Gluten Free Food Market

Gluten Free Food Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704388 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

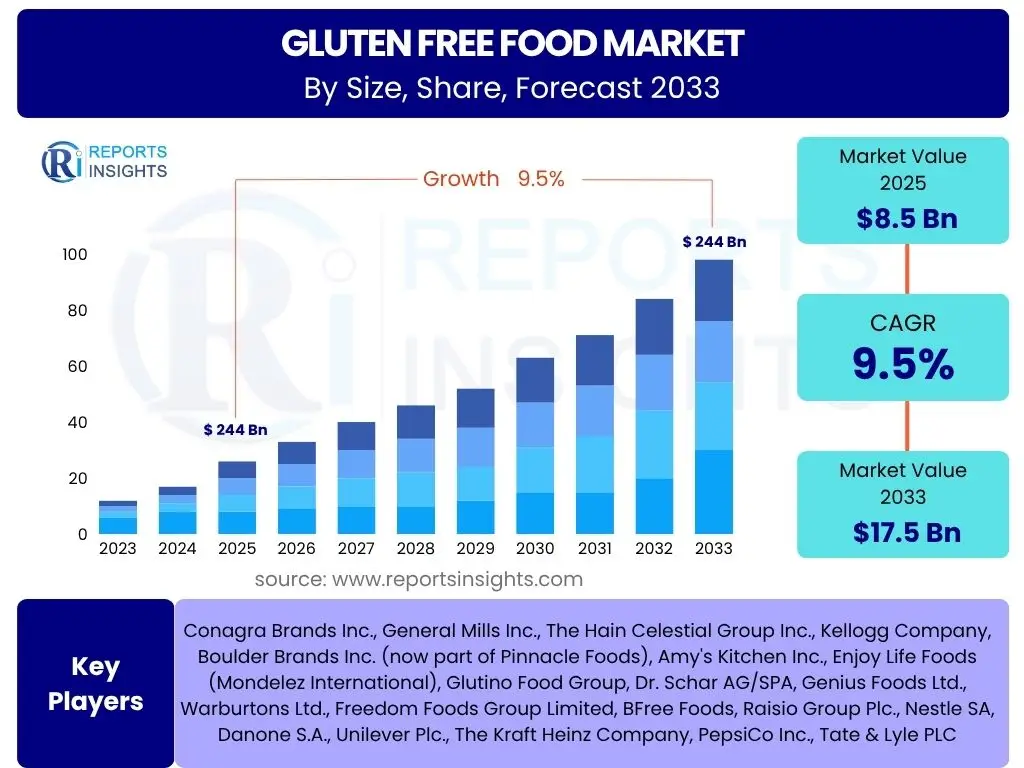

Gluten Free Food Market Size

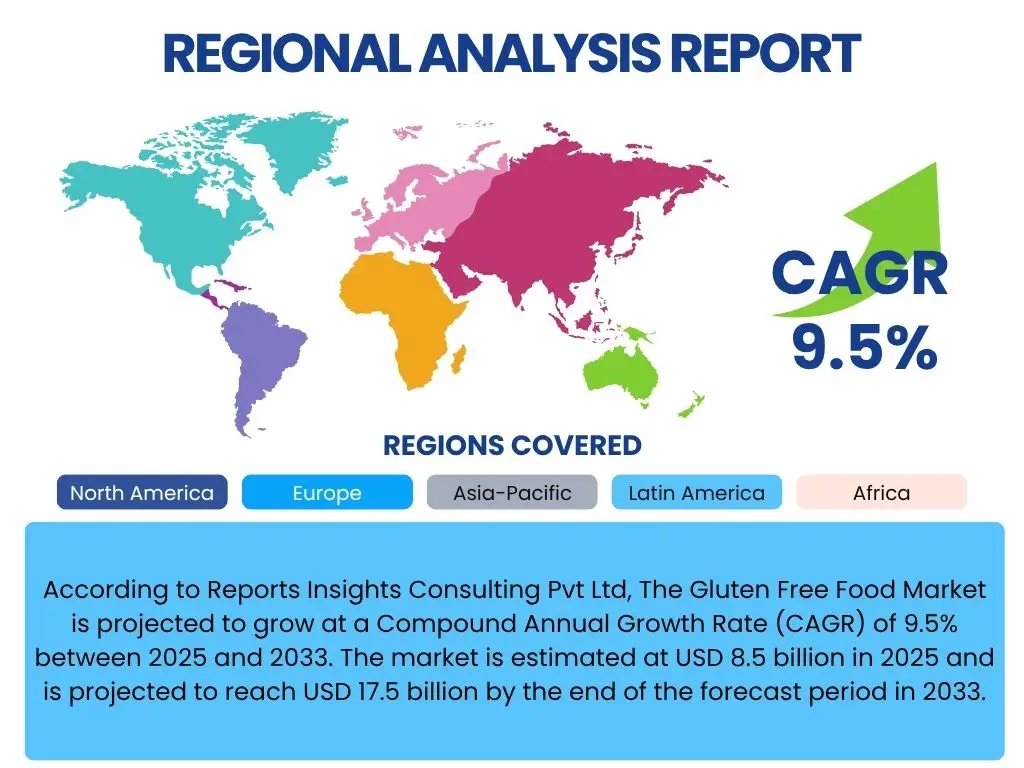

According to Reports Insights Consulting Pvt Ltd, The Gluten Free Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 8.5 billion in 2025 and is projected to reach USD 17.5 billion by the end of the forecast period in 2033.

Key Gluten Free Food Market Trends & Insights

Consumers frequently inquire about the evolving landscape of the gluten-free food market, seeking to understand the significant shifts and innovations driving its expansion. Common questions revolve around the influence of health and wellness trends, the role of dietary preferences beyond celiac disease, and the impact of technological advancements on product development and availability. There is also considerable interest in how retail channels are adapting to meet the growing demand for gluten-free options and the emerging categories gaining traction.

Analysis indicates a clear consumer inclination towards healthier lifestyles, with a notable increase in individuals adopting gluten-free diets for perceived health benefits or to manage sensitivities rather than solely due to celiac disease. This broadens the market's demographic considerably, influencing product innovation to cater to diverse tastes and nutritional needs. Furthermore, the convenience and accessibility offered by online retail platforms are profoundly shaping distribution strategies, making gluten-free products more readily available globally. The market is experiencing a significant shift from niche offerings to mainstream grocery staples.

- Rising health and wellness consciousness driving voluntary adoption of gluten-free diets.

- Increased demand for "free-from" products, extending beyond gluten to include dairy, nuts, and soy.

- Proliferation of e-commerce and direct-to-consumer channels enhancing product accessibility.

- Innovation in taste, texture, and nutritional profiles of gluten-free alternatives.

- Expansion into new product categories, including ready meals, snacks, and beverages.

- Growing consumer preference for clean label and organic gluten-free ingredients.

- Greater awareness and diagnosis of celiac disease and non-celiac gluten sensitivity.

AI Impact Analysis on Gluten Free Food

Users frequently pose questions regarding the potential transformative impact of Artificial Intelligence (AI) on the gluten-free food sector. Their inquiries often focus on how AI can enhance product development, streamline supply chains, improve quality control, and personalize consumer experiences. There is a general expectation that AI technologies could lead to more efficient and effective processes, addressing traditional challenges associated with gluten-free production, such as ingredient sourcing and cross-contamination risks.

The application of AI in the gluten-free food market is anticipated to revolutionize various operational facets, from farm to fork. AI-driven analytics can optimize ingredient selection, predict consumer preferences, and identify novel flavor combinations, thereby accelerating the research and development cycle for new gluten-free products. Furthermore, AI's capability in predictive maintenance and real-time monitoring can significantly enhance food safety protocols, minimizing cross-contamination risks and ensuring compliance with stringent gluten-free standards. This level of precision and predictive capability offers a competitive edge and fosters greater consumer trust.

- AI-driven ingredient formulation for enhanced taste and texture matching gluten-containing counterparts.

- Optimization of supply chain logistics and inventory management for sensitive gluten-free components.

- Predictive analytics for consumer trends and personalized dietary recommendations.

- Automated quality control and allergen detection systems to prevent cross-contamination.

- AI-powered marketing and engagement strategies targeting specific dietary needs.

- Enhanced R&D through rapid prototyping and ingredient discovery for novel gluten-free solutions.

Key Takeaways Gluten Free Food Market Size & Forecast

Common user questions regarding the Gluten Free Food market forecast often center on the long-term viability of the growth, factors sustaining its momentum, and the specific segments expected to drive significant expansion. Consumers and businesses alike seek clarity on whether the current upward trajectory is sustainable and what underlying market dynamics contribute to its resilience. There is particular interest in understanding the core reasons for projected market values and the strategic implications for product development and market entry.

The sustained growth of the gluten-free food market, as indicated by the projected CAGR, is primarily driven by increasing consumer awareness regarding dietary health and wellness, coupled with a higher incidence of diagnosed celiac disease and non-celiac gluten sensitivity. This dual-pronged demand ensures a robust market foundation. Furthermore, continuous innovation in product quality, variety, and accessibility is expanding the market's appeal beyond medical necessity to lifestyle choices, solidifying its position as a significant and enduring segment within the broader food industry. The market's future remains bright, supported by evolving consumer preferences and technological advancements.

- The market exhibits sustained double-digit growth potential driven by health consciousness and medical necessity.

- Significant expansion is expected across all product categories, particularly in bakery and snacks.

- North America and Europe currently dominate, but Asia Pacific is emerging as a high-growth region.

- Technological advancements in food processing are crucial for enhancing product attributes and cost-efficiency.

- E-commerce and specialty retail channels are pivotal for market penetration and consumer reach.

- Investment in research and development for novel ingredients and formulations is a key success factor.

Gluten Free Food Market Drivers Analysis

The growth of the gluten-free food market is propelled by several synergistic factors, primarily rooted in evolving consumer health perceptions and advancements in dietary science. A significant driver is the increasing diagnosis of celiac disease and non-celiac gluten sensitivity, leading to a medical necessity for gluten exclusion. This medical imperative forms a foundational demand segment. Concurrently, a broader trend of health and wellness consciousness is prompting a larger demographic to voluntarily reduce or eliminate gluten from their diets, often associating it with improved digestion, increased energy, and overall well-being. This expansion of the consumer base beyond those with clinical conditions significantly broadens market reach.

Beyond health considerations, the market benefits from continuous product innovation and improved sensory attributes. Manufacturers are increasingly successful in developing gluten-free products that closely mimic the taste and texture of their gluten-containing counterparts, overcoming a historical barrier to widespread adoption. This enhanced product quality, combined with aggressive marketing strategies and wider distribution through mainstream retail channels and online platforms, makes gluten-free options more appealing and accessible to a diverse consumer base. Furthermore, the rising disposable incomes in developing regions allow more consumers to afford the often higher-priced gluten-free products, contributing to global market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Celiac Disease & Gluten Sensitivity Diagnosis | +1.2% | Global, particularly North America, Europe | Long-term (5+ years) |

| Rising Health & Wellness Trends and Voluntary Adoption of Gluten-Free Diets | +1.5% | North America, Europe, Asia Pacific | Mid-term (3-5 years) |

| Product Innovation & Improvement in Taste/Texture | +0.8% | Global | Ongoing, Short-to-Mid term (1-5 years) |

| Expanded Distribution Channels (e-commerce, mainstream retail) | +0.7% | Global | Short-term (1-3 years) |

Gluten Free Food Market Restraints Analysis

Despite robust growth, the gluten-free food market faces several notable restraints that could temper its expansion. A primary challenge is the typically higher cost associated with gluten-free products compared to their traditional counterparts. This premium pricing stems from specialized ingredient sourcing, dedicated production facilities to prevent cross-contamination, and often smaller production scales. For a significant portion of the consumer base, particularly in price-sensitive markets, this cost disparity can act as a barrier to consistent purchasing, limiting market penetration and broad adoption.

Another significant restraint involves taste and texture limitations. While improvements have been substantial, some gluten-free products still struggle to replicate the sensory experience of traditional gluten-containing foods, especially in categories like baked goods which rely heavily on gluten for structure and elasticity. This can lead to consumer dissatisfaction and a reluctance to repurchase. Furthermore, concerns regarding cross-contamination in shared facilities and the perceived nutritional value of some highly processed gluten-free alternatives also present challenges, as consumers become more discerning about clean labels and wholesome ingredients.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Product Cost Compared to Traditional Alternatives | -0.9% | Global, particularly price-sensitive emerging markets | Long-term (5+ years) |

| Challenges in Replicating Taste and Texture | -0.6% | Global | Mid-term (3-5 years) |

| Risk of Cross-Contamination in Manufacturing | -0.4% | Global | Ongoing, Short-term (1-3 years) |

| Consumer Skepticism Regarding Nutritional Value | -0.3% | North America, Europe | Mid-term (3-5 years) |

Gluten Free Food Market Opportunities Analysis

The gluten-free food market is ripe with opportunities for innovation and expansion, primarily driven by evolving consumer demographics and technological advancements. A significant opportunity lies in targeting emerging markets, particularly in Asia Pacific and Latin America, where awareness of celiac disease and gluten sensitivity is growing, and disposable incomes are rising. These regions present untapped consumer bases with increasing purchasing power and a growing interest in Western dietary trends. Tailoring products to local tastes and dietary customs within these markets could unlock substantial growth potential.

Another crucial opportunity involves diversification into new product categories and meal occasions. While bakery and snack items have historically dominated, there is burgeoning demand for gluten-free ready meals, frozen foods, breakfast cereals, and even pet food. Furthermore, technological advancements in ingredient processing and formulation offer the chance to overcome current challenges related to texture and taste, allowing for the creation of more diverse and appealing gluten-free products. The rise of plant-based diets also presents a synergistic opportunity, as many gluten-free products align well with vegan or vegetarian lifestyles, enabling cross-market appeal.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets (Asia Pacific, Latin America) | +1.0% | Asia Pacific, Latin America | Long-term (5+ years) |

| Diversification into New Product Categories (Ready meals, functional foods) | +0.8% | Global | Mid-term (3-5 years) |

| Technological Advancements in Ingredient Sourcing and Formulation | +0.7% | Global | Ongoing, Short-to-Mid term (1-5 years) |

| Synergy with Plant-Based and Clean Label Trends | +0.6% | North America, Europe | Mid-term (3-5 years) |

Gluten Free Food Market Challenges Impact Analysis

The gluten-free food market faces several inherent challenges that require careful navigation from manufacturers and retailers. A significant hurdle is the complexity of regulatory compliance and certification. Ensuring products genuinely meet gluten-free standards and obtaining necessary certifications can be a costly and time-consuming process, particularly when dealing with diverse international regulations. This compliance burden adds to operational overheads and can limit market entry for smaller players. Moreover, consumer perceptions and skepticism surrounding the nutritional benefits of some gluten-free products, especially those high in starches or sugar, pose a marketing challenge that necessitates transparent labeling and educational efforts.

Furthermore, managing supply chain integrity to prevent cross-contamination is an ongoing and critical challenge. Even trace amounts of gluten can trigger adverse reactions in sensitive individuals, requiring stringent protocols from ingredient sourcing to final packaging. This necessitates dedicated facilities or rigorous cleaning procedures, which can elevate production costs. The market also experiences intense competition as major food companies enter the segment, potentially marginalizing smaller, dedicated gluten-free brands. Maintaining competitive pricing while upholding quality and safety standards remains a delicate balancing act for all market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Compliance and Certification Complexities | -0.5% | Global | Ongoing, Long-term (5+ years) |

| Maintaining Supply Chain Integrity and Preventing Cross-Contamination | -0.7% | Global | Ongoing, Short-to-Mid term (1-5 years) |

| Intense Competition from Mainstream Food Companies | -0.4% | North America, Europe | Mid-term (3-5 years) |

| Managing Consumer Perceptions and Education on Nutritional Value | -0.3% | Global | Long-term (5+ years) |

Gluten Free Food Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Gluten Free Food Market, offering critical insights into its current size, historical performance, and future growth trajectory. It examines the intricate market dynamics, including key drivers, prevailing restraints, emerging opportunities, and significant challenges that shape the industry landscape. The scope encompasses detailed segmentation analysis across various product types, distribution channels, and end-use applications, providing a granular view of market performance and potential within each category. Furthermore, the report highlights regional market nuances and identifies leading companies contributing to the market's evolution, presenting a holistic overview crucial for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 17.5 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Conagra Brands Inc., General Mills Inc., The Hain Celestial Group Inc., Kellogg Company, Boulder Brands Inc. (now part of Pinnacle Foods), Amy's Kitchen Inc., Enjoy Life Foods (Mondelez International), Glutino Food Group, Dr. Schar AG/SPA, Genius Foods Ltd., Warburtons Ltd., Freedom Foods Group Limited, BFree Foods, Raisio Group Plc., Nestle SA, Danone S.A., Unilever Plc., The Kraft Heinz Company, PepsiCo Inc., Tate & Lyle PLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The gluten-free food market is meticulously segmented to provide a granular understanding of consumer preferences and market dynamics across various product types, distribution channels, and end-use applications. This segmentation highlights the diverse demands within the market, ranging from staple bakery items to innovative prepared foods and snack alternatives. Each segment responds to unique consumer needs, whether driven by dietary necessity, health-conscious choices, or convenience. Understanding these specific segments is crucial for manufacturers to tailor their product offerings and for retailers to optimize their merchandising strategies, ensuring market relevance and capturing diverse consumer groups.

The product type segmentation reveals a dominance of bakery products and snacks, reflecting their essential role in daily diets and as convenient options. However, significant growth is also observed in dairy and meat alternatives, as well as prepared foods, indicating a broadening scope of gluten-free integration into various meal categories. Distribution channels are diversifying, with online retail experiencing robust growth due to its convenience and wider product availability, complementing the continued importance of supermarkets and specialty health food stores. Source-based segmentation further differentiates between plant-based and animal-based gluten-free options, catering to evolving dietary preferences and ethical considerations, providing a comprehensive view of the market's intricate structure.

- By Product Type:

- Bakery Products: Includes bread, cakes, cookies, pastries, and other baked goods. This segment holds a significant share due to daily consumption patterns.

- Dairy & Meat Alternatives: Encompasses gluten-free milk substitutes, yogurts, cheeses, and plant-based meat alternatives.

- Prepared Foods: Covers gluten-free pasta, pizza, ready-to-eat meals, and other convenient processed foods.

- Flours, Cereals & Snacks: Includes gluten-free flours (rice, almond, oat), breakfast cereals, granola, snack bars, chips, and crackers.

- Others: Broad category including gluten-free beverages, confectionery items, sauces, and condiments.

- By Distribution Channel:

- Supermarkets/Hypermarkets: Remain the primary channel for bulk purchases and wider product visibility.

- Convenience Stores: Caters to immediate consumption needs, offering a selection of popular gluten-free snacks and beverages.

- Online Retail: Experiencing rapid growth due to convenience, extensive product ranges, and direct-to-consumer models.

- Specialty Stores: Includes health food stores and organic markets, catering to consumers seeking niche or premium gluten-free options.

- By Source:

- Plant-Based: Products derived from gluten-free grains like rice, corn, quinoa, tapioca, and soy, as well as nuts and seeds.

- Animal-Based: Primarily refers to naturally gluten-free meat and dairy products, or their processed alternatives that maintain gluten-free certification.

- By End-Use:

- Household: Represents direct consumer purchases for in-home consumption.

- Commercial: Includes sales to restaurants, hotels, cafes, catering services, and institutions providing gluten-free meal options.

Regional Highlights

- North America: This region currently holds the largest market share, driven by a high prevalence of celiac disease diagnoses, increasing health consciousness, and robust consumer awareness. The presence of major market players and well-established distribution networks further contributes to its dominance. Innovation in product variety and aggressive marketing strategies continue to fuel growth in the United States and Canada.

- Europe: Following North America, Europe represents a substantial market for gluten-free foods. Countries like the UK, Germany, and Italy exhibit strong demand due to a rising number of celiac disease diagnoses and a general shift towards healthier eating habits. Strict European Union regulations regarding gluten-free labeling also build consumer trust, stimulating market expansion.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market during the forecast period. This growth is attributed to increasing disposable incomes, rising awareness about gluten-related disorders, and the growing influence of Western dietary trends. Countries such as China, India, and Japan are witnessing a surge in demand, presenting significant opportunities for market players to introduce culturally relevant gluten-free products.

- Latin America: This region is experiencing steady growth in the gluten-free food market, primarily in urban centers. Increasing health awareness, improving diagnostic capabilities for celiac disease, and the expanding presence of international food brands are key drivers. Brazil and Mexico are leading the adoption of gluten-free diets and products.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is showing nascent growth. Urbanization, changing lifestyles, and a gradual increase in health consciousness are contributing factors. The market's expansion here is slower compared to other regions but offers long-term potential as awareness and product availability improve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gluten Free Food Market.- Conagra Brands Inc.

- General Mills Inc.

- The Hain Celestial Group Inc.

- Kellogg Company

- Boulder Brands Inc.

- Amy's Kitchen Inc.

- Enjoy Life Foods

- Glutino Food Group

- Dr. Schar AG/SPA

- Genius Foods Ltd.

- Warburtons Ltd.

- Freedom Foods Group Limited

- BFree Foods

- Raisio Group Plc.

- Nestle SA

- Danone S.A.

- Unilever Plc.

- The Kraft Heinz Company

- PepsiCo Inc.

- Tate & Lyle PLC

Frequently Asked Questions

What is the current market size of the Gluten Free Food industry?

The Gluten Free Food market is estimated at USD 8.5 billion in 2025.

What is the projected growth rate for the Gluten Free Food market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033.

What are the primary drivers of growth in the Gluten Free Food market?

Key drivers include the rising incidence of celiac disease and gluten sensitivity, increasing consumer health consciousness, continuous product innovation, and expanding distribution channels like e-commerce.

Which region dominates the Gluten Free Food market?

North America currently holds the largest share in the Gluten Free Food market, attributed to high awareness and diagnosis rates, and established market players.

What are the main product types within the Gluten Free Food market?

The market segments primarily into Bakery Products, Dairy & Meat Alternatives, Prepared Foods, Flours, Cereals & Snacks, and other categories like beverages and confectionery.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted