Autonomou Car Chip Market

Autonomou Car Chip Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704928 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

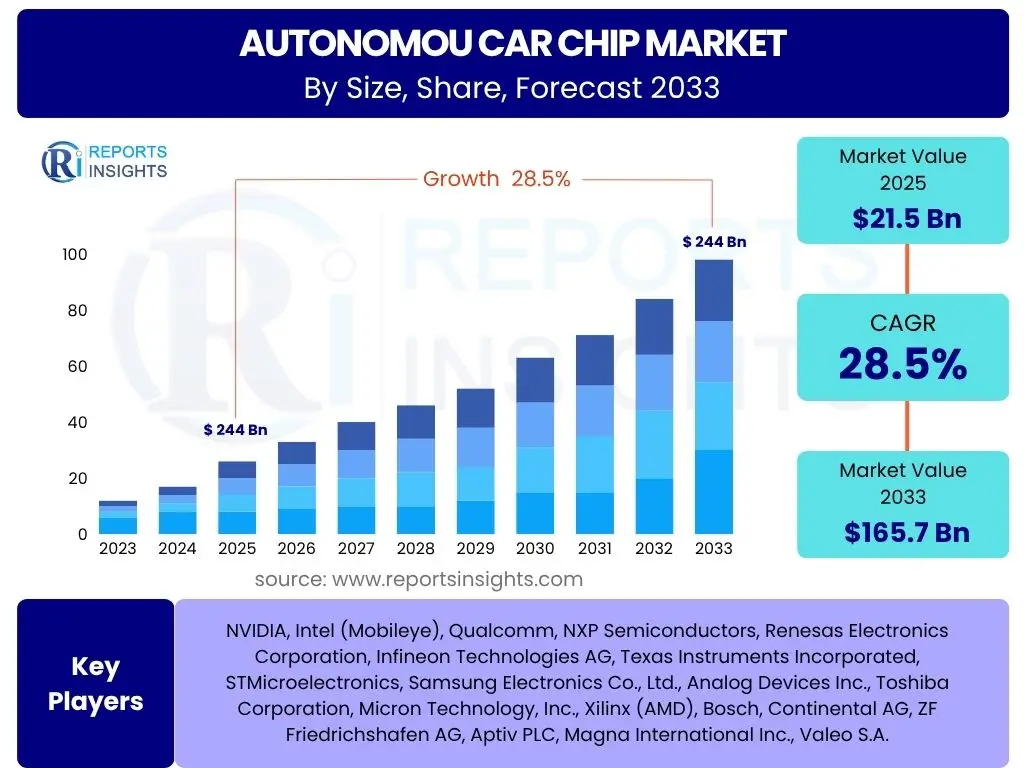

Autonomou Car Chip Market Size

According to Reports Insights Consulting Pvt Ltd, The Autonomou Car Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 21.5 Billion in 2025 and is projected to reach USD 165.7 Billion by the end of the forecast period in 2033.

Key Autonomou Car Chip Market Trends & Insights

User queries frequently highlight the rapid evolution of silicon architectures and software paradigms as central to the autonomous vehicle ecosystem. There is significant interest in how these advancements are shaping the capabilities and safety of self-driving cars. Emerging themes include the convergence of AI and high-performance computing (HPC) at the edge, the imperative for robust functional safety, and the shift towards software-defined vehicle architectures, which necessitate more versatile and powerful chip designs. The market is witnessing a profound transformation driven by the quest for higher autonomy levels and the integration of sophisticated sensor fusion technologies.

Another key area of user inquiry revolves around the industry's response to increasing complexity. There's a clear trend towards highly integrated System-on-Chips (SoCs) and specialized accelerators designed specifically for autonomous driving workloads, moving away from general-purpose processors for critical functions. Furthermore, the importance of redundant systems and fail-operational capabilities is paramount, influencing chip design to prioritize reliability and safety above all. The push for energy efficiency in these powerful chips is also a prominent concern, as it directly impacts vehicle range and thermal management challenges.

- Integration of high-performance System-on-Chips (SoCs) and Application-Specific Integrated Circuits (ASICs) for dedicated autonomous driving tasks.

- Shift towards software-defined vehicle architectures, demanding flexible and upgradable chip platforms.

- Increasing adoption of AI accelerators and neural processing units (NPUs) for real-time perception and decision-making.

- Emphasis on functional safety (ISO 26262) and cybersecurity within chip design and manufacturing processes.

- Growing demand for energy-efficient chips to extend battery life in electric autonomous vehicles.

AI Impact Analysis on Autonomou Car Chip

User questions related to the impact of AI on autonomous car chips predominantly revolve around how AI is transforming processing requirements, enabling new functionalities, and introducing complexities. There's significant curiosity about the types of AI algorithms being implemented (e.g., deep learning for perception, reinforcement learning for decision-making) and the specific hardware innovations (e.g., NPUs, AI accelerators) required to execute these algorithms efficiently at the edge. Users are keen to understand how AI influences chip design in terms of computational power, memory bandwidth, and low-latency processing, as these factors are critical for real-time autonomous operation.

Furthermore, concerns often arise regarding the computational demands and power consumption associated with complex AI models, directly impacting vehicle design and thermal management. The role of AI in improving sensor fusion accuracy, enabling predictive capabilities, and facilitating over-the-air (OTA) software updates is also a frequent area of interest. The underlying expectation is that AI will continue to push the boundaries of autonomous capabilities, requiring increasingly sophisticated and specialized chip designs that can handle vast amounts of data processing with unparalleled speed and accuracy while maintaining stringent safety standards.

- AI drives the need for specialized Neural Processing Units (NPUs) and AI accelerators within chips for efficient execution of machine learning algorithms.

- Enables advanced perception capabilities through deep learning for object detection, classification, and tracking from sensor data.

- Facilitates real-time decision-making and path planning by processing complex environmental data and predicting outcomes.

- Increases computational demand and bandwidth requirements, pushing the boundaries of chip performance and memory architecture.

- Contributes to the development of robust sensor fusion algorithms, integrating data from multiple sensor modalities for a comprehensive environmental model.

Key Takeaways Autonomou Car Chip Market Size & Forecast

Common user questions regarding key takeaways from the Autonomous Car Chip market size and forecast consistently point to the overwhelming growth potential and strategic importance of this sector within the broader automotive industry. Users are particularly interested in understanding the magnitude of growth, the primary factors driving it, and the long-term implications for vehicle manufacturing and urban mobility. The insights suggest a market poised for exponential expansion, fundamentally transforming how vehicles operate and interact with their environment, moving from driver-assisted to fully autonomous paradigms.

Another critical takeaway frequently sought by users is the identification of pivotal technological advancements and the competitive landscape. The market's forecast indicates that innovation in AI, high-performance computing, and specialized silicon will be central to achieving higher levels of autonomy. Furthermore, the increasing integration of software with hardware, leading to software-defined vehicles, represents a significant shift. The competitive environment is characterized by intense R&D efforts and strategic partnerships among semiconductor manufacturers, automotive OEMs, and software providers, all vying for leadership in this rapidly evolving domain.

- The Autonomous Car Chip Market is experiencing robust growth, driven by increasing adoption of ADAS and a clear roadmap towards higher autonomy levels.

- Technological advancements in AI, machine learning, and high-performance computing are crucial enablers for market expansion.

- The market's future is shaped by the imperative for functional safety, cybersecurity, and energy efficiency in chip design.

- Significant investment in research and development by semiconductor companies and automotive OEMs is a key characteristic of the market.

- The shift towards software-defined vehicles will continue to drive demand for flexible, powerful, and scalable chip architectures.

Autonomou Car Chip Market Drivers Analysis

The autonomous car chip market is primarily propelled by the escalating demand for advanced driver-assistance systems (ADAS) and the progressive evolution towards fully autonomous vehicles. As automotive manufacturers integrate more sophisticated features like adaptive cruise control, lane-keeping assist, and automatic emergency braking, the requirement for powerful and specialized processing units, sensors, and communication chips intensifies. These systems form the foundational building blocks for higher levels of autonomy, driving continuous innovation and demand in the semiconductor industry.

Furthermore, significant advancements in artificial intelligence (AI) and machine learning (ML) algorithms are fueling the market. AI is pivotal for real-time perception, decision-making, and sensor fusion, requiring dedicated AI accelerators and neural processing units (NPUs) within autonomous car chips. The increasing complexity of these AI models necessitates chips with higher computational power, improved energy efficiency, and low latency, thereby acting as a core driver for market expansion. Regulatory initiatives and increasing consumer awareness regarding vehicle safety also contribute significantly, pushing for the implementation of advanced safety features enabled by sophisticated chips.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of ADAS and Higher Autonomy Levels | +2.5% | Global | Short to Mid-term |

| Advancements in AI and Machine Learning Technologies | +2.0% | Global | Short to Mid-term |

| Strict Safety Regulations and Standards | +1.8% | North America, Europe, Asia Pacific | Mid-term |

| Growing Demand for Electric Vehicles and Their Digitalization | +1.5% | Global | Mid to Long-term |

| Investment in Smart City Infrastructure and V2X Communication | +1.2% | Asia Pacific, Europe | Long-term |

Autonomou Car Chip Market Restraints Analysis

Despite the robust growth trajectory, the autonomous car chip market faces several significant restraints that could impede its full potential. One primary challenge is the exceedingly high cost associated with the research and development, as well as the manufacturing, of these highly complex and specialized chips. Developing semiconductors that can meet the stringent functional safety (ISO 26262) and cybersecurity requirements of autonomous vehicles demands substantial investment in design, testing, and validation, making the barrier to entry quite high for new players and increasing the financial burden on existing ones.

Another major restraint involves the evolving and often fragmented regulatory and legal landscape across different regions. The absence of globally harmonized standards for autonomous vehicle deployment, liability, and data privacy creates uncertainties for manufacturers and chip designers. This regulatory ambiguity can slow down market adoption and complicate product development, as chips need to be adaptable to diverse legal frameworks. Furthermore, public acceptance and trust in autonomous technology remain a concern, influenced by safety incidents and ethical dilemmas, which can temper market growth by limiting consumer demand for high-level autonomous features.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development and Manufacturing Costs of Advanced Chips | +1.8% | Global | Short to Mid-term |

| Regulatory and Legal Uncertainties Across Regions | +1.5% | Global (varies by region) | Mid-term |

| Cybersecurity Threats and Data Privacy Concerns | +1.0% | Global | Ongoing |

| Public Acceptance and Trust Issues Regarding Autonomous Technology | +0.8% | North America, Europe | Mid to Long-term |

| Supply Chain Vulnerabilities and Geopolitical Tensions Affecting Chip Production | +0.7% | Global | Short-term (episodic) |

Autonomou Car Chip Market Opportunities Analysis

The autonomous car chip market presents a multitude of compelling opportunities for innovation and growth. A significant avenue lies in the continued development of domain-specific architectures, such as custom ASICs (Application-Specific Integrated Circuits) and highly optimized SoCs (System-on-Chips), specifically tailored for the unique computational demands of autonomous driving. These specialized chips offer superior performance and energy efficiency compared to general-purpose processors, creating a niche for companies capable of delivering highly integrated, purpose-built solutions for perception, planning, and control.

Another prominent opportunity stems from the industry's pivot towards software-defined vehicles (SDVs). This paradigm shift requires flexible, powerful, and updateable chip platforms that can support continuous software iterations and new functionalities over the vehicle's lifespan. Companies that can provide hardware platforms enabling seamless over-the-air (OTA) updates and modular software integration will gain a significant competitive advantage. Additionally, the expansion into commercial autonomous fleets, including robo-taxis, autonomous trucks, and delivery vehicles, represents a substantial market segment with high demand for robust and reliable autonomous chip solutions, distinct from consumer passenger vehicles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Domain-Specific Architectures (ASICs, SoCs) | +2.2% | Global | Mid to Long-term |

| Shift Towards Software-Defined Vehicle (SDV) Architectures | +2.0% | Global | Mid-term |

| Expansion into Commercial Autonomous Fleets (Trucking, Logistics) | +1.7% | North America, Europe, Asia Pacific | Mid to Long-term |

| Growth in V2X (Vehicle-to-Everything) Communication Integration | +1.3% | Asia Pacific, Europe | Long-term |

| Demand for Advanced Thermal Management Solutions for High-Performance Chips | +0.9% | Global | Mid-term |

Autonomou Car Chip Market Challenges Impact Analysis

The autonomous car chip market is confronted by complex technical and operational challenges that demand innovative solutions. One of the foremost challenges is achieving uncompromised functional safety and redundancy (ASIL D compliance) for autonomous driving systems. Chips must be designed to detect and mitigate faults in real-time, ensuring safe operation even in the event of hardware or software failures. This requires sophisticated fault-tolerant architectures, extensive verification, and validation processes, significantly increasing design complexity and development cycles.

Another critical challenge lies in managing the high power consumption and subsequent thermal dissipation of the powerful processors required for autonomous driving. Running complex AI models and processing vast amounts of sensor data in real-time generates substantial heat, which can degrade chip performance and reliability. Developing efficient cooling solutions and optimizing chip architectures for lower power consumption without compromising performance is a persistent hurdle. Furthermore, ensuring ultra-low latency and high data throughput for real-time decision-making, coupled with robust cybersecurity against potential threats, adds layers of complexity that require continuous innovation and industry-wide collaboration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Stringent Functional Safety (ASIL D) and Redundancy | +2.0% | Global | Ongoing |

| High Power Consumption and Thermal Management | +1.5% | Global | Ongoing |

| Real-time Data Processing and Ultra-Low Latency Requirements | +1.2% | Global | Ongoing |

| Complex Software Development, Integration, and Validation | +1.0% | Global | Ongoing |

| Interoperability and Lack of Standardization Across the Industry | +0.7% | Global | Mid to Long-term |

Autonomou Car Chip Market - Updated Report Scope

This market research report provides an in-depth analysis of the Autonomous Car Chip market, encompassing market size, segmentation, regional dynamics, competitive landscape, and future growth prospects. It offers a comprehensive overview of the market's evolution, highlighting key drivers, restraints, opportunities, and challenges that will shape its trajectory from 2025 to 2033. The report delves into the intricate technical aspects of autonomous car chips, including various component types, levels of autonomy supported, and diverse applications within the automotive sector, delivering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 165.7 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NVIDIA, Intel (Mobileye), Qualcomm, NXP Semiconductors, Renesas Electronics Corporation, Infineon Technologies AG, Texas Instruments Incorporated, STMicroelectronics, Samsung Electronics Co., Ltd., Analog Devices Inc., Toshiba Corporation, Micron Technology, Inc., Xilinx (AMD), Bosch, Continental AG, ZF Friedrichshafen AG, Aptiv PLC, Magna International Inc., Valeo S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The autonomous car chip market is comprehensively segmented to provide a detailed understanding of its diverse components, applications, and technological progression. This segmentation allows for granular analysis of market dynamics, identifying specific growth areas and technological imperatives. Key segments include chips categorized by their core function (e.g., processors, sensors, memory), the level of autonomous driving they enable (from L1 to L5), their specific application within the vehicle (e.g., ADAS, infotainment), and the type of vehicle they are integrated into (passenger or commercial).

Each segment represents a distinct facet of the autonomous driving ecosystem, influencing design considerations, performance requirements, and market demand. For instance, chips for L5 full autonomy demand significantly higher processing power, redundancy, and functional safety compared to those used in L1 driver assistance systems. Similarly, the requirements for sensor chips (Lidar, Radar, Camera) vary based on their role in environmental perception, while memory and communication modules are critical for data handling and vehicle-to-everything (V2X) connectivity. Understanding these interdependencies is crucial for market participants to strategize effectively.

- By Component:

- Processors (CPUs, GPUs, ASICs, FPGAs, NPUs)

- Sensors (Lidar, Radar, Camera, Ultrasonic)

- Memory (DRAM, NAND)

- Communication Modules (V2X, 5G)

- Power Management ICs

- Other Components

- By Autonomy Level:

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- By Application:

- ADAS (Adaptive Cruise Control, Lane Keeping Assist, Park Assist, Automatic Emergency Braking)

- Infotainment Systems

- Body Electronics

- Powertrain Systems

- Safety & Security Systems

- Other Automotive Applications

- By Vehicle Type:

- Passenger Vehicles

- Commercial Vehicles (Trucks, Buses, Robo-taxis)

Regional Highlights

- North America: This region is a leading market for autonomous car chips, characterized by significant investment in R&D by major technology companies and automotive OEMs. The presence of numerous autonomous vehicle testing programs and strong regulatory support for advanced safety features drives high demand for sophisticated chips. Early adoption of autonomous technologies in ride-sharing and logistics also contributes to market growth.

- Europe: Europe exhibits robust growth driven by its well-established automotive industry and stringent safety regulations. There is a strong emphasis on achieving high levels of functional safety and cybersecurity in chip design. Government initiatives promoting smart mobility and a push towards sustainable transportation solutions, including electric autonomous vehicles, further stimulate market expansion.

- Asia Pacific (APAC): The Asia Pacific region is anticipated to be the largest and fastest-growing market, primarily due to large automotive production volumes, increasing consumer demand for advanced vehicles, and strong government support for autonomous driving initiatives, particularly in China, Japan, and South Korea. Rapid urbanization, infrastructure development for smart cities, and significant investments in 5G networks and V2X technologies are key drivers.

- Latin America: This region represents an emerging market for autonomous car chips. Growth is expected to be gradual, influenced by economic stability, infrastructure development, and the adoption pace of ADAS features in new vehicle sales. Collaboration with international players and favorable government policies could accelerate market penetration.

- Middle East and Africa (MEA): The MEA region is in its nascent stages of autonomous vehicle adoption, with growth primarily concentrated in technologically progressive cities like Dubai and Riyadh. Government visions for smart cities and diversification of economies are slowly paving the way for autonomous mobility trials, driving future demand for car chips, though widespread adoption faces infrastructure and regulatory challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Autonomou Car Chip Market.- NVIDIA

- Intel (Mobileye)

- Qualcomm

- NXP Semiconductors

- Renesas Electronics Corporation

- Infineon Technologies AG

- Texas Instruments Incorporated

- STMicroelectronics

- Samsung Electronics Co., Ltd.

- Analog Devices Inc.

- Toshiba Corporation

- Micron Technology, Inc.

- Xilinx (AMD)

- Bosch

- Continental AG

- ZF Friedrichshafen AG

- Aptiv PLC

- Magna International Inc.

- Valeo S.A.

Frequently Asked Questions

What are the primary types of chips used in autonomous vehicles?

Autonomous vehicles rely on a diverse range of specialized chips, including high-performance processors like CPUs, GPUs, and ASICs for complex computations and AI tasks; FPGAs for prototyping and flexible computing; and NPUs specifically for neural network processing. Additionally, they incorporate various sensor chips for Lidar, Radar, and cameras, along with memory chips (DRAM, NAND), and communication modules (5G, V2X) for data handling and connectivity.

How does AI specifically enhance autonomous car chip functionality?

AI significantly enhances autonomous car chip functionality by enabling advanced perception, decision-making, and prediction capabilities. AI algorithms, particularly deep learning, allow chips to accurately interpret sensor data (from cameras, lidar, radar) for object detection, classification, and tracking. Specialized AI accelerators within chips process these algorithms efficiently in real-time, crucial for path planning, behavioral prediction of other road users, and ensuring safe autonomous operation.

What are the main challenges in developing autonomous car chips?

Key challenges in developing autonomous car chips include achieving stringent functional safety standards (e.g., ASIL D) and ensuring redundancy for fail-operational systems. Other significant hurdles are managing high power consumption and thermal dissipation from powerful processors, ensuring ultra-low latency for real-time decision-making, and addressing complex software development, validation, and cybersecurity threats. The lack of standardized interoperability across the industry also poses a significant challenge.

Which regions are leading the market for autonomous car chips?

North America, Europe, and Asia Pacific are the leading regions in the autonomous car chip market. North America benefits from extensive R&D and early adoption. Europe is strong due to its established automotive industry and focus on safety. Asia Pacific, particularly China, Japan, and South Korea, is projected to be the largest and fastest-growing market, driven by high production volumes, government support, and smart city initiatives.

What are the future trends shaping the autonomous car chip market?

Future trends shaping the autonomous car chip market include a continued shift towards highly integrated, domain-specific SoCs and ASICs for optimized performance and energy efficiency. The rise of software-defined vehicle architectures will demand more flexible and upgradable chip platforms. Additionally, increasing integration of AI accelerators, advancements in sensor fusion technologies, emphasis on end-to-end functional safety, and the expansion into commercial autonomous fleets are key future directions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted