Bentonite Market

Bentonite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678171 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

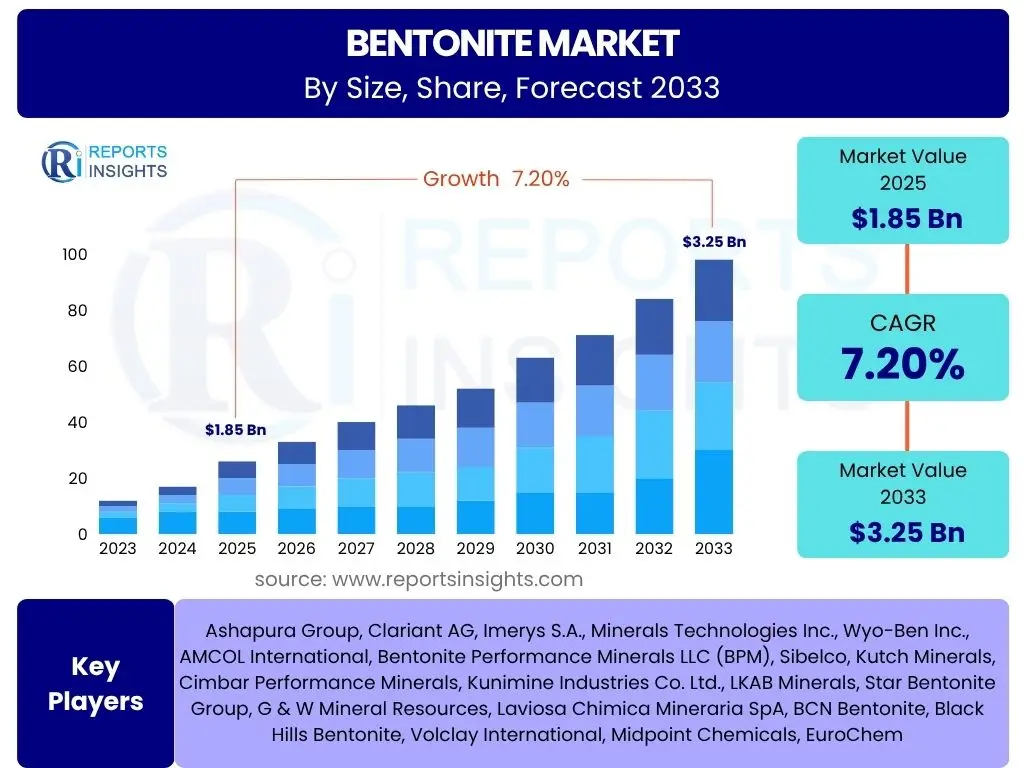

Bentonite Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, valued at USD 1.85 billion in 2025 and is projected to grow to USD 3.10 billion by 2033 at the end of the forecast period.

Key Bentonite Market Trends & Insights

The global bentonite market is experiencing dynamic shifts driven by evolving industrial demands and increasing sustainability focus. Key trends include the rising adoption of bentonite in specialized applications like pharmaceuticals and cosmetics, an emphasis on high-purity grades for advanced industrial processes, and the growing demand from the burgeoning infrastructure and construction sectors in emerging economies. Furthermore, advancements in drilling technologies for oil and gas exploration continue to bolster its consumption, while the agricultural sector increasingly leverages bentonite for soil conditioning and animal feed additives. The market is also seeing a trend towards efficient processing technologies to reduce environmental impact and optimize production costs.

- Growing demand from civil engineering and construction for waterproofing and sealing applications.

- Increased utilization in oil and gas drilling as a viscosifier and fluid loss control agent.

- Expanding adoption in the foundry industry for mold binding.

- Rising popularity in pet litter due to superior absorption properties.

- Emergence of new applications in pharmaceuticals, cosmetics, and environmental remediation.

- Focus on sustainable mining practices and value-added bentonite products.

- Shift towards specialized bentonite grades for high-performance applications.

- Influence of agricultural advancements on bentonite use for soil improvement and animal feed.

- Regional growth spurred by infrastructure development projects.

AI Impact Analysis on Bentonite

Artificial Intelligence (AI) is beginning to exert a transformative influence across various industrial sectors, and while its direct impact on raw material markets like bentonite may seem indirect, AI's applications in optimizing upstream and downstream processes are significant. AI can enhance exploration and mining efficiency, improve processing techniques, and revolutionize supply chain management, ultimately leading to more efficient resource utilization and reduced operational costs within the bentonite value chain. Predictive analytics, for instance, can forecast demand more accurately, enabling better inventory management and production planning. Moreover, AI-driven material science research may uncover new applications or optimize existing ones for bentonite, leading to innovative product development and market expansion.

- Optimizing bentonite mining operations through AI-driven geological data analysis and predictive maintenance for machinery.

- Enhancing bentonite processing efficiency using AI algorithms for quality control and process optimization, leading to higher purity and specialized grades.

- Improving supply chain logistics and demand forecasting for bentonite through AI-powered analytics, reducing waste and transportation costs.

- Accelerating research and development for new bentonite applications or enhanced formulations by leveraging AI for material simulation and discovery.

- Enabling more precise environmental monitoring and compliance in bentonite extraction and processing through AI-driven sensor networks and data analysis.

Key Takeaways Bentonite Market Size & Forecast

- The global bentonite market is poised for steady growth, driven by its versatile applications across multiple industries.

- Projected to reach a market valuation of USD 3.10 billion by 2033, demonstrating robust expansion over the forecast period.

- Compound Annual Growth Rate (CAGR) of 6.8% anticipated from 2025 to 2033, indicating a healthy market trajectory.

- Growth is primarily fueled by increasing demand from the construction, oil and gas, and foundry sectors.

- Emerging economies, particularly in Asia Pacific, are expected to be significant contributors to market expansion.

- Market forecast highlights sustained demand for bentonite as a crucial industrial mineral, underpinning various global industries.

Bentonite Market Drivers Impact Analysis

The bentonite market is significantly propelled by a confluence of factors stemming from its unique properties and extensive industrial applications. The burgeoning global construction and infrastructure development initiatives represent a primary driver, as bentonite is indispensable in civil engineering for diaphragm walls, tunneling, and waterproofing. Similarly, the ongoing activities in the oil and gas sector, particularly horizontal drilling and hydraulic fracturing, heavily rely on bentonite as a key component in drilling muds to maintain borehole stability and optimize drilling efficiency. Furthermore, the robust demand from the foundry industry for producing high-quality molds, coupled with its increasing use in environmental applications like wastewater treatment and landfill liners, collectively contribute to the market's upward trajectory. The diverse utility of bentonite across these critical sectors underscores its importance as a versatile industrial mineral, fostering consistent market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Construction and Civil Engineering Activities | +2.1% | Asia Pacific, North America, Europe (Urbanization, infrastructure projects) | Long-term (2025-2033) |

| Increasing Oil and Gas Drilling Activities | +1.8% | North America, Middle East & Africa, Latin America (Shale gas, conventional oil exploration) | Mid-to-long term (2025-2033) |

| Rising Demand from Foundry Industry | +1.2% | Asia Pacific, Europe (Automotive, machinery manufacturing) | Mid-term (2025-2030) |

| Expanding Pet Litter Market | +0.8% | North America, Europe (Increasing pet ownership, disposable income) | Long-term (2025-2033) |

| Growth in Agriculture and Environmental Applications | +0.9% | Global (Soil conditioning, wastewater treatment, animal feed) | Long-term (2025-2033) |

Bentonite Market Restraints Impact Analysis

Despite its broad utility, the bentonite market faces certain restraints that could temper its growth trajectory. Environmental regulations, particularly those pertaining to mining operations and land use, can significantly increase production costs and lead to delays in project approvals, thereby impacting supply. The availability and adoption of alternative materials in various applications, such as synthetic polymers in drilling fluids or other types of clays in foundry, pose a competitive threat to bentonite. Furthermore, the bulk nature of bentonite means that high transportation costs, especially over long distances from mining sites to consumption centers, can erode profit margins and make it less competitive in certain regions. These factors necessitate continuous innovation in processing and supply chain management to maintain bentonite's market competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations for Mining | -1.5% | Europe, North America (Permitting, land reclamation costs) | Long-term (2025-2033) |

| Availability of Substitute Materials | -1.0% | Global (Polymers in drilling, other clays in foundry) | Mid-to-long term (2025-2033) |

| High Transportation Costs | -0.8% | Regions far from major bentonite deposits (Logistics, fuel prices) | Ongoing (2025-2033) |

| Fluctuations in Raw Material Prices | -0.5% | Global (Market volatility, energy costs) | Short-to-mid term (2025-2028) |

Bentonite Market Opportunities Impact Analysis

Significant opportunities for growth exist within the bentonite market, primarily driven by innovations and expanding applications. The development of specialized bentonite grades tailored for high-value applications in pharmaceuticals, cosmetics, and advanced materials presents a promising avenue for market expansion and increased revenue. Furthermore, the growing global emphasis on sustainable practices and environmental protection creates demand for bentonite in areas such as groundwater purification, industrial wastewater treatment, and contaminated site remediation. Developing economies, undergoing rapid urbanization and industrialization, offer substantial untapped potential for bentonite consumption in construction, infrastructure, and oil and gas activities. Strategic investments in research and development aimed at enhancing bentonite's functional properties and exploring novel uses will be crucial for capitalizing on these emerging opportunities and driving future market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of New and Specialized Applications | +1.6% | Global (Pharmaceuticals, cosmetics, catalysts, advanced materials) | Long-term (2027-2033) |

| Increasing Demand from Emerging Economies | +1.3% | Asia Pacific, Latin America, Africa (Infrastructure, industrialization) | Long-term (2025-2033) |

| Focus on Sustainable and Green Solutions | +1.0% | Europe, North America, Asia Pacific (Environmental remediation, water treatment) | Mid-to-long term (2025-2033) |

| Technological Advancements in Processing | +0.7% | Global (Efficiency gains, purity improvement) | Mid-term (2025-2030) |

Bentonite Market Challenges Impact Analysis

The bentonite market faces several challenges that require strategic navigation for sustained growth. Disruptions in the global supply chain, often triggered by geopolitical events, natural disasters, or pandemics, can lead to significant volatility in material availability and pricing, impacting both production and delivery timelines. Fluctuations in energy costs, which are critical for mining, processing, and transportation of bentonite, directly influence operational expenses and can squeeze profit margins for market participants. Furthermore, maintaining consistent product quality across various geological deposits and processing methods remains a challenge, as end-use industries often demand specific purities and characteristics. Intense competition among existing players and the threat of new entrants in regions with accessible deposits also exert pressure on pricing and market share, necessitating continuous differentiation and cost efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Geopolitical Instability | -1.2% | Global (Freight availability, trade policies) | Short-to-mid term (2025-2028) |

| Volatile Energy Prices | -0.9% | Global (Production costs, transportation expenses) | Ongoing (2025-2033) |

| Maintaining Consistent Product Quality | -0.7% | Global (Processing complexity, varied deposits) | Long-term (2025-2033) |

| Intense Market Competition | -0.6% | Global (Pricing pressure, market saturation in mature regions) | Long-term (2025-2033) |

Bentonite Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global bentonite market, offering an in-depth analysis of its current landscape and future growth prospects. It provides a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages extensive primary and secondary research to deliver actionable insights, empowering stakeholders with the critical information needed for strategic decision-making. Through robust forecasting and competitive analysis, it aims to equip businesses with a clear understanding of market evolution and potential investment avenues within the bentonite industry.

| Report Attributes | Report Details |

|---|---|

| Report Name | Bentonite Market |

| Market Size in 2025 | USD 1.85 billion |

| Market Forecast in 2033 | USD 3.10 billion |

| Growth Rate | CAGR of 2025 to 2033 6.8% |

| Number of Pages | 150 |

| Key Companies Covered | Amcol(US), Bentonite Performance Minerals LLC(US), Wyo-Ben Inc(US), Black Hills Bentonite(US), Tolsa Group (Spain), Imerys (S&B) (France), Clariant (Switzerland), Bentonite Company LLC (Russia), Laviosa Minerals SpA (Italy), LKAB Minerals (Nerlands), Ashapura (India), Star Bentonite Group (India), Kunimine Industries (Japan), Huawei Bentonite (China), Fenghong New Material (China), Changan Renheng (China), Liufangzi Bentonite (China), Bentonit Uniao (Brazil), Castiglioni Pes y Cia (Argentina), Canbensan (Tur), Ayd?n Bentonit (Tur), KarBen (Tur), G & W Mineral Resources (South Africa), Ningcheng Tianyu (China) |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

The bentonite market is broadly segmented based on its inherent properties and diverse industrial utility, allowing for a granular understanding of demand patterns and growth drivers across different sectors. The classification by type distinguishes between sodium bentonite, known for its high swelling capacity and excellent colloidal properties, and calcium bentonite, recognized for its adsorptive capabilities. These distinct characteristics dictate their suitability for specific applications. Further segmentation by application provides insights into how bentonite is consumed across various industries, from large-volume uses in molding sands and drilling muds to specialized roles in pet litter and civil engineering. Understanding these segmentations is critical for market players to tailor their product offerings and strategic focus, addressing the precise needs of each end-use sector and leveraging the unique attributes of bentonite variants.

Market Product Type Segmentation:-- Sodium Bentonite

- Calcium Bentonite

- Molding Sands

- Iron Ore Pelletizing

- Pet Litter

- Drilling Mud

- Civil Engineering

- Agriculture

- Others

Regional Highlights

The global bentonite market exhibits distinct regional dynamics, influenced by geological endowments, industrial development, and regulatory landscapes. Each major region contributes uniquely to the market's overall growth, presenting varied opportunities and challenges for market participants. Understanding these regional specificities is vital for strategic planning, including optimizing supply chains, identifying key demand centers, and tailoring market entry strategies to local conditions. The presence of significant end-use industries and the pace of infrastructure development often determine the market's trajectory within a particular geographic area, making regional analysis a cornerstone of comprehensive market assessment.

- Asia Pacific: This region stands as a dominant force in the bentonite market, primarily driven by rapid industrialization, extensive infrastructure development, and burgeoning construction activities, particularly in countries like China and India. The region's growing oil and gas exploration, coupled with increasing demand from the foundry and agricultural sectors, fuels significant consumption.

- North America: A mature yet robust market, North America benefits from substantial oil and gas drilling operations, especially shale gas exploration, which heavily relies on bentonite for drilling fluids. The region also exhibits strong demand from the pet litter and civil engineering sectors, with continuous investment in infrastructure maintenance and new projects.

- Europe: The European market for bentonite is characterized by its focus on high-quality, specialized applications in areas such as environmental engineering, pharmaceuticals, and cosmetics, alongside its traditional use in foundries and civil construction. Stringent environmental regulations also drive demand for bentonite in wastewater treatment and landfill lining.

- Latin America: This region is emerging as a significant growth hub due to increasing investments in mining, oil and gas exploration, and infrastructure projects, particularly in countries like Brazil and Argentina. The agricultural sector's expansion also contributes to bentonite consumption for soil improvement and animal feed.

- Middle East & Africa (MEA): Rich in oil and gas reserves, the MEA region is a crucial consumer of bentonite for drilling mud applications. Growing construction and infrastructure development initiatives, especially in the GCC countries, further propel market demand. The region also presents opportunities in water treatment and agricultural applications.

Top Key Players:

The market research report covers the analysis of key stake holders of the Bentonite Market. Some of the leading players profiled in the report include -

- Amcol(US)

- Bentonite Performance Minerals LLC(US)

- Wyo-Ben Inc(US)

- Black Hills Bentonite(US)

- Tolsa Group (Spain)

- Imerys (S&B) (France)

- Clariant (Switzerland)

- Bentonite Company LLC (Russia)

- Laviosa Minerals SpA (Italy)

- LKAB Minerals (Nerlands)

- Ashapura (India)

- Star Bentonite Group (India)

- Kunimine Industries (Japan)

- Huawei Bentonite (China)

- Fenghong New Material (China)

- Changan Renheng (China)

- Liufangzi Bentonite (China)

- Bentonit Uniao (Brazil)

- Castiglioni Pes y Cia (Argentina)

- Canbensan (Tur)

- Ayd?n Bentonit (Tur)

- KarBen (Tur)

- G & W Mineral Resources (South Africa)

- Ningcheng Tianyu (China)

Frequently Asked Questions:

What is Bentonite and its primary uses?

Bentonite is an absorbent aluminum phyllosilicate clay formed from the alteration of volcanic ash, primarily composed of montmorillonite. Its primary uses are diverse, including as a drilling mud in oil and gas extraction, a binder in foundry molds, an absorbent for pet litter, a sealing agent in civil engineering and construction, and a soil conditioner in agriculture.

What is the projected growth rate for the Bentonite Market from 2025 to 2033?

The Bentonite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, indicating a steady expansion driven by increasing industrial demand and emerging applications.

Which regions are significant contributors to the Bentonite Market's growth?

Asia Pacific is a leading region due to rapid industrialization and infrastructure development. North America is significant for its oil and gas activities and pet litter market. Europe focuses on specialized applications, while Latin America and the Middle East & Africa show growth in mining, oil and gas, and construction sectors.

What are the key drivers propelling the Bentonite Market?

Key drivers include the expanding global construction and civil engineering sectors, increasing oil and gas drilling activities (especially shale exploration), robust demand from the foundry industry, and the growing pet litter market. Agricultural uses and environmental applications also significantly contribute to market growth.

What types of Bentonite are predominantly used in the market?

The two primary types of bentonite predominantly used in the market are Sodium Bentonite, known for its high swelling and colloidal properties, and Calcium Bentonite, valued for its adsorptive capabilities. Each type serves distinct industrial applications based on its unique characteristics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted