Polyvinylidene Chloride Market

Polyvinylidene Chloride Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705497 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

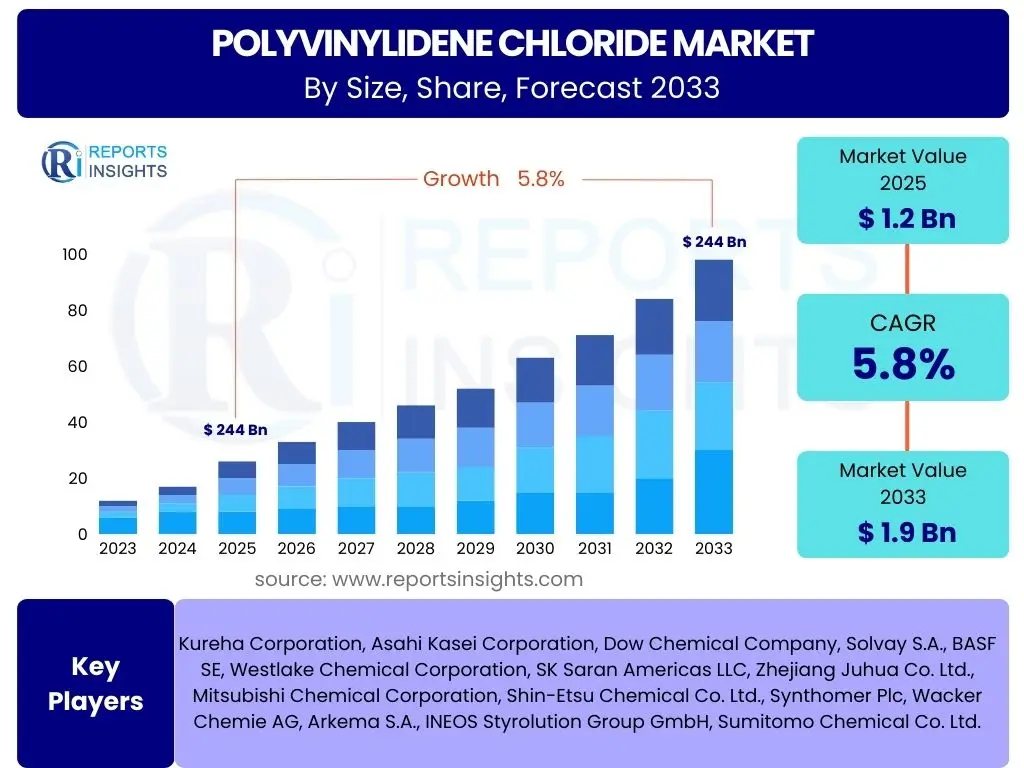

Polyvinylidene Chloride Market Size

According to Reports Insights Consulting Pvt Ltd, The Polyvinylidene Chloride Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 1.2 billion in 2025 and is projected to reach USD 1.9 billion by the end of the forecast period in 2033. This growth is primarily driven by the increasing demand for high-barrier packaging solutions across various industries, including food and beverage, pharmaceuticals, and consumer goods.

The exceptional barrier properties of Polyvinylidene Chloride (PVDC) against moisture, oxygen, and aroma make it an indispensable material for extending product shelf-life and maintaining quality. Global population growth, rising disposable incomes, and the expansion of the e-commerce sector further contribute to the escalating need for robust and efficient packaging. Manufacturers are increasingly adopting PVDC due to its performance benefits, even amidst evolving regulatory landscapes and increasing focus on sustainable material alternatives. This consistent demand, coupled with ongoing innovations in PVDC formulations, underpins the positive market trajectory.

Key Polyvinylidene Chloride Market Trends & Insights

User inquiries frequently focus on the evolving landscape of the Polyvinylidene Chloride market, seeking to understand the significant shifts and emerging patterns. Common questions revolve around the adoption of sustainable practices, the impact of alternative barrier materials, the rise of specialized applications, and the influence of regional economic developments. Analysis indicates a strong inclination towards sustainable solutions, driven by both consumer preference and regulatory pressures, compelling manufacturers to explore eco-friendlier PVDC variants or recycling initiatives. Furthermore, advancements in co-extrusion and lamination technologies are expanding PVDC's application versatility, allowing for its integration into more complex multi-layer structures.

Another key area of interest concerns the competitive dynamics posed by substitutes like EVOH and metallized films, prompting PVDC producers to highlight its superior barrier performance and chemical resistance in specific niches. The market is also observing a trend towards miniaturization and single-serve packaging, which inherently demands high-performance barrier films like PVDC to preserve product integrity. Lastly, the expansion of pharmaceutical and medical sectors, particularly in emerging economies, is creating new avenues for PVDC, given its inertness and reliability in protecting sensitive products. These trends collectively shape the strategic decisions of market participants and dictate the direction of research and development efforts.

- Emphasis on sustainable and recyclable PVDC solutions.

- Increased adoption of PVDC in pharmaceutical and medical packaging due to stringent barrier requirements.

- Growing demand for multi-layer films incorporating PVDC for enhanced barrier properties.

- Development of thinner, high-performance PVDC films to reduce material consumption.

- Strategic partnerships and collaborations among market players to expand reach and innovate.

- Shift towards specialized and customized barrier packaging for niche applications.

AI Impact Analysis on Polyvinylidene Chloride

User queries regarding the impact of Artificial Intelligence (AI) on the Polyvinylidene Chloride market often center on its potential to optimize production processes, enhance material properties through advanced simulations, and streamline supply chain management. There is significant interest in how AI can contribute to predictive maintenance for manufacturing equipment, thereby reducing downtime and improving operational efficiency. Furthermore, users are keen to understand AI's role in accelerating research and development, particularly in designing new PVDC formulations with improved barrier performance or more sustainable profiles, by analyzing vast datasets of chemical properties and experimental results.

AI's influence extends to quality control, where machine learning algorithms can detect subtle defects in PVDC films during production more accurately and rapidly than traditional methods, ensuring consistent product quality. In the supply chain, AI-driven analytics can forecast demand more precisely, optimize inventory levels, and manage logistics, leading to reduced waste and improved cost-effectiveness. While the direct application of AI to PVDC's chemical synthesis might be nascent, its indirect impact on manufacturing, quality assurance, and market analysis is poised to drive significant efficiencies and foster innovation across the value chain, leading to more competitive pricing and tailored product offerings.

- Optimization of PVDC manufacturing processes through AI-driven predictive analytics.

- Enhanced quality control and defect detection in PVDC films using machine vision and AI algorithms.

- Accelerated R&D for novel PVDC formulations and sustainable alternatives via AI-powered simulations.

- Improved supply chain efficiency and demand forecasting through AI-driven data analysis.

- Development of smart packaging solutions integrating PVDC with AI-enabled sensors for real-time monitoring.

Key Takeaways Polyvinylidene Chloride Market Size & Forecast

Analysis of common user questions concerning the Polyvinylidene Chloride market size and forecast reveals a strong interest in understanding the primary growth drivers, the significance of packaging innovations, and the regional dynamics shaping market expansion. Users frequently inquire about which end-use industries will contribute most significantly to growth and how environmental regulations might influence future market trajectories. The consensus points to sustained demand from the food and pharmaceutical packaging sectors as critical growth catalysts, underpinned by PVDC's unparalleled barrier properties essential for product preservation and safety.

A key insight is the strategic shift towards balancing performance with sustainability, leading to increased investment in recycling technologies and bio-based alternatives, even for traditional materials like PVDC. Regional economic development, particularly in Asia Pacific, is anticipated to fuel substantial market expansion due to burgeoning populations and rising consumer spending. The market's resilience in the face of competitive materials is also a notable takeaway, indicating PVDC's irreplaceable role in specific high-barrier applications. These insights collectively underscore a market poised for steady growth, driven by fundamental consumer needs and technological advancements.

- Sustained demand from food, pharmaceutical, and medical packaging sectors drives market growth.

- Asia Pacific is projected to be the fastest-growing region due to industrial expansion and urbanization.

- Innovations in sustainable PVDC solutions and enhanced barrier performance are crucial for future competitiveness.

- Regulatory landscape and environmental concerns will increasingly shape product development and market strategies.

- PVDC's superior barrier properties ensure its continued relevance despite the emergence of alternative materials.

Polyvinylidene Chloride Market Drivers Analysis

The Polyvinylidene Chloride (PVDC) market is significantly propelled by its exceptional barrier properties against moisture, oxygen, and flavor. This makes it a preferred material in industries where product integrity and shelf-life extension are paramount. The continuous expansion of the food and beverage industry, particularly the demand for processed and packaged foods, directly contributes to the increased consumption of PVDC for various packaging applications. Additionally, the pharmaceutical sector's stringent requirements for protecting sensitive medications from external contaminants further bolster the demand for high-barrier PVDC films.

Another crucial driver is the growth of the healthcare sector globally, including the rising need for sterile medical devices and blister packaging. PVDC's chemical resistance and non-reactivity with diverse substances make it an ideal choice for these critical applications. Furthermore, the burgeoning e-commerce trend necessitates robust and protective packaging solutions to ensure products reach consumers intact and fresh, thereby escalating the demand for high-performance barrier materials like PVDC. These combined factors create a strong foundation for the sustained growth of the PVDC market over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for high-barrier packaging | +1.8% | Global, particularly APAC & Europe | Short to Medium-term (2025-2030) |

| Growth in pharmaceutical & medical industries | +1.5% | North America, Europe, China | Medium to Long-term (2027-2033) |

| Expansion of processed food and beverage sector | +1.2% | Emerging Economies (India, Brazil, Southeast Asia) | Short to Medium-term (2025-2030) |

| Rise in e-commerce and logistics requirements | +0.9% | Global, especially urban areas | Short-term (2025-2028) |

| Technological advancements in co-extrusion and lamination | +0.4% | Developed Markets (US, Germany, Japan) | Medium-term (2026-2031) |

Polyvinylidene Chloride Market Restraints Analysis

Despite its superior properties, the Polyvinylidene Chloride (PVDC) market faces certain restraints that could temper its growth trajectory. Environmental concerns regarding the disposal and recyclability of chlorine-containing plastics represent a significant challenge. The presence of chlorine atoms in PVDC can complicate recycling processes and raise questions about end-of-life disposal, leading to scrutiny from environmental agencies and consumer groups. This has driven a push towards more easily recyclable or bio-degradable alternatives in various packaging applications, impacting PVDC's market share in certain segments.

Another major restraint is the increasing competition from alternative barrier materials, such as Ethylene Vinyl Alcohol (EVOH), Nylon, and various metallized films. While PVDC often boasts superior overall barrier performance, these alternatives can sometimes offer cost advantages, easier processability, or better environmental profiles for specific applications, thus presenting a competitive threat. Additionally, the volatility of raw material prices and the energy-intensive nature of PVDC production can influence manufacturing costs and final product pricing, potentially limiting its adoption in cost-sensitive markets. These factors necessitate continuous innovation and strategic positioning for PVDC manufacturers to maintain market relevance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental concerns & regulatory scrutiny | -1.3% | Europe, North America | Medium to Long-term (2026-2033) |

| Competition from alternative barrier materials | -1.0% | Global | Short to Medium-term (2025-2030) |

| Volatile raw material prices (vinyl chloride monomer) | -0.8% | Global | Short-term (2025-2027) |

| High production costs and energy consumption | -0.5% | Global | Medium-term (2026-2031) |

| Limited recyclability challenges for existing PVDC | -0.3% | Developed economies with strict waste management | Medium to Long-term (2027-2033) |

Polyvinylidene Chloride Market Opportunities Analysis

The Polyvinylidene Chloride (PVDC) market is presented with several promising opportunities that can fuel its expansion. One significant avenue lies in the development of more sustainable and easily recyclable grades of PVDC. As environmental regulations become stricter and consumer demand for eco-friendly products intensifies, innovations in bio-based PVDC or PVDC formulations compatible with existing recycling streams could unlock new market segments and improve public perception. Research into depolymerization or chemical recycling of PVDC could also transform its sustainability profile, presenting a significant competitive advantage.

Another key opportunity is the expansion into emerging markets, particularly in Asia Pacific, Latin America, and Africa. These regions are experiencing rapid urbanization, increasing disposable incomes, and a growing demand for packaged goods, pharmaceuticals, and medical supplies. Local manufacturing and distribution networks, coupled with tailored product offerings, can help PVDC manufacturers capitalize on these burgeoning markets. Furthermore, the ongoing advancements in food preservation technologies and smart packaging solutions, which often require superior barrier properties, open up new specialized applications for PVDC beyond traditional uses. These opportunities, if strategically pursued, can ensure long-term growth for the PVDC market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of sustainable & recyclable PVDC grades | +1.5% | Global, especially Europe & North America | Medium to Long-term (2027-2033) |

| Expansion into emerging economies (APAC, LATAM, MEA) | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

| Increasing demand for advanced food preservation solutions | +0.9% | Global | Short to Medium-term (2025-2030) |

| Growth in specialized medical & healthcare applications | +0.7% | Developed & rapidly developing healthcare markets | Medium-term (2026-2031) |

| Innovation in multi-layer and composite film structures | +0.5% | Global, driven by packaging converters | Medium-term (2026-2031) |

Polyvinylidene Chloride Market Challenges Impact Analysis

The Polyvinylidene Chloride (PVDC) market faces several challenges that require strategic responses from industry players. One significant challenge is the ongoing pressure from environmental regulations and public perception regarding the use of plastics containing chlorine. While PVDC offers superior performance, its chlorine content raises concerns about incineration by-products and complicates mechanical recycling, pushing industries to seek out "chlorine-free" or more easily recyclable alternatives. This mandates continuous investment in R&D for greener PVDC solutions or clear communication about its environmental benefits in specific high-value applications.

Another challenge stems from the intense competition from a diverse range of alternative barrier materials. Innovations in materials like EVOH, ceramic-coated films, and various bioplastics are constantly emerging, each offering specific advantages in terms of cost, processability, or environmental profile. PVDC manufacturers must consistently demonstrate the unique value proposition of their product, particularly its superior overall barrier performance and chemical resistance, to retain market share. Furthermore, global supply chain disruptions, energy price fluctuations, and geopolitical tensions can impact the availability and cost of raw materials, posing logistical and economic challenges to PVDC production and distribution. Navigating these complexities will be crucial for sustained market success.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict environmental regulations & public image concerns | -1.0% | Europe, North America, Japan | Medium to Long-term (2026-2033) |

| Intense competition from substitute barrier materials | -0.9% | Global | Short to Medium-term (2025-2030) |

| Fluctuations in raw material prices & supply chain volatility | -0.7% | Global | Short-term (2025-2027) |

| High entry barriers for new market players (capital intensive) | -0.4% | Global | Long-term (2028-2033) |

| Limited availability of specialized processing equipment | -0.2% | Developing Regions | Short to Medium-term (2025-2030) |

Polyvinylidene Chloride Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Polyvinylidene Chloride (PVDC) market, offering a detailed overview of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It aims to furnish stakeholders with actionable insights to navigate the evolving market landscape, identify growth avenues, and formulate informed business strategies. The report meticulously covers historical data, current market dynamics, and future projections, incorporating the impact of emerging technologies and sustainability initiatives on the PVDC industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 1.9 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kureha Corporation, Asahi Kasei Corporation, Dow Chemical Company, Solvay S.A., BASF SE, Westlake Chemical Corporation, SK Saran Americas LLC, Zhejiang Juhua Co. Ltd., Mitsubishi Chemical Corporation, Shin-Etsu Chemical Co. Ltd., Synthomer Plc, Wacker Chemie AG, Arkema S.A., INEOS Styrolution Group GmbH, Sumitomo Chemical Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyvinylidene Chloride (PVDC) market is comprehensively segmented to provide granular insights into its diverse applications and product types. This segmentation helps to delineate specific market dynamics, identify high-growth areas, and understand the varying demands from different end-use industries. The market is primarily categorized by type, which includes PVDC Copolymers and PVDC Homopolymers, reflecting the different chemical compositions and performance characteristics tailored for specific needs.

Further segmentation by application highlights the dominant roles of PVDC in food packaging, pharmaceutical packaging, and medical devices, where its superior barrier properties are indispensable. Additionally, its use extends to consumer goods packaging, industrial packaging, and various other specialized applications. The end-use industry segmentation further refines the analysis, covering critical sectors such as Food & Beverage, Pharmaceutical, Healthcare, Personal Care & Cosmetics, and Chemical & Industrial, illustrating the broad applicability and integral nature of PVDC across a multitude of commercial verticals. This detailed breakdown enables a precise assessment of market potential within each segment.

- By Type:

- PVDC Copolymers

- PVDC Homopolymers

- By Application:

- Food Packaging

- Pharmaceutical Packaging

- Medical Devices

- Consumer Goods Packaging

- Industrial Packaging

- Others

- By End-Use Industry:

- Food & Beverage

- Pharmaceutical

- Healthcare

- Personal Care & Cosmetics

- Chemical & Industrial

- Others

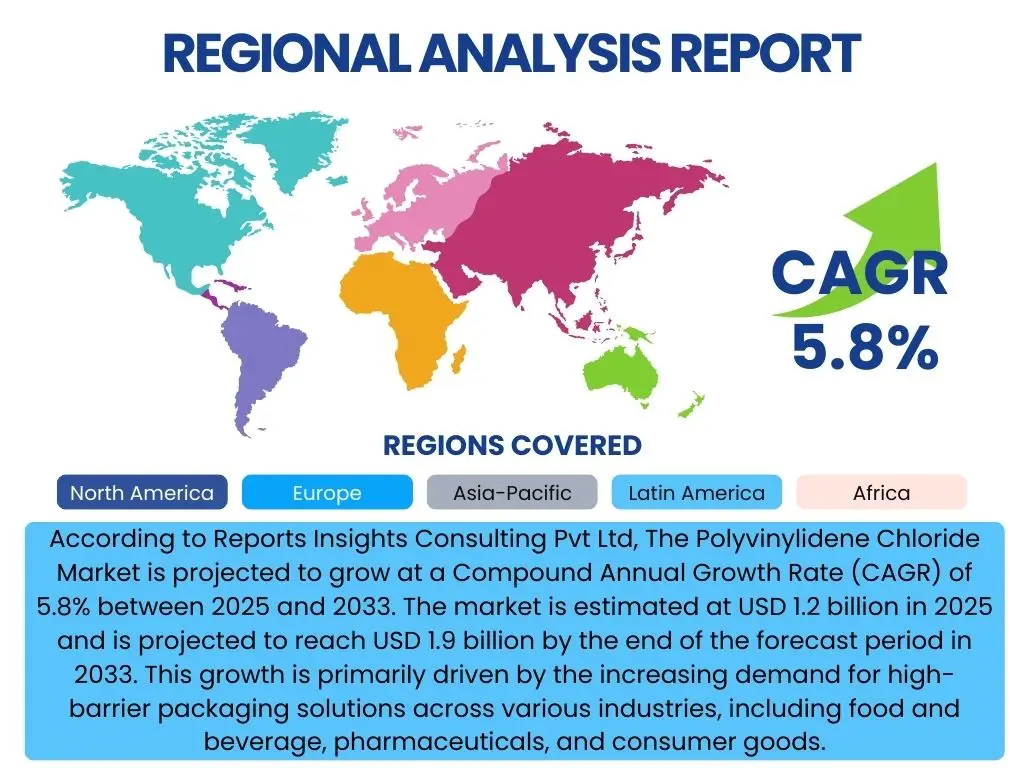

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by rapid industrialization, increasing population, rising disposable incomes, and the booming food processing and pharmaceutical industries in countries like China, India, and Southeast Asian nations. The expansion of e-commerce also significantly contributes to the demand for efficient packaging solutions.

- North America: A mature market characterized by stringent regulatory standards for food and pharmaceutical packaging. The region exhibits steady growth, primarily due to advanced healthcare infrastructure, high demand for packaged and convenience foods, and continuous innovation in packaging technologies.

- Europe: This region holds a significant share, fueled by a strong pharmaceutical sector, stringent food safety regulations, and a growing emphasis on sustainable packaging solutions. Countries like Germany, France, and the UK are key contributors, focusing on high-performance barrier films and exploring greener alternatives.

- Latin America: Demonstrates emerging growth potential, influenced by expanding food and beverage industries, improving healthcare access, and increasing urbanization. Brazil and Mexico are leading markets in this region, driven by a growing middle class and evolving consumer preferences for packaged goods.

- Middle East and Africa (MEA): Showing nascent growth, primarily in the food and pharmaceutical sectors, particularly in countries like Saudi Arabia, UAE, and South Africa. Investments in infrastructure and manufacturing capabilities are expected to boost the demand for PVDC in protective packaging solutions over the forecast period.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyvinylidene Chloride Market.- Kureha Corporation

- Asahi Kasei Corporation

- Dow Chemical Company

- Solvay S.A.

- BASF SE

- Westlake Chemical Corporation

- SK Saran Americas LLC

- Zhejiang Juhua Co. Ltd.

- Mitsubishi Chemical Corporation

- Shin-Etsu Chemical Co. Ltd.

- Synthomer Plc

- Wacker Chemie AG

- Arkema S.A.

- INEOS Styrolution Group GmbH

- Sumitomo Chemical Co. Ltd.

Frequently Asked Questions

Analysis of common user questions about the Polyvinylidene Chloride market and generation of a concise list of summarized FAQs reflecting key topics and concerns.What is Polyvinylidene Chloride (PVDC) used for?

Polyvinylidene Chloride (PVDC) is primarily used for its exceptional barrier properties against moisture, oxygen, and aromas. Its main applications include food packaging (e.g., meat, cheese, processed foods), pharmaceutical packaging (e.g., blister packs for medicines), medical devices, and other industrial applications where product protection and extended shelf-life are critical.

Why is PVDC considered a high-barrier material?

PVDC is considered a high-barrier material due to its highly ordered molecular structure and strong intermolecular forces. These characteristics create a dense, impermeable film that effectively blocks the passage of gases like oxygen, water vapor, and volatile organic compounds, crucial for preserving freshness and efficacy of sensitive products.

How does PVDC contribute to product shelf-life?

By forming an effective barrier against oxygen and moisture, PVDC significantly slows down spoilage processes, oxidation, and degradation in packaged goods. This extended protection helps maintain product freshness, flavor, nutritional value, and potency, thereby substantially increasing product shelf-life and reducing waste.

What are the environmental considerations for PVDC?

Environmental considerations for PVDC primarily revolve around its recyclability due to its chlorine content, which can complicate traditional mechanical recycling. However, ongoing research focuses on developing more sustainable, potentially recyclable, or bio-based PVDC grades, and exploring advanced chemical recycling methods to address these concerns and align with circular economy principles.

Which regions are key markets for PVDC?

Key markets for PVDC include Asia Pacific, driven by rapid industrialization and growing packaging demands; North America, due to its mature pharmaceutical and food industries; and Europe, known for stringent regulations and a focus on high-performance packaging. Latin America and MEA are emerging markets with increasing demand in packaged goods and healthcare sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted