Ambient Food Packaging Market

Ambient Food Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703996 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

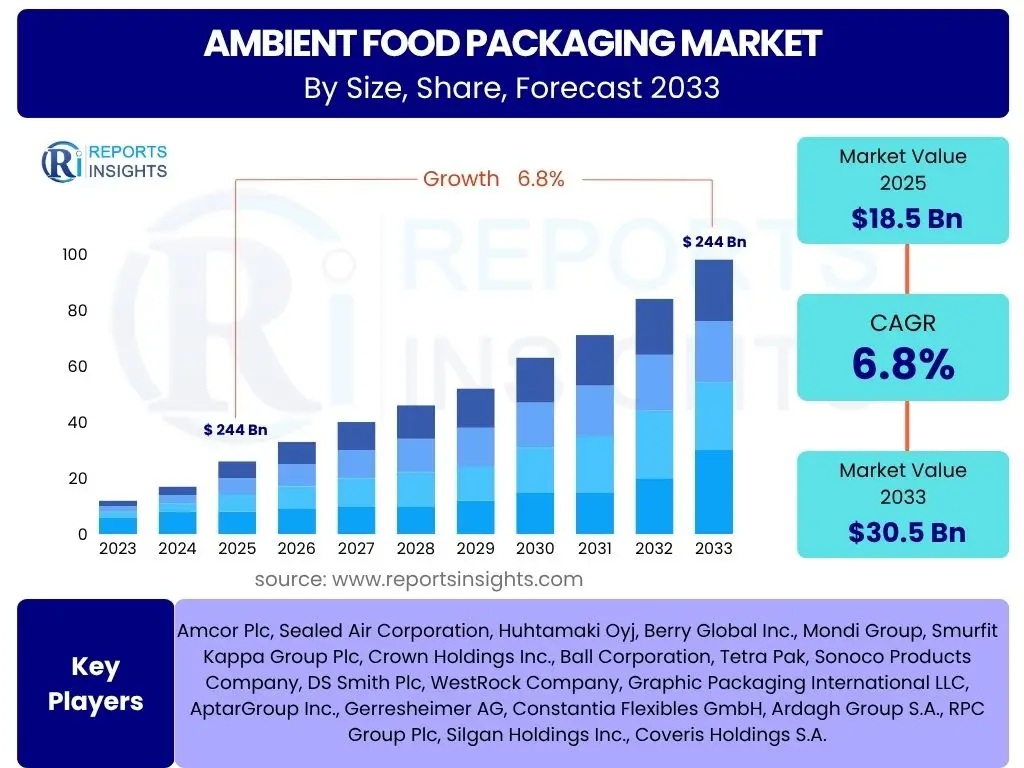

Ambient Food Packaging Market Size

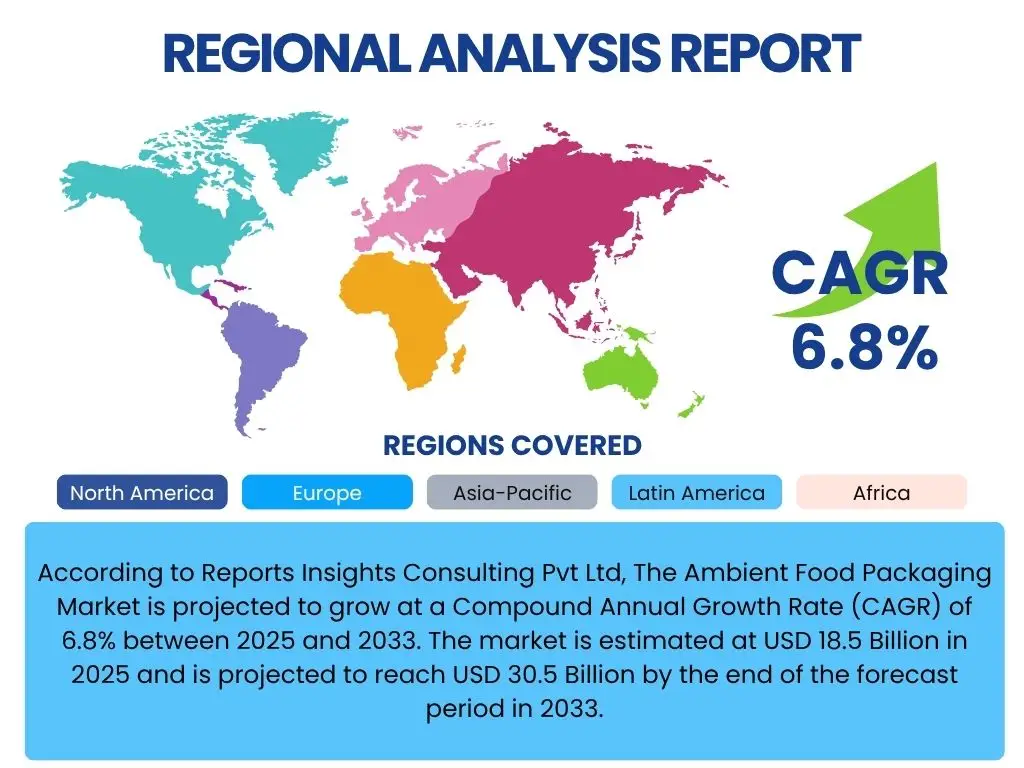

According to Reports Insights Consulting Pvt Ltd, The Ambient Food Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 30.5 Billion by the end of the forecast period in 2033.

Key Ambient Food Packaging Market Trends & Insights

The Ambient Food Packaging market is witnessing a profound transformation driven by evolving consumer preferences, technological advancements, and a heightened focus on sustainability. Users frequently inquire about the shift towards eco-friendly packaging solutions, the impact of e-commerce on packaging design, and the integration of smart technologies. The demand for packaging that extends shelf life without refrigeration while minimizing environmental footprint is a prominent theme, leading to innovation in barrier properties and material science.

Another significant area of interest revolves around convenience and portability. Consumers seek ready-to-eat and on-the-go food options, necessitating packaging that is easy to open, resealable, and microwaveable. This trend influences material selection and structural design, balancing functionality with aesthetic appeal. Furthermore, the rising awareness of food waste is propelling the adoption of packaging solutions that maintain product freshness for longer durations, thereby contributing to sustainability goals.

The digitalization of retail, particularly the rapid expansion of e-commerce, is reshaping packaging requirements. Packaging must not only protect contents during transit but also serve as a brand ambassador, offering an unboxing experience while being robust enough to withstand multiple touchpoints in the supply chain. This dual requirement drives innovation in lightweight, durable, and visually appealing designs that resonate with online consumers.

- Increased demand for sustainable and recyclable packaging materials.

- Growth in e-commerce necessitating robust and optimized packaging solutions.

- Rising adoption of smart packaging technologies for enhanced traceability and consumer engagement.

- Escalating consumer preference for convenient, ready-to-eat, and portion-controlled food items.

- Innovations in barrier technologies to extend product shelf life and reduce food waste.

- Shift towards lightweight and flexible packaging formats.

- Premiumization of ambient food products, driving demand for aesthetically appealing and high-quality packaging.

AI Impact Analysis on Ambient Food Packaging

The integration of Artificial intelligence (AI) into the ambient food packaging sector is a topic of considerable interest, with common user questions focusing on its potential to revolutionize manufacturing, supply chain management, and product design. Stakeholders are keen to understand how AI can optimize production processes, enhance quality control, and predict market demands, ultimately leading to greater efficiency and reduced operational costs. The ability of AI to analyze vast datasets for predictive maintenance and real-time fault detection is seen as a key driver for improving OEE (Overall Equipment Effectiveness) in packaging lines.

Beyond operational efficiencies, users also explore AI's role in developing innovative packaging solutions. AI algorithms can be employed in material science research to identify novel compositions with superior barrier properties or biodegradability, accelerating the development of next-generation packaging. Furthermore, AI-driven design tools can automate the creation of optimized packaging prototypes, considering factors such as material usage, structural integrity, and consumer interaction. This reduces design cycles and brings more efficient and effective packaging to market faster.

However, concerns also exist regarding data privacy, cybersecurity risks associated with interconnected systems, and the potential impact on human employment within the industry. While AI promises significant advancements, a balanced approach is required to harness its benefits while mitigating associated risks, ensuring ethical deployment and fostering workforce reskilling initiatives to adapt to an AI-augmented environment. The long-term implications for the skilled labor force are a recurring theme in discussions surrounding AI adoption.

- Enhanced quality control and defect detection through AI-powered vision systems.

- Optimization of supply chain logistics and inventory management using predictive analytics.

- Personalized packaging design and material selection based on consumer data and trends.

- Predictive maintenance for packaging machinery, reducing downtime and operational costs.

- Automation of sorting and recycling processes in waste management facilities.

- Improved food safety and traceability through AI-enabled monitoring systems.

- Accelerated research and development of sustainable and high-performance packaging materials.

Key Takeaways Ambient Food Packaging Market Size & Forecast

Analysis of user inquiries concerning the Ambient Food Packaging market size and forecast reveals a strong emphasis on understanding the primary growth catalysts, the long-term sustainability of market expansion, and the regional disparities in market development. Stakeholders are particularly interested in identifying the sectors within ambient food packaging that are poised for the most significant growth and the underlying demographic or economic shifts driving this expansion. The overarching consensus points to a market resilient to economic fluctuations due to the essential nature of food consumption, further bolstered by innovation.

A critical takeaway is the increasing influence of consumer health consciousness and environmental concerns on market trajectory. The forecast indicates that packaging solutions aligning with demands for reduced preservatives, extended natural shelf life, and eco-friendly materials will experience accelerated adoption. This suggests that future growth will not only be driven by volume but also by the value added through sustainable and functional packaging attributes. Strategic investments in biodegradable and compostable alternatives are expected to yield substantial returns over the forecast period.

Furthermore, the market's robust growth forecast is underpinned by the expansion of organized retail, the increasing penetration of processed and convenience foods in developing economies, and continuous advancements in packaging technologies that maintain food quality without refrigeration. The projection to reach USD 30.5 Billion by 2033 underscores the market's vitality and its capacity for sustained expansion, positioning it as a key component of the global food industry's infrastructure. The market will continue to be shaped by innovation in barrier technologies and material science.

- The market is on a robust growth trajectory, projected to exceed USD 30 Billion by 2033, driven by evolving consumer lifestyles.

- Sustainability and circular economy principles are central to future market development and investment.

- Technological advancements in material science and smart packaging are crucial for competitive advantage.

- Developing regions, particularly in Asia Pacific, are anticipated to be significant growth engines due to increasing urbanization and disposable incomes.

- Focus on convenience, extended shelf life, and food safety will continue to shape product innovation.

Ambient Food Packaging Market Drivers Analysis

The Ambient Food Packaging market is propelled by a confluence of factors, primarily the rising global population and subsequent increase in food consumption, coupled with the accelerating pace of urbanization which necessitates convenient and shelf-stable food options. Consumer lifestyles are becoming increasingly hectic, leading to a greater reliance on ready-to-eat meals, processed foods, and convenient snack items that require effective ambient packaging to ensure freshness and longevity without refrigeration. This fundamental shift in dietary habits and consumption patterns forms a robust foundation for market expansion.

Furthermore, the growth of organized retail chains, including supermarkets, hypermarkets, and increasingly, e-commerce platforms, significantly drives the demand for ambient food packaging. These distribution channels require standardized, durable, and appealing packaging that can withstand complex logistics and enhance product visibility on shelves or online. The extended shelf life offered by ambient packaging reduces food waste in the supply chain and provides greater flexibility for retailers in inventory management, making it an attractive solution.

Innovations in packaging materials and technologies, such as enhanced barrier films, aseptic processing, and modified atmosphere packaging (MAP), are continuously improving the quality and safety of ambient food products. These technological advancements enable a wider range of food items to be packaged for ambient storage, expanding the market's scope and appealing to health-conscious consumers seeking minimally processed yet shelf-stable options. The push for sustainable packaging solutions also acts as a driver, with companies investing in recyclable, biodegradable, and renewable materials to meet environmental regulations and consumer demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Convenience Foods | +1.2% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Expansion of Organized Retail & E-commerce | +1.0% | Emerging Economies (APAC, Latin America), Developed Markets | Mid to Long-term (2026-2033) |

| Technological Advancements in Packaging Materials | +0.8% | Global | Long-term (2028-2033) |

| Increasing Focus on Food Safety & Shelf Life Extension | +0.7% | Global | Short to Mid-term (2025-2030) |

| Rising Disposable Incomes in Developing Nations | +0.6% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

Ambient Food Packaging Market Restraints Analysis

Despite its robust growth, the Ambient Food Packaging market faces several significant restraints that could impede its full potential. One primary challenge is the volatility in raw material prices, particularly for plastics, paperboard, and metals, which are derivatives of petrochemicals, timber, and mining activities. Fluctuations in global commodity markets, geopolitical instability, and supply chain disruptions can lead to unpredictable manufacturing costs, pressuring profit margins for packaging producers and, subsequently, for food manufacturers. This unpredictability hinders long-term strategic planning and investment in new technologies or capacities.

Another considerable restraint stems from the growing consumer preference for fresh, chilled, and minimally processed foods, especially in developed markets. A segment of the consumer base perceives ambient foods as less natural or less healthy due to their extended shelf life, which is sometimes associated with preservatives or extensive processing. This perception, while not always accurate, can divert demand towards refrigerated or freshly prepared alternatives, limiting the growth of certain ambient food categories. Marketing and education efforts are required to dispel these misconceptions.

Furthermore, stringent environmental regulations and increasing public pressure regarding plastic waste and sustainability pose significant hurdles. While the industry is innovating towards eco-friendly solutions, the transition requires substantial investment in research and development, new production lines, and infrastructure for recycling or composting. The cost associated with adopting sustainable materials and processes, coupled with potential regulatory penalties for non-compliance, can act as a restraint, especially for smaller market players. The lack of standardized recycling infrastructure across different regions also complicates the widespread adoption of truly circular packaging solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.9% | Global | Short to Mid-term (2025-2028) |

| Increasing Preference for Fresh/Chilled Foods | -0.7% | North America, Europe | Mid to Long-term (2026-2033) |

| Stringent Environmental Regulations on Plastic Waste | -0.6% | Europe, North America, parts of Asia Pacific | Short to Mid-term (2025-2029) |

| High Initial Investment in Advanced Packaging Technologies | -0.5% | Global | Short-term (2025-2027) |

| Logistical Challenges for Remote Areas | -0.4% | Emerging Economies | Mid-term (2026-2030) |

Ambient Food Packaging Market Opportunities Analysis

Significant opportunities abound in the Ambient Food Packaging market, largely stemming from the accelerating demand for sustainable and biodegradable packaging solutions. As environmental consciousness grows globally and regulatory bodies push for reduced plastic waste, there is an immense potential for manufacturers to innovate and invest in eco-friendly materials such as bio-plastics, compostable films, and recycled content. This shift not only addresses environmental concerns but also resonates positively with a growing segment of environmentally aware consumers, opening new market niches and enhancing brand reputation. Companies that prioritize and successfully implement green packaging initiatives are poised for substantial market gains.

Another burgeoning opportunity lies in the burgeoning e-commerce sector, particularly for food products. Online grocery sales and meal kit deliveries are expanding rapidly, requiring packaging that is not only robust enough to withstand the rigors of shipping but also optimized for space efficiency and consumer convenience upon delivery. Packaging innovations that protect product integrity during transit, minimize shipping costs, and enhance the unboxing experience present a lucrative avenue for growth. The development of intelligent or smart packaging, incorporating QR codes, NFC tags, or sensors, can further enhance product traceability, authenticity verification, and consumer engagement, offering a competitive edge.

Furthermore, untapped potential exists in emerging economies, particularly in Asia Pacific, Latin America, and Africa. Rapid urbanization, increasing disposable incomes, and the expansion of organized retail in these regions are driving a surge in demand for processed and packaged foods. Manufacturers can leverage these markets by offering cost-effective, culturally appropriate, and highly functional ambient food packaging solutions tailored to local preferences and supply chain infrastructures. Customization and localization of packaging designs and sizes can unlock significant market penetration and long-term growth in these high-potential geographies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable & Biodegradable Materials | +1.5% | Global | Mid to Long-term (2027-2033) |

| Growth of E-commerce for Food Products | +1.3% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Integration of Smart Packaging Technologies | +1.0% | Developed Markets, gradually emerging economies | Long-term (2028-2033) |

| Expansion into Emerging Economies | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2026-2033) |

| Demand for Premium & Convenient Packaging Solutions | +0.8% | Global | Short to Mid-term (2025-2030) |

Ambient Food Packaging Market Challenges Impact Analysis

The Ambient Food Packaging market confronts a range of challenges that require strategic navigation to sustain growth and innovation. One significant hurdle is the escalating complexity of the regulatory landscape across different regions. Governments worldwide are implementing stricter regulations concerning food safety, material composition, labeling, and particularly, post-consumer waste management. Compliance with varied and evolving standards, such as those related to plastic reduction or recyclability targets, demands continuous investment in research, development, and operational adjustments, which can significantly increase production costs and market entry barriers for new players.

Another pervasive challenge is managing supply chain disruptions, which have become more frequent and severe in recent years due to geopolitical events, natural disasters, and global pandemics. These disruptions can lead to shortages of critical raw materials, delays in delivery, and increased transportation costs, directly impacting the production schedules and profitability of packaging manufacturers. Ensuring resilience and diversification in the supply chain is paramount to mitigate these risks, but it often involves complex strategic planning and significant capital outlay.

Furthermore, maintaining product quality and ensuring food safety throughout the extended shelf life of ambient products presents a continuous technical challenge. Packaging must offer robust barrier properties against oxygen, moisture, and light to prevent spoilage, while also being inert and non-reactive with the food contents. Any compromise in packaging integrity can lead to product recalls, reputational damage, and significant financial losses. The industry must consistently invest in advanced material science and quality control processes to uphold these high standards, especially as consumer expectations for product safety and freshness continue to rise.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex & Evolving Regulatory Landscape | -0.8% | Global, particularly Europe, North America | Mid-term (2026-2031) |

| Supply Chain Disruptions & Material Shortages | -0.7% | Global | Short to Mid-term (2025-2029) |

| Managing Consumer Perception of Processed Foods | -0.6% | Developed Markets | Long-term (2028-2033) |

| High Waste Management & Recycling Costs | -0.5% | Global | Mid to Long-term (2027-2033) |

| Competition from Alternative Food Preservation Methods | -0.4% | Global | Mid-term (2026-2030) |

Ambient Food Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Ambient Food Packaging market, offering a detailed understanding of its current landscape, historical performance, and future growth prospects. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It delivers actionable insights for stakeholders seeking to make informed strategic decisions in this dynamic industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 30.5 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor Plc, Sealed Air Corporation, Huhtamaki Oyj, Berry Global Inc., Mondi Group, Smurfit Kappa Group Plc, Crown Holdings Inc., Ball Corporation, Tetra Pak, Sonoco Products Company, DS Smith Plc, WestRock Company, Graphic Packaging International LLC, AptarGroup Inc., Gerresheimer AG, Constantia Flexibles GmbH, Ardagh Group S.A., RPC Group Plc, Silgan Holdings Inc., Coveris Holdings S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ambient Food Packaging market is comprehensively segmented across several key parameters, providing a granular view of its diverse components and dynamics. These segmentations allow for a detailed analysis of market performance based on material types, specific food applications, technological advancements in packaging, and the various packaging formats utilized. Understanding these distinct segments is crucial for identifying growth hotspots, niche opportunities, and areas requiring strategic intervention.

For instance, the segmentation by material, encompassing plastic, paper & paperboard, glass, metal, and flexible packaging, highlights the varying preferences and regulatory pressures influencing material adoption. Each material type offers distinct advantages in terms of barrier properties, cost-effectiveness, and sustainability, leading to differential growth rates within their respective sub-segments. Similarly, segmenting by application, from bakery and confectionery to ready-to-eat meals, reveals how specific food categories drive demand for particular packaging solutions, aligning with consumer trends and product requirements.

Furthermore, segmentation by technology, such as aseptic packaging, modified atmosphere packaging (MAP), and vacuum packaging, underscores the importance of advanced preservation methods in extending the shelf life of ambient foods. These technologies are instrumental in maintaining food quality and safety without refrigeration, thereby expanding the array of products suitable for ambient storage. Analyzing these segments collectively provides a holistic understanding of the market's structure and the intricate interplay between innovation, consumer demand, and regulatory frameworks.

- By Material: Plastic (Polyethylene, Polypropylene, PET, PVC, Others), Paper & Paperboard (Corrugated Board, Folding Cartons, Others), Glass, Metal (Aluminum, Steel), Flexible Packaging (Pouches, Films, Bags)

- By Application: Bakery & Confectionery, Dairy & Desserts, Fruits & Vegetables, Meat, Poultry & Seafood, Sauces, Dressings & Condiments, Ready-to-Eat Meals, Soups, Cereals & Snacks, Pet Food, Other Food Products

- By Technology: Aseptic Packaging, Modified Atmosphere Packaging (MAP), Vacuum Packaging, Retort Packaging, Other Technologies

- By Type: Bags & Pouches, Boxes & Cartons, Cans, Jars & Bottles, Trays & Containers, Wraps & Films

- By End-Use: Food Service, Retail, Industrial

Regional Highlights

The Ambient Food Packaging market exhibits distinct regional dynamics, influenced by varying economic development, consumer preferences, regulatory frameworks, and technological adoption rates. North America and Europe represent mature markets characterized by high consumer awareness regarding product quality and sustainability. These regions are at the forefront of adopting advanced packaging technologies and eco-friendly materials, driven by stringent environmental regulations and a strong emphasis on reducing food waste. The demand for convenience foods and premium packaging is also significant, stimulating innovation in design and functionality.

The Asia Pacific (APAC) region stands out as the fastest-growing market, propelled by rapid urbanization, increasing disposable incomes, and the expanding middle-class population. Countries like China, India, and Southeast Asian nations are witnessing a surge in the consumption of processed and packaged foods, leading to a robust demand for ambient packaging solutions. The organized retail sector's expansion, coupled with the nascent but rapidly growing e-commerce penetration in these regions, further fuels market growth. Investments in manufacturing infrastructure and a less stringent regulatory environment, compared to Western counterparts, also contribute to APAC's market expansion.

Latin America, the Middle East, and Africa (MEA) present emerging opportunities, albeit with different market drivers and challenges. In Latin America, economic growth and changing lifestyles are driving the demand for packaged foods, with a focus on cost-effective and functional packaging. The MEA region is characterized by diverse economic landscapes, with growth largely influenced by population expansion and increasing urbanization. While these regions may lag in terms of advanced technology adoption or sustainability initiatives compared to developed markets, they offer significant potential for basic ambient packaging solutions, especially for staple food products. Localized solutions and affordable packaging formats are key to success in these diverse markets.

- North America: Mature market with high adoption of sustainable packaging and advanced barrier technologies. Strong demand for convenience and ready-to-eat foods.

- Europe: Driven by strict environmental regulations and a strong emphasis on circular economy principles. Significant focus on recyclable and compostable packaging materials.

- Asia Pacific (APAC):Fastest-growing region due to rapid urbanization, increasing disposable incomes, and expanding retail infrastructure. High demand for cost-effective and efficient packaging.

- Latin America: Emerging market with growing demand for processed and packaged foods, driven by changing lifestyles and retail expansion.

- Middle East and Africa (MEA): Varied market with opportunities in population-dense areas and increasing reliance on packaged goods due to urbanization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ambient Food Packaging Market.- Amcor Plc

- Sealed Air Corporation

- Huhtamaki Oyj

- Berry Global Inc.

- Mondi Group

- Smurfit Kappa Group Plc

- Crown Holdings Inc.

- Ball Corporation

- Tetra Pak

- Sonoco Products Company

- DS Smith Plc

- WestRock Company

- Graphic Packaging International LLC

- AptarGroup Inc.

- Gerresheimer AG

- Constantia Flexibles GmbH

- Ardagh Group S.A.

- RPC Group Plc

- Silgan Holdings Inc.

- Coveris Holdings S.A.

Frequently Asked Questions

What is ambient food packaging?

Ambient food packaging refers to packaging solutions designed to store and preserve food products at room temperature, without the need for refrigeration or freezing. This type of packaging typically employs advanced barrier properties to protect food from external factors like oxygen, moisture, and light, thereby extending shelf life and ensuring food safety.

Why is ambient food packaging important?

Ambient food packaging is crucial for several reasons: it extends the shelf life of food products, reduces food waste, lowers transportation and storage costs by eliminating the need for cold chains, and provides convenience to consumers through ready-to-eat and on-the-go formats. It also facilitates wider distribution of food products, especially to regions with limited refrigeration infrastructure.

What are the common materials used in ambient food packaging?

Common materials include plastics (such as PET, PP, PE), paper and paperboard, glass, and metals (like aluminum and steel). Flexible packaging, often a combination of various films and foils, is also widely used for its lightweight and barrier properties. The choice of material depends on the food product, desired shelf life, and sustainability goals.

How does sustainability factor into ambient food packaging?

Sustainability is a significant factor, driving innovation towards recyclable, compostable, and bio-based materials. The industry is focused on reducing the environmental footprint of packaging by minimizing material usage, increasing recycled content, and improving end-of-life solutions. This includes designing for recyclability, promoting reusable options, and developing biodegradable alternatives to traditional plastics.

What are the future innovations expected in ambient food packaging?

Future innovations are expected to include widespread adoption of smart packaging technologies (e.g., QR codes, NFC tags for traceability and consumer engagement), advanced barrier coatings for enhanced preservation, development of truly circular economy packaging solutions, and further integration of AI for optimized design and production processes. Personalized and active packaging systems are also emerging trends.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted