Silicon Photonic Market

Silicon Photonic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704205 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

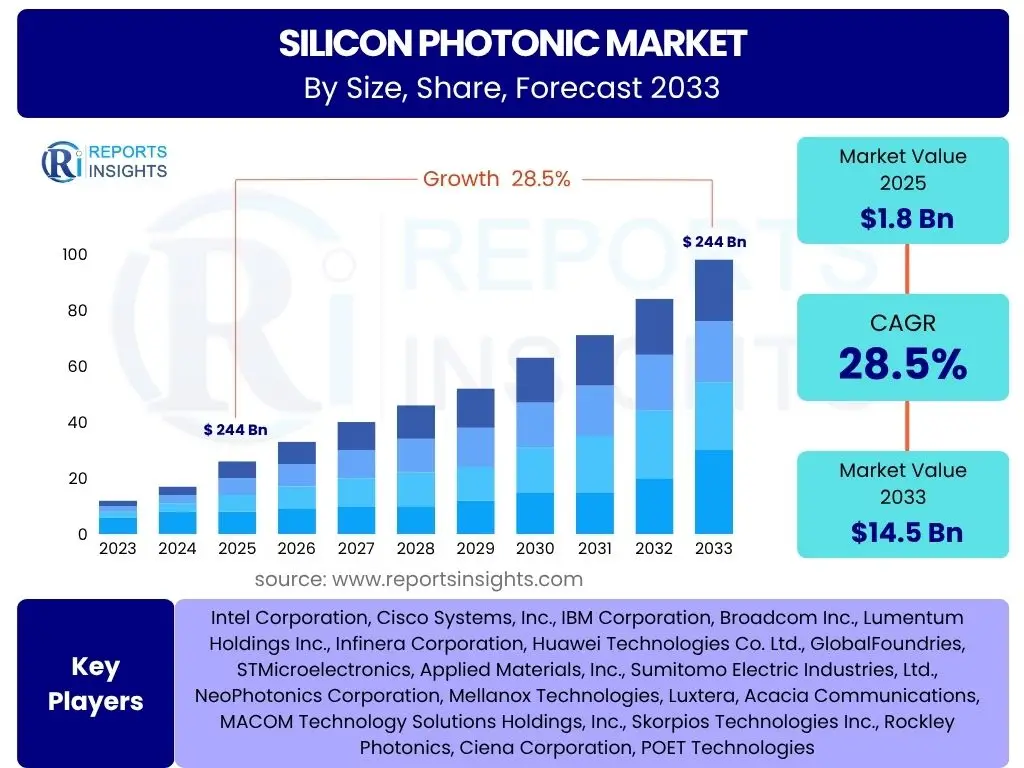

Silicon Photonic Market Size

According to Reports Insights Consulting Pvt Ltd, The Silicon Photonic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 14.5 Billion by the end of the forecast period in 2033.

Key Silicon Photonic Market Trends & Insights

User inquiries regarding Silicon Photonic market trends consistently highlight the accelerating demand for high-speed, energy-efficient data communication and processing capabilities. There is significant interest in how technological advancements are driving miniaturization, integration, and performance improvements across various applications. Users frequently seek insights into the market's trajectory concerning emerging applications like Artificial Intelligence (AI) acceleration, quantum computing, and advanced sensing, alongside the continued expansion in traditional sectors such as data centers and telecommunications.

The market is witnessing a strong shift towards co-packaged optics (CPO) and optical interconnects, which are crucial for overcoming electrical bandwidth limitations and reducing power consumption in next-generation computing infrastructures. Furthermore, the convergence of photonics with electronics on a single silicon platform is a dominant theme, promising enhanced performance and reduced manufacturing costs. Innovations in material science and fabrication techniques are also pivotal, enabling the development of more complex and higher-performing photonic integrated circuits (PICs) that can address diverse industrial requirements, from medical diagnostics to autonomous vehicles.

- Exponential growth in data center traffic driving demand for high-bandwidth interconnects.

- Increased adoption of silicon photonics in Artificial Intelligence (AI) and Machine Learning (ML) accelerators.

- Advancements in co-packaged optics (CPO) and hybrid integration techniques.

- Expansion into new application areas such as automotive LiDAR, quantum computing, and biosensing.

- Focus on energy efficiency and reduction of power consumption in optical communication systems.

AI Impact Analysis on Silicon Photonic

Common user questions related to the impact of Artificial Intelligence (AI) on Silicon Photonic technology primarily revolve around how AI's insatiable demand for computational power and data throughput is influencing the design and adoption of photonic solutions. Users are keen to understand if silicon photonics can provide the necessary bandwidth and low latency required for AI workloads, especially for inter-chip and intra-data center communication. There is also significant interest in the potential of AI to drive innovation within silicon photonics itself, perhaps through AI-driven design optimization or advanced manufacturing processes.

The proliferation of AI and Machine Learning (ML) applications necessitates processing massive datasets with unprecedented speed, leading to a bottleneck in traditional electrical interconnects. Silicon photonics offers a compelling solution by providing ultra-high bandwidth, low power consumption, and reduced latency, making it ideal for high-performance computing (HPC) and AI data centers. As AI models become more complex and require greater parallelism, the demand for optical interconnects supporting peta-bit scale data transfer will continue to surge. This symbiotic relationship positions silicon photonics as a foundational technology for the future of AI infrastructure.

- Drives demand for high-bandwidth, low-latency optical interconnects in AI clusters.

- Enables energy-efficient data transfer for large-scale AI model training and inference.

- Facilitates the development of specialized photonic AI accelerators and co-processors.

- Accelerates the integration of optics directly into AI computing units.

- Mitigates power consumption challenges associated with increasing AI computational loads.

Key Takeaways Silicon Photonic Market Size & Forecast

User inquiries about key takeaways from the Silicon Photonic market size and forecast consistently highlight the market's significant growth potential and its pivotal role in addressing the escalating demands of data communication. Users are keen to understand the primary drivers behind this expansion, the long-term sustainability of the growth trajectory, and the strategic implications for businesses and investors. Insights sought often include identifying the most impactful application segments and understanding the technological shifts that will define future market leadership.

The forecast indicates a robust Compound Annual Growth Rate (CAGR) of 28.5% through 2033, underscoring the indispensable nature of silicon photonics in evolving digital infrastructures. This growth is fundamentally driven by the relentless increase in global data traffic, the widespread adoption of cloud computing, and the transformative impact of emerging technologies like Artificial Intelligence (AI) and 5G. The market’s expansion signals a profound shift from traditional electronic-based communication to more efficient, high-speed optical solutions, making silicon photonics a critical area for technological investment and strategic development across various industries.

- The Silicon Photonic market is poised for exceptional growth, driven by fundamental shifts in data infrastructure requirements.

- Significant investment and innovation are concentrated on enhancing data center and telecommunication network capabilities.

- Integration with Artificial Intelligence and Machine Learning is a core catalyst for market acceleration.

- The transition towards more energy-efficient and higher-density optical components is a long-term strategic imperative.

- Technological advancements like co-packaged optics are vital for sustaining growth and overcoming scalability challenges.

Silicon Photonic Market Drivers Analysis

The Silicon Photonic market is primarily driven by the exponential growth in global data traffic, spurred by the proliferation of cloud computing, streaming services, and the Internet of Things (IoT). As data volumes continue to surge, traditional electrical interconnects are reaching their physical limits in terms of bandwidth, speed, and power efficiency. Silicon photonics offers a viable solution by enabling ultra-high-speed data transmission with significantly lower power consumption, addressing the critical needs of hyperscale data centers and communication networks.

Another significant driver is the increasing demand for high-speed and energy-efficient data communication within and between data centers. The deployment of 5G networks and the ongoing development of Artificial Intelligence (AI) and Machine Learning (ML) applications further intensify this demand, requiring faster, more compact, and more power-efficient optical transceivers. The inherent advantages of silicon photonics, such as its compatibility with existing CMOS manufacturing processes and its potential for high-volume, low-cost production, make it an attractive technology for scaling these critical infrastructures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth in Data Traffic and Cloud Computing | +3.0% | Global | 2025-2033 |

| Increasing Demand for High-Speed and Energy-Efficient Data Communication | +2.5% | North America, Asia Pacific | 2025-2030 |

| Emergence of Artificial Intelligence (AI) and Machine Learning (ML) Workloads | +2.0% | US, China | 2025-2033 | Advancements in Co-packaged Optics (CPO) and Optical Interconnects | +1.5% | Europe, Asia Pacific | 2026-2031 |

Silicon Photonic Market Restraints Analysis

Despite its significant advantages, the Silicon Photonic market faces several notable restraints. One primary challenge is the relatively high manufacturing costs and complex fabrication processes involved in producing silicon photonic devices. While leveraging existing CMOS infrastructure offers a long-term cost advantage, the initial investment in specialized equipment and the intricacies of integrating optical components with electronic circuits can be substantial. This complexity often leads to higher per-unit costs compared to traditional electronic components, particularly for low-volume applications, which can hinder wider adoption.

Another significant restraint is the ongoing challenge of seamlessly integrating silicon photonic devices with existing electronic systems. While silicon offers a promising platform, achieving efficient optical-to-electrical and electrical-to-optical conversion, alongside robust packaging and thermal management, remains a technical hurdle. These integration complexities can increase design cycles, development costs, and potentially impact overall system reliability. Furthermore, the market faces competition from established electronic solutions that, while less efficient at high speeds, benefit from mature supply chains and lower immediate implementation costs for certain applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Complex Fabrication Processes | -1.8% | Global | 2025-2027 |

| Integration Challenges with Existing Electronic Systems | -1.5% | Global | 2025-2029 |

| Thermal Management Issues in High-Density Integration | -1.0% | North America, Asia Pacific | 2025-2033 |

Silicon Photonic Market Opportunities Analysis

The Silicon Photonic market is presented with significant opportunities arising from its potential to expand into entirely new application areas beyond traditional data communications. Emerging fields such as quantum computing, advanced medical diagnostics, and autonomous vehicles are increasingly recognizing the unparalleled precision, speed, and miniaturization capabilities offered by silicon photonics. In quantum computing, photonic circuits are crucial for qubit manipulation and entanglement, while in medical technology, they can enable highly sensitive biosensors and imaging systems, opening up entirely new revenue streams and market segments.

Furthermore, continuous advancements in miniaturization and hybrid integration technologies offer substantial growth opportunities. As research and development efforts lead to smaller, more complex, and more efficient photonic integrated circuits (PICs), the scope for embedding silicon photonics into a wider array of consumer electronics and specialized industrial equipment expands. The drive towards more sophisticated sensing capabilities in sectors like environmental monitoring, industrial automation, and smart cities also positions silicon photonics favorably, allowing for the development of compact, highly sensitive, and cost-effective sensor solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas (e.g., LiDAR, Quantum Computing, MedTech) | +2.2% | Global | 2027-2033 |

| Further Miniaturization and Hybrid Integration Technologies | +1.8% | Europe, Asia Pacific | 2026-2032 |

| Growing Demand for Photonic Sensors in IoT and Automotive | +1.5% | North America, Europe | 2028-2033 |

Silicon Photonic Market Challenges Impact Analysis

The Silicon Photonic market faces several significant challenges that could impede its widespread adoption and growth. One key challenge is the lack of universally standardized platforms and a fully mature ecosystem. Unlike the electronics industry, which benefits from highly standardized manufacturing processes and design tools, silicon photonics still operates with a degree of fragmentation. This lack of broad standardization can lead to interoperability issues, increase development costs, and slow down time-to-market for new products, particularly for smaller innovators or those seeking to integrate components from multiple vendors.

Another substantial challenge lies in addressing yield and reliability issues during mass production. While silicon photonics leverages CMOS fabrication, the integration of optical components introduces new complexities that can affect manufacturing yields. Achieving consistent performance and high reliability for millions of integrated photonic devices remains a technical hurdle. Furthermore, the specialized nature of silicon photonics requires a highly skilled workforce with expertise spanning optics, electronics, and semiconductor manufacturing. The shortage of such specialized talent can constrain research, development, and mass production capabilities, impacting the market's ability to scale efficiently and meet burgeoning demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardized Platforms and Ecosystem Development | -1.7% | Global | 2025-2029 |

| Yield and Reliability Issues in Mass Production | -1.3% | Asia Pacific, Global | 2025-2027 |

| Shortage of Skilled Workforce and Expertise | -1.0% | North America, Europe | 2025-2033 |

Silicon Photonic Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Silicon Photonic market, offering a detailed understanding of its current landscape, historical performance, and future growth trajectory. It encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges that influence market evolution. The report segments the market extensively by components, applications, end-user industries, and product types, providing granular insights into each segment's contribution and growth potential. Furthermore, it delivers a critical assessment of the competitive landscape, profiling key market participants and highlighting their strategic initiatives and market positioning across major geographical regions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 14.5 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Cisco Systems, Inc., IBM Corporation, Broadcom Inc., Lumentum Holdings Inc., Infinera Corporation, Huawei Technologies Co. Ltd., GlobalFoundries, STMicroelectronics, Applied Materials, Inc., Sumitomo Electric Industries, Ltd., NeoPhotonics Corporation, Mellanox Technologies, Luxtera, Acacia Communications, MACOM Technology Solutions Holdings, Inc., Skorpios Technologies Inc., Rockley Photonics, Ciena Corporation, POET Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Silicon Photonic market is comprehensively segmented to provide a detailed understanding of its diverse components and applications, enabling precise market analysis and strategic planning. This segmentation facilitates the identification of key growth areas, emerging opportunities, and market dynamics specific to various industries and product types. By breaking down the market into its constituent parts, stakeholders can gain targeted insights into consumer needs, technological preferences, and competitive landscapes across different verticals.

The primary segments include categorization by component, such as modulators and photodetectors, which are fundamental building blocks of silicon photonic devices. Applications range from high-speed data communication and telecommunications infrastructure to advanced sensing and emerging biomedical uses. Furthermore, end-user industries, including hyperscale data centers, healthcare, and automotive, define the demand drivers for specific silicon photonic solutions. Product types like transceivers and switches represent the tangible output of this technology, showcasing the varied forms in which silicon photonics is integrated into modern systems.

- By Component: Silicon Optical Modulators, Silicon Photodetectors, Silicon Optical Filters, Silicon Optical Switches, Others

- By Application: Data Communication, Telecommunication, Sensing, Biomedical, Consumer Electronics, Others

- By End-User Industry: Data Centers, Telecommunications, Healthcare, Automotive, Aerospace & Defense, Consumer Electronics, Others

- By Product Type: Transceivers, Variable Optical Attenuators (VOAs), Switches, Multiplexer-Demultiplexer (Mux/DeMux), Cables, Others

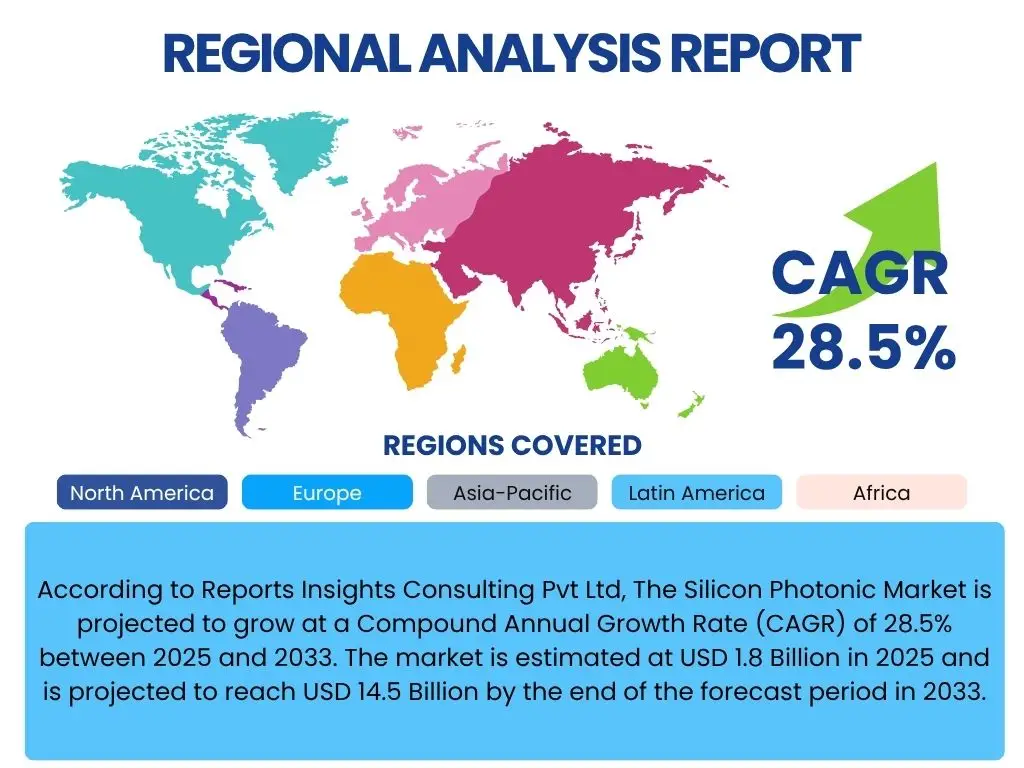

Regional Highlights

The Silicon Photonic market exhibits significant regional variations, influenced by factors such as technological infrastructure development, investment in data centers, government initiatives, and the presence of key industry players. North America, particularly the United States, stands as a dominant region due to its pioneering role in cloud computing, advanced research in AI, and substantial investments in high-speed communication networks. The presence of major technology corporations and a robust venture capital ecosystem further accelerates the adoption and innovation of silicon photonics in this region.

Asia Pacific is rapidly emerging as a high-growth region, primarily driven by massive investments in telecommunication infrastructure, the expansion of hyperscale data centers in countries like China and Japan, and the proliferation of 5G technology. Government support for indigenous semiconductor and photonics industries, coupled with a large manufacturing base, is fueling the regional market. Europe also demonstrates significant activity, with strong research capabilities and a focus on industrial automation and quantum technologies, contributing to the development and deployment of silicon photonic solutions across various applications.

- North America: Leading region due to extensive data center expansion, AI/ML adoption, and strong R&D infrastructure, particularly in the United States.

- Asia Pacific (APAC): Fastest-growing region driven by massive investments in telecommunications, 5G deployment, and expanding cloud services in countries like China, Japan, and South Korea.

- Europe: Significant advancements in quantum computing, advanced sensing, and industrial applications, with notable contributions from countries such as Germany and the UK.

- Latin America: Emerging market with increasing internet penetration and growing demand for data infrastructure, though at an earlier stage of adoption.

- Middle East and Africa (MEA): Gradual adoption spurred by digitalization initiatives and development of smart cities, with potential for future growth in data centers and telecom.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Silicon Photonic Market.- Intel Corporation

- Cisco Systems, Inc.

- IBM Corporation

- Broadcom Inc.

- Lumentum Holdings Inc.

- Infinera Corporation

- Huawei Technologies Co. Ltd.

- GlobalFoundries

- STMicroelectronics

- Applied Materials, Inc.

- Sumitomo Electric Industries, Ltd.

- NeoPhotonics Corporation

- Mellanox Technologies

- Luxtera

- Acacia Communications

- MACOM Technology Solutions Holdings, Inc.

- Skorpios Technologies Inc.

- Rockley Photonics

- Ciena Corporation

- POET Technologies

Frequently Asked Questions

Analyze common user questions about the Silicon Photonic market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is silicon photonics and why is it important?

Silicon photonics is a technology that integrates optical components onto a silicon chip, leveraging existing semiconductor manufacturing processes. It is crucial for high-speed data transmission, enabling faster and more energy-efficient communication compared to traditional electronics, essential for modern data centers and telecommunications.

What are the primary applications of silicon photonics?

The primary applications include high-bandwidth data communication in hyperscale data centers, telecommunication networks (especially 5G), advanced sensing (e.g., LiDAR for autonomous vehicles), biomedical devices, and emerging areas like Artificial Intelligence accelerators and quantum computing.

How does silicon photonics contribute to energy efficiency?

Silicon photonics reduces energy consumption by replacing electrical signals with light for data transfer, significantly lowering power dissipation, particularly at high data rates. This is vital for reducing the carbon footprint and operational costs of large data centers and communication infrastructures.

What are the main challenges hindering the broader adoption of silicon photonics?

Key challenges include high manufacturing costs and complex fabrication processes, difficulties in integrating photonic components with existing electronic systems, issues related to thermal management in high-density integration, and the need for standardized platforms and a skilled workforce.

What is the future outlook for the silicon photonic market?

The silicon photonic market is projected for substantial growth, driven by the increasing demand for data, AI integration, and the expansion of 5G networks. Continuous technological advancements, such as co-packaged optics and further miniaturization, are expected to open up new application areas and solidify its role as a foundational technology for future digital infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted