis, leading to reduced waste and improved operational costs. Furthermore, AI can accelerate research and development efforts by simulating new polymer formulations and material properties, paving the way for innovative PVC products with superior performance characteristics.

- Enhanced supply chain optimization through predictive analytics.

- Improved manufacturing efficiency and quality control via AI-driven process automation.

- Accelerated R&D for novel PVC formulations and applications.

- Optimized energy consumption and waste reduction in production.

- Smarter demand forecasting leading to better inventory management.

Key Takeaways Polyvinyl Chloride Market Size & Forecast

- The Polyvinyl Chloride market is projected to reach a valuation of USD 75.2 billion in 2025.

- Expected to grow at a Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period from 2025 to 2033.

- Forecasted to attain a market size of USD 107.5 billion by the year 2033.

- Growth is significantly driven by robust demand from the construction, automotive, and packaging sectors.

- Emerging economies in Asia Pacific and Latin America are anticipated to be key contributors to market expansion.

- Technological advancements in PVC production and sustainable product development are shaping future growth trajectories.

Polyvinyl Chloride Market Drivers Analysis

The Polyvinyl Chloride (PVC) market is propelled by a confluence of robust drivers, primarily rooted in its versatile applications and cost-effectiveness across numerous industries. A major impetus comes from the booming global construction and infrastructure development, particularly in developing economies, where PVC is indispensable for pipes, fittings, window profiles, and flooring. Its durability, light weight, and chemical resistance make it an ideal material for modern urban development projects. Furthermore, the expanding automotive and packaging sectors are increasingly adopting PVC for various components due to its performance attributes and economic viability.

Beyond traditional uses, the demand for PVC is also bolstered by its application in the electrical and electronics industry for cable insulation and in the healthcare sector for medical devices. Continuous innovation leading to specialized PVC grades, such as those with enhanced fire resistance or improved flexibility, further broadens its appeal and market penetration. The inherent properties of PVC, coupled with its adaptability to various manufacturing processes, ensure its sustained relevance and growth trajectory in a wide array of end-use sectors, contributing positively to its market expansion over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Robust Growth in Construction and Infrastructure Development | +1.5% | Asia Pacific, Middle East & Africa, Latin America | Short to Long-term |

| Increasing Demand for Pipes, Fittings, and Profiles | +1.2% | Global, particularly emerging economies | Short to Mid-term |

| Growth in Automotive and Packaging Industries | +0.8% | North America, Europe, Asia Pacific | Mid-term |

| Advancements in PVC Compounding and Processing Technologies | +0.6% | Global | Mid to Long-term |

| Cost-Effectiveness and Versatility of PVC | +0.5% | Global | Consistent, Long-term |

Polyvinyl Chloride Market Restraints Analysis

Despite its widespread utility, the Polyvinyl Chloride (PVC) market faces notable restraints that could temper its growth trajectory. Paramount among these are growing environmental concerns and stringent regulations surrounding plastic waste and the lifecycle management of PVC. Debates over the health and environmental impact of certain additives, such as phthalates, in PVC formulations, and challenges in PVC recycling, particularly for mixed plastic waste, continue to pose significant hurdles. These concerns often lead to public scrutiny and regulatory pressures for alternative materials or more environmentally friendly production methods.

Furthermore, the PVC market is susceptible to the volatility of raw material prices, particularly crude oil and natural gas, which are integral to ethylene and chlorine production. Fluctuations in these feedstock costs directly impact manufacturing expenses and can erode profit margins for PVC producers. Competition from substitute materials like polyethylene (PE), polypropylene (PP), and alternative metals, which may offer perceived environmental advantages or specific performance benefits for certain applications, also acts as a restraint. Economic downturns or slowdowns in key end-use industries like construction can further dampen demand, collectively posing challenges to the market's otherwise robust growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Public Scrutiny | -0.9% | Europe, North America, parts of Asia Pacific | Mid to Long-term |

| Volatile Raw Material Prices (Ethylene, Chlorine) | -0.7% | Global | Short to Mid-term |

| Competition from Substitute Materials | -0.5% | Global | Mid to Long-term |

| Challenges in PVC Recycling and Waste Management | -0.4% | Europe, North America | Long-term |

Polyvinyl Chloride Market Opportunities Analysis

The Polyvinyl Chloride (PVC) market is poised for significant opportunities driven by innovative applications, sustainability initiatives, and burgeoning demand in underserved markets. One prominent opportunity lies in the development and adoption of sustainable PVC solutions, including bio-attributed PVC, mechanically recycled PVC, and chemically recycled PVC. As industries increasingly prioritize circular economy principles and greener materials, investments in advanced recycling technologies and eco-friendly additives for PVC can open up substantial new market segments and improve public perception.

Furthermore, rapid urbanization and industrialization in emerging economies, particularly across Asia Pacific and Latin America, present vast untapped potential for PVC products in infrastructure, housing, and industrial applications. Niche applications in specialized industries such as medical devices, agriculture (e.g., irrigation pipes), and renewable energy infrastructure (e.g., cable insulation for solar panels) are also expanding, creating new avenues for high-performance and customized PVC formulations. The ongoing research and development into new PVC compounds with enhanced properties like improved heat resistance, fire retardancy, and UV stability will further broaden the material's utility and competitive advantage against alternatives, fostering long-term growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Sustainable and Recycled PVC | +1.0% | Europe, North America, Asia Pacific | Mid to Long-term |

| Untapped Potential in Emerging Economies for Infrastructure and Construction | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Short to Long-term |

| Expansion into Niche and High-Performance Applications | +0.7% | Global | Mid-term |

| Technological Innovation in PVC Compounding and Additives | +0.6% | Global | Mid to Long-term |

Polyvinyl Chloride Market Challenges Impact Analysis

The Polyvinyl Chloride (PVC) market faces several critical challenges that demand strategic responses from industry players. One significant challenge stems from the persistent negative public perception regarding PVC's environmental footprint, primarily due to concerns about its production processes, use of additives, and end-of-life disposal. This perception, often fueled by advocacy groups, can lead to reduced consumer preference and increased regulatory scrutiny, impacting market demand and growth potential. Overcoming this requires substantial investment in transparent communication, sustainable innovation, and robust recycling infrastructures.

Another challenge is navigating the volatile global economic landscape, which can directly affect construction and manufacturing output, the primary consumers of PVC. Supply chain disruptions, such as those experienced globally in recent years, also pose a significant threat, leading to raw material shortages, increased logistics costs, and production delays. Furthermore, intense competition from alternative materials, often positioned as more eco-friendly or performance-superior for specific applications, pressures PVC manufacturers to continuously innovate and demonstrate the material's value proposition. Managing energy costs, especially for energy-intensive PVC production, further adds to the operational challenges, influencing overall profitability and competitiveness within the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Public Perception and Environmental Stigma | -0.8% | Europe, North America | Long-term |

| Supply Chain Disruptions and Logistics Costs | -0.6% | Global | Short to Mid-term |

| Intensifying Competition from Alternative Materials | -0.5% | Global | Mid-term |

| Fluctuating Energy Costs for Production | -0.4% | Global | Short to Mid-term |

Polyvinyl Chloride Market - Updated Report Scope

The updated report scope for the Polyvinyl Chloride market provides a comprehensive analytical framework, offering in-depth insights into market dynamics, segmentation, competitive landscape, and future projections. This meticulously compiled study covers historical data alongside forward-looking forecasts, enabling stakeholders to make informed strategic decisions. It delves into the granular aspects of market segments, regional performance, and the influence of key trends, drivers, and challenges, presenting a holistic view of the market's current state and its potential trajectory over the defined forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 75.2 billion |

| Market Forecast in 2033 | USD 107.5 billion |

| Growth Rate | 4.6% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | OxyVinyls, Shin-Etsu Chemical, Ineos Group, Formosa Plastics Corporation, LG Chem, Westlake Chemical, Kem One, Wanhua Chemical Group, Xinjiang Zhongtai Chemical, Hanwha Solutions, Sekisui Chemical, Reliance Industries Limited, Axiall Corporation, Shintech Inc, China National Chemical Corporation (ChemChina), Kaneka Corporation, Mitsui Chemicals, Vynova Group, Mexichem (Orbia), Georgia Gulf Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyvinyl Chloride market is extensively segmented based on its fundamental characteristics, diverse applications, and the broad range of industries it serves. This granular segmentation provides a detailed understanding of market dynamics, growth drivers, and opportunities within each specific category, enabling targeted strategic planning for market participants. The primary segments include type, application, and end-use industry, each broken down into further sub-segments reflecting the versatility and specific demands for PVC across the global economy.

- By Type:

- Rigid PVC: Dominates the market due to its widespread use in pipes, window frames, and construction profiles, known for its durability and stiffness.

- Flexible PVC: Characterized by its elasticity, used in applications like cables, flooring, films, and medical tubing, achieved through plasticizers.

- Chlorinated PVC (CPVC): Offers enhanced heat and chemical resistance compared to standard PVC, making it suitable for hot water piping systems and industrial fluid handling.

- By Application:

- Pipes & Fittings: The largest application segment, critical for water supply, sewage, and drainage systems in residential, commercial, and agricultural sectors.

- Profiles & Tubing: Includes window and door profiles, conduits, and various industrial tubes, valued for its weather resistance and insulation properties.

- Films & Sheets: Used in packaging, roofing membranes, and various industrial covers, offering flexibility and protective barriers.

- Wires & Cables: Essential for electrical insulation due to its excellent dielectric properties and flame retardancy.

- Bottles: Utilized for packaging edible oils, mineral water, and certain chemicals, chosen for clarity and barrier properties.

- Others: Encompasses a wide array of uses such as flooring, medical devices (e.g., blood bags, IV sets), artificial leather, and consumer goods.

- By End-use Industry:

- Construction: The largest consumer of PVC, driven by housing, commercial buildings, and infrastructure projects, utilizing PVC for pipes, windows, doors, and flooring.

- Automotive: Employed in interior components, underbody coatings, and wire harnesses due to its durability and flame retardancy.

- Electrical & Electronics: Primarily for wire and cable insulation, conduits, and electronic component housings.

- Packaging: Used in various forms like films, rigid sheets, and bottles for food, non-food, and medical packaging.

- Healthcare: Critical for sterile medical devices, blood bags, and tubing due to its biocompatibility and sterilizability.

- Consumer Goods: Found in footwear, toys, garden hoses, and sporting goods, leveraging its versatility and cost-effectiveness.

- Agriculture: Essential for irrigation pipes, drainage systems, and greenhouse coverings due to its durability and resistance to chemicals and weathering.

Regional Highlights

The Polyvinyl Chloride market exhibits distinct growth patterns and demands across various global regions, driven by regional economic conditions, industrial development, and regulatory landscapes. Understanding these regional dynamics is crucial for strategic market penetration and investment decisions. Each region contributes uniquely to the overall market growth, with some serving as major production hubs and others as significant consumption centers.

- Asia Pacific (APAC): The leading and fastest-growing region in the Polyvinyl Chloride market. This dominance is primarily driven by rapid urbanization, extensive infrastructure development projects, and a booming construction sector in countries like China, India, and Southeast Asian nations. The region also benefits from a large manufacturing base and growing demand from packaging, automotive, and electrical industries. Abundant availability of raw materials and lower labor costs further bolster production capabilities.

- North America: A mature market characterized by steady demand from the construction, automotive, and healthcare sectors. The region focuses on high-performance PVC applications and is increasingly investing in sustainable PVC solutions and recycling technologies. Innovations in building codes and a strong emphasis on durable, long-lasting materials support continued, albeit slower, growth.

- Europe: This region is characterized by stringent environmental regulations and a strong emphasis on sustainability and circular economy principles. While traditional construction demand remains steady, the market is increasingly shifting towards recycled PVC and bio-attributed PVC products. Innovation in PVC compounding for specialized applications, coupled with a focus on energy efficiency in buildings, supports its market trajectory. Germany, France, and the UK are key contributors.

- Latin America: Showing significant growth potential due to increasing investments in infrastructure development, housing projects, and industrial expansion, particularly in countries like Brazil, Mexico, and Argentina. The demand for PVC pipes, profiles, and films is consistently rising, driven by economic development and urbanization.

- Middle East and Africa (MEA): Emerging as a promising market due to large-scale construction projects, oil and gas infrastructure development, and growing industrialization. Countries in the GCC (Gulf Cooperation Council) region are investing heavily in new cities and facilities, driving demand for PVC in various applications including pipes, window profiles, and cables.

Top Key Players:

The market research report covers the analysis of key stake holders of the Polyvinyl Chloride Market. Some of the leading players profiled in the report include -- OxyVinyls

- Shin-Etsu Chemical

- Ineos Group

- Formosa Plastics Corporation

- LG Chem

- Westlake Chemical

- Kem One

- Wanhua Chemical Group

- Xinjiang Zhongtai Chemical

- Hanwha Solutions

- Sekisui Chemical

- Reliance Industries Limited

- Axiall Corporation

- Shintech Inc

- China National Chemical Corporation (ChemChina)

- Kaneka Corporation

- Mitsui Chemicals

- Vynova Group

- Orbia (formerly Mexichem)

- Georgia Gulf Corporation

Frequently Asked Questions:

What is Polyvinyl Chloride (PVC) and its primary uses?

Polyvinyl Chloride (PVC) is a widely used synthetic plastic polymer known for its versatility, durability, and cost-effectiveness. It is primarily used in the construction sector for manufacturing pipes, fittings, window profiles, and flooring. Other significant applications include electrical wire and cable insulation, packaging films and sheets, automotive components, and medical devices due to its chemical resistance and long lifespan.

What factors are driving the growth of the Polyvinyl Chloride market?

The growth of the Polyvinyl Chloride market is primarily driven by the robust expansion of the global construction and infrastructure sector, particularly in developing economies. Increasing demand for PVC in pipes, fittings, and profiles for water management and building applications is a key factor. Additionally, growth in the automotive, electrical & electronics, and packaging industries, coupled with PVC's inherent cost-effectiveness and versatile properties, significantly contribute to its market expansion.

What are the main environmental concerns associated with PVC?

The main environmental concerns associated with PVC include issues related to its production, which involves chlorine chemistry, and its end-of-life management. Historically, concerns have been raised about the use of certain additives like phthalates and lead stabilizers, though many of these have been phased out or replaced. Challenges in mechanical recycling for certain PVC applications and the potential for dioxin emissions during uncontrolled incineration are also points of concern, prompting the industry to invest in sustainable solutions and advanced recycling technologies.

How is Polyvinyl Chloride recycled, and what are the advancements?

Polyvinyl Chloride can be recycled through mechanical and chemical processes. Mechanical recycling involves sorting, cleaning, shredding, and melting PVC waste into new products, commonly used for rigid PVC applications like pipes and window profiles. Advancements include improved sorting technologies, removal of contaminants, and the development of chemical recycling methods that break down PVC into its constituent monomers or other valuable chemicals, offering a more effective solution for complex or mixed PVC waste streams and enabling a circular economy approach.

What is the future outlook for the Polyvinyl Chloride market?

The future outlook for the Polyvinyl Chloride market is positive, driven by continued demand from the construction sector, especially in emerging economies, and the material's adaptability to new applications. Key trends shaping its future include a strong emphasis on sustainability, with increasing adoption of recycled and bio-attributed PVC. Innovation in PVC compounding to enhance performance properties and address environmental concerns, alongside digitalization in manufacturing and supply chain management, will further support its growth and relevance in diverse industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted