Geosynthetic Clay Liner Market

Geosynthetic Clay Liner Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710077 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

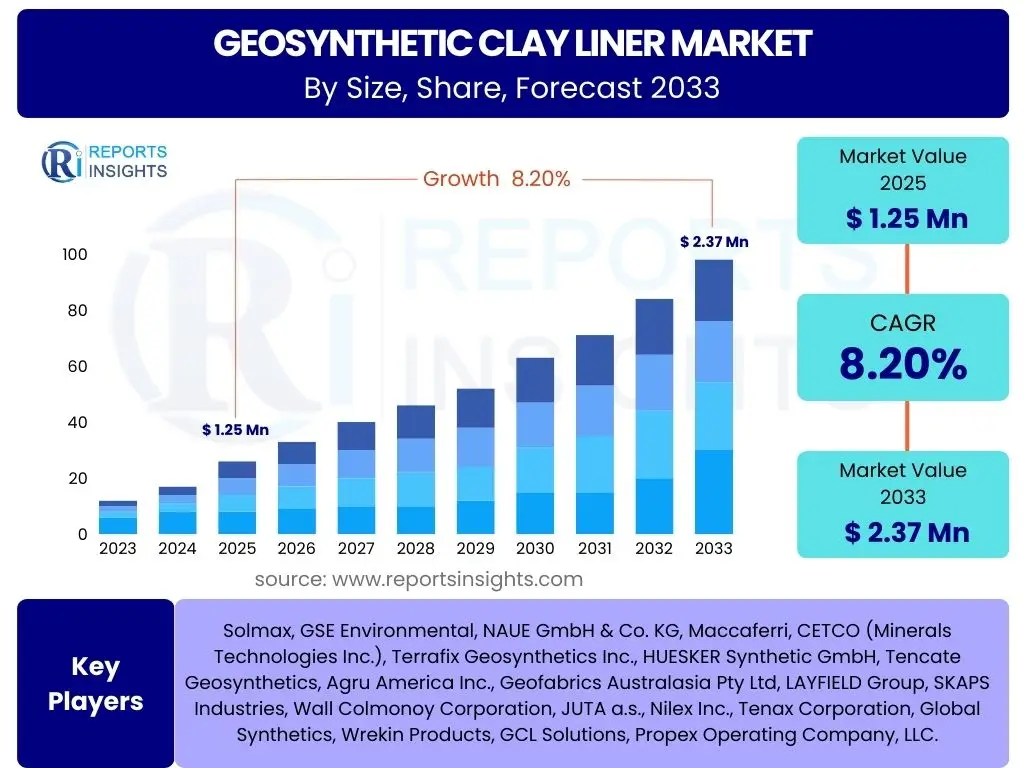

Geosynthetic Clay Liner Market Size

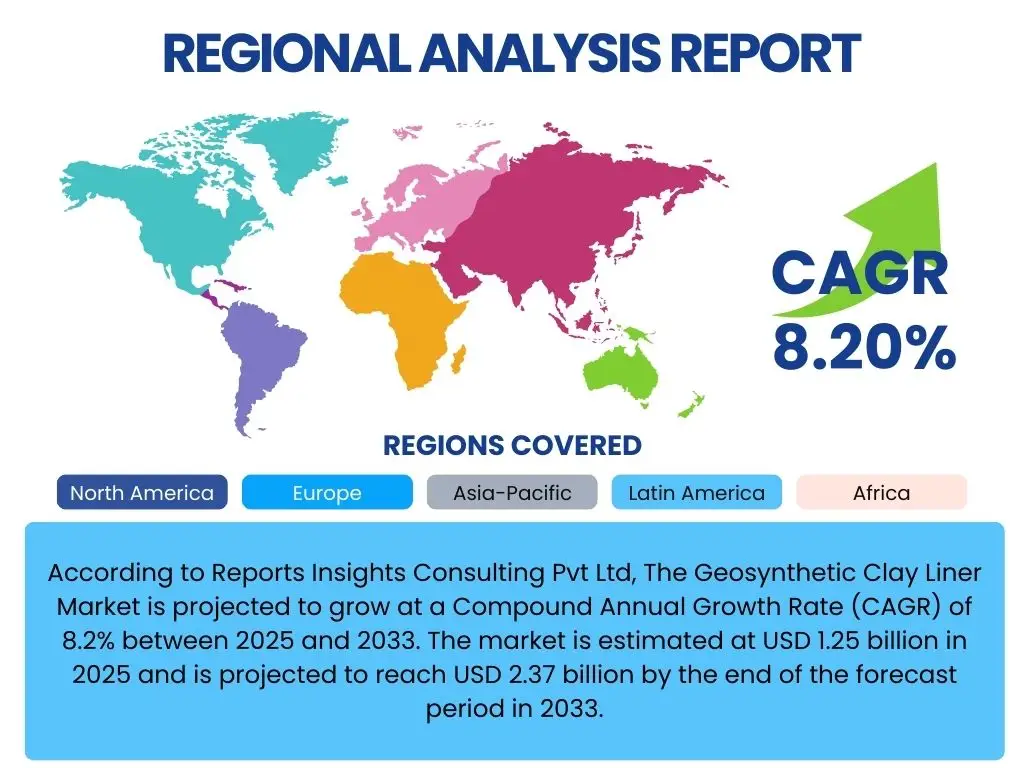

According to Reports Insights Consulting Pvt Ltd, The Geosynthetic Clay Liner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.37 billion by the end of the forecast period in 2033.

Key Geosynthetic Clay Liner Market Trends & Insights

The Geosynthetic Clay Liner (GCL) market is experiencing dynamic shifts driven by increasing environmental regulations and a global push for sustainable infrastructure. Key user inquiries frequently center on the adoption of advanced materials, the expansion into new application areas, and the integration of smart technologies for performance monitoring. There is a growing interest in GCLs that offer enhanced chemical resistance and durability for demanding applications such as hazardous waste containment and mining, alongside a sustained demand for traditional landfill lining solutions. The market is also witnessing a trend towards pre-fabricated and modular GCL systems, aiming to reduce installation time and labor costs on large-scale projects, reflecting an industry-wide focus on efficiency and economic viability.

Furthermore, the market is influenced by a rising awareness of the environmental benefits of GCLs, particularly their low hydraulic conductivity and self-sealing properties, which are crucial for minimizing leachate leakage and groundwater contamination. Innovations in manufacturing processes are leading to the development of thinner yet equally effective GCLs, optimizing material usage and transportation logistics. This evolution is vital as project specifications become more stringent, demanding high-performance barrier solutions that can withstand various environmental stressors over extended periods. Users are increasingly seeking information on the long-term performance data and certifications that validate the efficacy of these advanced GCL products.

- Increased adoption of GCLs in diverse civil engineering and environmental applications.

- Growing emphasis on sustainable and eco-friendly containment solutions.

- Development of GCLs with enhanced chemical resistance and mechanical strength.

- Integration of GCLs with other geosynthetics for composite liner systems.

- Rising demand for factory-produced, quality-assured GCL products minimizing field variables.

- Expansion of GCL use in water management, including reservoirs, canals, and wastewater treatment ponds.

AI Impact Analysis on Geosynthetic Clay Liner

User inquiries concerning AI's influence on the Geosynthetic Clay Liner (GCL) sector primarily focus on its potential to optimize design, improve quality control, and enhance project management efficiency. Stakeholders are keen to understand how artificial intelligence can streamline complex engineering calculations for GCL installations, predict material performance under varying conditions, and automate aspects of site monitoring. The expectation is that AI will contribute to more precise material specification, minimizing waste and ensuring optimal barrier integrity, especially for large-scale and critical containment projects where failure is not an option. This includes using AI-driven analytics to assess environmental data and tailor GCL solutions more effectively to specific geological and hydrological contexts.

Moreover, AI is anticipated to revolutionize quality assurance throughout the GCL product lifecycle, from manufacturing to installation. Machine learning algorithms can analyze vast datasets from production lines to detect anomalies, ensuring consistent product quality. On-site, AI-powered drones and sensors can monitor GCL deployment, identifying potential installation flaws in real-time and providing predictive maintenance insights for existing liner systems. This proactive approach aims to significantly reduce the risk of future failures, extend the service life of GCL installations, and lower overall maintenance costs. The integration of AI also promises improved project logistics, optimizing material delivery and scheduling, thereby enhancing overall operational efficiency and accelerating project completion.

- AI-driven optimization of GCL design and material selection for specific project requirements.

- Enhanced quality control in GCL manufacturing through predictive analytics and anomaly detection.

- Automated monitoring of GCL installation processes using AI-powered imaging and sensor technology.

- Predictive maintenance and performance assessment of installed GCL systems.

- Streamlined project management and logistics for GCL deployment, improving efficiency.

- Data-driven decision-making for environmental risk assessment in containment applications.

Key Takeaways Geosynthetic Clay Liner Market Size & Forecast

Analysis of user questions regarding the Geosynthetic Clay Liner market size and forecast consistently reveals a strong interest in understanding the underlying growth drivers, the long-term sustainability of the market, and the geographical areas poised for significant expansion. Users are particularly keen on how environmental protection mandates and infrastructure development initiatives globally will influence GCL adoption rates. The insights suggest that the market's robust growth trajectory is firmly linked to increasing regulatory pressures for effective waste containment and water resource management, alongside the ongoing expansion of urban and industrial infrastructure that necessitates reliable barrier solutions.

The forecast indicates sustained growth, underpinned by the inherent advantages of GCLs, such as their cost-effectiveness, ease of installation compared to compacted clay liners, and superior hydraulic performance. Key takeaways emphasize the critical role GCLs play in environmental remediation, civil engineering, and mining, with future growth propelled by product innovation and diversification into new application sectors. The market is expected to thrive in regions investing heavily in waste management infrastructure and sustainable resource projects, making GCLs an indispensable component for modern engineering and environmental protection efforts.

- Strong CAGR projected due to rising global environmental protection regulations.

- Significant market expansion driven by infrastructure development and waste management projects.

- Cost-effectiveness and performance benefits of GCLs over traditional liners are key adoption factors.

- Emerging economies present substantial growth opportunities for GCL manufacturers and suppliers.

- Technological advancements in GCL formulations enhance durability and chemical resistance.

- Continued demand in traditional applications like landfills, mining, and water containment.

Geosynthetic Clay Liner Market Drivers Analysis

The Geosynthetic Clay Liner (GCL) market is primarily driven by escalating global environmental concerns and the subsequent enforcement of stringent regulatory frameworks aimed at pollution control and waste management. Governments and international bodies are increasingly mandating the use of impermeable barrier systems in landfills, mining sites, and industrial containment areas to prevent the leakage of hazardous substances into soil and groundwater. GCLs, with their low hydraulic conductivity and self-sealing properties, offer an effective and compliant solution, thereby becoming indispensable in modern environmental engineering projects. This regulatory push provides a consistent demand floor for the market, particularly in developed regions with established environmental protection agencies.

Furthermore, rapid urbanization, industrialization, and infrastructure development worldwide significantly contribute to market expansion. Projects such as road construction, railway lines, reservoirs, canals, and wastewater treatment plants require reliable lining systems for erosion control, water retention, and contaminant isolation. GCLs present a cost-effective, easy-to-install, and high-performance alternative to traditional compacted clay liners, making them attractive for large-scale civil engineering applications. The ongoing global investment in these sectors, especially in emerging economies, fuels the demand for efficient and durable geosynthetic solutions, propelling the GCL market forward. The long-term performance and reduced carbon footprint of GCLs compared to alternative methods also appeal to projects focused on sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | +2.1% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Global Infrastructure Development | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2025-2033) |

| Advantages over Compacted Clay Liners | +1.5% | Global | Short to Long-term (2025-2033) |

| Growth in Mining and Waste Management | +1.2% | Asia Pacific, Latin America, North America | Mid to Long-term (2026-2033) |

Geosynthetic Clay Liner Market Restraints Analysis

Despite its robust growth, the Geosynthetic Clay Liner (GCL) market faces several significant restraints, with raw material price volatility being a primary concern. Bentonite clay, the core component of GCLs, is subject to price fluctuations influenced by mining costs, supply chain disruptions, and global demand for other bentonite applications. This unpredictability can impact manufacturing costs and, consequently, the final product price, potentially affecting market competitiveness, especially against alternative lining solutions. The reliance on specific geographical sources for high-quality bentonite also introduces geopolitical risks and logistical challenges that can hinder consistent supply and drive up expenses, making long-term planning more complex for manufacturers.

Another restraint is the lack of widespread awareness and expertise regarding GCL installation and benefits in certain developing regions. While GCLs offer ease of installation compared to traditional compacted clay liners, improper handling or installation techniques can compromise their performance. This necessitates specialized training and quality control measures, which may not always be readily available or prioritized in all markets. Furthermore, competition from other liner technologies, such as geomembranes (HDPE, LLDPE), can pose a challenge. While GCLs often perform optimally as part of a composite liner system with geomembranes, in some applications, a standalone geomembrane might be chosen due to initial cost perceptions or specific project requirements, limiting GCL market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility (Bentonite) | -0.8% | Global | Short to Mid-term (2025-2029) |

| Competition from Alternative Liner Technologies | -0.7% | Global | Long-term (2025-2033) |

| Lack of Awareness in Emerging Markets | -0.5% | Latin America, Middle East & Africa | Mid to Long-term (2026-2033) |

| Installation Expertise and Quality Control | -0.4% | Asia Pacific, Latin America | Short to Mid-term (2025-2029) |

Geosynthetic Clay Liner Market Opportunities Analysis

The Geosynthetic Clay Liner (GCL) market is ripe with opportunities, particularly driven by the increasing global focus on sustainable water management and agricultural practices. With growing concerns over water scarcity and contamination, there is an expanding demand for efficient and environmentally sound solutions for lining reservoirs, irrigation canals, aquaculture ponds, and water retention basins. GCLs offer an ideal solution due to their low permeability, self-sealing capabilities, and environmental inertness, making them superior to conventional methods in many aquatic applications. The adoption of GCLs in these areas not only helps conserve water but also prevents the seepage of pollutants, aligning with global sustainability goals and creating new market avenues.

Furthermore, emerging economies, particularly in Asia Pacific and Latin America, present significant untapped potential for GCL market expansion. These regions are undergoing rapid industrialization and urbanization, leading to an urgent need for modern waste management facilities, infrastructure development, and environmental remediation projects. As regulatory frameworks strengthen and awareness of advanced containment solutions grows, these economies are expected to become major consumers of GCLs. Product innovation, including the development of specialized GCLs with enhanced properties (e.g., improved chemical resistance for industrial waste, greater shear strength for steep slopes), will also unlock new niche applications and further solidify the market's growth trajectory, offering manufacturers a competitive edge.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Water Management & Aquaculture | +1.7% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Untapped Potential in Emerging Economies | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2026-2033) |

| Product Innovation and Specialization | +1.3% | Global | Mid to Long-term (2027-2033) |

| Renewable Energy Infrastructure (Solar/Wind Farms) | +0.9% | Europe, North America, Asia Pacific | Mid to Long-term (2026-2033) |

Geosynthetic Clay Liner Market Challenges Impact Analysis

The Geosynthetic Clay Liner (GCL) market faces significant challenges, particularly related to the complex and evolving regulatory landscape across different regions. While environmental regulations often drive GCL demand, inconsistencies or frequent changes in these regulations, particularly concerning material specifications, installation standards, and approval processes, can create uncertainty for manufacturers and project developers. Navigating a patchwork of diverse local, national, and international standards requires substantial investment in compliance and can delay project approvals, impacting market growth. Ensuring GCLs meet all necessary certifications for various applications and jurisdictions globally presents a continuous hurdle for market participants seeking broader penetration.

Another crucial challenge is managing the logistics and installation complexities associated with large-scale GCL projects. While GCLs offer ease of installation compared to traditional clay liners, their deployment still requires skilled labor, appropriate machinery, and careful site preparation to ensure optimal performance. Training and retaining skilled personnel capable of proper GCL handling, placement, and seaming, especially in remote project locations, can be difficult. Furthermore, ensuring consistent quality control both at the manufacturing facility and during field installation is paramount. Any compromise in material integrity or installation quality can lead to performance failures, which could damage market reputation and hinder future adoption, making rigorous quality assurance a continuous and demanding endeavor for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving Regulatory & Certification Standards | -0.6% | Global | Long-term (2025-2033) |

| Logistical & Installation Complexity for Large Projects | -0.5% | Global | Mid to Long-term (2026-2033) |

| Skilled Labor Shortage for Installation | -0.4% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Quality Assurance in Manufacturing & Field | -0.3% | Global | Long-term (2025-2033) |

Geosynthetic Clay Liner Market - Updated Report Scope

This report provides a comprehensive analysis of the global Geosynthetic Clay Liner market, detailing market size, growth trends, drivers, restraints, opportunities, and challenges from 2019 to 2033. It offers deep insights into market segmentation by type, application, and region, along with competitive landscape analysis. The scope includes an assessment of AI's emerging impact on the industry, offering a forward-looking perspective on technological integration and its potential to reshape GCL design, manufacturing, and deployment strategies. The report aims to equip stakeholders with actionable intelligence for strategic decision-making in this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 billion |

| Market Forecast in 2033 | USD 2.37 billion |

| Growth Rate | 8.2% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Solmax, GSE Environmental, NAUE GmbH & Co. KG, Maccaferri, CETCO (Minerals Technologies Inc.), Terrafix Geosynthetics Inc., HUESKER Synthetic GmbH, Tencate Geosynthetics, Agru America Inc., Geofabrics Australasia Pty Ltd, LAYFIELD Group, SKAPS Industries, Wall Colmonoy Corporation, JUTA a.s., Nilex Inc., Tenax Corporation, Global Synthetics, Wrekin Products, GCL Solutions, Propex Operating Company, LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Geosynthetic Clay Liner (GCL) market is segmented to provide a detailed understanding of its various components and their respective contributions to overall market growth. This segmentation helps identify key market dynamics, performance characteristics across different GCL types, and the diverse applications driving demand. By dissecting the market along these lines, stakeholders can gain a clearer perspective on where growth is concentrated and where future opportunities may lie, enabling more targeted strategic planning and product development efforts. Each segment represents a distinct facet of the GCL industry, influenced by specific technological advancements, regulatory requirements, and end-user needs.

- By Type:

- Woven GCLs: Characterized by their strength and suitability for applications requiring higher shear resistance.

- Non-Woven GCLs: Known for their flexibility and conformity to irregular surfaces, often preferred in landfill capping.

- Composite GCLs: Combine GCLs with other geosynthetics like geomembranes for enhanced barrier properties and durability.

- By Application:

- Landfills & Waste Containment: Primary application for municipal, hazardous, and industrial waste.

- Mining & Industrial Containment: Used for heap leach pads, tailings dams, and industrial ponds.

- Roadways & Railways: For subgrade stabilization, erosion control, and moisture barrier.

- Water Management (Ponds, Canals, Reservoirs): Impermeable lining for water conservation and pollution prevention.

- Environmental Remediation: Applications in brownfield sites, contaminant encapsulation, and soil stabilization.

- Other Civil Engineering Applications: Includes construction of sports fields, foundations, and tunnels.

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East & Africa (MEA)

Regional Highlights

- North America: A mature market with stringent environmental regulations, driving consistent demand for GCLs in landfill lining, mining, and civil infrastructure projects. High adoption rates of advanced GCL products are observed, supported by robust research and development activities and a focus on long-term performance and sustainability.

- Europe: Characterized by strong environmental protection policies and significant investment in waste management and renewable energy infrastructure. Germany, France, and the UK are key markets, with a growing emphasis on green building and sustainable land use practices. Demand for GCLs in water management and environmental remediation is particularly strong.

- Asia Pacific (APAC): The fastest-growing region, propelled by rapid urbanization, industrialization, and infrastructure development, especially in China, India, and Southeast Asian countries. Increasing environmental awareness and the implementation of new regulations are fostering a surge in demand for GCLs in waste containment, water resources, and civil engineering projects.

- Latin America: An emerging market with significant growth potential driven by expansion in mining operations, agricultural development, and growing infrastructure needs. Countries like Brazil and Mexico are witnessing increased adoption of GCLs for heap leach pads, tailing dams, and reservoir lining, as environmental compliance becomes more prevalent.

- Middle East & Africa (MEA): This region is experiencing nascent but growing demand for GCLs, primarily due to increasing investments in large-scale infrastructure projects, water management initiatives (desalination plants, irrigation), and the development of modern waste disposal facilities. Opportunities exist for both established and new players as environmental standards evolve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Geosynthetic Clay Liner Market.- Solmax

- GSE Environmental

- NAUE GmbH & Co. KG

- Maccaferri

- CETCO (Minerals Technologies Inc.)

- Terrafix Geosynthetics Inc.

- HUESKER Synthetic GmbH

- Tencate Geosynthetics

- Agru America Inc.

- Geofabrics Australasia Pty Ltd

- LAYFIELD Group

- SKAPS Industries

- Wall Colmonoy Corporation

- JUTA a.s.

- Nilex Inc.

- Tenax Corporation

- Global Synthetics

- Wrekin Products

- GCL Solutions

- Propex Operating Company, LLC.

Frequently Asked Questions

What are Geosynthetic Clay Liners (GCLs) and their primary function?

Geosynthetic Clay Liners (GCLs) are factory-manufactured hydraulic barriers consisting of a layer of bentonite clay sandwiched between two geotextiles or bonded to a geomembrane. Their primary function is to provide an effective, low-permeability barrier to prevent liquid and gas migration in various containment applications, such as landfills, ponds, and mining sites.

How do GCLs compare to traditional compacted clay liners?

GCLs offer several advantages over traditional compacted clay liners, including superior hydraulic performance (lower permeability), significant space savings due to their thin profile, reduced installation time and costs, and self-sealing capabilities if punctured. They also provide more consistent quality due to factory manufacturing and are less susceptible to installation variability or weather conditions.

What are the key applications for Geosynthetic Clay Liners?

GCLs are extensively used in diverse applications such as municipal and hazardous waste landfills (both base liners and caps), mining heap leach pads and tailing impoundments, wastewater treatment lagoons, retention ponds, canals, reservoirs, secondary containment for fuel tanks, and various civil engineering projects requiring impermeable barriers or erosion control.

What factors are driving the growth of the GCL market?

The GCL market is primarily driven by stringent environmental regulations mandating effective containment solutions, increasing global infrastructure development, the inherent performance and cost-effectiveness advantages of GCLs over traditional methods, and growing demand from waste management and mining sectors. Rising awareness of sustainable engineering solutions also contributes to growth.

What are the main types of GCLs available in the market?

The main types of GCLs include woven GCLs, which utilize a woven geotextile as a carrier or cover, offering higher shear strength; non-woven GCLs, which use non-woven geotextiles for flexibility and conformity; and composite GCLs, which integrate a geomembrane with the bentonite layer for enhanced impermeability and protection. Each type is suited for specific project requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted