Polyvinyl Chloride Film Market

Polyvinyl Chloride Film Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706787 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

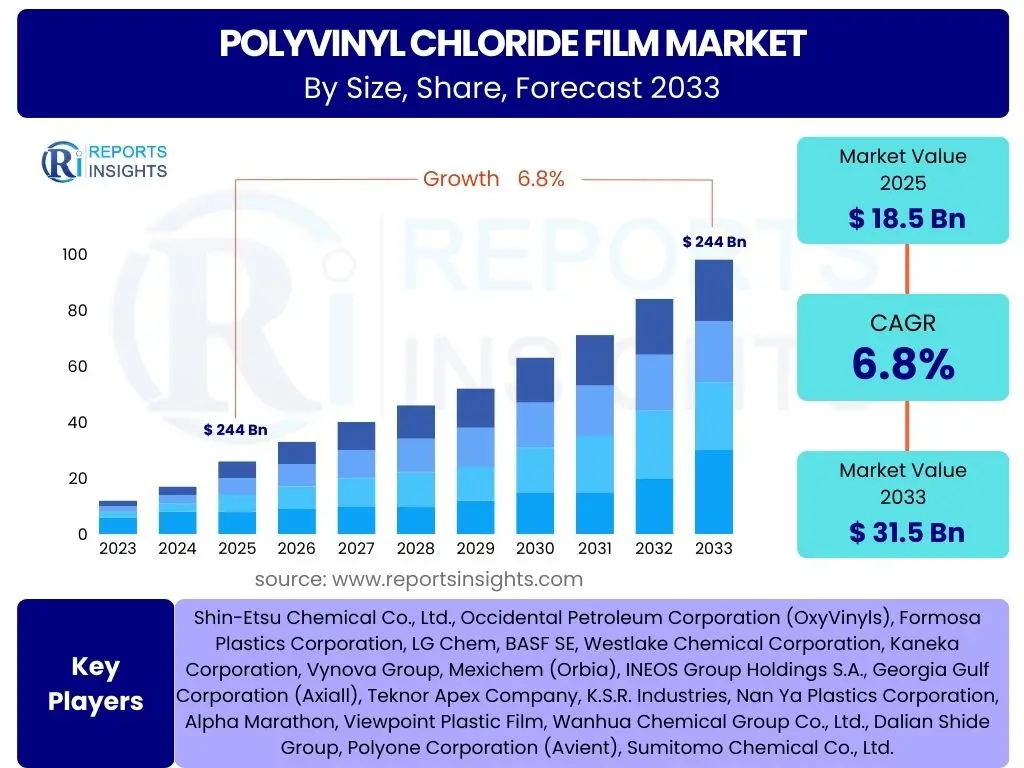

Polyvinyl Chloride Film Market Size

According to Reports Insights Consulting Pvt Ltd, The Polyvinyl Chloride Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 31.5 Billion by the end of the forecast period in 2033.

Key Polyvinyl Chloride Film Market Trends & Insights

The Polyvinyl Chloride (PVC) film market is experiencing transformative shifts driven by evolving consumer demands, regulatory pressures, and technological advancements. A prominent trend involves the increasing adoption of sustainable and eco-friendly PVC film solutions, propelled by growing environmental consciousness and stringent regulations aimed at reducing plastic waste. Manufacturers are investing in research and development to produce bio-based, recycled, and biodegradable PVC films, addressing concerns related to environmental impact while meeting industry performance requirements. This sustainability drive is not only influencing product development but also shaping supply chain practices and end-of-life management strategies.

Furthermore, the market is witnessing significant growth in specialized applications, particularly in the packaging and healthcare sectors. Innovations in flexible packaging demand high-performance, durable, and barrier-property films, which PVC films are increasingly designed to provide. In healthcare, the sterile and adaptable nature of PVC films makes them indispensable for medical packaging, IV bags, and tubing, with ongoing advancements focusing on enhanced safety and material purity. The integration of advanced manufacturing techniques, such as co-extrusion and lamination, is enabling the production of multi-layered PVC films with superior properties, catering to diverse industry needs and expanding the utility of PVC in complex applications.

Another key insight revolves around the expanding use of PVC film in the construction and automotive industries. In construction, PVC films are utilized for flooring, roofing, wall coverings, and window profiles due to their durability, weather resistance, and cost-effectiveness. The automotive sector increasingly employs PVC films for interior surfaces, protective coatings, and wire insulation, valuing their flexibility, aesthetic appeal, and flame-retardant properties. This widespread application across various high-growth sectors underscores the material's versatility and its continued relevance in modern industrial processes, supporting sustained market expansion.

- Growing demand for sustainable and recycled PVC film solutions.

- Technological advancements in film manufacturing, including co-extrusion and lamination.

- Increasing application in medical and pharmaceutical packaging for sterility and barrier properties.

- Expansion of PVC film usage in the construction industry for flooring, roofing, and window profiles.

- Rising adoption in the automotive sector for interior components and protective applications.

AI Impact Analysis on Polyvinyl Chloride Film

Artificial Intelligence (AI) is poised to significantly transform the Polyvinyl Chloride (PVC) film manufacturing landscape by optimizing various operational facets, from raw material procurement to final product delivery. Common user questions often revolve around how AI can enhance efficiency, improve quality control, and predict market trends within this sector. AI algorithms can analyze vast datasets from production lines, identifying patterns and anomalies that human operators might miss, thereby enabling predictive maintenance for machinery, minimizing downtime, and ensuring continuous production. This leads to substantial reductions in operational costs and improvements in overall equipment effectiveness, addressing the industry's continuous pursuit of operational excellence.

In terms of quality assurance, AI-powered vision systems can meticulously inspect PVC films for defects at high speeds, far surpassing human capabilities in consistency and accuracy. This ensures that only high-quality products reach the market, reducing waste and improving customer satisfaction. Furthermore, AI can optimize material formulations by simulating various compositions and predicting their performance characteristics, leading to the development of novel PVC film products with enhanced properties, such as improved durability, flexibility, or barrier resistance. This capability for rapid material innovation is crucial for staying competitive in a dynamic market that constantly demands superior product attributes.

Beyond the manufacturing floor, AI offers considerable potential in supply chain management and demand forecasting. Machine learning models can analyze historical sales data, economic indicators, and seasonal trends to predict future demand for different types of PVC films with greater accuracy, optimizing inventory levels and reducing storage costs. Additionally, AI can assist in sourcing raw materials more efficiently by monitoring global commodity prices and supplier performance, mitigating supply chain risks. While the initial investment in AI infrastructure may be substantial, the long-term benefits in terms of operational efficiency, quality improvement, and strategic decision-making are expected to drive significant competitive advantages for early adopters in the PVC film market.

- Optimization of manufacturing processes through predictive analytics and automation.

- Enhanced quality control and defect detection using AI-powered vision systems.

- Improved supply chain efficiency and logistics through advanced forecasting models.

- Accelerated research and development for new PVC film formulations and properties.

- Reduced operational costs and increased resource utilization through AI-driven insights.

Key Takeaways Polyvinyl Chloride Film Market Size & Forecast

The Polyvinyl Chloride (PVC) film market is poised for robust expansion, driven by its versatile applications across diverse industries. A primary takeaway from the market size and forecast is the sustained demand across established sectors like packaging and construction, complemented by emerging opportunities in healthcare and automotive. Users frequently inquire about the segments offering the highest growth potential and the regions that will dominate this growth. The market's resilience is underpinned by the inherent advantages of PVC, including its cost-effectiveness, durability, and adaptability, which continue to make it a preferred material despite increasing scrutiny over plastic use.

Another crucial insight is the accelerating shift towards sustainable PVC solutions. While traditional PVC faces environmental challenges, ongoing innovations in recycling technologies, bio-based PVC, and closed-loop systems are creating new pathways for growth. This push for sustainability is not merely regulatory compliance but a strategic imperative for manufacturers aiming to meet evolving consumer preferences and secure long-term market viability. Companies that successfully integrate circular economy principles and offer environmentally friendlier alternatives are expected to capture a larger share of the market, influencing future investment patterns and product development trajectories.

Geographically, the Asia Pacific region is anticipated to remain the dominant force in the PVC film market, largely due to rapid industrialization, burgeoning construction activities, and increasing consumer goods production in countries like China and India. However, significant growth potential also exists in emerging economies across Latin America and the Middle East & Africa, driven by infrastructure development and rising disposable incomes. For market participants, understanding these regional dynamics and investing in localized production capabilities or distribution networks will be vital for capitalizing on specific growth pockets and maintaining a competitive edge in a globally expanding market.

- The market exhibits steady growth, driven by broad industrial applications and cost-effectiveness.

- Sustainability initiatives, including recycling and bio-based PVC, are critical for future growth.

- Asia Pacific remains the leading region due to strong industrial and construction sector growth.

- Innovation in film properties and manufacturing processes will drive competitive advantage.

- Healthcare and specialized packaging segments offer significant long-term growth prospects.

Polyvinyl Chloride Film Market Drivers Analysis

The Polyvinyl Chloride (PVC) film market is significantly driven by its extensive and growing adoption across various end-use industries, capitalizing on its unique blend of properties and cost-effectiveness. The burgeoning packaging sector, encompassing food, pharmaceutical, and non-food applications, remains a primary impetus, where PVC films are valued for their excellent barrier properties, clarity, and sealability, ensuring product integrity and extended shelf life. This consistent demand from packaging, coupled with continuous innovation in packaging designs and requirements, propels the market forward. Simultaneously, the global construction industry's expansion, particularly in residential and commercial infrastructure, fuels the demand for PVC films in applications such as flooring, roofing membranes, window profiles, and electrical insulation, leveraging their durability, weather resistance, and ease of installation.

Another crucial driver is the increasing demand from the healthcare and automotive sectors. In healthcare, PVC films are indispensable for sterile medical packaging, IV bags, blood bags, and tubing due to their biocompatibility, flexibility, and ability to be easily sterilized. The consistent need for safe and reliable medical devices and pharmaceutical packaging, especially intensified by global health awareness and healthcare infrastructure development, directly translates into sustained demand for medical-grade PVC films. For the automotive industry, PVC films find widespread use in vehicle interiors, protective wraps, and wire harnesses, chosen for their aesthetics, sound dampening, flame retardancy, and resistance to chemicals and abrasion, aligning with the industry's focus on material performance and safety.

Furthermore, the inherent versatility and cost-efficiency of PVC films make them highly attractive alternatives to other materials in numerous applications. Their ability to be easily processed, printed, and molded into various forms contributes to their widespread industrial acceptance. While facing competition from alternative plastics, PVC films often provide a superior balance of performance and economic viability, securing their position in diverse markets. This combination of established broad applications, continuous innovation, and competitive pricing dynamics collectively contributes to the positive trajectory of the global PVC film market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Packaging Industry | +1.5% | Global, particularly Asia Pacific & Latin America | Medium-term (2025-2029) |

| Expansion of Construction Sector | +1.2% | Emerging economies: China, India, Southeast Asia | Long-term (2025-2033) |

| Rising Demand from Healthcare Sector | +1.0% | North America, Europe, developing nations | Long-term (2025-2033) |

| Cost-effectiveness and Versatility of PVC | +0.8% | Global | Persistent |

| Increasing Automotive Applications | +0.5% | Europe, North America, Asia Pacific | Medium-term (2025-2029) |

Polyvinyl Chloride Film Market Restraints Analysis

The Polyvinyl Chloride (PVC) film market faces significant restraints primarily stemming from growing environmental concerns and increasingly stringent regulatory frameworks globally. The non-biodegradable nature of conventional PVC films and their contribution to plastic waste accumulation have led to negative public perception and strong advocacy for sustainable alternatives. This environmental backlash often translates into consumer preference shifts away from PVC products, particularly in regions with high environmental awareness. Furthermore, the presence of certain additives in PVC, such as phthalates and heavy metals, raises health and safety concerns, prompting regulatory bodies in various countries to restrict or ban their use, thereby limiting the scope and application of traditional PVC films and necessitating costly reformulation efforts for manufacturers.

Competition from alternative materials also poses a substantial restraint to the PVC film market. Materials like polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), and various biodegradable polymers offer competitive performance characteristics and often come with a more favorable environmental profile. Industries, especially packaging and agriculture, are increasingly exploring and adopting these alternatives due to consumer demand for greener products and internal corporate sustainability goals. This competitive pressure forces PVC film manufacturers to innovate continuously and demonstrate the unique advantages of PVC, which can be challenging against a backdrop of increasing environmental scrutiny and the diverse functionalities offered by competing materials.

Fluctuations in the prices of raw materials, primarily crude oil and natural gas derivatives which are feedstocks for ethylene and chlorine, represent another persistent restraint. The volatility in global energy markets directly impacts the production costs of PVC resin, which in turn affects the final price of PVC films. Unpredictable raw material costs can erode profit margins for manufacturers and make long-term planning difficult, potentially hindering investment in new production capacities or research and development. This economic sensitivity adds a layer of uncertainty for market participants, compelling them to manage supply chain risks and optimize operational efficiencies more rigorously to maintain competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns & Waste Management | -1.3% | Global, prominent in Europe & North America | Long-term (2025-2033) |

| Stringent Regulations & Bans on Additives | -1.0% | Europe, North America, parts of Asia Pacific | Medium-term (2025-2029) |

| Competition from Alternative Materials | -0.8% | Global | Persistent |

| Volatile Raw Material Prices | -0.6% | Global | Short-term to Medium-term (2025-2027) |

| Negative Public Perception | -0.5% | Developed countries | Long-term (2025-2033) |

Polyvinyl Chloride Film Market Opportunities Analysis

The Polyvinyl Chloride (PVC) film market presents significant opportunities through the ongoing advancements in sustainable alternatives and recycling technologies. As global awareness concerning environmental impact intensifies, the development of bio-based PVC, recycled PVC (RPVC), and more easily recyclable PVC formulations offers a crucial pathway for market growth. These innovations address key environmental concerns, enabling manufacturers to meet stringent regulatory requirements and cater to the increasing demand for eco-friendly products from both consumers and industries. Investing in research and development for sustainable PVC solutions can open up new market segments and improve the material's overall public image, fostering long-term acceptance and growth.

Another substantial opportunity lies in the expansion into emerging economies, particularly across Asia Pacific, Latin America, and the Middle East & Africa. These regions are experiencing rapid urbanization, industrialization, and significant infrastructure development, leading to a surge in demand for packaging materials, construction components, and healthcare products. With growing populations and improving economic conditions, there is an expanding consumer base and increasing disposable incomes, translating into higher consumption of goods that utilize PVC films. Establishing strong local manufacturing bases and efficient distribution networks in these burgeoning markets can allow companies to tap into immense untapped potential and secure substantial growth.

Furthermore, continuous innovation in flexible packaging solutions and the exploration of niche applications offer promising avenues for market expansion. The demand for lightweight, durable, and highly functional packaging films is on the rise across various industries, including food and beverage, consumer goods, and pharmaceuticals. PVC films, with their excellent barrier properties, clarity, and printability, can be further optimized through multi-layering and coating technologies to meet these evolving requirements. Additionally, exploring niche applications such as smart films, anti-microbial films for medical environments, or specialized protective films for electronics can diversify revenue streams and create new high-value market segments for PVC film manufacturers, leveraging advanced material science and application-specific demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Recycled PVC | +1.4% | Global, particularly Europe & North America | Long-term (2027-2033) |

| Expansion in Emerging Economies | +1.2% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Innovation in Flexible Packaging | +0.9% | Global | Medium-term (2025-2029) |

| Growth in Healthcare & Medical Applications | +0.7% | Global | Long-term (2025-2033) |

| Niche Applications (e.g., Smart Films) | +0.5% | Developed markets | Medium-term (2027-2033) |

Polyvinyl Chloride Film Market Challenges Impact Analysis

The Polyvinyl Chloride (PVC) film market faces significant challenges related to the disposal and recycling infrastructure, which directly impacts its environmental footprint and long-term sustainability. Despite efforts to promote PVC recycling, the collection, sorting, and processing of PVC waste remain complex and less developed compared to other plastics, particularly for mixed plastic streams. This lack of robust recycling infrastructure often leads to PVC films ending up in landfills or incinerators, contributing to pollution and resource depletion. The economic viability of PVC recycling can also be challenging due to the need for specialized sorting and processing technologies, coupled with the presence of additives that can complicate the recycling process. This challenge necessitates substantial investment in infrastructure and technological advancements to truly realize a circular economy for PVC.

Public perception and regulatory pressure also present formidable challenges to the PVC film market. The historical association of PVC with environmental concerns, such as the release of harmful chemicals during its production or disposal, has fostered a negative image among certain consumer groups and environmental organizations. This negative perception can influence consumer choices and prompt businesses to seek alternative materials to enhance their corporate sustainability image. Simultaneously, governments and regulatory bodies worldwide are imposing stricter environmental regulations on plastics, including PVC, covering aspects such as production processes, chemical additives, and end-of-life management. Compliance with these evolving regulations often requires significant capital investment in cleaner technologies and reformulation, increasing operational costs and potentially limiting market access for non-compliant products.

Furthermore, fluctuating energy costs and potential supply chain disruptions contribute to the operational challenges faced by PVC film manufacturers. The production of PVC is energy-intensive, and rising or volatile energy prices, especially for natural gas and electricity, directly impact manufacturing costs and profitability. Geopolitical instability, trade disputes, and global events like pandemics can disrupt the supply of key raw materials such as ethylene dichloride (EDC) and vinyl chloride monomer (VCM), leading to shortages and price spikes. Managing these external economic and logistical volatilities requires robust supply chain strategies, diversification of suppliers, and efficient inventory management to ensure continuous production and competitive pricing, all of which add complexity to market operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Disposal and Recycling Infrastructure | -1.1% | Global | Long-term (2025-2033) |

| Negative Public Perception | -0.9% | Developed countries, Europe | Persistent |

| Stringent Regulatory Pressure | -0.8% | Europe, North America, parts of Asia | Medium-term (2025-2029) |

| Fluctuating Raw Material & Energy Costs | -0.7% | Global | Short-term to Medium-term (2025-2027) |

| Competition from Sustainable Alternatives | -0.6% | Global | Long-term (2025-2033) |

Polyvinyl Chloride Film Market - Updated Report Scope

This report provides an in-depth analysis of the global Polyvinyl Chloride Film market, offering a comprehensive overview of its current size, historical trends, and future growth projections from 2025 to 2033. It examines key market dynamics, including drivers, restraints, opportunities, and challenges, alongside an assessment of the impact of emerging technologies such as Artificial Intelligence. The report segments the market by product type, application, and end-use industry across major global regions, identifying key growth areas and competitive landscapes to provide strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 31.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical Co., Ltd., Occidental Petroleum Corporation (OxyVinyls), Formosa Plastics Corporation, LG Chem, BASF SE, Westlake Chemical Corporation, Kaneka Corporation, Vynova Group, Mexichem (Orbia), INEOS Group Holdings S.A., Georgia Gulf Corporation (Axiall), Teknor Apex Company, K.S.R. Industries, Nan Ya Plastics Corporation, Alpha Marathon, Viewpoint Plastic Film, Wanhua Chemical Group Co., Ltd., Dalian Shide Group, Polyone Corporation (Avient), Sumitomo Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Polyvinyl Chloride (PVC) film market is extensively segmented to provide a detailed understanding of its diverse applications and product types, allowing for a granular analysis of market dynamics across various sectors. This segmentation helps identify specific growth drivers, market sizes, and emerging opportunities within each category, offering a comprehensive view of the industry's intricate structure. Understanding these distinct segments is crucial for manufacturers, suppliers, and investors to tailor strategies, optimize product portfolios, and target specific end-use industries with precision, ensuring that product development aligns with market demand and regulatory landscapes.

- By Type:

- Rigid PVC Film

- Flexible PVC Film

- Calendered PVC Film

- Extruded PVC Film

- Blown PVC Film

- By Application:

- Packaging

- Food Packaging

- Non-Food Packaging

- Pharmaceutical Packaging (Blister Packaging, IV Bags, Blood Bags)

- Construction

- Flooring

- Roofing

- Wall Coverings

- Window Profiles

- Electrical Insulation

- Automotive

- Interior Components (Dashboards, Door Panels)

- Protective Films

- Wire Harnesses

- Medical

- IV Bags

- Blood Bags

- Tubing

- Other Sterile Packaging

- Agriculture

- Greenhouse Films

- Silage Wraps

- Mulch Films

- Consumer Goods (Stationery, Toys, Apparel)

- Others (Promotional Materials, Industrial Covers)

- Packaging

- By End-Use Industry:

- Consumer Goods

- Healthcare & Pharmaceuticals

- Building & Construction

- Automotive

- Agriculture

- Industrial

- Others

Regional Highlights

- North America: A mature market characterized by innovation in specialized applications and a growing emphasis on sustainable PVC solutions. Significant demand from the healthcare, automotive, and construction sectors, driven by technological advancements and high consumer awareness regarding product quality. The region focuses on high-value applications and recycling initiatives.

- Europe: Marked by stringent environmental regulations and a strong push towards circular economy principles, leading to increased adoption of recycled and bio-based PVC films. Key markets include Germany, France, and the UK, with significant demand from packaging, medical, and construction industries, coupled with ongoing efforts to reduce environmental footprint.

- Asia Pacific (APAC): The largest and fastest-growing market, primarily driven by rapid industrialization, urbanization, and expanding manufacturing sectors in China, India, Japan, and Southeast Asian countries. Robust demand from construction, packaging, and automotive industries, coupled with lower production costs and increasing disposable incomes, fuels market expansion.

- Latin America: An emerging market experiencing steady growth due to increasing infrastructure development, particularly in Brazil and Mexico, and a rising demand for packaged goods. Economic development and urbanization are contributing to increased consumption across various end-use industries, presenting significant growth opportunities.

- Middle East and Africa (MEA): Showing nascent growth driven by investments in infrastructure projects, diversification of economies away from oil, and increasing healthcare spending. While smaller in market size currently, the region holds long-term potential as industrial and consumer sectors expand, leading to higher demand for PVC films in packaging and construction.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Polyvinyl Chloride Film Market.- Shin-Etsu Chemical Co., Ltd.

- Occidental Petroleum Corporation (OxyVinyls)

- Formosa Plastics Corporation

- LG Chem

- BASF SE

- Westlake Chemical Corporation

- Kaneka Corporation

- Vynova Group

- Mexichem (Orbia)

- INEOS Group Holdings S.A.

- Georgia Gulf Corporation (Axiall)

- Teknor Apex Company

- K.S.R. Industries

- Nan Ya Plastics Corporation

- Alpha Marathon

- Viewpoint Plastic Film

- Wanhua Chemical Group Co., Ltd.

- Dalian Shide Group

- Polyone Corporation (Avient)

- Sumitomo Chemical Co., Ltd.

Frequently Asked Questions

What is the current market size of Polyvinyl Chloride (PVC) film?

The Polyvinyl Chloride Film Market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 31.5 Billion by 2033, growing at a CAGR of 6.8%.

What are the primary applications driving the PVC film market growth?

Key growth drivers include expanding demand from the packaging industry (food, pharmaceutical), robust growth in construction (flooring, roofing), and increasing adoption in healthcare (IV bags, medical packaging) and automotive sectors.

How do environmental regulations impact the PVC film industry?

Environmental regulations, particularly concerning non-biodegradability and certain additives, pose significant restraints, driving manufacturers towards sustainable solutions, recycled PVC, and bio-based alternatives to ensure compliance and improve public perception.

What innovations are emerging in the PVC film sector?

Innovations include the development of bio-based and recycled PVC, advancements in co-extrusion and lamination technologies for enhanced film properties, and the exploration of niche applications such as smart films and anti-microbial variants.

Which regions exhibit the highest growth potential for PVC film?

Asia Pacific is the leading and fastest-growing region due to rapid industrialization and construction, while emerging economies in Latin America and MEA also present significant long-term growth opportunities driven by infrastructure development and rising consumption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted