Photonic Chip Market

Photonic Chip Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704889 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Photonic Chip Market Size

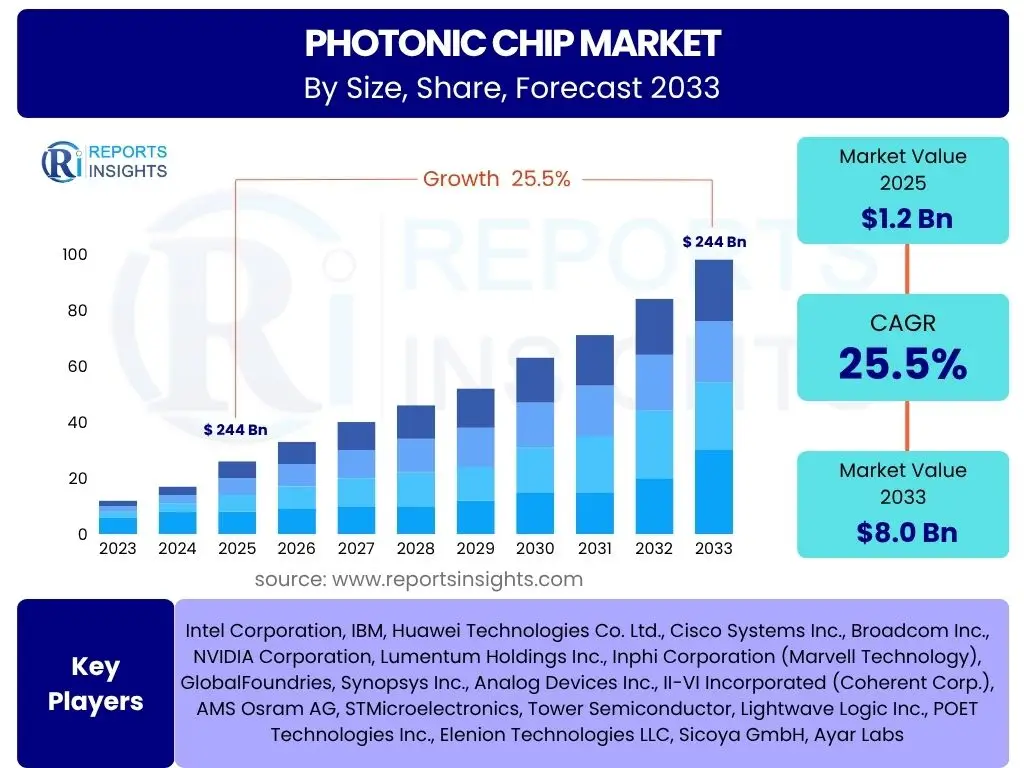

According to Reports Insights Consulting Pvt Ltd, The Photonic Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2033. The market is estimated at USD 1.2 billion in 2025 and is projected to reach USD 8.0 billion by the end of the forecast period in 2033.

Key Photonic Chip Market Trends & Insights

Users frequently inquire about the evolving landscape of photonic chip technology, seeking to understand the significant shifts and innovations driving the market. The industry is currently witnessing a profound integration of photonics into mainstream computing and communication infrastructures, propelled by the insatiable demand for higher bandwidth, lower latency, and superior energy efficiency. A key trend involves the maturation of silicon photonics, which leverages existing semiconductor manufacturing processes to reduce costs and enhance scalability, thereby making advanced optical functionalities more accessible for diverse applications. Furthermore, the convergence of photonic chips with artificial intelligence and quantum computing paradigms is opening new frontiers, particularly in specialized hardware for accelerated computation and secure communication.

Another prominent trend is the increasing miniaturization and integration of photonic components, leading to more compact and powerful devices. This advancement is critical for applications in consumer electronics, medical diagnostics, and advanced sensing, where space and power consumption are key constraints. The industry is also observing a growing emphasis on hybrid integration, combining different material platforms to optimize performance for specific functionalities, such as integrating indium phosphide lasers with silicon photonic waveguides. This hybrid approach allows designers to leverage the best properties of various materials, pushing the boundaries of what integrated photonics can achieve. The demand from data centers and telecommunications networks for faster data transfer rates is consistently driving the adoption of photonic chips, solidifying their role as foundational technology for the digital age.

- Maturation and widespread adoption of silicon photonics for cost-effective, scalable solutions.

- Increased integration of photonic chips into Artificial Intelligence (AI) and Machine Learning (ML) accelerators.

- Rising demand for high-speed, energy-efficient data communication in data centers and telecommunications.

- Advancements in hybrid integration techniques combining various material platforms for enhanced performance.

- Growing development of photonic sensors for healthcare, automotive, and environmental monitoring.

- Emergence of quantum photonic chips for quantum computing and secure communication.

AI Impact Analysis on Photonic Chip

Common user inquiries regarding the impact of Artificial Intelligence on photonic chips often center on how AI can accelerate photonic chip development and, conversely, how photonic chips are becoming indispensable for advanced AI computations. AI significantly influences the photonic chip market by driving an unprecedented demand for high-performance computing, necessitating architectures that can handle massive data volumes with minimal latency and power consumption. Photonic chips, with their inherent advantages in speed and energy efficiency, are ideally positioned to serve as the backbone for next-generation AI hardware, including neural network accelerators and specialized processors for deep learning algorithms. AI's computational needs are pushing the limits of traditional electronic chips, making optical interconnects and integrated photonic circuits vital for future data centers and AI supercomputers.

Moreover, AI is not just a consumer of photonic technology but also a catalyst for its innovation. Machine learning algorithms are increasingly being employed in the design, optimization, and manufacturing processes of photonic chips. This includes using AI for inverse design, where desired optical functionalities are translated into optimal chip geometries, and for defect detection and yield improvement in fabrication. The synergy between AI and photonics extends to novel computing paradigms such as optical neural networks and neuromorphic photonics, which aim to perform AI computations directly in the optical domain, promising orders of magnitude improvement in speed and energy efficiency compared to electronic counterparts. This symbiotic relationship positions AI as a pivotal force shaping both the demand for and the evolution of photonic chip technology.

- AI-driven demand for high-bandwidth, low-latency interconnects in data centers and cloud computing.

- Development of dedicated photonic AI accelerators for machine learning and deep learning workloads.

- Utilization of AI and machine learning in the design, simulation, and optimization of photonic chip architectures.

- Advancements in neuromorphic photonics for energy-efficient, optical AI computing.

- Increased research into quantum AI and its reliance on integrated photonic circuits for quantum information processing.

Key Takeaways Photonic Chip Market Size & Forecast

Users frequently seek a concise summary of the most critical insights from the photonic chip market size and forecast, focusing on the core implications for stakeholders and future developments. The primary takeaway is the exceptionally robust growth trajectory projected for the photonic chip market, indicating its transition from a niche technology to a foundational component across multiple industries. This growth is fundamentally driven by the escalating global demand for data bandwidth, fueled by widespread digital transformation, 5G deployment, the proliferation of IoT devices, and the exponential expansion of cloud services and artificial intelligence. The forecast underscores a clear market shift towards optical solutions for high-performance computing and communication, driven by the inherent limitations of traditional electronic circuitry in addressing future speed and power requirements.

Another crucial insight is the strategic importance of photonic chip technology for national competitiveness and technological leadership. Countries and major corporations are heavily investing in research and development, as well as manufacturing capabilities, recognizing that photonics will be critical for next-generation infrastructure, from secure communication to advanced medical diagnostics and autonomous systems. The market's diversification beyond traditional telecommunications into areas like sensing, quantum computing, and consumer electronics highlights its broad applicability and long-term potential. While challenges such as manufacturing complexity and integration hurdles persist, the overwhelming need for superior performance across data-intensive applications ensures a sustained upward trajectory for the photonic chip market, making it an attractive sector for innovation and investment.

- The photonic chip market is poised for significant, sustained growth driven by escalating global data traffic and the proliferation of AI workloads.

- Silicon photonics emerges as a dominant platform due to its scalability and compatibility with existing semiconductor infrastructure.

- Strategic investments in R&D and manufacturing are crucial for market players to capitalize on emerging opportunities.

- The technology's application scope is broadening beyond traditional telecom to include sensing, healthcare, and quantum computing.

- Energy efficiency and high bandwidth are primary drivers differentiating photonic chips from electronic counterparts, making them essential for future computing.

Photonic Chip Market Drivers Analysis

The photonic chip market is propelled by several robust drivers, primarily stemming from the increasing global reliance on data and high-speed communication. The burgeoning demand for bandwidth-intensive applications such as cloud computing, artificial intelligence, and big data analytics necessitates optical interconnects that can outperform traditional electronic solutions in terms of speed, energy efficiency, and data throughput. Furthermore, the rapid deployment of 5G networks globally is creating an urgent need for advanced optical components that can handle the massive data traffic generated at the edge and core of these networks. These technological advancements are foundational in pushing the boundaries of what is possible in data communication and processing.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand for High-Speed Data Communication | +5.0% | Global, North America, Asia Pacific | 2025-2033 |

| Proliferation of Artificial Intelligence and Machine Learning | +4.5% | Global, North America, Europe | 2025-2033 |

| Expansion of Data Centers and Cloud Infrastructure | +4.0% | Global, Asia Pacific, North America | 2025-2033 |

| Deployment of 5G and Next-Generation Communication Networks | +3.5% | Global, Asia Pacific, Europe | 2025-2033 |

| Advancements in Quantum Computing and Neuromorphic Computing | +2.5% | North America, Europe | 2028-2033 |

Photonic Chip Market Restraints Analysis

Despite significant growth potential, the photonic chip market faces several restraints that could impede its expansion. One of the primary challenges is the high manufacturing cost associated with photonic integrated circuits (PICs), particularly for advanced material platforms like Indium Phosphide, which can limit their widespread adoption in cost-sensitive applications. The complexity of integrating photonic components with existing electronic systems also presents a significant hurdle, requiring specialized design tools and expertise that are not universally available. These factors contribute to slower adoption rates in some sectors and demand ongoing innovation to overcome.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Photonic Integrated Circuits | -3.0% | Global, Europe | 2025-2030 |

| Complexity of Integration with Existing Electronic Systems | -2.5% | Global, North America | 2025-2030 |

| Lack of Standardization Across Different Material Platforms | -2.0% | Global | 2025-2033 |

| Limited Availability of Skilled Workforce and Expertise | -1.5% | Global, Emerging Markets | 2025-2033 |

Photonic Chip Market Opportunities Analysis

The photonic chip market is rich with significant opportunities for innovation and growth, driven by emerging applications and technological advancements. The development of new use cases in sectors like autonomous vehicles (LiDAR), advanced medical diagnostics (biosensors), and consumer electronics (AR/VR devices) presents substantial untapped market segments. Furthermore, ongoing research into novel materials and advanced packaging techniques promises to enhance performance, reduce costs, and expand the functionality of photonic chips, opening doors for broader commercialization. These opportunities are critical for stakeholders seeking to diversify their portfolios and capture new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Applications (LiDAR, Biosensors, AR/VR) | +3.0% | Global, North America, Asia Pacific | 2028-2033 |

| Advancements in Hybrid and Heterogeneous Integration | +2.5% | Global, Europe | 2025-2033 |

| Increased Government Funding for Photonics Research and Development | +2.0% | North America, Europe, Asia Pacific | 2025-2033 |

| Miniaturization and Cost Reduction Through Advanced Manufacturing | +1.5% | Global, Asia Pacific | 2025-2030 |

Photonic Chip Market Challenges Impact Analysis

Despite its promise, the photonic chip market encounters several challenges that require strategic navigation. The inherent complexity of fabricating photonic components, which often demands ultra-high precision and sophisticated lithography techniques, can lead to lower yields and increased production costs compared to conventional electronics. Scaling up production to meet future demand remains a significant hurdle, as current manufacturing capacities for advanced photonic chips are limited. Furthermore, achieving seamless and efficient integration of photonic chips with existing electronic systems, particularly at the package level, poses considerable engineering challenges. Addressing these complexities is vital for the market to realize its full potential and achieve widespread adoption across diverse industries.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexities in Fabrication and Manufacturing Processes | -3.5% | Global | 2025-2030 |

| Scalability Issues for Mass Production and High Volume | -3.0% | Global, Asia Pacific | 2025-2033 |

| Thermal Management and Power Dissipation in High-Density Integration | -2.0% | Global | 2025-2033 |

| Interoperability and Ecosystem Development Across Different Vendors | -1.5% | Global | 2025-2033 |

Photonic Chip Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Photonic Chip Market, offering detailed insights into its size, growth trends, competitive landscape, and future projections. The report segments the market extensively by component, application, material, and end-user, providing a granular view of market dynamics across various dimensions. It also covers key regional insights, highlighting the growth opportunities and challenges specific to North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The study incorporates a thorough examination of market drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 8.0 Billion |

| Growth Rate | 25.5% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, IBM, Huawei Technologies Co. Ltd., Cisco Systems Inc., Broadcom Inc., NVIDIA Corporation, Lumentum Holdings Inc., Inphi Corporation (Marvell Technology), GlobalFoundries, Synopsys Inc., Analog Devices Inc., II-VI Incorporated (Coherent Corp.), AMS Osram AG, STMicroelectronics, Tower Semiconductor, Lightwave Logic Inc., POET Technologies Inc., Elenion Technologies LLC, Sicoya GmbH, Ayar Labs |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global photonic chip market is comprehensively segmented to provide a detailed understanding of its diverse applications and technological underpinnings. This segmentation allows for a granular analysis of market dynamics, identifying key growth areas and niche opportunities across various industries. The market is primarily broken down by components, applications, the materials used in chip fabrication, and the ultimate end-user industries, reflecting the broad utility and technological versatility of photonic chips. Each segment highlights specific market drivers and challenges, enabling a more targeted approach to market strategy and investment.

- By Component:

- Lasers

- Modulators

- Detectors

- Waveguides

- Optical Filters

- Others (e.g., Couplers, Mux/Demux)

- By Application:

- Data Centers & High-Performance Computing (HPC)

- Telecommunications

- Medical & Life Sciences (e.g., Biosensors, Imaging)

- Sensing & Imaging (e.g., LiDAR, Spectroscopy)

- Defense & Aerospace

- Consumer Electronics (e.g., AR/VR, Smartphones)

- Others (e.g., Industrial, Energy)

- By Material:

- Silicon

- Indium Phosphide (InP)

- Gallium Arsenide (GaAs)

- Silicon Nitride (SiN)

- Lithium Niobate (LN)

- Others (e.g., Gallium Nitride, Polymers)

- By End-User:

- IT & Telecommunications

- Healthcare

- Automotive

- Industrial

- Consumer

Regional Highlights

- North America: This region is a dominant force in the photonic chip market, characterized by significant investments in research and development, a strong presence of leading technology companies, and early adoption of advanced computing and communication infrastructure. The high concentration of data centers, the rapid integration of AI technologies, and ongoing innovations in quantum computing contribute substantially to market growth. Extensive government funding for photonics research further solidifies North America's leadership position.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by massive investments in 5G infrastructure, the burgeoning number of data centers, and a robust electronics manufacturing ecosystem. Countries like China, South Korea, and Japan are at the forefront of adopting and developing photonic technologies due to their large consumer bases and aggressive digital transformation agendas. The increasing demand for high-speed connectivity and AI integration across various industries fuels the rapid expansion of the photonic chip market here.

- Europe: The European market demonstrates steady growth, supported by strong government initiatives aimed at fostering innovation in photonics, particularly in industrial and automotive applications. Europe is a hub for advanced manufacturing and boasts significant research capabilities in integrated photonics. The region's focus on sustainable and energy-efficient technologies also drives the adoption of photonic chips, especially in telecommunications and sensing applications, contributing to its consistent market development.

- Latin America: While currently a smaller market, Latin America is expected to witness gradual growth, primarily due to increasing digitalization, expanding internet penetration, and investments in telecommunications infrastructure. The demand for enhanced data center capabilities and connectivity in urban areas will slowly drive the adoption of photonic chips.

- Middle East and Africa (MEA): The MEA region is at an nascent stage but holds potential due to ongoing smart city initiatives, diversification of economies away from oil, and increasing investments in IT and telecom infrastructure. Countries like UAE and Saudi Arabia are leading the adoption of advanced technologies, which will eventually include photonic chips for high-speed data transmission and sensing applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Photonic Chip Market.- Intel Corporation

- IBM

- Huawei Technologies Co. Ltd.

- Cisco Systems Inc.

- Broadcom Inc.

- NVIDIA Corporation

- Lumentum Holdings Inc.

- Inphi Corporation (Marvell Technology)

- GlobalFoundries

- Synopsys Inc.

- Analog Devices Inc.

- II-VI Incorporated (Coherent Corp.)

- AMS Osram AG

- STMicroelectronics

- Tower Semiconductor

- Lightwave Logic Inc.

- POET Technologies Inc.

- Elenion Technologies LLC

- Sicoya GmbH

- Ayar Labs

Frequently Asked Questions

What are the primary applications of photonic chips?

Photonic chips are primarily used for high-speed data communication in data centers and telecommunication networks, offering significant advantages in bandwidth and energy efficiency over traditional electronics. Beyond these core applications, they are increasingly vital in advanced sensing for automotive (LiDAR), medical diagnostics (biosensors), and environmental monitoring. They also play a crucial role in the emerging fields of artificial intelligence acceleration, quantum computing, and augmented/virtual reality devices, enabling faster computation and more immersive experiences.

How do photonic chips differ from traditional electronic chips?

The fundamental difference lies in their operational medium: photonic chips use photons (light particles) to transmit and process information, whereas electronic chips rely on electrons (electrical signals). This distinction allows photonic chips to offer superior speed, higher bandwidth, and lower power consumption due to the inherent properties of light. They also generate less heat, enabling higher integration density and reducing cooling requirements, which is a critical advantage for data-intensive applications and high-performance computing.

What materials are commonly used in the manufacturing of photonic chips?

The most common material for photonic chip manufacturing is silicon, owing to its compatibility with existing semiconductor fabrication processes, which makes silicon photonics a cost-effective and scalable solution. Other significant materials include Indium Phosphide (InP) and Gallium Arsenide (GaAs), which are prized for their excellent light-emitting and detecting properties, making them ideal for integrated lasers and detectors. Silicon Nitride (SiN) and Lithium Niobate (LN) are also gaining prominence for their ultra-low loss and high-speed modulation capabilities, expanding the range of applications for photonic integrated circuits.

What is the future outlook for the photonic chip market?

The future outlook for the photonic chip market is exceptionally positive, characterized by strong, sustained growth. This trajectory is driven by the escalating global demand for high-speed data, the imperative for energy-efficient computing, and the transformative impact of artificial intelligence and quantum technologies. As traditional electronic chips approach their physical limits, photonic chips are poised to become indispensable components for next-generation data centers, advanced communication networks, and innovative sensing solutions across various industries. Continuous advancements in materials, manufacturing techniques, and integration methods will further accelerate market expansion.

What are the main challenges impacting the widespread adoption of photonic chips?

Despite their significant advantages, photonic chips face several key challenges that influence their widespread adoption. These include the relatively high manufacturing costs associated with advanced photonic integration processes, which can be more complex and specialized than traditional electronic chip fabrication. Integrating photonic components seamlessly with existing electronic systems also poses a significant engineering hurdle, requiring specialized design tools and expertise. Additionally, achieving industry-wide standardization across different material platforms and ensuring robust thermal management in highly integrated designs are ongoing challenges that the market is actively addressing through research and development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted